| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Black Pepper Market Size 2024 |

USD 4,266.73 million |

| Black Pepper Market, CAGR |

4.60% |

| Black Pepper MarketSize 2032 |

USD 6,274.33 million |

Market Overview:

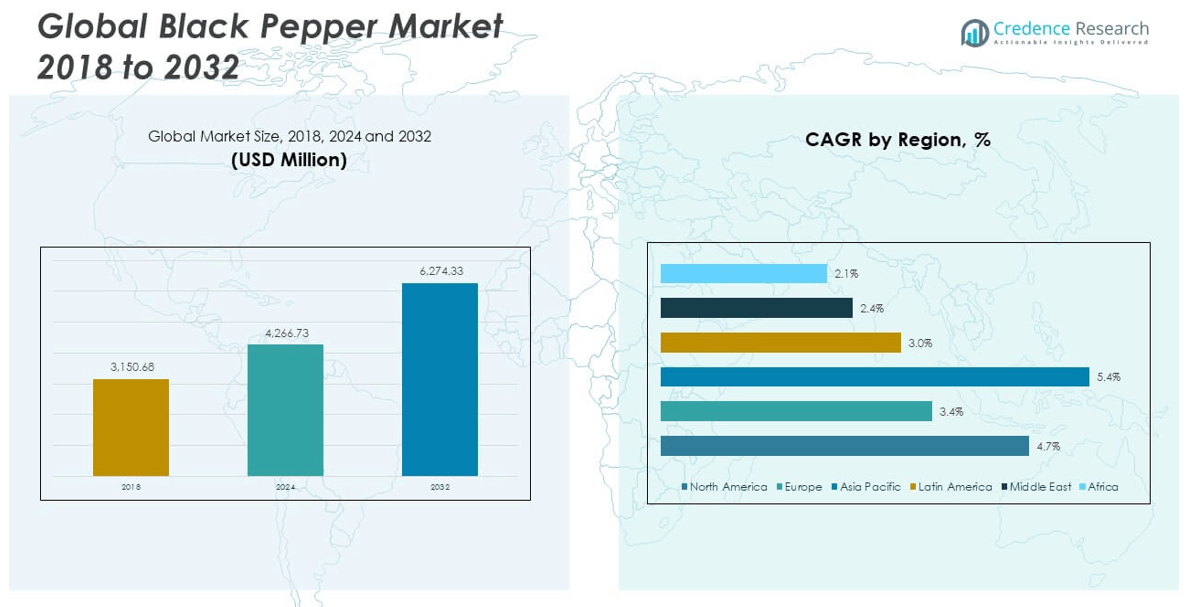

The Global Black Pepper Market size was valued at USD 3,150.68 million in 2018 to USD 4,266.73 million in 2024 and is anticipated to reach USD 6,274.33 million by 2032, at a CAGR of 4.60% during the forecast period.

The global black pepper market is experiencing consistent growth due to a combination of health trends, culinary demand, and supply-side advancements. Rising awareness of black pepper’s therapeutic benefits—such as its antioxidant, anti-inflammatory, and digestive properties—has positioned it as a preferred ingredient in both nutraceuticals and functional foods. Additionally, the processed food industry, including ready-to-eat meals and fast-food chains, continues to rely heavily on black pepper for flavor enhancement, stimulating demand across global markets. The organic and clean-label movement is further reshaping the market, with a growing share of consumers seeking non-GMO, chemical-free spice options. Market players are also leveraging digital retail platforms, innovative packaging, and product diversification to increase accessibility and shelf appeal. Simultaneously, improvements in agricultural practices, particularly in Vietnam and India, are optimizing yield quality and enabling more stable global supply chains, further supporting sustained market expansion.

Asia-Pacific dominates the global black pepper market, driven by high production volumes from countries such as Vietnam, India, and Indonesia. Vietnam leads the world in black pepper exports, benefiting from advanced cultivation techniques, government support, and efficient supply chains. India plays a dual role as both a major producer and a rapidly expanding consumer, supported by its strong culinary traditions and growing packaged food industry. North America ranks as a key importer, propelled by increasing consumer interest in ethnic cuisines, organic spices, and health-based dietary choices. The U.S., in particular, shows rising demand through foodservice channels and e-commerce. In Europe, demand is also growing steadily due to clean-label trends, premium product preferences, and heightened culinary experimentation. Meanwhile, emerging regions such as the Middle East & Africa and South America are witnessing rising consumption, fueled by urbanization, economic development, and the integration of black pepper into local and industrial food applications.

