Market Overview

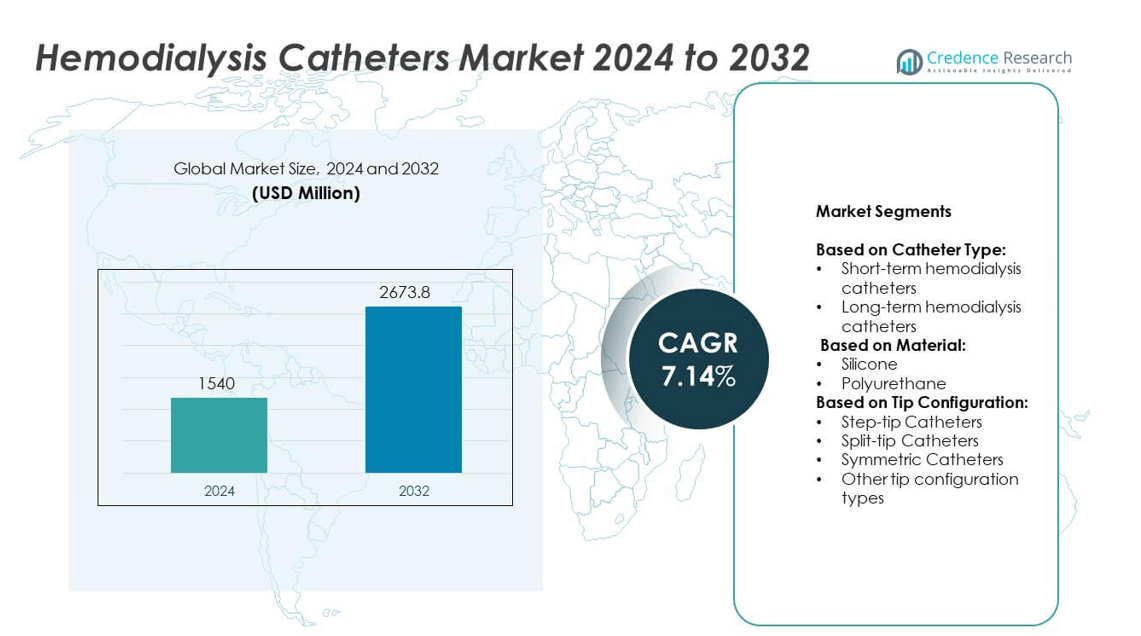

The Hemodialysis Catheters Market size was valued at USD 1540 million in 2024 and is anticipated to reach USD 2673.8 million by 2032, at a CAGR of 7.14% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Hemodialysis Catheters Market Size 2024 |

USD 1540 million |

| Hemodialysis Catheters Market, CAGR |

7.14% |

| Hemodialysis Catheters Market Size 2032 |

USD 2673.8 million |

The Hemodialysis Catheters market is driven by the rising prevalence of chronic kidney disease, growing geriatric populations, and increasing demand for long-term dialysis solutions. Advancements in catheter design, including antimicrobial coatings and biocompatible materials, enhance safety and performance, fueling adoption. The trend toward minimally invasive procedures and the expansion of home-based dialysis practices further strengthen demand. Healthcare infrastructure growth in emerging economies and supportive reimbursement policies also contribute to market expansion, creating opportunities for innovation and wider patient accessibility.

North America leads the Hemodialysis Catheters market due to advanced healthcare systems and high adoption of innovative catheter technologies, while Europe shows steady growth supported by strong regulatory frameworks and research focus. Asia Pacific is emerging rapidly with expanding dialysis infrastructure and rising patient populations. Key players shaping the market include B Braun Melsungen AG, Baxter International Inc., Medtronic plc, and Teleflex, each investing in product innovation and global expansion to meet the growing demand for effective dialysis solutions.

Market Insights

- The Hemodialysis Catheters market was valued at USD 1540 million in 2024 and is projected to reach USD 2673.8 million by 2032, growing at a CAGR of 7.14%.

