Hydrogen Energy Storage Market Overview:

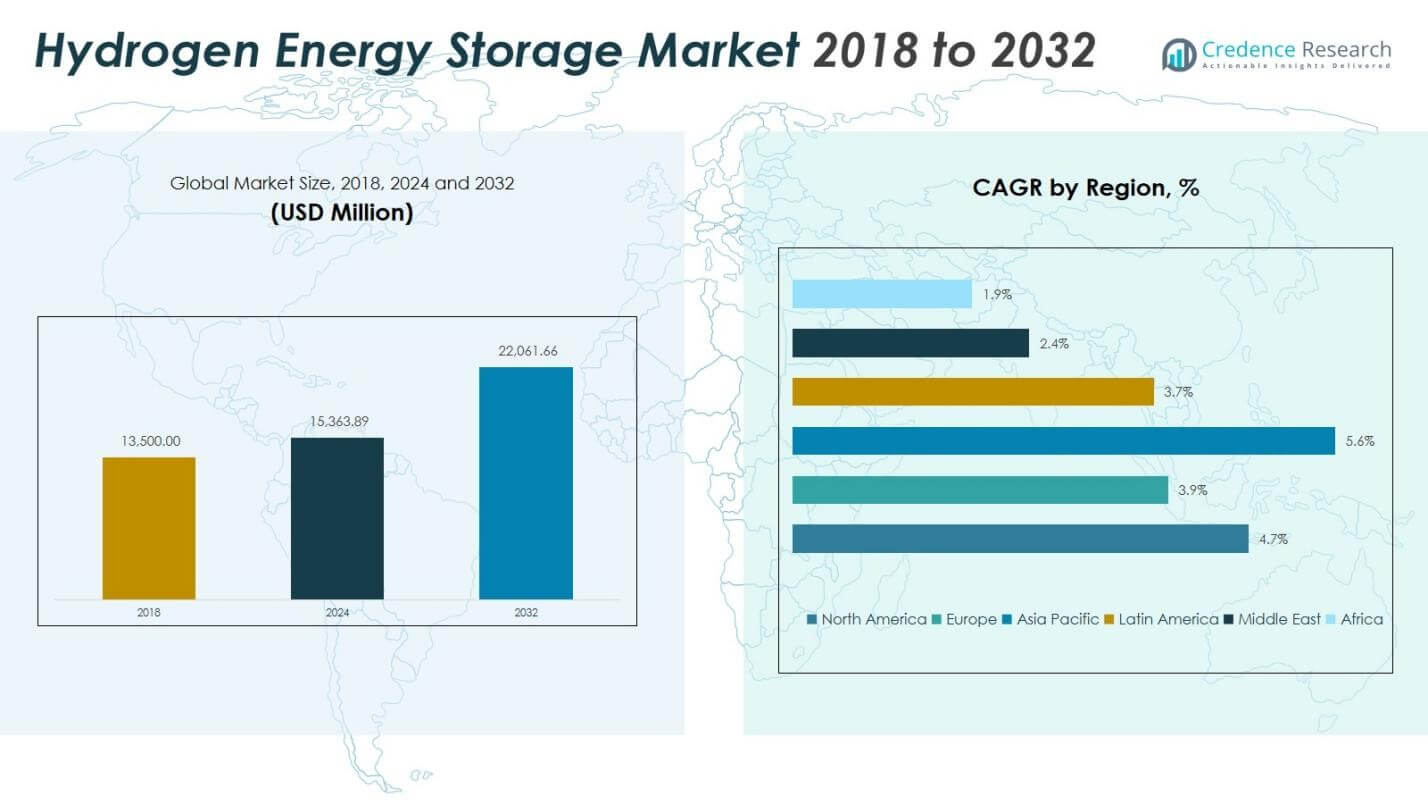

Hydrogen Energy Storage Market size was valued at USD 13,500.00 Million in 2018, increased to USD 15,363.89 Million in 2024, and is anticipated to reach USD 22,061.66 Million by 2032, at a CAGR of 4.71% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Hydrogen Energy Storage Market Size 2024 |