Market Insights:

- The Global Black Pepper Market reached USD 4,266.73 million in 2024 and is projected to grow to USD 6,274.33 million by 2032, expanding at a CAGR of 4.60%.

- Rising demand for functional foods and dietary supplements is driving the use of black pepper in nutraceutical applications due to its antioxidant and digestive properties.

- Processed food growth, especially in ready-to-eat meals and fast food, is fueling consistent commercial demand for black pepper across global markets.

- The clean-label movement is encouraging producers to offer organic, traceable, and chemical-free pepper varieties, which appeal to health-conscious consumers.

- Vietnam, India, and Indonesia lead global production, with Vietnam dominating exports through advanced cultivation techniques and efficient supply chains.

- Market volatility due to weather conditions, yield inconsistency, and shifting trade policies presents challenges for pricing and supply stability.

- Asia-Pacific leads in market share, while North America and Europe show rising consumption through e-commerce and foodservice expansion, supported by consumer interest in global cuisines.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Rising Health Awareness and Functional Benefits Are Strengthening Consumer Preference

Growing consumer interest in natural remedies and functional ingredients is significantly influencing the Global Black Pepper Market. Black pepper is widely recognized for its antioxidant, anti-inflammatory, and digestive properties, which appeal to health-conscious individuals seeking natural solutions. The inclusion of piperine in wellness formulations and dietary supplements has expanded black pepper’s application scope beyond traditional culinary use. Nutraceutical manufacturers increasingly incorporate it into products aimed at boosting metabolism and nutrient absorption. This functional positioning supports consistent demand across both developed and emerging markets. It is also gaining popularity in traditional medicine systems, reinforcing its reputation as a therapeutic spice.

Expansion of Processed Food and Foodservice Sectors Is Fueling Commercial Demand

The processed food and foodservice industries play a central role in driving consumption of black pepper. Its use in ready-to-eat meals, snacks, sauces, seasonings, and instant food categories continues to increase. Foodservice operators, including quick-service restaurants and gourmet establishments, rely on black pepper to enhance flavor profiles and meet diverse culinary preferences. With rising urbanization and time-constrained lifestyles, demand for flavor-packed convenience foods has surged. This trend supports bulk procurement by commercial buyers and strengthens global supply chains. The Global Black Pepper Market benefits from its versatility, as it complements a wide range of cuisines and processing formats.

Rising Demand for Organic, Clean-Label, and Traceable Products Is Reshaping the Market

Shifting consumer expectations around food transparency, safety, and environmental responsibility are reshaping the black pepper supply chain. Organic and sustainably sourced variants are gaining traction, with retailers and manufacturers responding by expanding certified offerings. A growing segment of buyers actively seeks clean-label spices, free from synthetic additives or chemical processing. This shift is prompting producers to invest in traceability systems, quality certifications, and eco-friendly cultivation practices. It is also driving innovation in packaging and labeling to communicate product origin and purity. These developments are elevating product differentiation and enabling premium pricing opportunities.

- For example, Olam Food Ingredients expanded its AtSource platform to cover 100% of its Vietnamese black pepper supply chain in 2023, providing real-time data on carbon footprint, pesticide use, and labor practices for over 8,000 smallholder farmers.

Improved Cultivation Practices and Supply Chain Efficiencies Are Supporting Global Distribution

Advancements in black pepper farming and post-harvest handling have enhanced yield quality and consistency. Leading producers such as Vietnam and India are adopting modern irrigation, pest control, and fermentation techniques to boost output and reduce crop loss. Mechanization and digital monitoring tools are also improving farm-level productivity and traceability. Exporters are streamlining logistics and storage infrastructure, ensuring better preservation during long-distance transportation. It enables reliable supply to major consumption markets while maintaining competitive pricing. The Global Black Pepper Market continues to benefit from increased production efficiency and supply chain stability.

- For example, Vinaseed, a leading Vietnamese agritech firm, deployed drip irrigation and integrated pest management systems across 2,500 hectares of contracted black pepper farms, resulting in a increase in average yield.

Market Trends:

Technological Integration in Spice Processing Is Enhancing Quality and Consistency

Technological advancements are playing a pivotal role in elevating the quality and standardization of black pepper production. Automated drying systems, optical sorters, and advanced grinding machines are enabling precise processing while reducing contamination risks. These innovations are helping manufacturers comply with stringent food safety regulations in international markets. Investment in processing infrastructure is also increasing in key producing countries, facilitating higher export readiness. Digital tools such as blockchain and IoT are being introduced to monitor quality and traceability throughout the value chain. The Global Black Pepper Market is seeing an improvement in processing efficiency and traceable product integrity.

