Market Overview

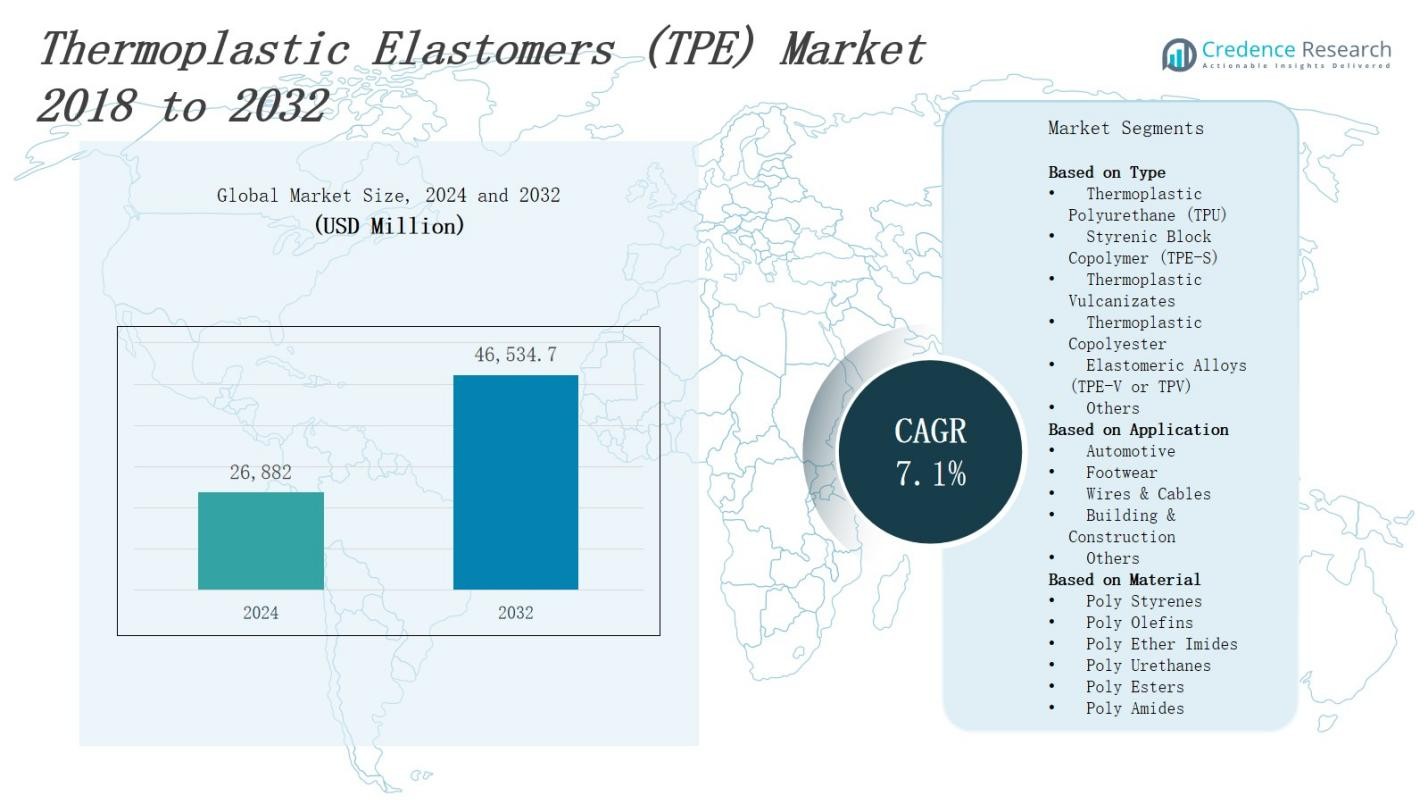

The Thermoplastic Elastomers (TPE) Market is projected to grow from USD 26,882 million in 2024 to USD 46,534.7 million by 2032, expanding at a CAGR of 7.1%.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Thermoplastic Elastomers (TPE) Market Size 2024 |

