| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| LATAM RIS and PACS Market Size 2024 |

USD 342.0 Million |

| LATAM RIS and PACS Market, CAGR |

8.31% |

| LATAM RIS and PACS Market Size 2032 |

USD 646.3 Million |

Market Overview:

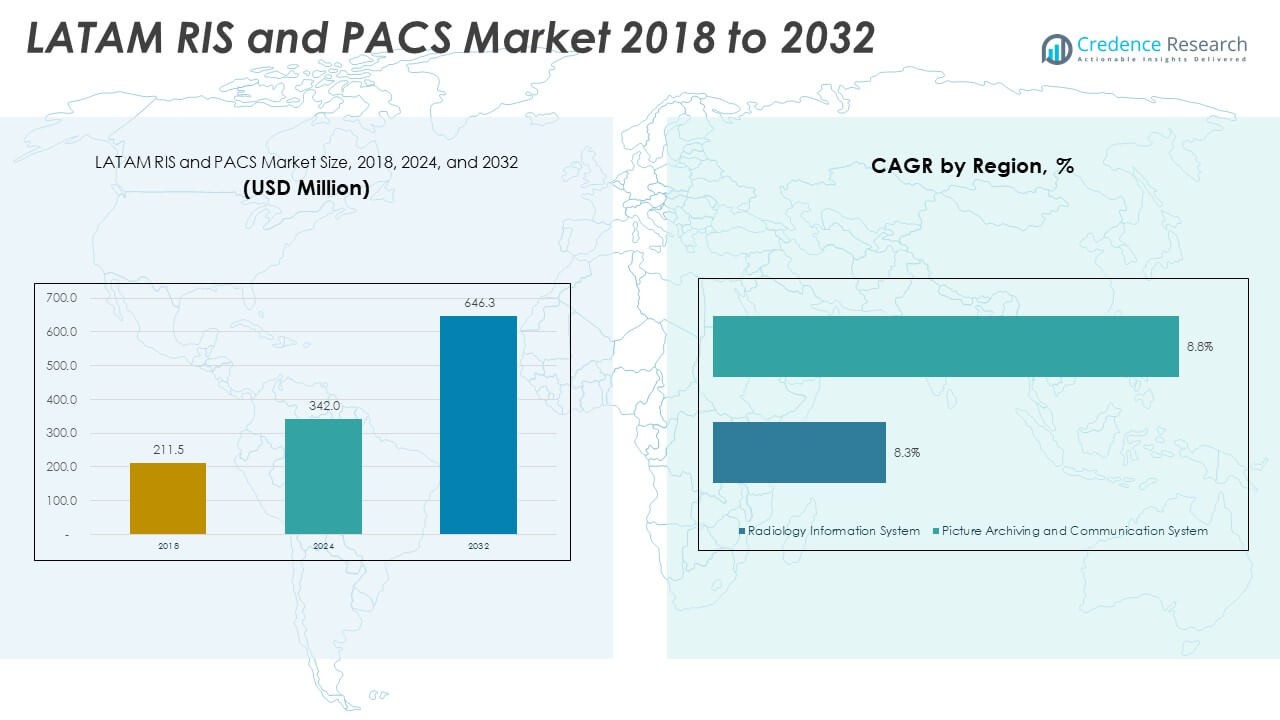

The LATAM RIS and PACS Market size was valued at USD 211.5 million in 2018 to USD 342.0 million in 2024 and is anticipated to reach USD 646.3 million by 2032, at a CAGR of 8.31% during the forecast period.

The market is driven by a combination of healthcare modernization efforts, rising imaging volumes, and increasing demand for scalable IT solutions. One of the key factors fueling market growth is the push toward digital transformation across hospitals and diagnostic centers, aiming to streamline imaging workflows, reduce manual errors, and improve overall efficiency. The rising prevalence of chronic conditions and the consequent increase in diagnostic imaging procedures have further stressed the need for advanced systems like RIS and PACS that can manage large volumes of patient data effectively. Additionally, cloud-based deployment models are gaining traction due to their cost-effectiveness, scalability, and ability to support remote access—making them particularly appealing in regions with limited physical infrastructure. Technological advancements, such as artificial intelligence (AI), machine learning integration, and real-time analytics, are also reshaping the market, enabling better diagnostic accuracy and decision-making.

