Market Overview

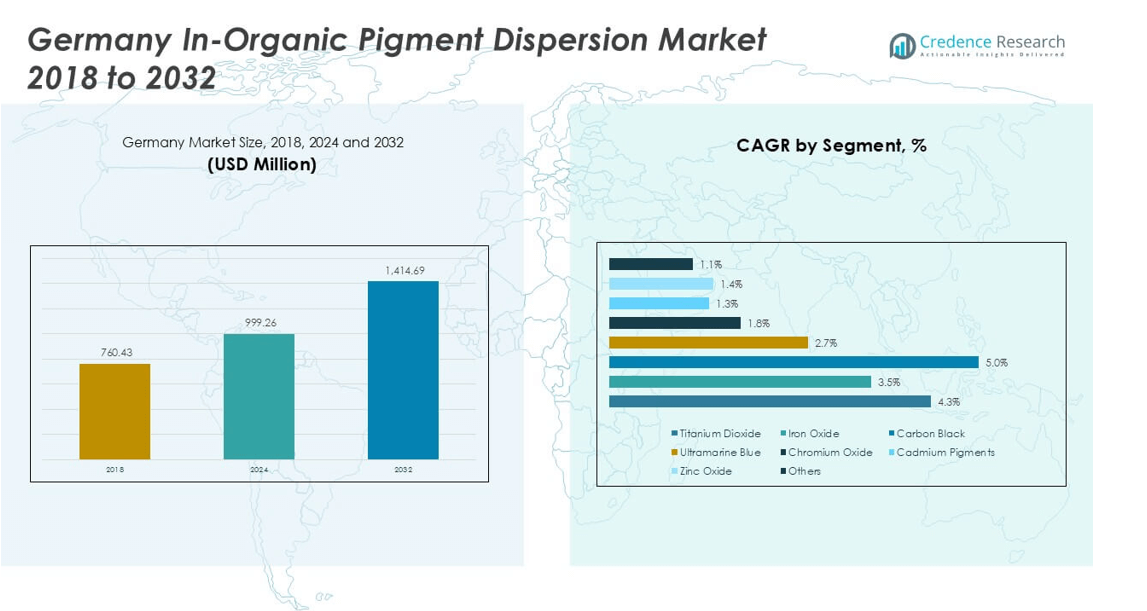

Germany In-Organic Pigment Dispersion market size was valued at USD 760.43 million in 2018, increased to USD 999.26 million in 2024, and is anticipated to reach USD 1,414.69 million by 2032, at a CAGR of 4.36% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Germany In-Organic Pigment Dispersion Market Size 2024 |

USD 999.26 million |

| Germany In-Organic Pigment Dispersion Market, CAGR |

4.36% |

| Germany In-Organic Pigment Dispersion Market Size 2032 |

USD 1,414.69million |

The Germany in-organic pigment dispersion market is led by BASF SE, Clariant AG, Heubach GmbH, Lanxess AG, and Venator Materials PLC, with strong contributions from Cabot Corporation, Ferro Corporation, DIC Corporation, Sudarshan Chemical Industries, Huntsman Corporation, and Chromaflo. These companies dominate through extensive product portfolios, advanced manufacturing facilities, and compliance with EU environmental standards. South Germany holds the largest share at 32%, driven by its concentration of automotive, chemical, and plastics industries. North Germany follows with 28%, supported by its port infrastructure and coatings demand, while West Germany and East Germany account for 22% and 18%, respectively.

Market Insights

- The Germany in-organic pigment dispersion market was valued at USD 999.26 million in 2024 and is projected to reach USD 1,414.69 million by 2032, growing at a CAGR of 4.36%.

- Strong demand from paints & coatings and plastics drives growth, supported by infrastructure development, automotive coatings, and packaging applications that require high opacity, color stability, and UV resistance.

- Sustainable and low-VOC pigment dispersions are gaining popularity as EU Green Deal and REACH regulations push manufacturers toward eco-friendly solutions, creating opportunities for advanced dispersion technologies.

- The market is moderately consolidated with BASF SE, Clariant AG, Heubach GmbH, Lanxess AG, and Venator Materials PLC leading through R&D investments, product innovations, and expansions to strengthen domestic supply capabilities.