- Rising prevalence of chronic kidney disease and end-stage renal disease is a major driver fueling strong demand for advanced hemodialysis access solutions.

- Key trends include adoption of minimally invasive catheter designs, integration of antimicrobial coatings, and the growing use of long-term tunneled catheters for chronic dialysis patients.

- Competitive intensity is high, with leading players focusing on innovation, strategic acquisitions, and expanding distribution networks to strengthen market presence globally.

- The market faces restraints such as risks of catheter-related infections, thrombosis, and limited affordability in developing regions due to economic barriers and infrastructure gaps.

- North America remains the leading region, driven by advanced healthcare facilities, high awareness, and favorable reimbursement policies, while Europe shows steady growth supported by strict safety regulations and innovation.

- Asia Pacific is emerging rapidly with rising dialysis patient populations, government support for healthcare expansion, and increasing adoption of cost-effective catheters, while Latin America and the Middle East & Africa offer gradual but promising opportunities.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Prevalence of Chronic Kidney Disease

The Hemodialysis Catheters market is primarily driven by the increasing prevalence of chronic kidney disease (CKD) worldwide. Growing cases of diabetes and hypertension have significantly contributed to renal complications. Patients with end-stage renal disease require dialysis as a life-sustaining therapy, fueling demand for advanced catheters. Governments and healthcare organizations are raising awareness about early diagnosis, boosting treatment rates. It is expected that higher patient inflow will support consistent adoption of hemodialysis devices. The rising burden of CKD continues to push healthcare providers to expand dialysis services globally.

- For instance, Baxter International Inc. reported in 2023 that it treated over 1 million kidney patients annually with its renal therapies, underlining the expanding demand for dialysis solutions.

Growing Geriatric Population and Lifestyle Disorders

The rising geriatric population is another major factor accelerating growth in this sector. Older adults face a higher risk of kidney failure due to age-related organ deterioration and coexisting health conditions. The Hemodialysis Catheters market benefits from expanding demand for treatment solutions among elderly patients. Lifestyle factors such as obesity, smoking, and poor dietary habits also contribute to renal dysfunction. This trend is creating a constant demand for reliable and safe dialysis access solutions. It is driving manufacturers to deliver innovative catheter designs that reduce complications.

- For instance, Becton, Dickinson and Company (BD) is a major global producer of vascular access devices, including catheters designed to improve safety and reduce complications for high-risk patient groups. The January 2025 news release explicitly stated that new production lines would add “100s of millions of units annually” to support U.S. healthcare delivery.

Technological Advancements in Catheter Design

Innovation in catheter design and materials is enhancing treatment outcomes and safety standards. Manufacturers are introducing catheters with antimicrobial coatings, reduced thrombosis risks, and improved durability. These advancements are improving patient comfort and reducing infection rates. The Hemodialysis Catheters market benefits from such innovations, which directly improve clinical acceptance. Hospitals and dialysis centers are adopting advanced devices to ensure efficient therapy delivery. It is encouraging continuous investment in research and development.

Expanding Healthcare Infrastructure and Access

Developing economies are witnessing rapid growth in healthcare infrastructure with improved access to dialysis facilities. Governments are investing in public health programs to support patients requiring dialysis services. The Hemodialysis Catheters market is supported by this growing network of specialized centers. Insurance coverage and reimbursement support for dialysis treatments are also improving patient accessibility. This expansion ensures a steady rise in demand for effective catheter solutions. It is expected to create long-term growth opportunities across both developed and emerging regions.

Market Trends

Shift Toward Minimally Invasive Catheter Designs

The Hemodialysis Catheters market is witnessing a strong trend toward minimally invasive designs. Patients and healthcare providers prefer solutions that reduce complications and improve comfort. Manufacturers are introducing catheters with advanced materials that limit trauma during insertion. It is enhancing patient recovery times and reducing procedure-related risks. Hospitals and dialysis centers are adopting these designs to improve outcomes and efficiency. This trend is likely to accelerate innovation in product engineering and material science.

