| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| ASIC Fabless Design House Market Size 2024 |

USD 774.44 million |

| ASIC Fabless Design House Market, CAGR |

13.50% |

| ASIC Fabless Design House Market Size 2032 |

USD 2,132.82 million |

Market Overview

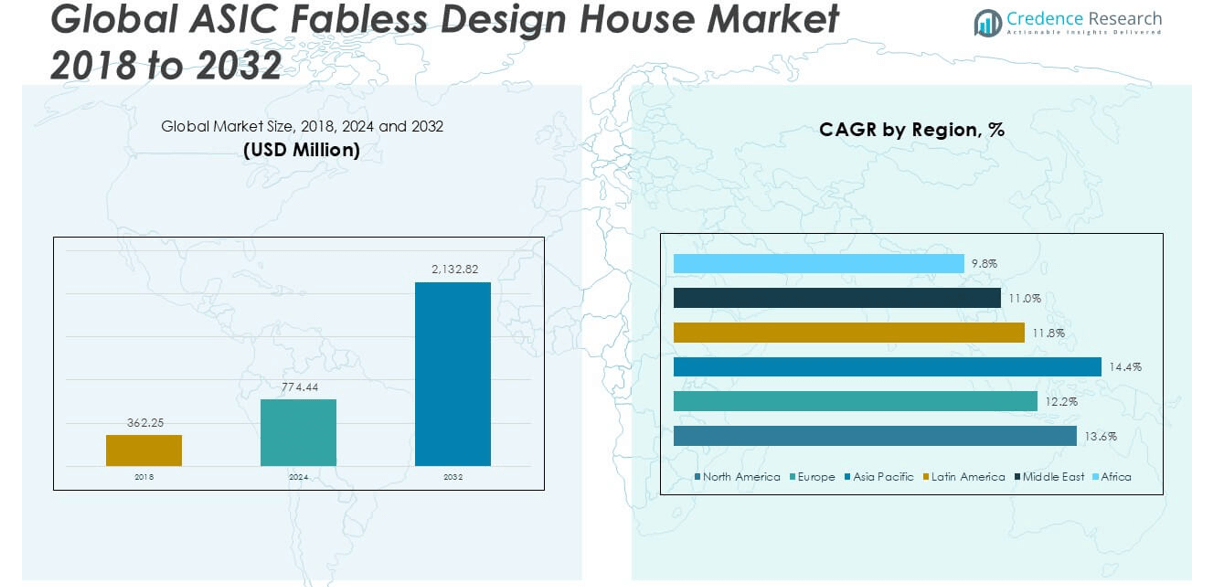

The ASIC Fabless Design House market size was valued at USD 362.25 million in 2018, reached USD 774.44 million in 2024, and is anticipated to reach USD 2,132.82 million by 2032, at a CAGR of 13.50% during the forecast period.

The ASIC Fabless Design House market is led by key players such as NVIDIA, Qualcomm, Broadcom, AMD, and MediaTek, which collectively hold a substantial portion of the global market due to their technological leadership, broad IP portfolios, and strategic partnerships with foundries. These companies dominate high-growth sectors including mobile devices, automotive electronics, and AI-enabled hardware. Emerging players like Marvell Technology Group, Novatek Microelectronics, Tsinghua Unigroup, and Realtek Semiconductor are expanding their presence, particularly in Asia Pacific. Regionally, Asia Pacific leads the market with a commanding 42.7% share in 2024, driven by high-volume semiconductor production and strong regional demand from consumer electronics and telecom industries. North America follows with a 29.9% share, supported by advanced R&D capabilities and a mature fabless ecosystem. These regions serve as strategic hubs for innovation and manufacturing, reinforcing the competitive advantage of top-tier fabless firms.

Market Insights

- The ASIC Fabless Design House market was valued at USD 774.44 million in 2024 and is projected to reach USD 2,132.82 million by 2032, growing at a CAGR of 13.50% during the forecast period.

- Market growth is driven by rising demand for customized, low-power ICs in mobile devices, automotive systems, and AI-powered applications across various industries.

- The market is witnessing strong trends in edge computing, 5G, and AI integration, with increased adoption of advanced semiconductor nodes below 7nm for enhanced performance and efficiency.

- The competitive landscape features key players like NVIDIA, Qualcomm, and Broadcom, supported by a growing number of Asia-based companies such as MediaTek and Realtek, focusing on design innovation and strategic foundry collaborations.

