Market Overview

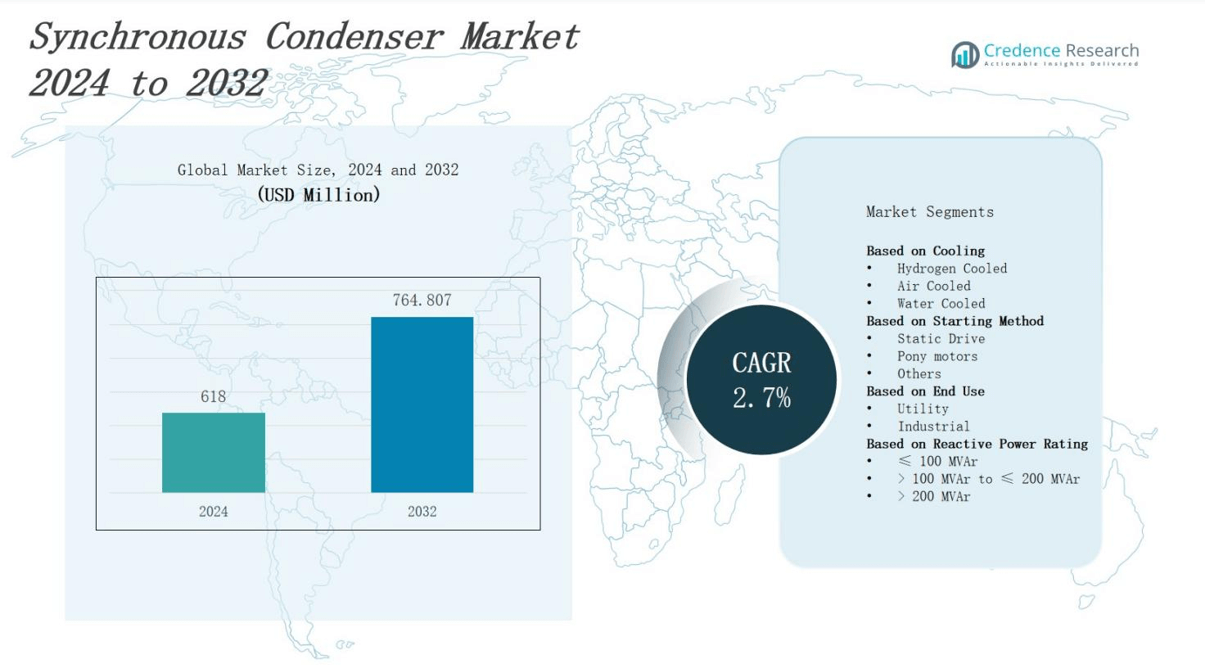

The synchronous condenser market is projected to grow from USD 618 million in 2024 to USD 764.807 million by 2032, registering a compound annual growth rate (CAGR) of 2.7%.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Synchronous Condenser Market Size 2024 |

USD 618 million |

| Synchronous Condenser Market, CAGR |

2.7% |

| Synchronous Condenser Market Size 2032 |

USD 764.807 million |

The synchronous condenser market grows steadily driven by increasing demand for grid stability and reactive power compensation amid rising renewable energy integration. Utilities and industries adopt synchronous condensers to enhance voltage regulation, reduce power outages, and improve power quality. Technological advancements in condenser design improve efficiency and reduce operational costs. Growing investments in smart grid infrastructure and stringent regulations on power reliability further stimulate market expansion. Trends include the integration of digital monitoring and control systems, adoption of compact and modular condensers, and rising preference for eco-friendly solutions that minimize environmental impact. These factors collectively strengthen market momentum globally.