- For instance, Teleflex is a leading provider of infection-prevention technologies, distributing the Global Impact Report mentions selling “440,000,000+ total product units” across all its product lines in 2024, it does not break down this number by specific product or brand.

Integration of Antimicrobial and Antithrombogenic Features

Manufacturers are increasingly focusing on catheters with antimicrobial and antithrombogenic properties. These features aim to reduce bloodstream infections and clot formation, two major risks in dialysis. The Hemodialysis Catheters market benefits from higher adoption of these advanced solutions across critical care units. It is improving patient safety and aligning with global healthcare standards. Regulatory authorities are encouraging safer device development, which further supports this trend. Growing clinical preference for reduced-risk devices is driving consistent demand.

Rising Adoption of Long-Term Catheters

Long-term catheters are gaining traction due to their durability and suitability for chronic dialysis patients. Growing cases of end-stage renal disease require access devices that sustain frequent treatments. The Hemodialysis Catheters market reflects this shift with increasing demand for tunneled and cuffed designs. It is providing patients with more reliable and safer vascular access. Healthcare providers also benefit from reduced catheter replacement rates, lowering overall treatment costs. This trend highlights the need for patient-focused and cost-effective solutions.

Expansion of Home-Based Dialysis Practices

The global healthcare system is encouraging home-based dialysis to reduce hospital dependency. Patients prefer at-home treatments for convenience and cost savings. The Hemodialysis Catheters market is aligning with this trend by offering products suitable for home use. It is pushing manufacturers to design catheters that are easier to manage outside clinical settings. Growing awareness and training programs support wider acceptance of home-based dialysis solutions. This expansion is reshaping demand patterns and opening new growth opportunities.

Market Challenges Analysis

High Risk of Catheter-Related Complications

The Hemodialysis Catheters market faces significant challenges due to complications such as infections, thrombosis, and mechanical failures. Catheter-related bloodstream infections remain a leading cause of hospitalization and mortality among dialysis patients. These complications increase healthcare costs and reduce patient quality of life. It creates hesitation among physicians and patients, pushing them to explore alternative vascular access methods like arteriovenous fistulas. Strict regulatory guidelines further demand higher safety standards, raising development costs for manufacturers. The constant risk of adverse events limits wider acceptance of catheters in some regions.

Cost Constraints and Limited Access in Developing Regions

Economic barriers continue to restrict the adoption of advanced catheter technologies in low- and middle-income countries. The Hemodialysis Catheters market experiences slower growth in these regions due to affordability issues. It becomes difficult for patients to access high-quality devices without strong reimbursement support. Healthcare systems in such regions often lack adequate infrastructure for safe catheter management. This challenge is compounded by a shortage of trained professionals to handle complex procedures. Cost pressures and infrastructure gaps remain key restraints for market expansion in emerging economies.

Market Opportunities

Advancements in Product Innovation and Design

The Hemodialysis Catheters market offers significant opportunities through advancements in product innovation and design. Manufacturers are focusing on developing catheters with antimicrobial coatings, biocompatible materials, and enhanced flow efficiency. These innovations reduce infection risks and improve long-term performance. It creates strong prospects for higher adoption in both hospital and home care settings. Growing investment in research and development is supporting the introduction of next-generation devices. The emphasis on patient safety and comfort continues to expand market potential globally.

Expanding Access in Emerging Economies

Emerging markets present major opportunities with rising demand for affordable and efficient dialysis solutions. The Hemodialysis Catheters market is expected to benefit from government initiatives that expand healthcare infrastructure. It enables greater availability of dialysis centers and wider use of advanced catheters. Increasing medical tourism in countries like India and Thailand also supports growth. Strong focus on affordable healthcare and improving reimbursement policies will encourage broader adoption. This expansion is set to unlock long-term opportunities for manufacturers targeting developing regions.