USD 15,363.89 million |

| Hydrogen Energy Storage Market, CAGR |

4.71% |

| Hydrogen Energy Storage Market Size 2032 |

USD 22,061.66 million |

Hydrogen Energy Storage Market Insights

- Market driver reflects rising adoption of hydrogen storage in industrial applications, with the Industrial segment accounting for 57.3% share in 2024 due to growing decarbonization initiatives and transition toward low-carbon fuel systems

- Market trends highlight strong growth in compression-based storage technologies, which led the market with a 48.6% share in 2024, supported by expansion of hydrogen refueling networks and large-scale renewable integration projects.

- Market analysis indicates strong presence of leading players focusing on technology advancements, infrastructure expansion, and partnerships to strengthen hydrogen storage capabilities across power, mobility, and industrial sectors.

- Regional analysis shows Asia Pacific leading the market with a 36.88% share in 2024, followed by North America with 29.96% and Europe with 22.48%, supported by renewable investments, hydrogen infrastructure projects, and government-backed clean-energy programs across key economies.

Hydrogen Energy Storage Market Segmentation Analysis:

By Technology

The Hydrogen Energy Storage Market by technology is led by Compression, which accounted for 48.6% share in 2024, driven by its lower infrastructure cost, high system efficiency, and suitability for large-scale renewable integration and mobility applications. Liquefaction held a significant share due to rising adoption in long-distance hydrogen transport and export projects, while Material-Based Storage gained traction in niche applications such as metal hydrides and chemical carriers. The dominance of Compression is further supported by expanding hydrogen refueling networks, increased deployment of fuel-cell vehicles, and strong investments in grid-level energy storage and industrial decarbonization initiatives.

- For instance, McPhy Energy deployed a hydrogen production unit in the HyWay project with three alkaline electrolyzers producing up to 150,000 m³ of hydrogen annually, where the hydrogen is compressed to 200 bar in gaseous form for mobility applications.

By Application

By application, the Industrial segment dominated the Hydrogen Energy Storage Market with a 57.3% share in 2024, supported by strong demand from refineries, chemicals, steel manufacturing, and power generation sectors transitioning to low-carbon hydrogen. The Commercial segment recorded steady growth due to adoption in distributed energy systems, backup power, and hydrogen-based microgrids, while the Residential segment remained smaller but expanded with fuel-cell heating systems and off-grid renewable storage solutions. The leadership of the Industrial segment is driven by government decarbonization mandates, hydrogen-based process heat requirements, and strategic investments in green hydrogen production and storage infrastructure.

- For instance, Reliance Industries trialed torrefied biomass gasification at its Jamnagar refinery to produce green hydrogen, advancing plans for demonstration plants yielding up to 50 tonnes per day.