- Asia Pacific held the largest regional share with 42.7% in 2024, followed by North America at 29.9%; by segment, Logic ICs dominated the type category, while Mobile Devices led in the application segment.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Type

In the ASIC Fabless Design House market, Logic ICs emerged as the dominant sub-segment, accounting for the largest market share in 2024. Their widespread use in data processing, system control, and communication functions across various devices drives their prominence. The demand is particularly high in mobile computing, network equipment, and automotive applications, where performance efficiency and miniaturization are crucial. Microcontrollers & Microprocessors represent another significant share within the type segment, fueled by their extensive application in embedded systems across consumer electronics, industrial automation, and medical devices. Their scalability, low power consumption, and versatility drive consistent demand. Analog ICs and Memory ICs follow closely, serving critical functions in power management, signal conversion, and data storage. Memory ICs, in particular, benefit from rising data-centric applications such as cloud computing and high-performance servers.

- For instance, Broadcom shipped over 1.5 billion logic ICs in 2023, primarily for networking and broadband applications, leveraging its multi-chip package SoCs for Wi-Fi 6 and Wi-Fi 7 solutions.

By Application

Mobile Devices hold the largest market share in the application segment of the ASIC Fabless Design House market. The continued growth in smartphone penetration, wearable technologies, and tablets fuels demand for customized, high-performance ASICs. OEMs prioritize power efficiency, speed, and integration, all of which are effectively met by fabless ASIC designs. With 5G rollouts and rising consumer expectations for real-time processing, the role of ASICs in mobile chipsets has become more prominent. Automotive follows as a fast-growing application segment, driven by the rapid adoption of electric vehicles (EVs), ADAS (Advanced Driver Assistance Systems), and in-vehicle infotainment systems. Industrial & Medical and Network Infrastructure segments also show steady growth, fueled by the increasing digitization of factories, smart healthcare devices, and cloud-based services. Servers and Appliances/Consumer Goods round out the application scope, contributing to stable demand for energy-efficient and performance-optimized ICs in everyday use and enterprise computing.

- For instance, Qualcomm’s Snapdragon mobile platform powered over 1.4 billion smartphones globally in 2023, with chipsets like the Snapdragon 8 Gen 2 delivering up to 4.35 TOPS (Tera Operations Per Second) for AI tasks.

Market Overview

Rising Demand for Customized Integrated Circuits

The growing need for application-specific performance and power efficiency across industries is driving demand for customized integrated circuits. ASICs offer tailored solutions that outperform general-purpose chips in mobile devices, automotive systems, and consumer electronics. Fabless design houses, with their design agility and outsourcing capabilities, enable faster development cycles and cost-effective production. As industries seek differentiated hardware for AI, IoT, and automation, the adoption of ASICs continues to grow, positioning fabless design houses as strategic partners in delivering specialized and scalable silicon solutions.

- For instance, AMD’s semi-custom business model enabled the delivery of over 40 million custom SoCs for gaming consoles like PlayStation 5 and Xbox Series X, built with specific GPU and CPU configurations tailored for immersive performance.

Expansion of the Consumer Electronics and Mobile Devices Sector

The proliferation of smartphones, tablets, wearables, and other smart devices is significantly boosting the ASIC fabless market. Manufacturers rely heavily on high-performance, low-power custom chips to meet space and battery constraints while delivering real-time processing and wireless communication. Fabless companies play a key role in meeting these requirements by providing flexible and innovative IC designs. The rollout of 5G and increasing integration of AI features into mobile devices further fuel the demand for tailored ASICs, ensuring sustained growth in this sector.

- For instance, MediaTek shipped over 600 million chipsets for smartphones and IoT devices in 2023, including Dimensity processors with integrated 5G modems and AI enhancements

Growing Integration of Semiconductor Solutions in Automotive Applications

The automotive industry is undergoing rapid technological transformation with the rise of electric vehicles (EVs), autonomous driving, and vehicle connectivity. These applications require highly reliable, energy-efficient, and real-time capable ASICs. Fabless design houses are essential in delivering chips for battery management, ADAS, infotainment, and vehicle-to-everything (V2X) communication. The increasing demand for electronics in vehicles is expanding the role of fabless companies, as OEMs prioritize cost-efficiency and flexibility in chip design to stay competitive in the evolving automotive ecosystem.