- For example, ofi’s proprietary steam sterilization technology ensures black pepper meets international microbial safety standards (less than 1,000 CFU/g for total plate count), while advanced optical sorters like the TOMRA 5B achieve up to 98% accuracy in removing foreign material and defective peppercorns

Emergence of Gourmet and Specialty Pepper Varieties Is Driving Premiumization

Consumer interest in regional and specialty spice variants is prompting producers to develop unique black pepper offerings. Varieties such as Tellicherry, Malabar, and Lampong are gaining attention for their distinct aroma, size, and flavor intensity. Chefs and culinary professionals are influencing demand for such high-grade peppers in gourmet cooking. Retailers are responding by expanding shelf space for single-origin, hand-harvested, or sun-dried products with elevated sensory appeal. It is creating new market segments within the spice category, where consumers are willing to pay a premium for exclusivity and origin-based differentiation. The Global Black Pepper Market is gradually shifting toward a more segmented, value-driven landscape.

Growing Influence of E-Commerce and Direct-to-Consumer Channels Is Reshaping Sales Models

The rise of e-commerce platforms and direct-to-consumer business models is transforming how black pepper reaches end users. Online retail has become a key distribution channel, particularly for organic, gourmet, and small-batch pepper products. Startups and artisanal spice brands are leveraging digital platforms to bypass traditional supply chains and engage directly with niche customer bases. Subscription services, curated spice kits, and storytelling-based branding are also gaining popularity in the digital space. It is enabling smaller producers to access global markets with lower entry barriers and build loyal consumer communities. The Global Black Pepper Market is witnessing a shift in distribution dynamics through digital engagement.

Climate Variability and Environmental Pressures Are Influencing Cultivation Practices

Changing weather patterns, erratic rainfall, and rising temperatures are exerting pressure on black pepper farming regions. These environmental changes are prompting a reevaluation of cultivation zones and farming practices to maintain crop viability. Growers are adopting climate-resilient strategies such as intercropping, shade management, and water conservation techniques. Research institutions and agricultural agencies are working with farmers to introduce pepper varieties better suited to fluctuating conditions. It is driving investment in sustainability-focused farming and adaptive agro-technologies. The Global Black Pepper Market is increasingly affected by the interplay between climate risk and agricultural innovation.

- For instance, the Indian Institute of Spices Research (IISR) partnered with local cooperatives to promote intercropping with nitrogen-fixing species, improving soil organic carbon by 0.4% annually and reducing input costs by 10%. These adaptive measures are documented in annual sustainability reports and have been recognized by the Sustainable Spice Initiative for their measurable impact on farm resilience and environmental stewardship.

Market Challenges Analysis:

Price Volatility and Supply Chain Disruptions Are Affecting Market Stability

The black pepper industry remains vulnerable to price fluctuations driven by inconsistent production volumes, weather variability, and changing export policies. Key producing countries such as Vietnam and India experience yield disruptions due to climate anomalies, pest outbreaks, and limited access to farm inputs. These issues create supply imbalances that directly affect global pricing and contract stability. Sudden shifts in export tariffs, quality regulations, and currency exchange rates also introduce uncertainty for exporters and buyers. The Global Black Pepper Market must navigate these variables while maintaining product consistency and fulfilling long-term contracts. It faces the ongoing challenge of balancing supply-side risks with pricing predictability to protect margins and trade flow.

Quality Control and Adulteration Concerns Are Undermining Consumer Trust

Maintaining high product quality remains a persistent challenge, particularly for exporters catering to regulated markets in North America and Europe. Issues such as microbial contamination, pesticide residue, and adulteration with substandard material threaten brand reputation and regulatory compliance. Small-scale producers and fragmented supply chains often lack access to adequate testing, traceability systems, and certification processes. Importing countries are tightening food safety standards, placing pressure on producers to meet strict benchmarks. The Global Black Pepper Market must invest in upgraded testing infrastructure, farmer education, and third-party certification to meet rising expectations. It must prioritize transparency and quality assurance to sustain consumer trust and market access.

