Market Overview

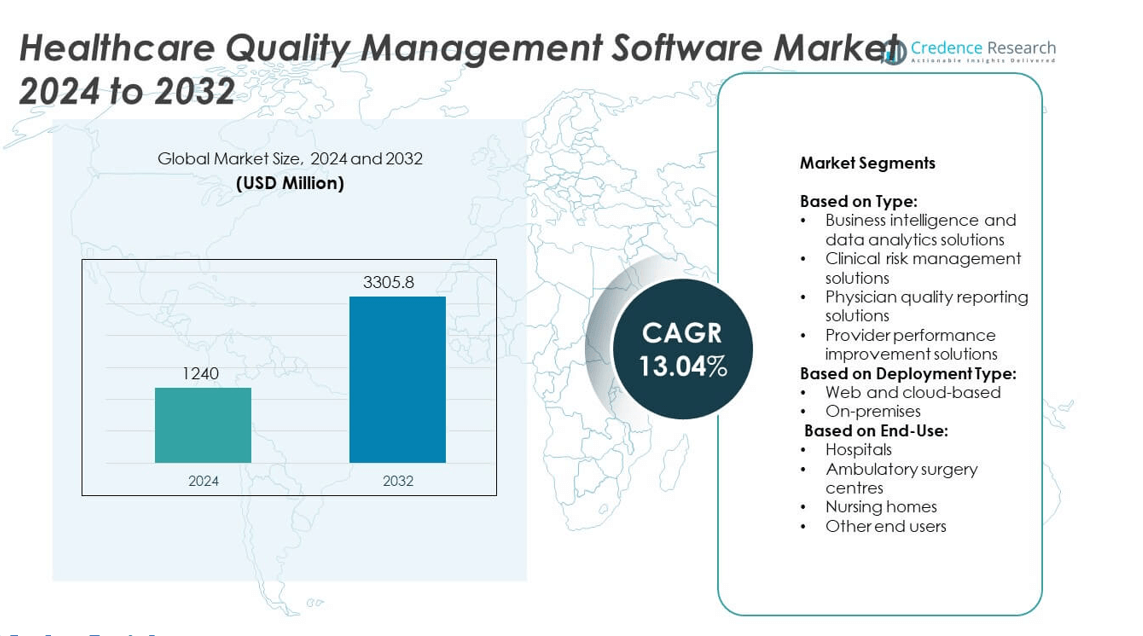

Healthcare Quality Management Software Market size was valued at USD 1240 million in 2024 and is anticipated to reach USD 3305.8 million by 2032, at a CAGR of 13.04% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Healthcare Quality Management Software Market Size 2024 |

USD 1240 million |

| Healthcare Quality Management Software Market, CAGR |

13.04% |

| Healthcare Quality Management Software Market Size 2032 |

USD 3305.8 million |

The Healthcare Quality Management Software market grows due to rising demand for error reduction, regulatory compliance, and real-time data monitoring. Hospitals adopt advanced tools to improve care outcomes and support value-based care models. AI-driven analytics and cloud-based platforms enhance performance tracking and decision-making. Integration with EHRs and scalable deployment options attract both large and mid-sized providers. Vendors focus on predictive insights, automation, and interoperability to meet evolving healthcare needs and improve operational efficiency across clinical and administrative workflows.

North America leads the Healthcare Quality Management Software market due to strong digital health adoption and regulatory mandates. Europe follows with growing demand for performance tracking and patient safety tools. Asia-Pacific shows rapid growth with rising healthcare investments and infrastructure development. Latin America and the Middle East & Africa see steady adoption in urban hospitals. Key players operating in this market include Veeva Systems, Sparta Systems, HealthStream, and Ideagen, each offering specialized solutions to support quality and compliance goals.

Market Insights

- The Healthcare Quality Management Software market was valued at USD 1240 million in 2024 and is projected to reach USD 3305.8 million by 2032, growing at a CAGR of 13.04%.

- Demand for error reduction, clinical compliance, and patient safety boosts software adoption across hospitals and clinics.