- South Germany holds 32% share, followed by North Germany with 28%, West Germany at 22%, and East Germany with 18%; titanium dioxide dominates pigment type segment, followed by iron oxide and carbon black.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Pigment Type

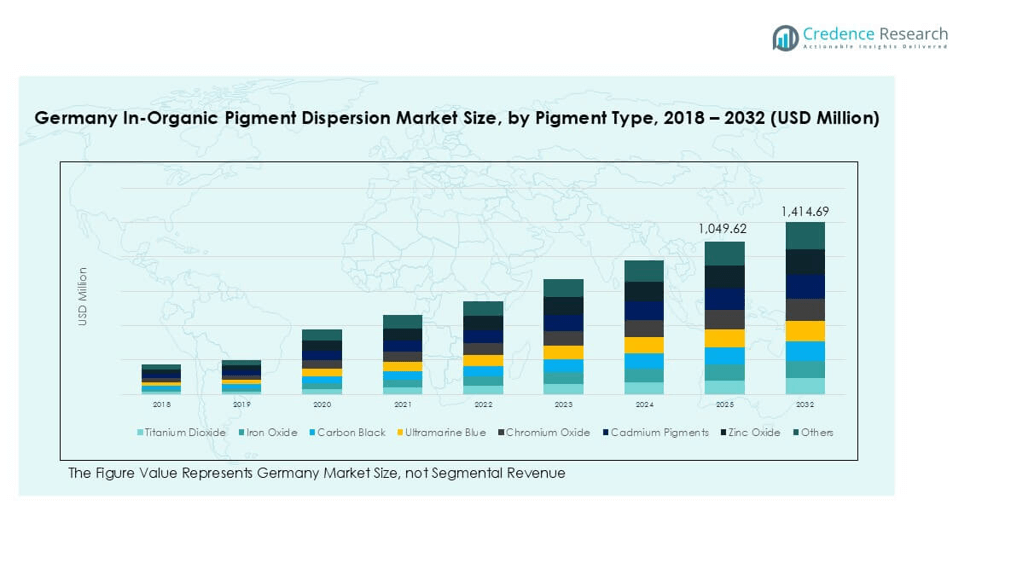

Titanium dioxide led the Germany in-organic pigment dispersion market, capturing over 35% share in 2024. Its dominance comes from its high opacity, brightness, and excellent UV resistance, making it a preferred choice in paints, coatings, and plastics. Iron oxide followed, driven by its color stability and use in construction materials and decorative coatings. Carbon black held a significant share due to its applications in automotive plastics and inks. Ultramarine blue, chromium oxide, cadmium pigments, and zinc oxide serve niche applications, mainly in ceramics, cosmetics, and specialty coatings, supporting growth through demand for vibrant, durable colors.

- For instance, Kronos Worldwide operates a titanium dioxide production capacity of 556,000 metric tons per year, with major facilities in Germany supporting European demand.

By Application

Paints & coatings dominated the market, accounting for over 40% share in 2024, supported by strong demand from the construction and automotive industries. The segment benefits from titanium dioxide’s high-performance dispersion properties, which improve coverage and durability. Printing inks form the second-largest segment, supported by demand from packaging and publishing industries. Plastics follow closely, boosted by automotive lightweighting and consumer goods production. Construction materials, ceramics and glass, and cosmetics represent steady growth areas, driven by infrastructure projects, architectural finishes, and rising use of high-quality pigments in personal care products.

- For instance, BASF Coatings GmbH operates a Münster plant capable of producing more than 300,000 metric tons of automotive coatings annually, supplying major OEMs.

Market Overview

Rising Demand from Paints & Coatings

The paints & coatings industry drives strong demand for in-organic pigment dispersions in Germany, holding the largest application share. Titanium dioxide and iron oxide are widely used to improve opacity, UV resistance, and color stability. Growth is fueled by infrastructure development, renovation projects, and automotive coatings that require high-performance pigments. Environmental regulations also push manufacturers toward dispersions with better dispersion quality and reduced VOC emissions, further boosting market adoption.

- For instance, Evonik Industries operates a large multi-user chemical site in Antwerp, which manufactures products such as methionine for animal feed and crosslinkers for coatings. Evonik sold its conventional titanium dioxide pigment business in 2011.

Expansion in Plastics and Packaging

Plastics remain a significant growth driver, supported by Germany’s thriving automotive and consumer goods sectors. Pigment dispersions such as carbon black and titanium dioxide are used in polymers to enhance color consistency, heat stability, and UV protection. Demand is also increasing in food and industrial packaging where color precision and compliance with EU safety regulations are critical. Lightweight plastics with improved aesthetics and durability are boosting consumption of dispersions, particularly in injection-molded parts and flexible packaging applications.