The synchronous condenser market spans key regions including North America, Europe, Asia-Pacific, and the Rest of the World, with North America holding the largest share due to advanced grid infrastructure and renewable integration. Europe and Asia-Pacific follow, driven by stringent regulations and rapid electrification, respectively, while the Rest of the World focuses on grid modernization amid growing energy demand. Leading players such as ABB, General Electric, Hitachi Energy Ltd., Alstom SA, Bharat Heavy Electricals Limited, ANDRITZ, Baker Hughes, Eaton, Doosan, BRUSH, Ansaldo Energia, and Ingeteam compete globally, offering innovative and region-specific solutions.

Market Insights

- Synchronous condenser market projected to grow from USD 618 million in 2024 to USD 764.807 million by 2032 at 2.7% CAGR.

- Rising renewable energy integration drives demand for grid stability and reactive power compensation.

- Synchronous condensers improve voltage regulation, reduce flicker, and enhance power quality.

- Technological advances in digital monitoring and modular designs boost efficiency and lower costs.

- Smart grid investments and regulations on power reliability support market growth.

- North America leads with 35% market share; Europe 28%; Asia-Pacific 22%; Rest of World 15%.

- Challenges include high upfront costs, installation complexity, and competition from alternative technologies.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Integration of Renewable Energy Sources Driving Demand

The synchronous condenser market experiences significant growth due to the increasing integration of renewable energy sources such as wind and solar power into electrical grids. These renewable sources cause voltage fluctuations and instability, creating a critical need for reactive power compensation and voltage regulation. The synchronous condenser provides reliable grid support by stabilizing voltage levels and improving power quality. Utilities prioritize synchronous condensers to maintain grid reliability amid the variable nature of renewables, accelerating market adoption worldwide.

- For instance, NTPC Limited has converted retiring thermal power plants into synchronous condensers to support grid stability near renewable generation sites, effectively managing voltage regulation and reactive power compensation.

Enhancement of Grid Stability and Power Quality

Grid operators and industries deploy synchronous condensers to improve overall grid stability and enhance power quality. It supports voltage control, reduces flicker, and mitigates power disturbances caused by fluctuating loads. With growing industrialization and urbanization, the demand for stable and high-quality power supply rises sharply. The synchronous condenser’s ability to respond rapidly to grid faults and maintain system inertia strengthens its appeal, encouraging widespread installation across transmission and distribution networks.

- For instance, Siemens Energy supplies synchronous condensers with capabilities up to 1,300 MVA, providing necessary system inertia and reactive power to stabilize voltage and support grids with high renewable energy penetration.

Technological Advancements Boosting Operational Efficiency

The synchronous condenser market benefits from continuous technological improvements that enhance performance and reduce operational costs. Modern designs incorporate advanced control systems, digital monitoring, and automation features, enabling better real-time management and predictive maintenance. Compact and modular synchronous condensers simplify installation and integration into existing infrastructure. These innovations improve energy efficiency and lifespan, making synchronous condensers more attractive for utilities and industrial end-users seeking cost-effective grid solutions.

Increasing Investments and Regulatory Support Accelerate Market Growth

Investment in smart grid infrastructure and government policies focused on power reliability support synchronous condenser market expansion. Regulatory mandates on grid stability and renewable integration compel utilities to adopt advanced reactive power compensation technologies. Public and private funding for modernization projects promotes synchronous condenser installations in aging grids. It aligns with environmental regulations by providing an eco-friendly alternative to traditional capacitor banks, reinforcing its role in sustainable energy systems worldwide.

Market Trends

Adoption of Digital Monitoring and Advanced Control Systems

The synchronous condenser market increasingly integrates digital monitoring and advanced control technologies to optimize performance. It enables real-time data collection, remote diagnostics, and predictive maintenance, improving reliability and reducing downtime. Utilities use these intelligent systems to enhance operational efficiency and quickly respond to grid fluctuations. The shift toward digitalization supports proactive asset management, extending the service life of synchronous condensers and lowering overall maintenance costs, driving widespread acceptance in modern grids.

- For instance, Valmet’s DNA Synchronous Condenser Automation integrates advanced control, protection, and information management systems to optimize the condenser’s dynamic response and ensure precise grid stability management.