- AI-driven analytics, real-time performance monitoring, and cloud-based deployments are major trends shaping the market.

- Key players such as Veeva Systems, Sparta Systems, HealthStream, and Ideagen invest in scalable, integrated, and secure platforms.

- High initial costs, limited IT infrastructure, and privacy concerns create barriers for small and mid-sized healthcare providers.

- North America leads the market, followed by Europe and Asia-Pacific, due to strong digital health initiatives and quality mandates.

- Vendors compete by offering modular tools, EHR integration, multilingual features, and regulatory-ready solutions for global expansion.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Demand for Error Reduction and Compliance in Clinical Workflows

Healthcare providers aim to reduce medical errors and meet regulatory standards. Electronic systems improve data tracking and ensure clinical safety. Government mandates such as MACRA and HIPAA push hospitals toward digital quality management. Real-time analytics and alerts help staff take quick action during patient care. Healthcare Quality Management Software market gains from demand for accuracy and accountability. It improves patient outcomes and supports audit trails. The system aligns hospitals with national and international compliance standards.

- For instance, before its acquisition by Oracle in June 2022, Cerner Corporation’s products were reportedly used by over 27,000 healthcare facilities worldwide. Since the acquisition, the combined entity, known as Oracle Health, has faced significant challenges. Public reports from 2023 onwards, particularly from KLAS Research, highlighted shrinking market share, growing customer dissatisfaction, and struggles with major implementations like the U.S. Department of Veterans Affairs’ EHR rollout

Expanding Role of Data Analytics in Healthcare Decision-Making

Hospitals rely more on data-driven tools to improve performance and patient safety. These systems offer insights on care quality, staff productivity, and resource use. They help identify underperforming departments and guide process changes. The Healthcare Quality Management Software market benefits from strong focus on measurable outcomes. It supports benchmarking and scorecards that aid in continuous improvement. Integration with business intelligence tools makes these platforms more valuable. Leaders use the insights to guide training and operational plans.

- For instance, Nuance Communications (a Microsoft company) reported that its AI-powered solutions, including speech recognition and ambient intelligence technologies, process hundreds of millions of patient encounters annually, capturing “300 million patient stories each year” through its voice-powered platform.

Increasing Healthcare Spending Across Public and Private Sectors

Rising healthcare investments boost IT system upgrades across hospitals, clinics, and diagnostic labs. Budget allocation shifts toward quality improvement and digital transformation. Stakeholders seek long-term cost savings by reducing inefficiencies. The Healthcare Quality Management Software market responds to this shift with scalable solutions. It supports both large networks and small clinics with tailored offerings. Public programs and private insurance firms encourage quality-linked reimbursements. That shift increases demand for accurate performance tracking.

Growing Need for Centralized Quality Monitoring Systems

Healthcare providers operate across multiple locations and service lines. They require centralized platforms to standardize care delivery and track metrics. Fragmented systems lead to data silos and poor visibility. The Healthcare Quality Management Software market addresses this gap through integrated dashboards. It enables cross-department collaboration and data consolidation. Central control helps hospitals act faster on critical safety issues. Standard tools ensure better alignment between clinical goals and operational performance.

Market Trends

Adoption of AI-Powered Analytics for Real-Time Quality Insights

Healthcare facilities adopt artificial intelligence tools to detect patterns and prevent care gaps. These tools process vast data sets to flag safety risks and quality issues. Real-time feedback improves clinical decisions and reduces time delays in reporting. The Healthcare Quality Management Software market integrates AI to offer predictive and prescriptive insights. It helps administrators take timely actions and reduce human errors. Hospitals rely on automated scoring models to assess care delivery. The trend reflects a shift toward precision and speed in performance management.