USD 26,882 Million |

| Thermoplastic Elastomers (TPE) Market, CAGR |

7.1% |

| Thermoplastic Elastomers (TPE) Market Size 2032 |

USD 46,534.7 Million |

The thermoplastic elastomers (TPE) market grows driven by increasing demand for lightweight, flexible, and recyclable materials across automotive, medical, and consumer goods industries. Rising emphasis on sustainability promotes TPE adoption due to its eco-friendly, reusable properties. Innovations in high-performance formulations enhance durability and temperature resistance, expanding application scope. Growing automotive electrification and medical device advancements further boost demand. Additionally, manufacturers focus on cost-effective production and process efficiency, encouraging broader industrial use. The trend toward miniaturization and customization in consumer products also stimulates market growth, positioning TPE as a critical material for modern manufacturing and sustainable design.

The thermoplastic elastomers (TPE) market spans key regions including North America, Europe, Asia-Pacific, and the Rest of the World, with North America leading at 32%, followed by Asia-Pacific at 30%, Europe at 28%, and the Rest of the World at 10%. Each region benefits from specific industry demands and regulatory environments driving TPE adoption. Leading key players such as BASF SE, Arkema S.A., Bayer MaterialScience LLC, and LyondellBasell Industries actively compete across these regions, focusing on innovation, sustainability, and expanded production to capture growing market opportunities globally.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The thermoplastic elastomers (TPE) market is projected to grow from USD 26,882 million in 2024 to USD 46,534.7 million by 2032, expanding at a CAGR of 7.1%.

- Rising demand for lightweight, flexible, and recyclable materials across automotive, medical, and consumer goods industries drives market growth.

- Emphasis on sustainability promotes TPE adoption due to its eco-friendly and reusable properties, supporting circular economy initiatives.

- Innovations in high-performance formulations enhance durability and temperature resistance, broadening application areas.

- Growth in automotive electrification and medical device advancements further increase demand for TPE materials.

- Manufacturers focus on cost-effective production and process efficiency, encouraging broader industrial use and product customization.

- North America leads the market with 32% share, followed by Asia-Pacific at 30%, Europe at 28%, and the Rest of the World at 10%, each driven by unique industry demands and regulatory support.

Market Drivers

Rising Demand for Lightweight and Flexible Materials

The thermoplastic elastomers (TPE) market benefits from growing demand for lightweight and flexible materials across various industries. Manufacturers prioritize materials that reduce product weight without compromising durability, particularly in automotive and consumer electronics sectors. TPEs provide excellent flexibility, impact resistance, and ease of processing, making them ideal substitutes for traditional rubber and plastics. This demand supports product innovation and expands TPE applications in industries seeking enhanced performance and design versatility.

- For instance, General Motors uses polyolefin-based TPEs in numerous car parts including bumpers, door seals, and dashboards to enhance flexibility and reduce vehicle weight, improving fuel efficiency.

Sustainability and Recyclability Focus

Increasing environmental regulations and corporate sustainability goals drive the adoption of thermoplastic elastomers. It offers recyclability and reduces reliance on non-renewable materials compared to conventional elastomers. Companies pursue eco-friendly solutions to meet regulatory compliance and consumer preferences for sustainable products. The TPE market gains momentum from these trends, with manufacturers investing in biodegradable and recyclable formulations that align with circular economy principles and minimize environmental impact.

- For instance, Teknor Apex’s Monprene® TPE, which incorporates 35% sustainable content including post-consumer recycled material and sustainable plastic substitutes, supporting carbon footprint reduction and plastic waste elimination.

Advancements in Medical and Automotive Applications

Technological progress in medical devices and automotive components fuels growth in the thermoplastic elastomers market. It meets stringent requirements for biocompatibility, sterilization resistance, and mechanical performance in medical equipment. In the automotive sector, TPEs contribute to noise reduction, vibration control, and lightweight part manufacturing, which enhance fuel efficiency and safety. This broad application spectrum increases TPE demand and encourages ongoing research to develop specialized grades for emerging industry needs.

Cost Efficiency and Manufacturing Advantages

The thermoplastic elastomers market expands due to its cost-effective production and manufacturing benefits. It simplifies processing by combining the properties of rubber with thermoplastics, enabling faster cycle times and reduced waste. Manufacturers achieve lower overall production costs and greater design flexibility by using TPEs in injection molding and extrusion processes. These economic advantages support adoption across various sectors, making TPE a preferred material for high-volume and customized product manufacturing.