Regionally, the LATAM RIS and PACS market is characterized by varied levels of adoption and infrastructure readiness. Brazil, Mexico, and Argentina lead the market, accounting for a major share due to their relatively mature healthcare IT ecosystems, growing investments in digital health, and the presence of international and domestic vendors. These countries have shown consistent growth in healthcare spending and have adopted national strategies to digitize medical imaging systems. Chile, Colombia, and Peru represent emerging markets where digital health adoption is on the rise, driven by the need to expand access to diagnostic services, especially in underserved areas. While infrastructure gaps and budget constraints continue to pose challenges in some regions, there is a clear shift toward adopting cloud-based solutions to bypass traditional IT limitations. In contrast, countries in Central America and smaller economies in South America are in earlier stages of PACS and RIS adoption.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights:

- The LATAM RIS and PACS Market grew from USD 211.5 million in 2018 to USD 342.0 million in 2024 and is projected to reach USD 646.3 million by 2032, registering a CAGR of 8.31%.

- Healthcare modernization, rising imaging volumes, and the demand for scalable IT infrastructure continue to drive adoption across hospitals and diagnostic centers.

- Cloud-based deployment models are expanding rapidly due to their affordability, ease of access, and lower infrastructure requirements, especially in resource-limited regions.

- Technological advancements, including AI integration and real-time analytics, are transforming RIS and PACS into intelligent diagnostic platforms, reducing errors and improving workflow efficiency.

- Government-led digital health initiatives in countries like Brazil, Mexico, and Argentina are accelerating adoption through policy support, standardization, and financial incentives.

- Infrastructure disparities and limited IT readiness in rural and public sectors remain key barriers, slowing adoption in smaller economies and underserved areas.

- Regulatory complexity and concerns around data privacy and cybersecurity continue to challenge vendors, prolonging implementation cycles and limiting market penetration in certain countries.

Market Drivers:

Rising Demand for Diagnostic Imaging Fuels System Adoption

The growing burden of chronic diseases and aging populations across Latin America has led to a surge in diagnostic imaging procedures. Hospitals and diagnostic centers are increasingly adopting RIS and PACS to manage higher imaging volumes and improve patient care coordination. Traditional manual systems are no longer sufficient to handle the complexity and scale of imaging data, pushing healthcare providers toward integrated digital solutions. The LATAM RIS and PACS Market benefits from this trend, with institutions seeking to streamline radiology workflows and improve turnaround times for clinical decisions. It supports clinicians in reducing redundancy, enabling faster diagnoses and improving treatment planning. The need for structured image storage and faster retrieval is becoming a priority across urban and semi-urban healthcare facilities.

Government-Led Digital Health Initiatives Create Enabling Environment

Health ministries across Brazil, Mexico, Argentina, and other major LATAM countries are implementing national strategies to enhance digital healthcare infrastructure. These efforts include encouraging hospitals to adopt electronic medical records and centralized imaging systems like RIS and PACS. Public healthcare reforms are focusing on increasing efficiency, minimizing manual errors, and enabling data-driven decision-making across departments. The LATAM RIS and PACS Market benefits from policies that support DICOM standards, cloud adoption, and interoperability across radiology networks. It gains momentum in environments where governments offer incentives or subsidies for technology upgrades. Regulatory frameworks are gradually evolving to accommodate cross-border teleradiology and data sharing, which enhances regional collaboration.

- For instance, Brazil’s Ministry of Healthhas implemented a cloud-based patient record system in Rio de Janeiro, digitizing over 1 million patient records in just a few months using the VitaHisCare solution based on Microsoft technologies.

Cloud-Based Deployment Offers Scalability and Cost Efficiency

Many healthcare institutions in Latin America face limited IT infrastructure, high upfront costs, and resource constraints. Cloud-based RIS and PACS solutions provide a scalable and affordable alternative to traditional on-premise installations. These systems eliminate the need for extensive hardware investments and reduce maintenance burdens on hospitals. The LATAM RIS and PACS Market is seeing faster adoption in smaller clinics and regional hospitals due to cloud deployment models. It allows secure remote access to images and reports, improving collaboration among specialists across locations. Cloud-enabled platforms also support business continuity, ensuring that imaging services remain uninterrupted even during local infrastructure failures.