- For instance, TeleTracking’s cloud-based systems are used in various UK hospitals and NHS Trusts, employing electronic wristbands and central control rooms for real-time patient tracking. This technology has demonstrably led to faster patient turnaround times. For example, Maidstone and Tunbridge Wells NHS Trust reported annual savings of £2.1 million from efficiencies gained through its use

Growth in Cloud-Based Quality Management Platforms

Cloud deployment models gain traction due to lower costs and easier scalability. Hospitals prefer subscription-based tools with minimal setup time. Cloud platforms ensure data accessibility across locations and departments. The Healthcare Quality Management Software market reflects this shift through web-based offerings. It supports fast updates, remote access, and reduced hardware needs. Security upgrades and compliance tools strengthen trust in these platforms. Providers use cloud tools to monitor multiple facilities from centralized control rooms.

- For instance, Philips deployed an AI-enabled clinical platform with Vestre Viken Health Trust. The platform now assists radiologists in diagnosing bone fractures for about 500 000 patients across 22 municipalities.

Integration of Quality Systems with Broader Healthcare IT Ecosystems

Hospitals seek seamless connection between EHRs, ERP systems, and quality tools. They require unified data flows to track performance without duplication. Integration improves visibility across financial, clinical, and operational processes. The Healthcare Quality Management Software market evolves to support open APIs and interoperability. It ensures smoother coordination across care teams and departments. Vendors focus on integration features that support clinical workflow continuity. The goal is a connected infrastructure that improves response times and decision accuracy.

Rising Emphasis on Patient-Centered Outcome Tracking

Healthcare providers shift focus to value-based care and patient experience. Outcome metrics now include satisfaction scores, readmission rates, and recovery timelines. Hospitals use quality tools to link interventions with patient-reported results. The Healthcare Quality Management Software market supports this trend through customizable dashboards. It enables tracking of both clinical outcomes and patient engagement. The approach builds transparency and strengthens provider-patient relationships. Quality tools become central to achieving value and trust in care delivery.

Market Challenges Analysis

High Implementation Costs and Limited IT Infrastructure in Small Healthcare Facilities

Smaller clinics and rural hospitals face challenges due to high initial software costs. These facilities lack advanced IT infrastructure and skilled personnel. Many providers struggle with integrating quality tools into legacy systems. The Healthcare Quality Management Software market feels pressure from demand for cost-effective options. It must offer flexible pricing models and simpler deployment methods. High customization and training costs create barriers for widespread adoption. Vendors must address these gaps to reach underserved segments.

Data Privacy Concerns and Regulatory Complexities Across Regions

Hospitals handle sensitive patient records that require strict data protection. Frequent changes in regional data laws create compliance challenges for software providers. Cross-border data transfers often involve legal and technical risks. The Healthcare Quality Management Software market must ensure full compliance with HIPAA, GDPR, and similar rules. It faces the task of securing data while enabling access across multiple systems. Failing to meet privacy standards can lead to legal penalties and reputational harm. Trust in digital tools depends on their ability to meet evolving regulatory demands.

Market Opportunities

Expansion into Emerging Markets with Rising Healthcare Digitization

Healthcare systems in Asia-Pacific, Latin America, and the Middle East increase investment in digital health tools. Governments fund programs to improve care quality and patient safety. Hospitals seek modern software to track performance and meet global standards. The Healthcare Quality Management Software market sees strong potential in these regions. It can offer cloud-based, low-maintenance solutions to meet local infrastructure limits. Vendors that localize tools and support regional languages gain faster entry. Demand grows for systems that align with public health goals and improve clinical workflows.

Rising Focus on Value-Based Care Creates Demand for Advanced Quality Metrics

Payers shift reimbursement models toward outcomes-based contracts and quality-linked incentives. Hospitals need tools to measure results, reduce costs, and boost patient satisfaction. This creates room for advanced software that offers real-time benchmarking and root cause analysis. The Healthcare Quality Management Software market benefits from this shift in care priorities. It can offer solutions that track clinical outcomes, safety incidents, and patient feedback on a single platform. Vendors that support regulatory reporting and scorecard generation gain competitive edge. These tools become essential for financial performance and compliance tracking.