Market Trends

Expansion of TPE Applications in Automotive and Consumer Goods

The thermoplastic elastomers (TPE) market experiences significant growth due to expanding applications in the automotive and consumer goods sectors. It supports the shift toward lightweight vehicle components that enhance fuel efficiency and reduce emissions. Manufacturers use TPE for interior parts, seals, and vibration dampers, benefiting from its flexibility and durability. In consumer goods, TPE improves ergonomics and aesthetics in products such as wearables and household appliances. This diversification drives continuous market expansion.

- For instance, Kraiburg TPE produces compounds used in vehicle interiors and engine compartments, providing weather resistance and high-temperature sealing for major car manufacturers.

Increased Focus on Sustainable and Biodegradable TPE Solutions

Sustainability remains a prominent trend shaping the thermoplastic elastomers market. It drives demand for bio-based and biodegradable TPE variants that reduce environmental footprint. Manufacturers invest in developing formulations using renewable raw materials to meet stricter regulations and consumer expectations. The shift supports circular economy initiatives and aligns with global efforts to minimize plastic waste. Sustainable TPE products gain traction, fostering innovation in eco-friendly material development and broadening market appeal.

- For instance, Teknor Apex emphasizes circularity by producing sustainable TPEs that leverage both renewable and recycled content, fostering collaboration across the supply chain to enhance transparency and eco-friendly material adoption.

Integration of Advanced Manufacturing Technologies

The thermoplastic elastomers market adopts advanced manufacturing technologies that enhance product performance and production efficiency. It leverages automation and precision molding techniques to improve consistency and reduce cycle times. Innovations in compounding and blending enable customization of TPE properties for specialized applications. Digitalization in production monitoring and quality control ensures higher standards and cost savings. These technological advancements strengthen the market position by meeting complex industry demands with superior solutions.

Growing Demand from Healthcare and Medical Device Industries

The healthcare and medical device industries contribute notably to thermoplastic elastomers market growth. It provides biocompatible, sterilizable, and flexible materials required for medical tubing, seals, and wearable devices. The expanding focus on minimally invasive procedures and patient comfort increases TPE utilization. Regulatory approvals and certifications boost confidence in TPE-based medical products. This trend drives manufacturers to innovate specialized grades catering to evolving healthcare requirements, reinforcing the market’s growth trajectory.

Market Challenges Analysis

Raw Material Price Volatility and Supply Chain Disruptions

The thermoplastic elastomers (TPE) market faces challenges from fluctuating raw material prices and supply chain uncertainties. It relies heavily on petrochemical derivatives, making it vulnerable to crude oil price volatility and geopolitical tensions. Supply chain disruptions can delay production schedules and increase manufacturing costs, impacting profitability. Manufacturers must manage inventory efficiently and seek alternative suppliers to mitigate risks. These factors constrain consistent output and affect market stability, posing significant hurdles for growth and scalability.

Performance Limitations and Competitive Material Alternatives

The thermoplastic elastomers market encounters challenges related to performance limitations compared to traditional elastomers and other advanced materials. It sometimes offers lower heat resistance and chemical stability, restricting use in high-demand applications. Competitors such as silicone and vulcanized rubber provide specialized properties that TPE cannot fully match. This limitation forces manufacturers to balance cost advantages against performance requirements. Continuous innovation remains essential to improve TPE properties and maintain competitiveness in evolving industry landscapes.

Market Opportunities

Growth Potential in Emerging Markets and Expanding End-Use Industries

The thermoplastic elastomers (TPE) market holds significant opportunities in emerging economies due to rapid industrialization and urbanization. It can capitalize on increasing demand from automotive, construction, and consumer goods sectors in regions such as Asia-Pacific and Latin America. Rising disposable incomes and infrastructure development create favorable conditions for TPE adoption. Expanding end-use industries seek lightweight, durable, and flexible materials to improve product performance and sustainability, offering a broad growth platform for manufacturers willing to invest in localized production and tailored solutions.