Market Opportunities:

Expanding Use in Non-Culinary Sectors Is Opening New Revenue Streams

The application of black pepper is expanding beyond culinary use into pharmaceuticals, cosmetics, and wellness products. Piperine, the bioactive compound in black pepper, is gaining traction in formulations aimed at enhancing nutrient absorption and metabolic performance. Demand from the nutraceutical and dietary supplement industries is rising as consumers seek natural health-enhancing ingredients. Cosmetic brands are also exploring black pepper extracts for use in exfoliants and anti-aging treatments due to their antioxidant properties. The Global Black Pepper Market can capitalize on these developments by aligning production with quality standards required in these regulated industries. It presents long-term potential for value-added products and functional ingredient innovation.

Rising Demand from Emerging Markets Is Creating Scalable Export Opportunities

Rapid urbanization, dietary shifts, and increasing disposable incomes in emerging markets are strengthening demand for spices, including black pepper. Countries in Africa, the Middle East, and Southeast Asia are showing notable growth in spice consumption across retail and foodservice sectors. Rising awareness of global cuisine and greater exposure to international flavor profiles are reinforcing this trend. Exporters and producers have an opportunity to establish strong market positions by offering standardized, competitively priced products tailored to regional preferences. The Global Black Pepper Market can benefit by expanding distribution networks and enhancing trade relations with high-growth economies. It positions itself for sustained growth through strategic geographic diversification.

Market Segmentation Analysis:

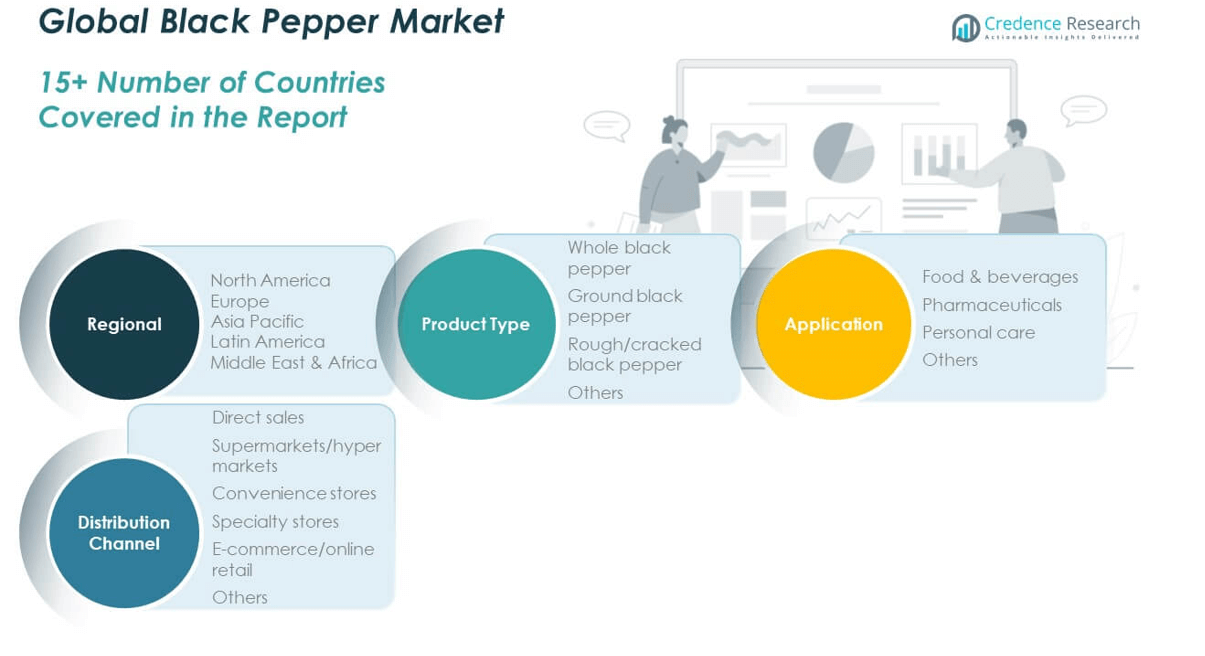

The Global Black Pepper Market is segmented by product type, application, and distribution channel.

By product type, whole black pepper dominates due to its strong presence in traditional cooking and bulk foodservice applications. Ground black pepper follows closely, driven by its convenience in household and packaged food usage. Rough/cracked black pepper caters to seasoning blends and premium culinary uses, while the others category includes processed variants used in industrial formulations.

- For example, McCormick & Company’s ground black pepper is a staple in household kitchens and is widely used in packaged foods.