Market Segmentation Analysis:

By Type:

Business intelligence and data analytics solutions hold a major share due to rising demand for data-driven decision-making. Hospitals use these tools to monitor care quality, improve safety, and streamline workflows. Clinical risk management solutions follow closely, as healthcare providers aim to prevent errors and minimize legal risks. Physician quality reporting solutions support providers in meeting regulatory requirements and performance tracking. Provider performance improvement solutions gain attention for enabling benchmarking and internal audits. The Healthcare Quality Management Software market offers these types to address diverse operational and compliance needs.

- For instance, before its 2015 acquisition by Aptean, Medworxx was a provider of health IT solutions and served over 400 hospitals across Canada, the U.S., UK, and France with patient flow dashboards. The company’s products and client base were integrated into Aptean’s portfolio, and any reference to Medworxx as an independent provider of these services is now outdated.

By Deployment Type:

Web and cloud-based platforms dominate the market. Hospitals and clinics prefer cloud models for their low upfront costs and easier scalability. These platforms offer centralized access, regular updates, and improved collaboration across departments. On-premises systems still serve large hospitals that prioritize data control and system customization. It supports offline access and internal hosting where security rules require tighter control. Vendors balance both models to meet the varied infrastructure needs of global healthcare settings.

- For instance, the Surat Municipal Corporation’s new HMIS processed 89,119 patients across multiple hospitals and centers.

By End-Use:

Hospitals remain the largest adopters of quality management tools. Their complex systems, large staff base, and regulatory exposure drive demand for advanced software. Ambulatory surgery centers use quality systems to manage risks and ensure procedural consistency. Nursing homes apply these tools to monitor care standards, resident safety, and compliance audits. Other end users such as diagnostic labs and specialty clinics also adopt basic modules to meet quality benchmarks. The Healthcare Quality Management Software market caters to each segment with tailored solutions that align with operational scale and care focus.

Segments:

Based on Type:

- Business intelligence and data analytics solutions

- Clinical risk management solutions

- Physician quality reporting solutions

- Provider performance improvement solutions

Based on Deployment Type:

- Web and cloud-based

- On-premises

Based on End-Use:

- Hospitals

- Ambulatory surgery centres

- Nursing homes

- Other end users

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America holds the highest share in the Healthcare Quality Management Software market, accounting for 38.7% of global revenue in 2024. The region benefits from a mature healthcare IT ecosystem, widespread adoption of electronic health records (EHRs), and strong regulatory frameworks. The presence of large healthcare providers and government-backed value-based care models drive demand for advanced quality management tools. The United States leads with widespread enforcement of Medicare quality reporting programs, encouraging adoption among hospitals and physician groups. Canada follows with growing use of performance monitoring solutions across public health systems. Companies in this region focus on offering integrated platforms that align with federal standards such as HIPAA and MACRA. Cloud-based deployments and AI-enabled analytics are in high demand across large health systems and specialty networks.

Europe

Europe captures a significant share of 26.4% in the global Healthcare Quality Management Software market. Countries such as Germany, the United Kingdom, and France adopt these tools to improve patient safety, reduce errors, and support clinical governance. The European Union’s strict regulatory environment pushes healthcare providers toward systematic performance monitoring. National healthcare systems invest in centralized quality monitoring platforms for hospitals and outpatient clinics. Digital health transformation strategies under the EU4Health programme further expand software adoption. Hospitals seek real-time data integration between EHRs, quality systems, and administrative platforms. Vendors target the market with GDPR-compliant solutions that support multilingual and regional customization for effective deployment.

Asia-Pacific

Asia-Pacific holds a market share of 18.3%, driven by healthcare digitization and expanding hospital networks. Countries such as China, India, Japan, and Australia invest in IT infrastructure to enhance patient safety and operational efficiency. Rapid growth in urban hospitals and medical tourism hubs increases the need for quality control systems. Governments implement national health programs to standardize care outcomes and improve accountability. Cloud-based tools gain traction due to limited on-site infrastructure in rural areas. Local and global vendors offer simplified, low-cost solutions tailored to mid-sized hospitals and clinics. The region shows rising interest in outcome tracking, infection control, and physician reporting modules.