Market Segmentation Analysis:

By Catheter Type:

Short-term and long-term devices. Short-term hemodialysis catheters are widely used in emergency situations where immediate vascular access is required. These catheters serve critical roles in acute kidney injury cases or temporary treatment needs. Long-term catheters, particularly tunnelled designs, dominate usage among chronic kidney disease patients. It is preferred for patients undergoing repeated dialysis sessions where durability and safety are essential. The growing number of chronic dialysis cases continues to boost demand for long-term devices.

- For instance, over 850 million people worldwide have some form of kidney disease. This is a much larger figure than the number with ESRD and reflects the full scope of the disease, from early stages to complete kidney failure.

By Material:

The market is divided into silicone and polyurethane catheters. Silicone catheters are valued for their flexibility and biocompatibility, making them suitable for sensitive patients. They reduce the risk of vessel trauma and enhance patient comfort during extended use. Polyurethane catheters, on the other hand, are stronger and provide higher flow rates. It is widely adopted in cases requiring frequent and high-volume dialysis. The balance of comfort and performance across these materials influences product selection in hospitals and clinics.

- For instance, Poly Medicure Ltd. manufactures over 1.5 billion medical devices annually, including various dialysis and vascular access products, demonstrating its capacity to supply high-volume catheter materials such as polyurethane and silicone.

By Tip Configuration:

The market includes step-tip, split-tip, symmetric, and other catheter types. Step-tip catheters are designed to improve blood flow dynamics and minimize recirculation issues. Split-tip catheters are preferred for their ability to reduce clotting and enhance performance. Symmetric catheters focus on ensuring balanced flow and efficient dialysis delivery. It is gaining traction among physicians who prioritize consistent performance and patient safety. Other tip configurations provide niche solutions tailored to specific clinical requirements. The growing variety of catheter tips highlights ongoing innovation to improve treatment efficiency.

Segments:

Based on Catheter Type:

- Short-term hemodialysis catheters

- Long-term hemodialysis catheters

Based on Material:

Based on Tip Configuration:

- Step-tip Catheters

- Split-tip Catheters

- Symmetric Catheters

- Other tip configuration types

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America holds the largest share in the Hemodialysis Catheters market, accounting for 38% in 2024. The region benefits from a well-established healthcare system, high awareness of chronic kidney disease, and advanced dialysis infrastructure. Rising prevalence of diabetes and hypertension has significantly increased the number of dialysis patients. It is supported by favorable reimbursement policies and strong adoption of technologically advanced catheters. Leading companies maintain their base in the United States, ensuring rapid product availability and regulatory approvals. The growing elderly population and demand for long-term catheters further solidify the region’s dominant position.

Europe

Europe represents a substantial portion of the Hemodialysis Catheters market with 27% share in 2024. Countries such as Germany, the United Kingdom, and France lead adoption due to strong healthcare access and government-funded treatment programs. It is driven by increasing chronic kidney disease prevalence among aging populations. Investments in research and development across European nations encourage innovation in catheter designs with enhanced safety. The region also emphasizes strict quality regulations, pushing manufacturers to adopt advanced materials and coatings. Widespread clinical use of tunneled catheters for long-term dialysis care contributes to consistent demand across the region.

Asia Pacific

Asia Pacific accounts for 22% of the Hemodialysis Catheters market in 2024, reflecting rapid growth in patient demand. Countries like China, India, and Japan are expanding dialysis infrastructure to handle rising CKD cases. It is fueled by urbanization, lifestyle disorders, and increasing awareness of dialysis therapies. Governments in the region are investing heavily in affordable treatment access and reimbursement models. Medical tourism in markets such as India and Thailand also supports wider adoption of advanced catheters. Expanding healthcare networks and rising focus on home-based dialysis care are driving future opportunities.