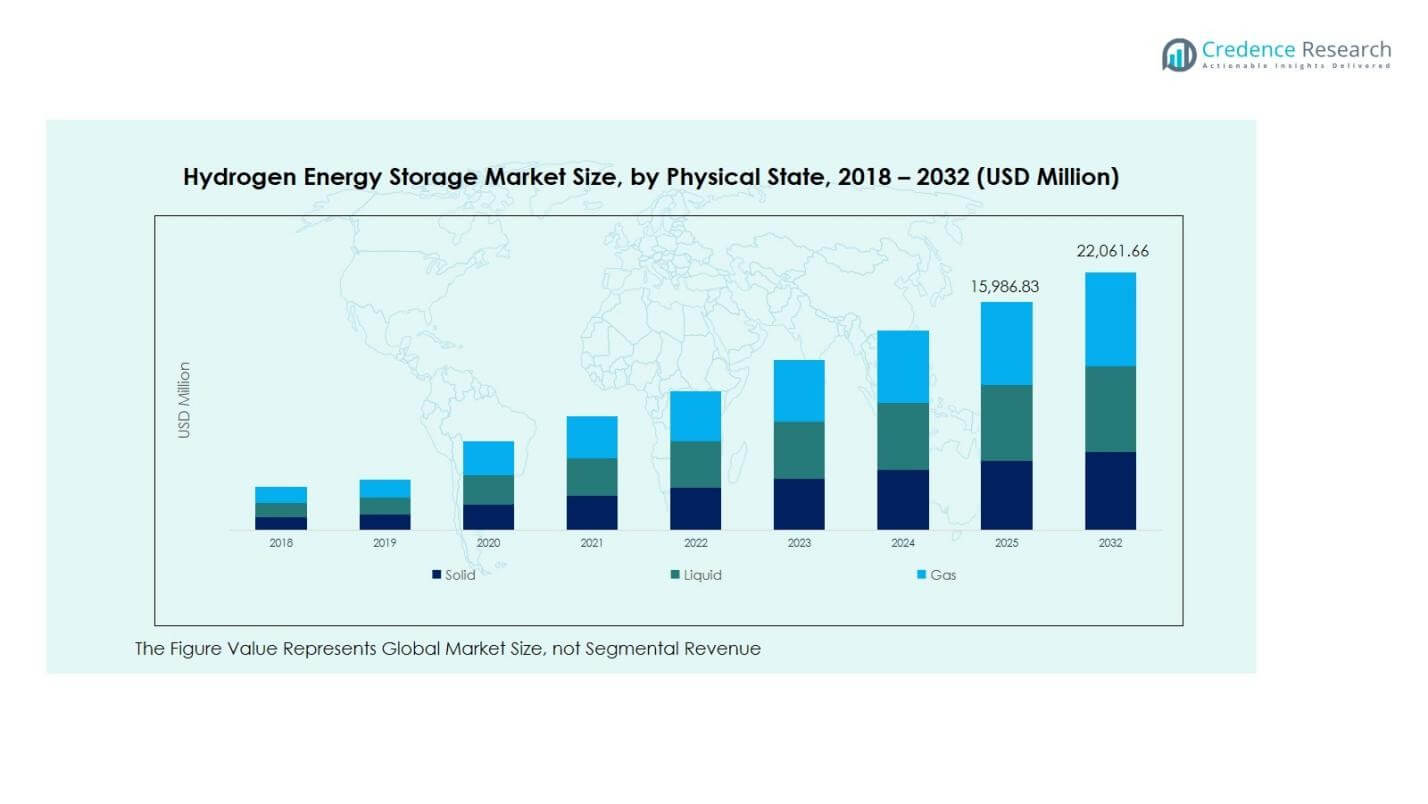

By Physical State

In terms of physical state, Gas-phase hydrogen storage led the market with a 51.9% share in 2024, owing to its technical maturity, compatibility with compression-based systems, and widespread use in mobility, industrial applications, and refueling infrastructure. Liquid hydrogen accounted for a growing share as it supports high-density storage for aerospace, long-haul transport, and international hydrogen supply chains, while Solid-state storage advanced in research-driven energy and defense applications. The dominance of Gas storage is strengthened by declining compression costs, scalable pipeline networks, and increasing adoption of hydrogen blending and distributed renewable energy storage systems.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Hydrogen Energy Storage Market Overview

Key Growth Drivers

Rising Demand for Renewable Energy Integration

The Hydrogen Energy Storage Market is witnessing strong growth as hydrogen plays a critical role in stabilizing power grids with increasing renewable energy penetration. Excess electricity generated from solar and wind is converted into hydrogen through electrolysis and stored for later use in power generation, grid balancing, and long-duration storage applications. This capability enables utilities and policymakers to address intermittency challenges while supporting energy-transition goals. Large-scale renewable projects, particularly in Europe, Asia Pacific, and the Middle East, are accelerating investments in power-to-gas and hydrogen storage infrastructure, strengthening hydrogen’s position as a cornerstone of clean-energy system resilience.

- For instance, ITM Power partners with Stablegrid Group on two German projects totaling 710 MW electrolysis capacity, using underground caverns for hydrogen storage to balance renewables and stabilize the power grid.