Key Trends & Opportunities

Adoption of AI and Edge Computing Technologies

The shift toward AI-driven applications and edge computing presents a major opportunity for fabless design houses. Custom ASICs optimized for machine learning, computer vision, and neural processing are in high demand for use in smart cameras, industrial automation, and autonomous systems. Fabless companies are capitalizing on this trend by delivering domain-specific architectures with minimal latency and enhanced data throughput. This shift is enabling new product innovations across verticals while creating long-term growth prospects for custom silicon providers.

- For instance, NVIDIA’s Jetson edge AI platform shipped over 2 million units globally by 2023, enabling developers to deploy up to 275 TOPS performance in edge AI systems.

Transition to Advanced Semiconductor Nodes

The ongoing move toward smaller semiconductor nodes, such as 5nm and below, opens up new possibilities for performance optimization and power efficiency. Fabless design houses that can adapt quickly to these technologies are gaining a competitive edge. As end-use industries demand faster and more energy-efficient chips, fabless companies are investing in EDA tools and collaborating closely with foundries to leverage cutting-edge manufacturing capabilities. This trend is helping to reduce chip size and cost while enhancing functionality and scalability.

- For instance, Qualcomm’s Snapdragon 8 Gen 3 chipset, built on TSMC’s N4P node, delivers a 20% increase in CPU performance and 25% GPU power efficiency over its predecessor.

Key Challenges

High Design Complexity and Development Costs

ASIC design involves high complexity and requires advanced tools, skilled engineers, and significant upfront investment. As customization needs grow and semiconductor nodes shrink, design cycles become longer and more resource-intensive. This poses a challenge for smaller fabless firms with limited budgets and access to talent. Meeting stringent performance and compliance requirements across applications such as automotive or medical adds further design burden, making cost control and time-to-market management increasingly difficult.

Dependency on Third-Party Foundries

Fabless design houses rely heavily on third-party foundries for chip manufacturing. Any disruption in the foundry ecosystem—whether due to geopolitical tensions, capacity constraints, or natural disasters—can significantly affect the supply chain and delivery timelines. This dependency limits control over production schedules, quality assurance, and pricing. Furthermore, the global concentration of leading foundries increases exposure to regional risks, compelling fabless firms to diversify partnerships and mitigate operational vulnerabilities.

Intellectual Property and Security Risks

As ASIC designs become more valuable and application-specific, protecting intellectual property (IP) becomes critical. Fabless design houses face the risk of IP theft, reverse engineering, and design replication, especially when working with offshore partners. Ensuring data security across collaborative development environments and maintaining secure IP cores is essential but challenging. Weaknesses in design verification or third-party IP integration can expose products to functional failures or security breaches, affecting brand reputation and end-user trust.

Regional Analysis

North America

In 2024, North America held a significant share of the ASIC Fabless Design House market, valued at USD 231.49 million, up from USD 109.93 million in 2018, and is projected to reach USD 640.09 million by 2032 at a CAGR of 13.6%. This region accounted for approximately 29.9% of the global market in 2024, driven by strong demand from the consumer electronics, data center, and automotive sectors. The U.S. continues to lead in fabless innovation due to a robust semiconductor ecosystem, strategic partnerships with foundries, and increasing investments in AI, 5G, and autonomous technologies.

Europe

Europe accounted for nearly 18.6% of the global ASIC Fabless Design House market in 2024, with market size growing from USD 71.12 million in 2018 to USD 144.13 million in 2024. The region is anticipated to reach USD 362.82 million by 2032, registering a CAGR of 12.2%. The growth is fueled by increased demand from the automotive industry, especially in Germany and France, where adoption of EVs and ADAS technologies is rising. Additionally, regulatory support for digital transformation and strong R&D infrastructure are enabling fabless companies to thrive within industrial, medical, and telecom applications.

Asia Pacific

Asia Pacific led the global ASIC Fabless Design House market in 2024 with a dominant 42.7% market share, reaching USD 331.05 million from USD 149.01 million in 2018. It is projected to surge to USD 970.68 million by 2032 at a CAGR of 14.4%, the highest among all regions. The region’s leadership is driven by high-volume electronics manufacturing, a strong base of consumer device OEMs, and growing investments in AI, automotive, and semiconductor R&D, particularly in China, Japan, South Korea, and Taiwan. Strategic collaborations between fabless firms and foundries continue to accelerate product development and time-to-market.