Shift Toward Compact and Modular Designs for Flexible Deployment

The market experiences a growing trend toward compact and modular synchronous condenser designs that facilitate easier installation and scalability. It allows utilities and industries to deploy condensers in constrained spaces and expand capacity based on demand. Modular units reduce project timelines and lower initial capital expenditure by enabling phased implementation. This trend supports grid modernization efforts and addresses evolving power system requirements efficiently, making synchronous condensers more adaptable to diverse infrastructure conditions.

- For instance, ABB offers pre-designed synchronous condenser packages up to 80 MVAr that are small, easy to transport, and integrate quickly into substations or microgrids, reducing installation time to as little as 12 months.

Increasing Focus on Environmentally Friendly and Sustainable Solutions

Environmental sustainability influences the synchronous condenser market strongly, prompting the development of eco-friendly technologies. It replaces or supplements conventional capacitor banks, offering reduced environmental impact through lower emissions and enhanced energy efficiency. Manufacturers prioritize materials and designs that minimize noise and heat generation. The synchronous condenser’s ability to support renewable energy integration aligns with global decarbonization goals, encouraging utilities to adopt cleaner, sustainable grid stabilization methods.

Rising Integration with Smart Grid and Renewable Energy Projects

The synchronous condenser market benefits from rising integration within smart grid and renewable energy projects worldwide. It provides essential support to grids facing increased variability from solar and wind power sources. Grid operators incorporate synchronous condensers to maintain frequency stability and inertia, crucial for reliable energy delivery. The trend toward hybrid solutions combining synchronous condensers with energy storage and power electronics boosts overall grid resilience, positioning it as a key component in future-proof energy infrastructure.

Market Challenges Analysis

High Initial Capital Expenditure and Installation Complexity

The synchronous condenser market faces challenges related to its high upfront costs and installation complexity. It requires substantial capital investment for procurement, site preparation, and commissioning, which can deter smaller utilities and emerging markets from adoption. The size and weight of synchronous condensers demand specialized infrastructure and skilled labor, extending project timelines and increasing overall expenses. Integration into existing power grids often involves complex engineering and coordination with other grid assets, which may further complicate deployment and increase costs.

Competition from Alternative Technologies and Operational Maintenance

The market encounters competition from emerging reactive power compensation solutions such as static VAR compensators (SVCs) and power electronic devices, which offer faster response times and lower space requirements. It struggles to maintain cost-effectiveness compared to these alternatives, especially in applications with limited grid inertia needs. The synchronous condenser requires regular maintenance to ensure optimal performance, involving skilled personnel and downtime that can impact grid operations. These operational challenges, combined with evolving technology preferences, create barriers to widespread adoption despite its proven benefits in grid stability.

Market Opportunities

Expanding Renewable Energy Integration Creating Demand for Grid Support Solutions

The synchronous condenser market presents significant opportunities due to the accelerating integration of renewable energy sources worldwide. It addresses the critical need for voltage regulation, reactive power compensation, and system inertia in grids with high renewable penetration. Utilities and grid operators increasingly seek synchronous condensers to stabilize fluctuating power inputs from wind and solar plants. Growing investments in renewable infrastructure and government incentives for clean energy projects further drive demand, positioning synchronous condensers as essential components in modernizing and future-proofing electrical networks.

Growing Smart Grid Initiatives and Infrastructure Modernization Efforts

The market benefits from expanding smart grid programs and infrastructure modernization efforts across developed and developing regions. It plays a vital role in enhancing grid flexibility, reliability, and resilience through improved voltage control and fault response capabilities. Utilities prioritize synchronous condensers to upgrade aging transmission and distribution systems and comply with stringent regulatory standards on power quality. Integration with advanced digital controls and predictive maintenance systems unlocks additional value, enabling better asset management and operational efficiency. These developments create a favorable environment for market growth and technology adoption.