Decarbonization Policies and Industrial Transition

Stringent global decarbonization mandates and net-zero commitments are driving hydrogen storage adoption across heavy industries such as refining, steel, chemicals, and transportation. Governments are implementing financial incentives, hydrogen roadmaps, and industrial transition strategies to replace fossil-based fuels with low-carbon hydrogen. Stored hydrogen supports industrial heat processes, backup power systems, and clean-fuel applications, encouraging long-term infrastructure development. Major economies are prioritizing green hydrogen value chains, supported by public-private investments, carbon-pricing frameworks, and clean-energy funding programs. This regulatory push, combined with corporate sustainability initiatives, is accelerating the shift toward hydrogen-based industrial energy ecosystems.

- For instance, HYBRIT led by SSAB, LKAB, and Vattenfall successfully completed a pilot project storing fossil-free hydrogen gas in a steel-lined rock cavern at 250 bar pressure. The 100 cubic meter facility, expandable to 100,000–120,000 m³, supplies enough hydrogen for 3-4 days of steel plant operations and passed 50-year equivalent mechanical tests with no leakage.

Advancements in Storage Technologies and Infrastructure

Technological advancements in compression, liquefaction, and material-based storage systems are significantly enhancing the scalability, safety, and efficiency of hydrogen storage solutions. Innovations in storage tanks, composite cylinders, cryogenic systems, and solid-state storage materials are reducing operational costs and improving energy density. Simultaneously, expansion of hydrogen refueling networks, large-capacity storage hubs, and integrated hydrogen transport corridors is strengthening supply-chain reliability. These developments support applications in mobility, distributed energy, and industrial fuel switching. Continued research investments and technology commercialization efforts are enabling broader market adoption while positioning hydrogen as a competitive long-term energy carrier.

Key Trends & Opportunities

Emergence of Green Hydrogen and Power-to-X Ecosystems

One of the most significant trends in the Hydrogen Energy Storage Market is the rapid expansion of green hydrogen production, supported by falling renewable electricity costs and large-scale electrolyzer deployment. Stored hydrogen is increasingly converted into multiple downstream energy products under Power-to-X pathways, including synthetic fuels, ammonia, methanol, and hydrogen-based e-fuels for shipping and aviation. This trend creates new revenue opportunities across cross-sector energy integration, export-oriented hydrogen corridors, and hydrogen-to-power applications. Growing collaborations between utilities, technology providers, and industrial customers are accelerating commercialization of integrated green hydrogen storage and conversion projects worldwide.

- For instance, ITM Power deployed a 10 MW electrolyzer at Shell’s Rhineland Refinery in Germany through the REFHYNE project. This initiative produces green hydrogen for industrial applications and transportation fuels, partnering with Linde for refueling stations and large-scale production.

Expansion of Hydrogen Storage in Mobility and Transport

Hydrogen storage is gaining strategic importance in mobility applications such as fuel-cell vehicles, heavy-duty transport, rail networks, marine propulsion, and aviation research programs. Compressed gas and liquid hydrogen storage systems support extended driving range, rapid refueling capability, and high-energy transportation use cases where battery-electric solutions face limitations. Governments are investing in hydrogen refueling infrastructure, corridor-based logistics routes, and zero-emission public transport fleets, creating strong market opportunities for storage solution providers. This trend enhances supply-chain development, stimulates OEM partnerships, and positions hydrogen as a key enabler of low-carbon transportation ecosystems.

- For instance, Toyota’s Mirai fuel-cell sedan utilizes high-pressure (700 bar) hydrogen tanks that offer a range of approximately 650 km per refueling, showcasing the efficiency of advanced composite storage systems.