Innovation in Sustainable and High-Performance TPE Formulations

The thermoplastic elastomers market can leverage innovation opportunities by developing sustainable and high-performance TPE variants. It can focus on bio-based raw materials and recyclable formulations that address growing environmental concerns and regulatory pressures. New grades with enhanced heat resistance, chemical stability, and mechanical properties can open doors to advanced applications in medical devices, electronics, and automotive components. Collaborations between material scientists and manufacturers to optimize TPE characteristics will support market expansion and create competitive advantages in a rapidly evolving industry.

Market Segmentation Analysis:

By Type

The thermoplastic elastomers (TPE) market segments prominently by type, with Thermoplastic Polyurethane (TPU) holding a dominant position. TPU offers superior abrasion resistance, flexibility, and chemical stability, making it highly favored across diverse industries. Styrenic Block Copolymer (TPE-S) and Thermoplastic Vulcanizates (TPV) follow closely, providing cost-effective alternatives with good elasticity and processing advantages. Emerging segments like Thermoplastic Copolyester and Elastomeric Alloys (TPE-V or TPV) gain traction due to their enhanced mechanical properties and thermal stability, broadening application scope.

- For instance, Covestro’s Desmopan® TPU series is widely used in the automotive industry for interior trim parts, offering durability, chemical resistance, and UV stability.

By Application

The automotive sector drives substantial demand within the thermoplastic elastomers market. It uses TPE materials for lightweight parts, seals, gaskets, and interior components, improving vehicle performance and fuel efficiency. Footwear and wires & cables applications also contribute meaningfully, leveraging TPE’s flexibility and durability. Building & construction applications benefit from TPE’s weather resistance and insulation properties. Other sectors explore TPE for innovative uses, expanding the overall market reach and reinforcing its versatility across industries.

- For instance, Volkswagen uses TPVs in engine compartment components due to their chemical resistance and temperature endurance.

By Material

The thermoplastic elastomers market segments by material primarily into Poly Olefins, Poly Urethanes, Poly Styrenes, Poly Esters, Poly Amides, and Poly Ether Imides. Poly Olefins and Poly Urethanes dominate due to their excellent mechanical strength, chemical resistance, and ease of processing. Poly Styrenes provide cost-effective solutions for flexible applications, while Poly Esters and Poly Amides offer enhanced thermal and chemical stability. Poly Ether Imides, though niche, find specialized uses in high-performance environments, diversifying material options in the market.

Segments:

Based on Type

- Thermoplastic Polyurethane (TPU)

- Styrenic Block Copolymer (TPE-S)

- Thermoplastic Vulcanizates

- Thermoplastic Copolyester

- Elastomeric Alloys (TPE-V or TPV)

- Others

Based on Application

- Automotive

- Footwear

- Wires & Cables

- Building & Construction

- Others

Based on Material

- Poly Styrenes

- Poly Olefins

- Poly Ether Imides

- Poly Urethanes

- Poly Esters

- Poly Amides

Based on the Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

North America

North America holds the largest share in the thermoplastic elastomers (TPE) market, accounting for 32% of the global revenue. It benefits from a well-established automotive and consumer goods industry, which drives steady demand for lightweight and flexible materials. The region’s strong focus on sustainability and regulatory support encourages the adoption of recyclable and eco-friendly TPE products. Leading manufacturers invest heavily in research and development to improve product performance. It also enjoys advanced manufacturing infrastructure and a robust supply chain, supporting consistent market growth.

Europe

Europe captures 28% of the thermoplastic elastomers market share due to stringent environmental regulations and a mature manufacturing base. The region prioritizes sustainable materials, fueling demand for bio-based and recyclable TPE formulations. Automotive, construction, and medical sectors contribute significantly to market expansion. Europe supports innovation through government incentives and collaboration between industry and academia. It also emphasizes circular economy principles, which align with TPE’s recyclable nature. Manufacturers focus on customized solutions to meet specific application needs.

Asia-Pacific

Asia-Pacific represents 30% of the global thermoplastic elastomers market, driven by rapid industrialization and urbanization in countries like China, India, and Japan. Growing automotive production, expanding consumer electronics, and footwear industries boost regional demand. It benefits from cost-effective manufacturing and increasing foreign investments. The rising middle-class population creates strong consumption prospects for TPE-based products. The region shows increasing focus on environmental compliance, prompting gradual adoption of sustainable TPE variants. Local manufacturers continue to scale operations to meet rising demand.