Technological Advancements Drive Demand for Intelligent Imaging Systems

Radiology departments are seeking tools that enhance diagnostic accuracy and reduce reporting time. Advanced features such as AI-powered image analysis, speech recognition, and automated workflow management are becoming essential components of modern RIS and PACS. The LATAM RIS and PACS Market is evolving to accommodate these capabilities, offering solutions that go beyond simple image archiving. It supports integration with third-party AI tools and decision-support applications, which improves diagnostic outcomes and reduces radiologist workload. Vendors are investing in feature-rich platforms that enable intelligent image processing and structured reporting. Healthcare providers value systems that deliver both performance and clinical insight in a single interface.

- For example, Pixeon Aurora PACSintegrates AI-powered features such as automatic segmentation of breast masses for mammography, detection of lung opacities in chest X-rays, bone age calculation, and sarcopenia analysis. These tools directly increase diagnostic accuracy and reporting speed, supporting radiologists in high-volume environments and reducing workload through automation.

Market Trends:

Integration of Artificial Intelligence Enhances Diagnostic Capabilities

Hospitals and imaging centers across Latin America are incorporating AI tools to improve accuracy and efficiency in radiology workflows. AI algorithms support radiologists by detecting anomalies, prioritizing cases, and automating measurements. These capabilities are helping reduce diagnostic errors and streamline interpretation time for high-volume imaging departments. The LATAM RIS and PACS Market is evolving to support AI integration within existing systems, enabling seamless data exchange between imaging platforms and intelligent applications. It allows healthcare providers to use structured reports, decision-support tools, and predictive analytics directly within the RIS/PACS interface. This trend reflects a shift toward data-driven radiology and precision diagnostics.

- For instance, Sectra’s solution integrates AI applications directly into radiology workflows via the Sectra Amplifier Marketplace, which serves as a centralized point for contracting, purchasing, and servicing validated AI tools.

Cloud and Web-Based Platforms Gain Momentum Across Healthcare Facilities

Latin American healthcare providers are moving toward cloud-based and web-enabled RIS and PACS solutions due to their lower capital investment and operational flexibility. These platforms allow secure image access from multiple sites, improve disaster recovery, and enable remote reporting. Cloud adoption is rising not only in urban centers but also in smaller regions where physical infrastructure remains limited. The LATAM RIS and PACS Market is benefiting from the scalability and affordability of these solutions, especially for mid-sized hospitals and diagnostic chains. It helps providers maintain continuity of care without relying on high-maintenance, in-house servers. Vendors are offering customizable, subscription-based models to meet diverse organizational needs.

- For example, GE Healthcare, for example, has deployed cloud-based PACS solutions that improve diagnostic speed and enable remote access critical for Latin American providers expanding telemedicine and teleradiology services

Focus on Interoperability Strengthens Hospital IT Ecosystems

Healthcare institutions in the region are prioritizing systems that support interoperability with electronic medical records (EMR), laboratory systems, and other hospital information platforms. Seamless data exchange improves care coordination, reduces duplication, and allows for centralized patient records. The LATAM RIS and PACS Market is aligning with this trend by offering open-architecture solutions that comply with global standards such as DICOM and HL7. It enables healthcare professionals to access imaging data alongside clinical notes and lab results through a unified interface. This integration enhances diagnostic decision-making and supports multi-disciplinary care approaches. Interoperable systems also prepare institutions for future regulatory compliance and data-sharing requirements.

Mobile Access and Remote Diagnostics Expand Reach of Imaging Services

Mobile accessibility and remote diagnostics are becoming essential in Latin America, where geographic and economic disparities affect healthcare delivery. Providers are adopting RIS and PACS systems that allow radiologists to access, review, and report images through mobile devices and web portals. This supports faster turnaround in underserved areas and enables collaboration with specialists across regions. The LATAM RIS and PACS Market is witnessing increased demand for mobile-compatible solutions that ensure secure, real-time access. It extends imaging capabilities beyond traditional hospital settings, supporting teleradiology and second-opinion services. This trend is reshaping radiology workflows and expanding access to specialized care.

Market Challenges Analysis:

Infrastructure Gaps and Limited IT Readiness Hinder Adoption in Rural and Public Sectors

Many healthcare institutions across Latin America, especially in rural and low-income areas, face persistent infrastructure limitations that delay the deployment of advanced radiology systems. Limited internet connectivity, outdated hardware, and insufficient technical support reduce the feasibility of implementing cloud-based or enterprise-grade RIS and PACS platforms. The LATAM RIS and PACS Market is affected by this uneven readiness, which slows the pace of digital transformation outside major urban centers. It also creates disparities in diagnostic capabilities between public and private healthcare providers. Budget constraints in government-funded hospitals further restrict investments in scalable, interoperable systems. Without adequate infrastructure, these institutions struggle to meet growing imaging demands or maintain continuity in patient care.