By application, the food & beverages segment leads with the largest revenue share, supported by extensive use in processed foods, ready-to-eat meals, and condiments. The pharmaceuticals segment is expanding due to the growing use of piperine in supplements and therapeutic products. Personal care applications are rising with demand for natural antioxidants in skincare. The others category includes functional food and wellness product uses.

- For instance, Nestlé uses black pepper extracts in its Maggi range of instant noodles and soups, processed foods and ready-to-eat meals.

By distribution channel, supermarkets/hypermarkets remain dominant due to wide consumer reach and product visibility. E-commerce/online retail is growing rapidly with the shift toward digital shopping and direct-to-consumer sales. Direct sales serve bulk buyers and institutional clients. Convenience stores and specialty stores support niche and premium products, while others include foodservice and industrial distribution. The Global Black Pepper Market benefits from diverse channel strategies and evolving consumer preferences.

Segmentation:

By Product Type:

- Whole Black Pepper

- Ground Black Pepper

- Rough/Cracked Black Pepper

- Others

By Application:

- Food & Beverages

- Pharmaceuticals

- Personal Care

- Others

By Distribution Channel:

- Direct Sales

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialty Stores

- E-commerce/Online Retail

- Others

By Region:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America

The North America Black Pepper Market size was valued at USD 927.04 million in 2018 to USD 1,236.07 million in 2024 and is anticipated to reach USD 1,825.19 million by 2032, at a CAGR of 4.7% during the forecast period. The region holds 19.5% of the Global Black Pepper Market share. Strong demand from the foodservice industry, particularly fast food and fine dining, continues to drive consumption. Consumers in the United States and Canada show a growing preference for organic and traceable pepper products. Retailers and private-label brands are expanding black pepper offerings with premium packaging and clean-label claims. It benefits from robust import infrastructure and strict quality compliance mechanisms that support stable supply chains. The market is further supported by rising awareness of functional health benefits and demand for high-quality culinary ingredients.

Europe

The Europe Black Pepper Market size was valued at USD 618.95 million in 2018 to USD 794.56 million in 2024 and is anticipated to reach USD 1,068.03 million by 2032, at a CAGR of 3.4% during the forecast period. Europe accounts for 12.5% of the Global Black Pepper Market share. Demand is largely driven by processed food manufacturers, gourmet retailers, and ethnic food importers. Countries such as Germany, France, and the United Kingdom lead regional consumption, with rising interest in fair-trade and sustainably sourced pepper. Regulatory frameworks across the EU promote transparency, quality control, and pesticide compliance. It faces challenges from price-sensitive consumers but gains traction through innovation and organic certifications. The market is characterized by consistent demand and high safety standards.

Asia Pacific

The Asia Pacific Black Pepper Market size was valued at USD 1,305.11 million in 2018 to USD 1,836.25 million in 2024 and is anticipated to reach USD 2,873.67 million by 2032, at a CAGR of 5.4% during the forecast period. Holding the largest share at 37%, this region dominates the Global Black Pepper Market in both production and consumption. Vietnam, India, and Indonesia lead global supply with robust farming infrastructure and export capacity. Rising domestic demand in China, India, and Southeast Asia is driven by changing food habits and increased packaged food consumption. It benefits from low production costs, skilled labor, and favorable climatic conditions. Exporters in the region are strengthening quality certification and post-harvest handling to maintain competitiveness in global markets.

Latin America

The Latin America Black Pepper Market size was valued at USD 151.97 million in 2018 to USD 203.30 million in 2024 and is anticipated to reach USD 265.32 million by 2032, at a CAGR of 3.0% during the forecast period. The region contributes 3.2% of the Global Black Pepper Market share. Brazil remains the leading producer, supported by suitable agro-climatic conditions and improving farming techniques. Domestic consumption is growing, especially in processed foods and spice blends. Import reliance in smaller Latin American countries is increasing, supporting intra-regional trade. It is gradually attracting foreign investment in spice cultivation and packaging operations. The market holds potential through infrastructure development and regional export expansion.

Middle East

The Middle East Black Pepper Market size was valued at USD 89.64 million in 2018 to USD 111.12 million in 2024 and is anticipated to reach USD 138.31 million by 2032, at a CAGR of 2.4% during the forecast period. The region holds 1.8% of the Global Black Pepper Market share. Imports meet most of the regional demand, driven by growing consumer interest in international cuisines and spice blends. The United Arab Emirates and Saudi Arabia are major consumption hubs, supported by hospitality and foodservice sector expansion. It depends on reliable import partnerships and value-added repackaging activities. Regional distributors focus on supplying to hotels, restaurants, and premium retail chains. Growth remains modest but steady due to rising disposable incomes and evolving food preferences.