Latin America

Latin America contributes 9.1% to the global Healthcare Quality Management Software market. Brazil, Mexico, and Argentina drive regional growth through healthcare reforms and hospital accreditation efforts. Public-private partnerships in healthcare IT create new opportunities for vendors. Hospitals and clinics aim to improve performance metrics to align with global benchmarks. Adoption remains higher in urban hospitals with digital record systems and accreditation goals. Cost-sensitive buyers prefer modular systems that allow stepwise implementation. Regulatory requirements around infection control and patient rights support steady demand for quality-focused solutions.

Middle East and Africa

The Middle East and Africa represent a smaller yet growing share of 7.5% in the Healthcare Quality Management Software market. Gulf countries such as the UAE and Saudi Arabia lead adoption with large-scale investments in hospital digitization. Governments launch national eHealth initiatives to improve transparency and care standards. Public and private providers use quality management tools to support accreditation, incident tracking, and service benchmarking. In Africa, adoption remains limited to larger hospitals in countries like South Africa and Nigeria. Vendors face infrastructure and connectivity challenges but explore partnerships with NGOs and health ministries. Demand is rising for mobile-accessible, multilingual platforms suited for low-resource settings.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Sparta Systems

- MorCare

- Veeva Systems

- Karminn Consultancy Network

- MEG

- Qualityze

- HealthStream

- Glorium Technologies

- HTD Health

- Intelex Technologies

- Okkala Solutions

- Ideagen

- Title21 Health Solutions

- OdiTek Solutions

- EFFIVITY

Competitive Analysis

The Healthcare Quality Management Software market features strong competition among key players such as Veeva Systems, Sparta Systems, HealthStream, Glorium Technologies, HTD Health, Ideagen, Intelex Technologies, Karminn Consultancy Network, MEG, MorCare, OdiTek Solutions, Okkala Solutions, Qualityze, Title21 Health Solutions, and EFFIVITY. These companies compete by offering advanced, scalable platforms that help healthcare providers improve clinical outcomes, reduce errors, and meet regulatory requirements. Most vendors focus on cloud-based deployments to support flexible implementation across hospitals, ambulatory centers, and other care settings. Integration capabilities with EHRs and compliance tools are key differentiators. Market leaders invest in AI-driven analytics and real-time performance dashboards to strengthen their offerings. Smaller firms often cater to niche segments or provide tailored modules to meet specific provider needs. Strong customer support, multilingual features, and regional compliance alignment are critical for expansion into global markets. Vendors prioritize user-friendly interfaces and modular product designs to attract mid-sized and small healthcare facilities. Partnerships with hospitals and government bodies further support brand positioning and product trust. Continuous innovation, cybersecurity enhancements, and regulatory updates remain central to maintaining competitive advantage in this evolving landscape.

Recent Developments

- In 2025, Veeva announced AI features across its applications to improve automation and employee productivity.

- In 2025, Honeywell launched the TrackWise Life Sciences Platform, designed for integrated manufacturing and quality operations across life sciences.

- In 2022, Hexagon AB’s announced the acquisition of ETQ, a major QMS, EHS, and compliance SaaS provider. ETQ’s advanced software capabilities coupled with the existing software allowed Hexagon AB to capture quality data and enable digital transformation with an amplified potential across all clients.

Report Coverage

The research report offers an in-depth analysis based on Type, Deployment Type, End-Use and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will see steady growth driven by rising demand for data-driven quality improvement.

- Hospitals will continue adopting cloud-based platforms for flexibility and cost control.

- AI and predictive analytics will play a larger role in identifying care gaps and risks.

- Vendors will focus on developing tools aligned with value-based care models.

- Smaller healthcare providers will seek affordable, modular software options.

- Integration with EHRs and clinical decision systems will become a standard requirement.

- Regulatory changes will push healthcare systems to invest more in quality tracking tools.

- Emerging markets will present new opportunities due to growing digital health adoption.

- Cybersecurity and data privacy will remain key priorities for software vendors.

- Patient-centered outcome tracking will gain more importance in performance metrics.