Latin America

Latin America captured a modest 4.8% share of the global ASIC Fabless Design House market in 2024, with the market rising from USD 17.47 million in 2018 to USD 36.90 million in 2024. It is expected to reach USD 90.19 million by 2032, growing at a CAGR of 11.8%. Market expansion is supported by increased adoption of smart devices, digital infrastructure growth, and regional government initiatives in countries such as Brazil and Mexico to strengthen electronics manufacturing capabilities. Despite a smaller market base, emerging applications in telecom and industrial sectors are presenting growth opportunities for fabless providers.

Middle East

The Middle East accounted for around 2.9% of the global ASIC Fabless Design House market in 2024, growing from USD 9.86 million in 2018 to USD 19.22 million in 2024, and is forecasted to reach USD 44.41 million by 2032 at a CAGR of 11.0%. The region’s market is gaining traction due to rising investments in smart city projects, digital healthcare, and advanced infrastructure. Countries like the UAE and Saudi Arabia are increasingly deploying ASICs in security, automation, and energy-efficient systems. However, limited regional semiconductor design infrastructure remains a constraint to accelerated fabless growth.

Africa

Africa held the smallest share in the global ASIC Fabless Design House market in 2024, contributing approximately 1.5% with a market size of USD 11.64 million, up from USD 4.86 million in 2018. It is expected to reach USD 24.63 million by 2032, at a CAGR of 9.8%. The market remains in its nascent stage, with opportunities emerging in telecommunications, consumer electronics, and energy management. As internet penetration, mobile device usage, and digital infrastructure expand, demand for low-power, application-specific chips is gradually increasing. However, underdeveloped manufacturing and R&D ecosystems limit rapid regional scalability.

Market Segmentations:

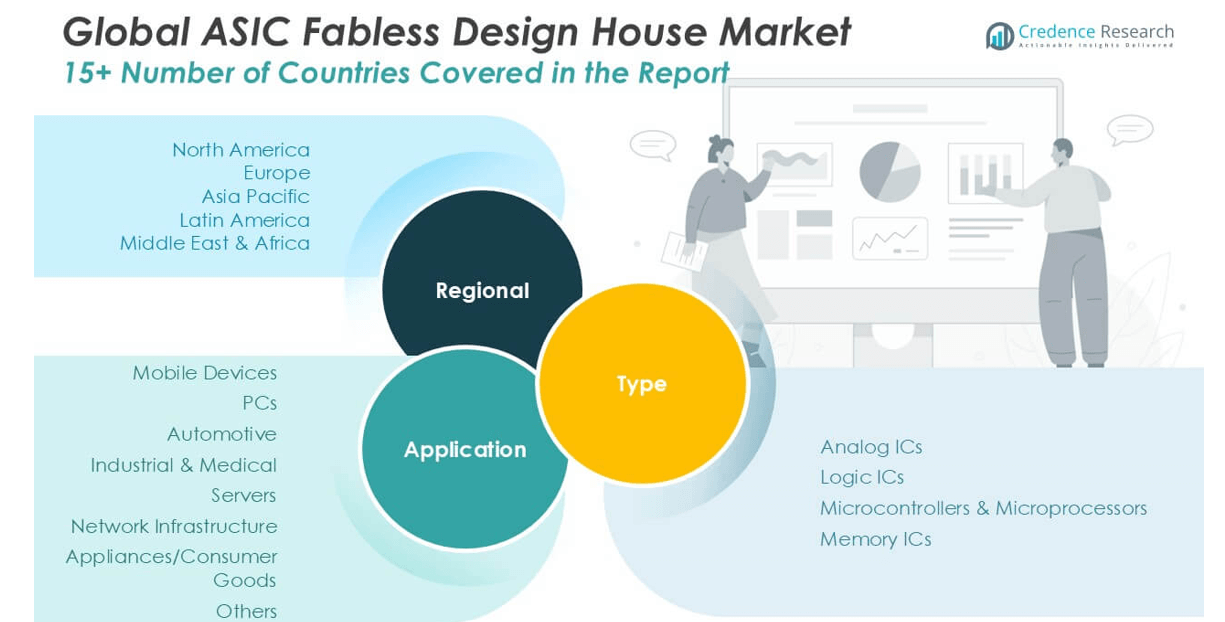

By Type

- Analog ICs

- Logic ICs

- Microcontrollers & Microprocessors

- Memory ICs

By Application

- Mobile Devices

- PCs

- Automotive

- Industrial & Medical

- Servers

- Network Infrastructure

- Appliances / Consumer Goods

- Others

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The ASIC Fabless Design House market is characterized by intense competition, driven by rapid technological advancements and growing demand for customized integrated circuits across diverse applications. Leading players such as NVIDIA, Qualcomm, Broadcom, AMD, and MediaTek dominate the market with robust design capabilities, extensive IP portfolios, and strategic partnerships with leading foundries. These companies focus heavily on AI, automotive, and 5G innovations to sustain their market positions. Emerging players like Novatek Microelectronics, Tsinghua Unigroup, and Realtek Semiconductor are also gaining ground by targeting niche markets and expanding their presence in Asia. Continuous investment in R&D, product differentiation, and time-to-market strategies remain critical success factors. Additionally, M&A activities and collaborations with EDA tool providers and OEMs are reshaping the competitive dynamics. As the complexity of ASIC design increases, firms with advanced design tools, strong ecosystem alliances, and scalable production models are better positioned to capture emerging opportunities and defend market share.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- NVIDIA

- Qualcomm

- Broadcom

- Advanced Micro Devices (AMD)

- MediaTek

- Marvell Technology Group

- Novatek Microelectronics

- Tsinghua Unigroup

- Realtek Semiconductor

- OmniVision Technologies

Recent Developments

- In June 2025, Broadcom is continuing its established strategy of offering custom ASIC design services to enterprise and hyperscale clients, focusing on AI acceleration and high-speed networking protocols. This approach, highlighted in industry analysis and recent earnings calls, involves creating specialized silicon tailored for both AI training and inference workloads. Broadcom is strategically positioning itself to capitalize on the growing demand for custom silicon in AI infrastructure, particularly for inference, which involves high-volume, low-latency, and cost-sensitive applications.

- In May 2025, NVIDIA announced DGX Cloud Lepton at Computex 2025. This platform connects AI developers with NVIDIA’s GPU cloud providers, making flexible, cloud-independent access to GPU resources possible—critical for AI model training and inference. This is a step into offering specialized cloud infrastructure for AI teams, leveraging NVIDIA’s expertise in both ASIC and GPU design.

- In May 2025, NVIDIA launched RTX PRO Servers and the Enterprise AI Factory platform, built around the NVIDIA Blackwell architecture. These systems, featuring the RTX PRO 6000 Blackwell Server Edition ASICs, are designed to accelerate enterprise workloads in AI, design, and simulation. The platform aims to facilitate a shift from CPU-based systems to GPU-accelerated infrastructure within enterprise data centers.

- In 2024, AMD is seeing significant growth in its ASIC and semi-custom business, particularly due to the high demand for AI accelerators and partnerships with major cloud service providers, leading to substantial increases in revenue and volume for the company.

Market Concentration & Characteristics

The ASIC Fabless Design House Market exhibits a moderately concentrated structure, with a few dominant players such as NVIDIA, Qualcomm, Broadcom, and MediaTek holding a significant share of the global revenue. It is characterized by high barriers to entry due to substantial design complexity, capital-intensive R&D, and the need for strong intellectual property portfolios. The market favors companies with deep expertise in application-specific solutions and long-standing partnerships with advanced foundries. Innovation speed, time-to-market, and customization capabilities shape competitive advantage. It serves a diverse set of end-use industries, including mobile, automotive, consumer electronics, and industrial sectors, each requiring differentiated IC designs. Companies focus on scalable and energy-efficient designs to meet evolving performance needs. The presence of strong ecosystems in North America and Asia Pacific enables continuous advancement in chip architecture, software integration, and manufacturing collaboration. It is highly dynamic, driven by fast-paced technological evolution and demand for specialized, high-performance semiconductor solutions.

Report Coverage

The research report offers an in-depth analysis based on Type, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The demand for customized ASIC solutions will continue to rise across industries such as automotive, telecommunications, and consumer electronics.

- Fabless companies will increasingly adopt advanced semiconductor nodes to enhance performance and reduce power consumption.

- Artificial intelligence and machine learning applications will drive innovation in ASIC architecture and design.

- The expansion of 5G networks will create new opportunities for ASICs in mobile devices and infrastructure equipment.

- Edge computing growth will boost demand for low-latency, high-efficiency ASICs in smart devices and industrial systems.

- Automotive applications, particularly in electric vehicles and ADAS, will become a major revenue stream for fabless design houses.

- Strategic collaborations between fabless firms and foundries will intensify to meet rising production and innovation demands.

- The Asia Pacific region will maintain its leadership in market share due to strong manufacturing and consumer demand.

- Security and IP protection will become more critical as design complexity and outsourcing increase.

- Continuous investment in R&D and EDA tools will remain essential for maintaining competitiveness and design agility.