Africa

The Africa Black Pepper Market size was valued at USD 57.98 million in 2018 to USD 85.43 million in 2024 and is anticipated to reach USD 103.80 million by 2032, at a CAGR of 2.1% during the forecast period. Africa represents 1.3% of the Global Black Pepper Market share. Regional consumption is rising due to urbanization, population growth, and increasing demand for packaged and processed foods. Nigeria and South Africa lead market activity, with imports fulfilling the majority of demand. It faces logistical and infrastructure constraints that limit access and affordability. Local production remains minimal, though some countries are exploring spice cultivation potential. Market development depends on economic growth, investment in food industries, and improved trade networks.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- McCormick & Company

- MDH Spices

- Everest Spices

- Olam International

- Synthite Industries Ltd.

- DS Group

- British Pepper & Spice

- Vietnam Spice Company

- Ajinomoto Company, Inc.

- doTERRA International

Competitive Analysis:

The Global Black Pepper Market features a fragmented landscape with strong participation from both regional producers and international exporters. Key players include Olam International, Kancor Ingredients, Vietnam Hanfimex Corporation, McCormick & Company, and Everest Spices. These companies compete on factors such as sourcing reliability, product purity, organic certification, and supply chain efficiency. Leading exporters from Vietnam and India dominate global supply, while global spice brands focus on value addition, packaging, and branding to reach retail consumers. It faces rising competition from smaller, niche brands offering single-origin and specialty pepper variants. Strategic alliances, investments in post-harvest technologies, and expansion into direct-to-consumer channels are shaping market positioning. Companies that can ensure consistent quality, meet regulatory standards, and adapt to evolving consumer preferences are likely to maintain a competitive edge.

Recent Developments:

- In April 2025, Olam International announced a strategic shift by investing $500 million into its food ingredients division, which includes its spice business. The company plans to divest from other business ventures and assets, focusing on strengthening its core ingredients operations.

- In October 2024, Lactalis UK & Ireland introduced a new black pepper-flavored cheese spread under its Seriously Spreadable range. This innovative product features 50% cheddar and a touch of black pepper, catering to vegetarian consumers and packaged in fully recyclable materials.

- In July 2024, McCormick & Company emphasized that innovation remains a top priority, with new product launches expected to double in the second half of the year. The company recently introduced several new products, including Lawry’s new seasoning blends, Flavor Makers blend, and Frank’s RedHot Dip’N sauce in a squeeze bottle format.

- In January 2024, Phuc Sinh JSC, Vietnam’s largest spice exporter and a leading player in the black pepper market, received a significant investment from a European fund. This marks the first time in 22 years that the company has attracted foreign investment.

Market Concentration & Characteristics:

The Global Black Pepper Market demonstrates moderate market concentration, with Vietnam, India, and Indonesia accounting for the majority of global production. It operates within a price-sensitive framework, where smallholder farmers contribute significantly to output. The market is characterized by seasonality, yield variability, and dependence on climatic conditions. Supply chains remain fragmented in many regions, though leading exporters are investing in quality control, traceability, and infrastructure improvements. Product differentiation is limited, but opportunities exist through organic certification, specialty variants, and origin labeling. It reflects strong export orientation, with bulk shipments dominating trade, while retail segments focus on consumer-facing innovations. The market maintains a balance between traditional agricultural practices and modern processing technologies.

Report Coverage:

The research report offers an in-depth analysis based on product type, application, and distribution channel. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Demand will increase across foodservice and processed food industries driven by evolving consumer tastes.

- Health-focused applications in nutraceuticals and functional foods will expand usage of piperine-based ingredients.

- Organic and sustainably sourced pepper will gain market share through clean-label trends and eco-conscious consumers.

- Technological upgrades in drying, grading, and packaging will enhance product consistency and export readiness.

- Specialty varieties such as Tellicherry and Malabar will attract premium buyers in gourmet and retail segments.

- E-commerce and direct-to-consumer models will support market access for niche brands and small producers.

- Climate-resilient cultivation practices will become critical to mitigate yield instability in producing countries.

- Asia Pacific will retain its dominance in production and consumption, while Africa and Latin America show gradual demand growth.

- Regulatory compliance and food safety standards will drive investments in quality assurance systems.

- Market players will pursue value addition, certification, and branding to strengthen competitive positioning.