- For instance, Orion Engineered Carbons maintains European carbon black capacity exceeding 200,000 metric tons annually, serving automotive plastics manufacturers.

Growth in Construction and Industrial Applications

Germany’s construction sector is fueling demand for pigment dispersions in concrete, tiles, and decorative materials. Iron oxide pigments dominate this segment due to their strong weather resistance, high tinting strength, and cost-effectiveness. Increasing investment in infrastructure modernization, public housing, and commercial spaces supports consistent consumption. Industrial coatings and powder coatings also benefit from inorganic pigments for their heat resistance and long-term color stability, making them preferred choices for machinery, equipment, and metal parts.

Key Trends & Opportunities

Shift Toward Sustainable Pigments

Manufacturers are developing eco-friendly pigment dispersions to comply with REACH and EU Green Deal targets. Low-VOC, heavy-metal-free, and recyclable dispersions are gaining traction across paints, inks, and packaging sectors. Companies are investing in bio-based dispersions and advanced wetting agents to improve efficiency and reduce environmental footprint. This shift creates opportunities for suppliers offering sustainable solutions while maintaining performance standards required by industries like automotive and construction.

- For instance, Clariant introduced its EcoTain® range of sustainable pigment preparations, with over 200 products certified for reduced environmental impact.

Rising Adoption of Advanced Dispersion Technologies

Technological advancements in milling and wet dispersion techniques are improving product quality and consistency. Nano-dispersion technologies enhance opacity, brightness, and color strength while lowering pigment consumption. German manufacturers are also adopting automated production systems to ensure uniformity and reduce waste. These innovations present opportunities for premium-grade dispersions used in high-end coatings, plastics, and specialty inks where superior performance and aesthetics are critical.

- For instance, Venator Materials developed TiO2 products with particle sizes below 300 nanometers, reducing formulation requirements by up to 15%.

Key Challenges

Volatility in Raw Material Prices

Price fluctuations of raw materials such as titanium dioxide and iron oxides create uncertainty for manufacturers. Rising energy costs in Germany also add to production expenses, affecting profit margins. Suppliers often face difficulty passing these costs on to end-users, leading to margin pressure. This volatility challenges smaller players and drives the need for long-term sourcing strategies and supply chain resilience.

Stringent Environmental Regulations

Compliance with strict EU and German environmental regulations can be costly and time-intensive. Producers must continuously invest in cleaner technologies and formulations free from hazardous substances like cadmium and chromium VI. Meeting these standards without compromising pigment quality increases R&D costs. This challenge is particularly significant for smaller producers with limited resources, potentially slowing innovation and market competitiveness.

Regional Analysis

North Germany

North Germany accounted for nearly 28% market share in 2024, supported by its strong industrial base and port-driven trade infrastructure. Hamburg and Bremen play key roles in importing raw materials and exporting pigment-based products to Northern Europe. The region sees high demand from paints & coatings, driven by construction, shipbuilding, and industrial coatings applications. Growth is also supported by increasing investments in eco-friendly coatings that meet EU environmental standards. Rising automotive component production and packaging industries in Lower Saxony further contribute to steady pigment consumption, keeping the region a key contributor to Germany’s overall pigment dispersion market.

South Germany

South Germany led the market with 32% share in 2024, driven by its concentration of automotive, plastics, and chemical manufacturing hubs. Bavaria and Baden-Württemberg host major automotive OEMs and suppliers, creating strong demand for pigment dispersions in coatings, plastics, and high-performance materials. The construction sector in Munich and Stuttgart further supports consumption, particularly for iron oxide pigments used in tiles, concrete, and decorative finishes. The region also benefits from advanced R&D facilities and innovation centers, which encourage the adoption of sustainable, high-performance dispersions aligned with EU regulatory standards, cementing its position as the dominant regional market in Germany.

East Germany

East Germany represented around 18% market share in 2024, with demand driven by construction materials, ceramics, and infrastructure projects. Cities like Leipzig and Dresden are experiencing industrial growth, leading to increased consumption of iron oxide and titanium dioxide dispersions. Government-led infrastructure modernization programs support steady demand for pigment dispersions in architectural coatings and road markings. The region also has a growing plastics and packaging manufacturing base, which uses carbon black and zinc oxide dispersions for color stability and UV protection. Although smaller compared to other regions, East Germany is witnessing consistent growth supported by manufacturing expansion and investments.