Key Challenges

High Capital Costs and Infrastructure Development Barriers

Despite strong growth potential, the Hydrogen Energy Storage Market faces challenges related to high capital costs associated with storage tanks, liquefaction systems, compression units, and support infrastructure. Large-scale storage hubs and hydrogen transport networks require significant upfront investments and long development cycles, which can limit adoption in emerging markets and price-sensitive industries. Uncertain demand maturity and project financing constraints further add to investment risks. Additionally, cost competitiveness with conventional fuels and alternative storage technologies remains a major barrier, requiring continued technological innovation, scale-driven cost reductions, and supportive financial policy mechanisms.

Safety, Handling, and Regulatory Standardization Issues

Hydrogen’s physical characteristics, including high flammability and low molecular density, create safety and storage handling challenges that demand stringent engineering standards, monitoring systems, and regulatory compliance frameworks. Variations in hydrogen codes, certification procedures, and infrastructure standards across regions hinder uniform deployment and global interoperability. Public perception concerns, workforce skill gaps, and operational safety requirements increase implementation complexity for new projects. Addressing these challenges requires coordinated international standardization, improved safety protocols, specialized training, and continuous technology validation to enhance confidence in large-scale hydrogen storage operations.

Regional Analysis

North America

North America accounted for 29.96% share of the Hydrogen Energy Storage Market in 2024, supported by strong investments in clean hydrogen infrastructure and energy-transition initiatives. The regional market increased from USD 4,104.00 Million in 2018 to USD 4,602.93 Million in 2024, and it is projected to reach USD 6,598.68 Million by 2032, registering a CAGR of 4.7%. Growth is driven by industrial decarbonization programs, expanded hydrogen refueling networks, and large-scale renewable-based hydrogen storage projects in the U.S. and Canada. Policy incentives and government-backed clean-energy targets continue to reinforce technology deployment across power, mobility, and industrial sectors.

Europe

Europe held 22.48% share of the Hydrogen Energy Storage Market in 2024, reflecting strong policy-driven hydrogen adoption across industrial clusters and renewable-energy storage applications. The market grew from USD 3,172.50 Million in 2018 to USD 3,453.38 Million in 2024, and it is expected to reach USD 4,649.55 Million by 2032, recording a CAGR of 3.9%. Growth is supported by EU hydrogen roadmaps, green-hydrogen investment programs, and large-scale electrolyzer integration in power-to-gas projects. Expansion of hydrogen transport corridors and energy-storage initiatives in Germany, France, and the UK strengthens regional leadership in clean-energy transition frameworks.

Asia Pacific

Asia Pacific emerged as the largest regional market with 36.88% share in 2024, driven by rapid renewable-energy deployment, industrial hydrogen demand, and government-supported clean-energy programs. The market expanded from USD 4,833.00 Million in 2018 to USD 5,666.91 Million in 2024, and it is forecast to reach USD 8,720.99 Million by 2032, advancing at a CAGR of 5.6%. Strong contributions come from China, Japan, South Korea, and India through investments in hydrogen mobility, ammonia and chemicals, and grid-level storage solutions. Strategic manufacturing capacity expansion and integrated hydrogen value-chain development continue to reinforce regional growth momentum.

Latin America

Latin America accounted for 6.14% share of the Hydrogen Energy Storage Market in 2024, supported by emerging renewable-hydrogen projects and increasing industrial decarbonization initiatives. The regional market value rose from USD 837.00 Million in 2018 to USD 943.19 Million in 2024, and it is projected to reach USD 1,254.65 Million by 2032, registering a CAGR of 3.7%. Growth is driven by green-hydrogen export initiatives, ammonia production opportunities, and pilot storage projects across Brazil, Chile, and Argentina. Expanding solar and wind capacity and government-backed hydrogen development frameworks are strengthening the region’s long-term hydrogen storage potential.

Middle East

The Middle East accounted for 2.16% share of the Hydrogen Energy Storage Market in 2024, reflecting early-stage but strategic investments in large-scale green and blue hydrogen programs. The market increased from USD 324.00 Million in 2018 to USD 331.76 Million in 2024, and it is expected to reach USD 399.44 Million by 2032, growing at a CAGR of 2.4%. Growth is influenced by export-oriented hydrogen projects, ammonia production hubs, and integration of hydrogen into industrial and energy transition plans. GCC countries are leading regional initiatives, supported by giga-project investments and long-term hydrogen economy strategies.