Regulatory Complexity and Data Security Concerns Impact Market Growth

The region’s fragmented regulatory landscape presents challenges for consistent RIS and PACS adoption. Countries vary in their standards for medical data exchange, patient privacy, and health IT certifications, making it difficult for vendors to deliver region-wide solutions. The LATAM RIS and PACS Market must navigate diverse compliance requirements while ensuring data integrity and confidentiality. It faces rising concerns over cybersecurity, particularly with cloud-based platforms that involve remote access and external hosting. Some providers remain hesitant to shift from legacy systems due to perceived data risks or unclear legal protections. These challenges increase implementation timelines and raise the cost of compliance, slowing market penetration in key segments.

Market Opportunities:

Rising Investments in Healthcare Infrastructure Unlock New Deployment Potential

Governments and private investors are increasing funding to modernize hospitals and diagnostic centers across Latin America. These investments create favorable conditions for implementing advanced imaging IT solutions. The LATAM RIS and PACS Market can benefit from projects focused on expanding healthcare access, especially in underserved regions. It presents opportunities for vendors to offer scalable systems tailored to diverse institutional needs. Solutions that combine cloud deployment, mobile access, and AI support are well-positioned to meet this demand. The market stands to grow by aligning with national healthcare transformation agendas.

Growing Demand for Teleradiology and Remote Diagnostics Expands Market Scope

The adoption of teleradiology is gaining traction in Latin America due to the shortage of radiologists and the need to extend diagnostic services beyond major cities. The LATAM RIS and PACS Market can leverage this shift by offering platforms that support secure remote image access and reporting. It can play a vital role in facilitating cross-regional collaboration and second-opinion services. Vendors that enable mobile compatibility and real-time data sharing will be better equipped to capture this opportunity. Teleradiology also supports healthcare continuity in remote and emergency settings. This trend broadens the market’s relevance across varied healthcare delivery models.

Market Segmentation Analysis:

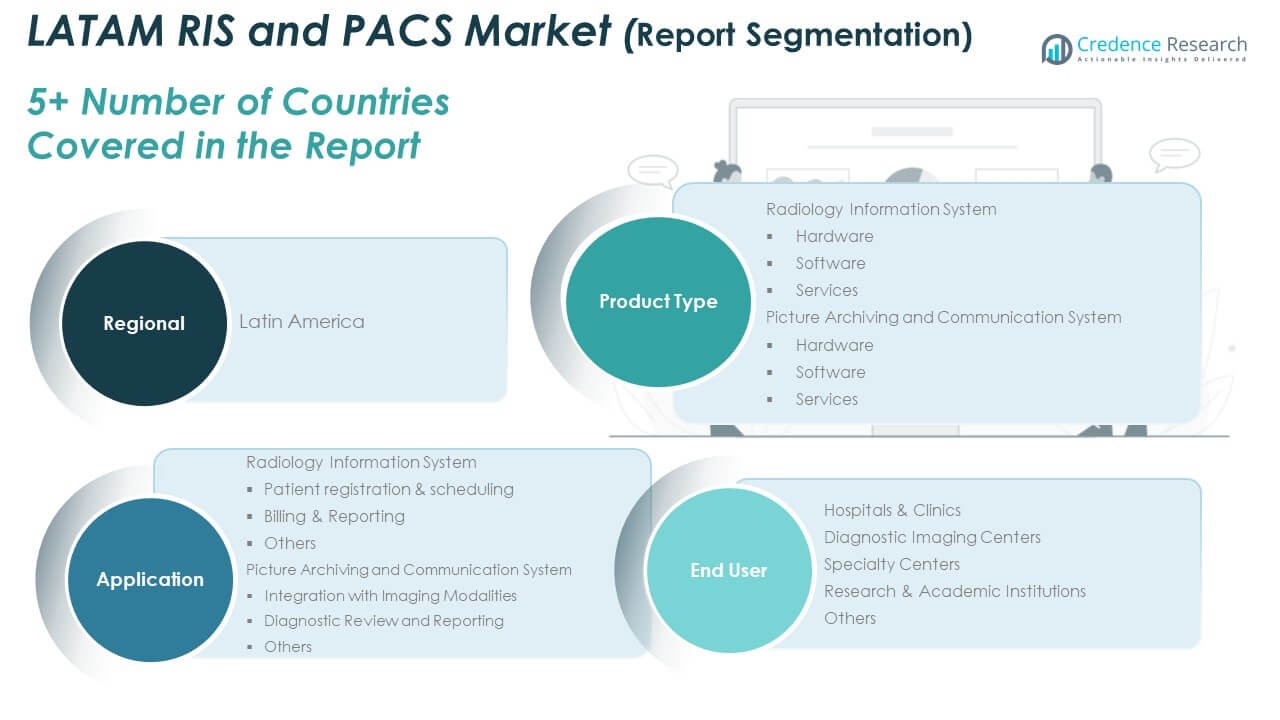

The LATAM RIS and PACS Market is segmented by product type, application, and end user, reflecting the diverse needs of healthcare providers across the region.

By product type, Radiology Information System (RIS) is divided into hardware, software, and services. Software dominates due to rising demand for workflow automation and integration with EMRs. Picture Archiving and Communication System (PACS) also includes hardware, software, and services, with software leading adoption because of its role in image storage, retrieval, and sharing.

- For example, RamSoftoffers cloud-based RIS and PACS solutions where software is central to workflow automation, image storage, retrieval, and sharing. Their PowerServer RIS/PACS is built on a single, unified database, providing seamless integration with EMRs and eliminating the need for costly hardware investments.

By application, the RIS segment covers patient registration & scheduling, billing & reporting, and others. Patient registration & scheduling holds the largest share due to its role in managing patient flow and resource allocation. In PACS, integration with imaging modalities and diagnostic review & reporting are the key applications. Diagnostic review & reporting leads due to increasing imaging volumes and the need for timely interpretation.

- For instance, broadly adopted in Spanish-speaking Latin America by both hospitals and imaging centers, Philips Vue PACS is recognized for reliability and minimal downtime, supporting high-volume diagnostic review and reporting needs

By end user, the LATAM RIS and PACS Market serves hospitals & clinics, diagnostic imaging centers, specialty centers, research & academic institutions, and others. Hospitals & clinics dominate the segment, driven by infrastructure development and higher imaging demand. Diagnostic imaging centers follow closely, adopting scalable solutions to improve service efficiency and data management.

Segmentation:

By Product Type

- Radiology Information System (RIS)

- Hardware

- Software

- Services

- Picture Archiving and Communication System (PACS)

- Hardware

- Software

- Services

By Application

- Radiology Information System

- Patient Registration & Scheduling

- Billing & Reporting

- Others

- Picture Archiving and Communication System

- Integration with Imaging Modalities

- Diagnostic Review and Reporting

- Others

By End User

- Hospitals & Clinics

- Diagnostic Imaging Centers

- Specialty Centers

- Research & Academic Institutions

- Others

By Region (within LATAM)

- Brazil

- Mexico

- Argentina

- Peru

- Colombia

- Chile

- Central America

- Rest of LATAM

Regional Analysis:

Brazil, Mexico, and Argentina Lead Market Expansion Across Latin America

Brazil holds the largest share in the LATAM RIS and PACS Market, accounting for approximately 38% of the regional market. Its advanced hospital networks, public-private healthcare investments, and growing number of diagnostic centers support widespread RIS and PACS adoption. Mexico follows with a 25% share, driven by strong demand from both public health institutions and private imaging chains seeking to digitize operations. Argentina contributes around 15% of the market, supported by academic hospitals and urban diagnostic labs modernizing their radiology infrastructure. The LATAM RIS and PACS Market gains strength from these three countries due to their relatively better infrastructure, stable vendor networks, and early-stage integration of AI-enabled imaging tools. It sees continued growth from cloud-based deployments that reduce IT maintenance costs for smaller institutions.

Emerging Markets Like Chile, Colombia, and Peru Show Strong Growth Potential

Chile, Colombia, and Peru collectively account for nearly 14% of the regional RIS and PACS market and present high growth opportunities. These countries are improving healthcare IT infrastructure, particularly in urban areas, through strategic health modernization plans. Cloud-based RIS and PACS systems are becoming attractive in these regions due to limited in-house IT resources and high scalability requirements. The LATAM RIS and PACS Market benefits from local government interest in enhancing diagnostic access in remote areas, which fuels interest in mobile-compatible and web-based platforms. It also reflects vendor efforts to expand footprint in secondary cities where adoption remains low but demand is rising. Partnerships between healthcare providers and regional IT firms help tailor solutions to local regulatory and workflow needs.