West Germany

West Germany held close to 22% market share in 2024, supported by a well-developed industrial and logistics network. The region is home to several chemical production facilities and pigment manufacturers that supply to domestic and export markets. Demand is strong from printing inks, packaging, and specialty coatings, driven by the presence of consumer goods and publishing industries. Cities like Cologne and Düsseldorf also contribute through construction activities and infrastructure upgrades that require high-performance coating solutions. The region’s strategic location near Benelux countries and France enhances cross-border trade, supporting stable market growth for pigment dispersions in multiple end-use applications.

Market Segmentations:

By Pigment Type

- Titanium Dioxide

- Iron Oxide

- Carbon Black

- Ultramarine Blue

- Chromium Oxide

- Cadmium Pigments

- Zinc Oxide

- Others

By Application

- Paints & Coatings

- Printing Inks

- Plastics

- Construction Materials

- Ceramics and Glass

- Cosmetics

- Others

By Geography

- North Germany

- South Germany

- East Germany

- West Germany

Competitive Landscape

The Germany in-organic pigment dispersion market is moderately consolidated, with major players including BASF SE, Clariant AG, Heubach GmbH, Lanxess AG, Venator Materials PLC, Cabot Corporation, Ferro Corporation, DIC Corporation, Sudarshan Chemical Industries, Huntsman Corporation, and Chromaflo. BASF SE and Clariant AG lead the market with extensive product portfolios and strong domestic manufacturing bases, focusing on high-performance titanium dioxide and iron oxide dispersions. Heubach GmbH and Lanxess AG specialize in sustainable pigment solutions, aligning with EU environmental regulations. Venator and Cabot provide innovative carbon black and specialty dispersions for plastics and coatings. Companies are emphasizing R&D investments, mergers, and capacity expansions to strengthen regional presence and meet demand from construction, automotive, and packaging sectors. Competitive strategies also include developing low-VOC and heavy-metal-free formulations to address regulatory requirements and growing preference for eco-friendly, high-performance pigment solutions across multiple industries in Germany.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- BASF SE

- Clariant AG

- Heubach GmbH

- Lanxess AG

- Venator Materials PLC

- Cabot Corporation

- Ferro Corporation

- DIC Corporation

- Sudarshan Chemical Industries

- Huntsman Corporation

- Chromaflo

Recent Developments

- In March 2025, Sudarshan Chemical Industries Limited (SCIL) completed its acquisition of the Heubach Group, establishing a global pigment leader with operations across 19 sites worldwide. The combined company will offer a wide, technologically advanced pigment portfolio and strengthen its presence in key markets like Europe and the Americas.

- In January 2023, BASF announced an investment to expand its polymer dispersions production capacity at its Merak site in Indonesia. The expansion aimed to meet the rising demand for styrene-butadiene and acrylic dispersions, driven by the growth of new paper mills and the high-quality packaging sector across Southeast Asia, Australia, and New Zealand. The Merak site, strategically located near key raw material suppliers and customers, played a vital role in supporting this regional demand.

- In January 2023, Cabot Corporation expanded its inkjet production facility in Haverhill, Massachusetts, to meet growing demand for digital printing applications. The expansion will increase capacity for aqueous inkjet dispersions, which support the shift from analog to digital printing by offering benefits like greater design customization, faster speed to market, and improved sustainability through reduced waste. Recent upgrades at the facility also include enhanced manufacturing equipment and processes that improve operational efficiency and reduce water usage. This investment positions Cabot to better serve the rapidly evolving inkjet market with a broader product portfolio and reliable global supply.

Report Coverage

The research report offers an in-depth analysis based on Pigment Type, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for titanium dioxide dispersions will remain strong, driven by coatings and plastics growth.

- Sustainable and heavy-metal-free pigments will see faster adoption due to EU regulations.

- Advanced nano-dispersion technologies will improve color strength and reduce pigment consumption.

- Construction sector recovery will boost iron oxide pigment demand for decorative materials.

- Automotive lightweighting trends will increase carbon black usage in plastic components.

- Printing inks will gain from growth in flexible and sustainable packaging solutions.

- R&D investments will focus on low-VOC and energy-efficient pigment dispersion processes.

- South Germany will continue leading, supported by automotive and chemical production hubs.

- Strategic mergers and capacity expansions will strengthen domestic supply and reduce imports.

- Growing demand from cosmetics and personal care will open opportunities for niche pigment solutions.