Latin America

Latin America captures 7% of the Hemodialysis Catheters market in 2024. Brazil and Mexico are the key contributors, supported by gradual improvements in healthcare infrastructure. Rising prevalence of kidney disease and increasing access to public health services are fueling demand. It is influenced by government programs aimed at expanding dialysis availability across urban and semi-urban areas. Challenges remain due to uneven healthcare access in rural locations, yet private investments are improving conditions. Market players are targeting this region with cost-effective catheter solutions to strengthen adoption.

Middle East and Africa

The Middle East and Africa region accounts for 6% of the Hemodialysis Catheters market in 2024. Growth is supported by rising investments in hospital infrastructure and expanding prevalence of lifestyle-related kidney disorders. Countries like Saudi Arabia, South Africa, and the UAE are enhancing dialysis capabilities to meet patient needs. It is also boosted by increasing government healthcare spending and public-private partnerships. Limited access in certain low-income countries restricts adoption, but urban centers show strong progress. Growing focus on advanced treatment technologies and imported catheter products is helping the region achieve steady expansion.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Cook Medical

- Medtronic plc

- B Braun Melsungen AG

- Teleflex (Arrow)

- Amecath Medical Technologies

- Poly Medicure Ltd

- Vygon

- Becton, Dickinson, and Company

- Baxter International Inc.

- Bain Medical Equipment (Guangzhou) Co., Ltd.

- Merit Medical System, Inc.

Competitive Analysis

The Hemodialysis Catheters market features strong competition among leading players such as Amecath Medical Technologies, B Braun Melsungen AG, Bain Medical Equipment (Guangzhou) Co., Ltd., Baxter International Inc., Becton, Dickinson, and Company, Cook Medical, Medtronic plc, Merit Medical System, Inc., Poly Medicure Ltd, Teleflex (Arrow), and Vygon. These companies compete by focusing on product innovation, quality improvement, and expanding their distribution networks across global markets. Manufacturers are investing in advanced catheter technologies with antimicrobial coatings and improved tip designs to enhance patient safety and reduce complications. Strong emphasis on research and development ensures continuous product upgrades and competitive positioning. Strategic collaborations, mergers, and acquisitions are widely used to strengthen global footprints and gain access to new customer bases. Leading players also expand in emerging regions by introducing cost-effective solutions to meet growing dialysis needs. Growing competition pushes companies to differentiate through quality certifications, regulatory compliance, and clinical trial support. The market remains highly dynamic, with global leaders facing increasing pressure from regional players offering affordable alternatives. This competitive landscape drives continuous innovation and supports steady growth in both developed and developing markets.

Recent Developments

- In March 2025, B. Braun Melsungen AG was highlighted in an FDA notice regarding bloodline shortages, following the company’s January 8, 2025 letter that outlined supply challenges, demonstrating the firm’s proactive communication in ensuring continuity of care for dialysis patients

- In January 2025, Becton, Dickinson, and Company (BD) confirmed expanded U.S. production capacity for intravenous catheters and vascular access lines, strengthening its ability to meet growing healthcare demand while reinforcing its leadership in catheter technology.

- In August 2024, Baxter International Inc. announced the separation of its kidney care division, later branded as Vantive, marking a strategic restructuring aimed at focusing resources on specialized dialysis and vascular access solutions in the global market.

Report Coverage

The research report offers an in-depth analysis based on Catheter Type, Material, Tip Configuration and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand steadily with growing cases of chronic kidney disease.

- Long-term catheters will gain higher adoption due to rising dialysis demand.

- Technological innovations will improve safety and reduce infection risks.

- Home-based dialysis will increase demand for easy-to-use catheter designs.

- Aging populations worldwide will drive consistent need for dialysis access.

- Emerging economies will create strong opportunities through healthcare expansion.

- Reimbursement support will strengthen patient access to advanced devices.

- Sustainable and biocompatible materials will shape future product development.

- Competition will intensify with global and regional manufacturers investing in R&D.

- Regulatory focus on patient safety will encourage innovation and higher quality standards.