Rest of the World

The Rest of the World holds 10% market share in the thermoplastic elastomers market, with emerging economies in Latin America, Middle East, and Africa contributing to growth. These regions witness growing automotive and construction activities, creating new opportunities for TPE materials. Limited manufacturing infrastructure and regulatory challenges restrict rapid market expansion. However, increasing foreign direct investments and technology transfer initiatives encourage market development. It remains a potential growth area for manufacturers targeting untapped markets and diverse applications.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Dynasol Elastomers LLC

- Arkema S.A.

- Nippon Polyurethane Industry Company Ltd.

- Bayer MaterialScience LLC

- Teknor APEX Company

- China Petroleum & Chemical Corporation

- Advanced Elastomer Systems L.P.

- BASF SE

- Yantai Wanhua Polyurethane Co. Ltd.

- Avient Corporation

- LyondellBasell Industries

- TSRC Corporation

Competitive Analysis

The thermoplastic elastomers (TPE) market features intense competition among key global players striving to enhance product portfolios and expand geographic presence. Leading companies focus on innovation to develop high-performance and sustainable TPE formulations that meet evolving industry standards. It witnesses frequent strategic initiatives such as mergers, acquisitions, and partnerships to strengthen market position and increase production capabilities. Manufacturers emphasize cost optimization and advanced manufacturing processes to maintain competitive pricing without compromising quality. The market also sees growing investments in research and development to improve material properties and application versatility. Companies compete to serve end-use sectors including automotive, medical, and consumer goods, driving differentiation through specialized solutions. This competitive environment pushes the industry toward continuous improvement and rapid adoption of emerging technologies.

Recent Developments

- In March 2023, Arkema SA and Engie SA entered into an agreement in France for the supply of 300 GWh per year of renewable biomethane, aiming to lower the carbon footprint of Arkema’s 3D printing materials.

- In September 2024, KRAIBURG TPE (Germany) launched a new TPE compound series specifically developed for automotive exterior applications, highlighting growing focus on automotive markets within the TPE sector.

- In March 2023, Arkema S.A. partnered with Engie S.A. to supply 300 GWh/year of renewable biomethane in France, supporting sustainability initiatives in its operations.

- In January 2025, GEON Performance Solutions acquired Foster Corporation to enhance its medical polymer portfolio. Foster’s expertise in biomedical compounds strengthens GEON’s healthcare offerings.

Market Concentration & Characteristics

The thermoplastic elastomers (TPE) market demonstrates a moderately concentrated competitive landscape dominated by several global key players that control a significant share of production and innovation. It features leading manufacturers such as BASF SE, Arkema S.A., Bayer MaterialScience LLC, and LyondellBasell Industries, which leverage strong research and development capabilities to enhance product performance and sustainability. The market’s characteristics include rapid technological advancements, increasing demand for eco-friendly materials, and diversification across various end-use industries. It balances scale advantages with the need for customization, allowing both large and mid-sized companies to compete effectively. Production processes emphasize cost efficiency and environmental compliance to meet stringent regulatory requirements. It maintains dynamic growth due to expanding applications in automotive, medical, and consumer goods sectors, while facing challenges like raw material price volatility. This combination of innovation, strategic investments, and market demand shapes a competitive yet opportunity-rich environment within the thermoplastic elastomers market.

Report Coverage

The research report offers an in-depth analysis based on Type, Application, Material and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The thermoplastic elastomers market will expand driven by rising demand for lightweight and flexible materials.

- It will witness increased adoption due to growing sustainability and recyclability requirements.

- Innovations in high-performance TPE formulations will open new application areas.

- The automotive industry will continue to be a major consumer of TPE products.

- Medical and healthcare sectors will drive demand for biocompatible and sterilizable TPE materials.

- Emerging economies will offer significant growth opportunities for TPE manufacturers.

- Manufacturers will focus on cost-efficient production techniques to enhance competitiveness.

- Technological advancements will improve TPE properties such as durability and temperature resistance.

- Customization and miniaturization trends in consumer goods will stimulate TPE use.

- Collaboration between material developers and end-users will accelerate product innovation.