Africa

Africa represented 2.38% share of the Hydrogen Energy Storage Market in 2024, driven by emerging renewable-hydrogen development corridors and pilot-scale storage projects. The regional market grew from USD 229.50 Million in 2018 to USD 365.72 Million in 2024, and it is projected to reach USD 438.35 Million by 2032, recording a CAGR of 1.9%. Growth is supported by green-hydrogen initiatives in South Africa, North Africa’s export-focused hydrogen partnerships, and integration of hydrogen in power and industrial value chains. Increasing renewable capacity expansion and international investment collaboration continue to shape Africa’s hydrogen storage market outlook.

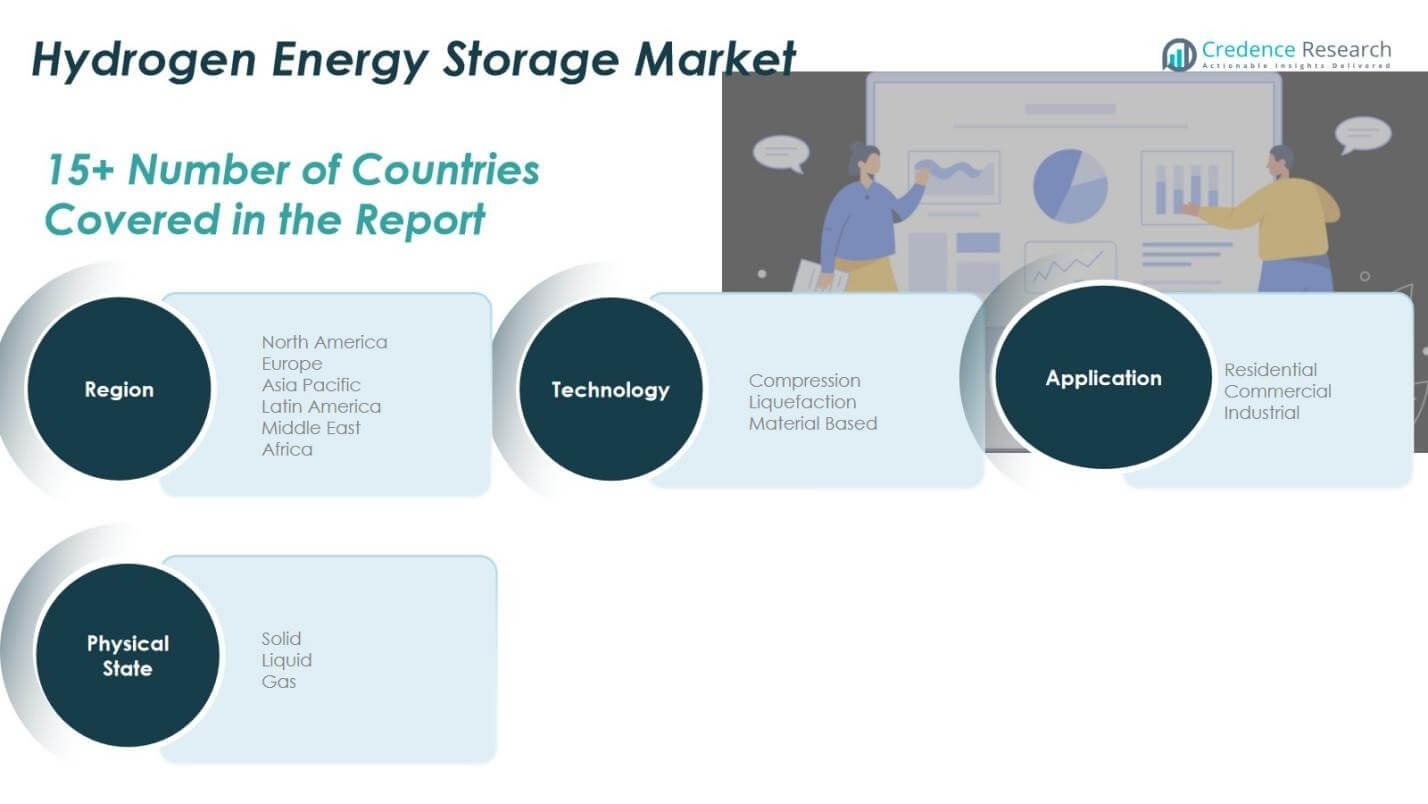

Hydrogen Energy Storage Market Segmentations:

By Technology

- Compression

- Liquefaction

- Material-Based Storage

By Application

- Residential

- Commercial

- Industrial

By Physical State

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

Competitive landscape analysis in the Hydrogen Energy Storage Market is shaped by leading players such as Air Liquide, Air Products Inc., Cummins Inc., Engie, ITM Power, Iwatani Corporation, Linde plc, Nel ASA, Nedstack Fuel Cell Technology BV, and Steelhead Composites Inc., who play a central role in technology development and market expansion. The market reflects strong strategic focus on large-scale hydrogen storage infrastructure, electrolyzer integration, and advanced compression and liquefaction systems to support industrial decarbonization, mobility, and renewable-energy storage applications. Key players are strengthening their portfolios through partnerships, demonstration projects, and investments in green hydrogen ecosystems, while also expanding manufacturing capabilities and developing long-duration storage solutions. Competitive momentum is further influenced by mergers, joint ventures, and government-backed clean-hydrogen programs that encourage cross-industry collaboration. Companies are prioritizing cost-efficient storage technologies, safety performance, and scalability to address growing adoption across industrial, grid, and transport end-use sectors, reinforcing continuous innovation and technology commercialization across global hydrogen storage value chains.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Air Liquide

- Air Products Inc.

- Cummins Inc.

- Engie

- ITM Power

- Iwatani Corporation

- Linde plc

- Nedstack Fuel Cell Technology BV

- Nel ASA

- Steelhead Composites Inc.

Recent Developments

- In January 2025, EQUANS and INOCEL signed a partnership to develop hydrogen storage and production solutions that integrate carbon-free hydrogen technologies and enhance energy storage capabilities.

- In April 2025, Hyroad Energy partnered with Bosch Rexroth and GenH2 to develop a liquid hydrogen refueling station that eliminates boil-off losses, advancing hydrogen infrastructure and storage efficiency.

- In June 2024, GKN Hydrogen entered an exclusive partnership with ZYNP in China to promote metal hydride-based hydrogen storage systems and strengthen the regional hydrogen supply chain.

- In September 2024, ADNOC agreed to acquire a 35% equity stake in ExxonMobil’s low-carbon hydrogen and ammonia facility in Baytown, Texas, accelerating decarbonization and expanding hydrogen production and storage infrastructure.

Report Coverage

The research report offers an in-depth analysis based on Technology, Application, Physical State and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand as hydrogen becomes a core enabler of long-duration renewable energy storage and grid stability.

- Green hydrogen storage capacity will increase with large-scale electrolyzer deployment and renewable integration initiatives.

- Industrial sectors will drive demand as hydrogen storage supports low-carbon fuels, process heating, and energy transition strategies.

- Hydrogen storage adoption will rise in mobility applications, particularly in heavy-duty transport, rail, marine, and aviation use cases.

- Technological innovation will enhance compression, liquefaction, and material-based storage efficiency and safety performance.

- Government policies, hydrogen roadmaps, and decarbonization targets will accelerate investment in large storage infrastructure projects.

- Hydrogen export corridors and international supply chains will create new storage and logistics opportunities across regions.

- Collaboration among energy companies, OEMs, and technology developers will strengthen commercialization and ecosystem development.

- Declining technology costs and scaling benefits will improve the economic viability of hydrogen storage solutions over time.

- Integration of hydrogen storage into hybrid energy systems and smart grids will support resilient, flexible, and sustainable energy networks.