Rest of Latin America Offers Long-Term Potential Despite Infrastructure Gaps

Central America and smaller South American nations, including Ecuador, Bolivia, and Paraguay, hold the remaining 8% of the LATAM RIS and PACS Market. Adoption remains limited due to financial constraints, fragmented healthcare delivery, and low IT readiness in public facilities. However, market potential exists as these countries invest in basic digitization and telemedicine capabilities. It gains relevance in small-scale hospitals looking for low-cost, cloud-based platforms that can integrate with basic EMR systems. Vendors that offer simplified, modular solutions with strong remote support can position themselves competitively in these underserved areas. Market maturity remains low but signals opportunity for long-term expansion through targeted education, training, and infrastructure development.

Key Player Analysis:

- Allscripts Healthcare Solutions, Inc.

- Hoffmann-La Roche Ltd

- Carestream Health, Inc.

- Cerner Corporation

- Epic Systems Corporation

- Merge Healthcare Incorporated

- GE Healthcare

- Brit Systems

- Pixeon

- Other Key Players

Competitive Analysis:

The LATAM RIS and PACS Market features a mix of global and regional players competing on technology, customization, and service support. Leading companies such as GE Healthcare, Siemens Healthineers, Philips Healthcare, Fujifilm, and Agfa-Gevaert dominate with strong brand presence and scalable enterprise solutions. Regional vendors, including Pixeon and Novarad Latin America, offer cost-effective and localized platforms tailored to mid-sized hospitals and diagnostic centers. The LATAM RIS and PACS Market sees rising demand for cloud-based, AI-integrated, and interoperable systems, driving vendors to innovate in user interface design, mobile accessibility, and data security. It favors companies that provide flexible deployment models and strong after-sales service. Strategic partnerships with healthcare institutions and IT providers remain critical for market expansion. Competitive advantage depends on the ability to deliver seamless integration with EMRs, meet regional compliance standards, and adapt to variable infrastructure capabilities across Latin American countries.

Recent Developments:

- In March 2025, F. Hoffmann-La Roche AG entered into the largest ever single asset partnership with Zealand Pharma A/S, valued at up to $5.3 billion. This deal focuses on co-developing and co-commercializing petrelintide monotherapy and potential combination products for obesity treatment, mainly targeting the U.S. and European markets. Although not directly tied to RIS or PACS, this partnership demonstrates Roche’s continued investment in healthcare collaborations and innovation.

- In June 2024, Carestream Health secured a crucial business partner agreement in Peru with Distribuidora Diagnostica Medica SAC (DMD). Under this partnership, DMD became an exclusive distributor for Carestream in the region, purchasing 80 DryView printers with significant projected print volumes for 2024 and beyond.

Market Concentration & Characteristics:

The LATAM RIS and PACS Market is moderately concentrated, with a few global players holding a significant share alongside several regional vendors offering tailored solutions. It features a competitive landscape shaped by product differentiation, deployment flexibility, and service reliability. Leading companies such as GE Healthcare, Philips, Siemens Healthineers, and Fujifilm dominate the high-end segment, while local providers like Pixeon and Novarad address the needs of mid-sized and public hospitals. The market favors vendors that offer scalable, cloud-based platforms with strong integration capabilities and localized support. It is characterized by growing demand for interoperability, mobile access, and AI-enhanced tools, which drive innovation across offerings. Vendors that adapt to varied infrastructure levels and compliance requirements maintain a strong position in this dynamic environment.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage:

The research report offers an in-depth analysis based on product type, application, and end user. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Increased adoption of cloud-based RIS and PACS solutions will drive cost efficiency and scalability across mid-sized and rural healthcare facilities.

- Government-backed healthcare digitization programs are expected to accelerate system implementation in public hospitals.

- AI-integrated imaging platforms will gain traction, improving diagnostic accuracy and reducing radiologist workload.

- Mobile compatibility and remote access capabilities will expand imaging services in underserved regions.

- Local vendors offering customizable, low-cost solutions will strengthen their presence in secondary markets.

- Interoperability with EMRs and other clinical systems will become a standard requirement for procurement.

- Teleradiology demand will grow, supporting cross-border diagnostics and regional collaboration.

- Private healthcare investments will rise, especially in urban centers, increasing system upgrades.

- Strategic partnerships between technology providers and healthcare networks will drive integrated solutions.

- Vendor success will depend on offering secure, scalable platforms that comply with evolving data protection regulations.