Market Segmentation Analysis:

By Cooling

The synchronous condenser market segments cooling methods into hydrogen cooled, air cooled, and water cooled types. Hydrogen cooled condensers provide superior heat dissipation and higher efficiency, making them suitable for large-scale applications. Air cooled units offer simpler installation and lower maintenance costs, favored in moderate-capacity environments. Water cooled condensers deliver effective thermal management in confined spaces but require additional infrastructure. Each cooling type addresses specific operational needs, allowing utilities and industries to select solutions based on performance, cost, and environmental conditions.

- For instance, ANDRITZ supplied hydrogen-cooled synchronous condensers to the Marmeleiro 2 and Livramento 3 substations in Brazil, leveraging hydrogen’s superior cooling for high-capacity grid stability at voltages up to 525 kV.

By Starting Method

The synchronous condenser market categorizes products by starting methods, including static drive, pony motors, and others. Static drive starters offer precise control and smooth acceleration, enhancing operational reliability. Pony motors provide robust and straightforward starting mechanisms, preferred in conventional setups. Other starting methods cater to specialized requirements, optimizing condenser performance in varied grid conditions. This segmentation allows stakeholders to choose the most efficient and compatible starting system for their specific grid integration challenges.

- For instance, GE’s static frequency converter starters provide precise control and smooth acceleration, enhancing synchronous condenser reliability in modern grids.

By End Use

The market divides end-use applications into utility and industrial segments. Utilities primarily deploy synchronous condensers for grid stability, voltage regulation, and reactive power support in transmission and distribution networks. Industrial users leverage these condensers to maintain power quality, reduce outages, and protect sensitive equipment in manufacturing plants and large facilities. It plays a critical role in both sectors by enhancing energy reliability and supporting infrastructure modernization, driving demand across diverse operational environments.

Segments:

Based on Cooling

- Hydrogen Cooled

- Air Cooled

- Water Cooled

Based on Starting Method

- Static Drive

- Pony motors

- Others

Based on End Use

Based on Reactive Power Rating

- ≤ 100 MVAr

- > 100 MVAr to ≤ 200 MVAr

- > 200 MVAr

Based on the Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

North America

North America commands the largest share of the synchronous condenser market, holding 35% of the global revenue. It leads due to early adoption of advanced grid stabilization technologies and significant investments in renewable energy infrastructure. Utilities in the region prioritize synchronous condensers to address grid reliability challenges from increasing wind and solar capacity. Regulatory frameworks emphasize power quality and system inertia, driving widespread deployment. Strong focus on modernizing aging power infrastructure also supports market growth. It continues to benefit from technological innovations and government incentives promoting sustainable energy solutions.

Europe

Europe holds 28% of the synchronous condenser market share, driven by stringent regulations on grid stability and power quality. Countries invest heavily in renewable energy projects, requiring effective reactive power compensation and voltage regulation. The synchronous condenser market gains momentum through large-scale transmission upgrades and smart grid initiatives. It serves to enhance system resilience against intermittent renewable generation. European utilities focus on reducing carbon emissions while ensuring reliable electricity supply. The market expands due to favorable policies encouraging clean energy integration and infrastructure modernization.

Asia-Pacific

Asia-Pacific accounts for 22% of the synchronous condenser market and demonstrates rapid growth due to increasing electrification and renewable capacity expansion. Emerging economies invest in grid reinforcement to manage fluctuating renewable inputs and rising power demand. It benefits from government incentives aimed at upgrading transmission and distribution networks. The region’s urbanization and industrialization trends further propel synchronous condenser installations. Key countries focus on balancing grid stability with clean energy targets, fostering strong market opportunities. The market reflects ongoing infrastructure development and modernization programs.

Rest of the World

The Rest of the World represents 15% of the synchronous condenser market, encompassing Latin America, the Middle East, and Africa. These regions experience growing demand for grid stability solutions amid increasing renewable energy adoption. Investments target modernizing aging grids and expanding capacity to meet rising electricity needs. Synchronous condensers provide critical support in remote and industrial areas where power quality challenges persist. The market growth depends on infrastructure funding and regulatory support. It gradually gains traction as utilities prioritize reliable and efficient power delivery systems.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Baker Hughes

- Hitachi Energy Ltd.

- BRUSH

- Alstom SA

- Eaton

- Doosan

- General Electric

- Bharat Heavy Electricals Limited

- Ansaldo Energia

- ABB

- Ingeteam

- ANDRITZ

Competitive Analysis

The synchronous condenser market features strong competition among established global players focusing on innovation, quality, and service differentiation. Leading companies such as ABB, General Electric, Hitachi Energy Ltd., Alstom SA, and Bharat Heavy Electricals Limited invest heavily in research and development to enhance product efficiency and reliability. It emphasizes developing advanced digital control systems and modular designs to meet evolving grid requirements. Companies also pursue strategic partnerships and regional expansions to strengthen their market presence. Firms like ANDRITZ, Baker Hughes, Eaton, Doosan, BRUSH, Ansaldo Energia, and Ingeteam compete by offering customized solutions tailored to utility and industrial applications. The market remains dynamic with ongoing technological advancements and increasing demand for sustainable and efficient grid stabilization solutions, compelling players to continuously improve their product portfolios and operational capabilities.

Recent Developments

- In March 2024, ABB announced it will deliver a third synchronous condenser to the Faroe Islands to support their transition to 100% green energy by 2030.

- In April 2024, Hitachi Energy partnered with SP Energy Networks to design and deliver a combined SVC Light® STATCOM and synchronous condenser solution, enhancing grid stability and renewable energy flow in the UK.

- In May 2025, ANDRITZ and GE Vernova formed a joint venture to install two synchronous condensers at the Bakersfield substation in West Texas, strengthening grid stability amid growing renewable demands.

- In December 2024, Hitachi Energy and Ørsted collaborated to ensure grid stability at Hornsea 4, Europe’s first offshore wind farm using Enhanced STATCOM technology to integrate 2.4 GW of clean energy into the UK grid.

Market Concentration & Characteristics

The synchronous condenser market exhibits a moderately concentrated competitive landscape dominated by a few key global players such as ABB, General Electric, Hitachi Energy Ltd., and Alstom SA. These companies hold significant market shares due to their strong technological capabilities, extensive product portfolios, and established customer relationships. It operates in a capital-intensive industry requiring high investment in research and development to innovate advanced, efficient, and reliable solutions. Market participants focus on enhancing product efficiency through digital control integration and modular designs to meet diverse grid requirements. The market’s characteristics include a high barrier to entry because of complex manufacturing processes, stringent regulatory standards, and the need for specialized expertise. It serves both utility and industrial sectors, emphasizing grid stability, voltage regulation, and reactive power compensation. The market’s growth depends on ongoing infrastructure modernization and increasing adoption of renewable energy sources demanding robust grid support solutions.

Report Coverage

The research report offers an in-depth analysis based on Cooling, Starting Method, End-Use, Reactive Power Rating and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The synchronous condenser market will expand due to increasing renewable energy integration worldwide.

- Utilities will prioritize synchronous condensers to enhance grid stability and power quality.

- Technological innovation will focus on digital monitoring and advanced control systems.

- Modular and compact designs will gain popularity for flexible and scalable deployment.

- Regulatory policies will encourage adoption of eco-friendly and efficient grid support solutions.

- Investment in smart grid infrastructure will drive synchronous condenser installations.

- Emerging markets will offer significant growth opportunities through grid modernization efforts.

- Competition from alternative reactive power technologies will push manufacturers to innovate continuously.

- Maintenance optimization through predictive analytics will improve operational efficiency.

- Integration of synchronous condensers with energy storage and power electronics will strengthen grid resilience.