| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| 5G Infrastructure ASIC Market Size 2024 |

USD 5,626.29 million |

| 5G Infrastructure ASIC Market, CAGR |

19.73% |

| 5G Infrastructure ASIC Market Size 2032 |

USD 26,125.05 million |

Market Overview:

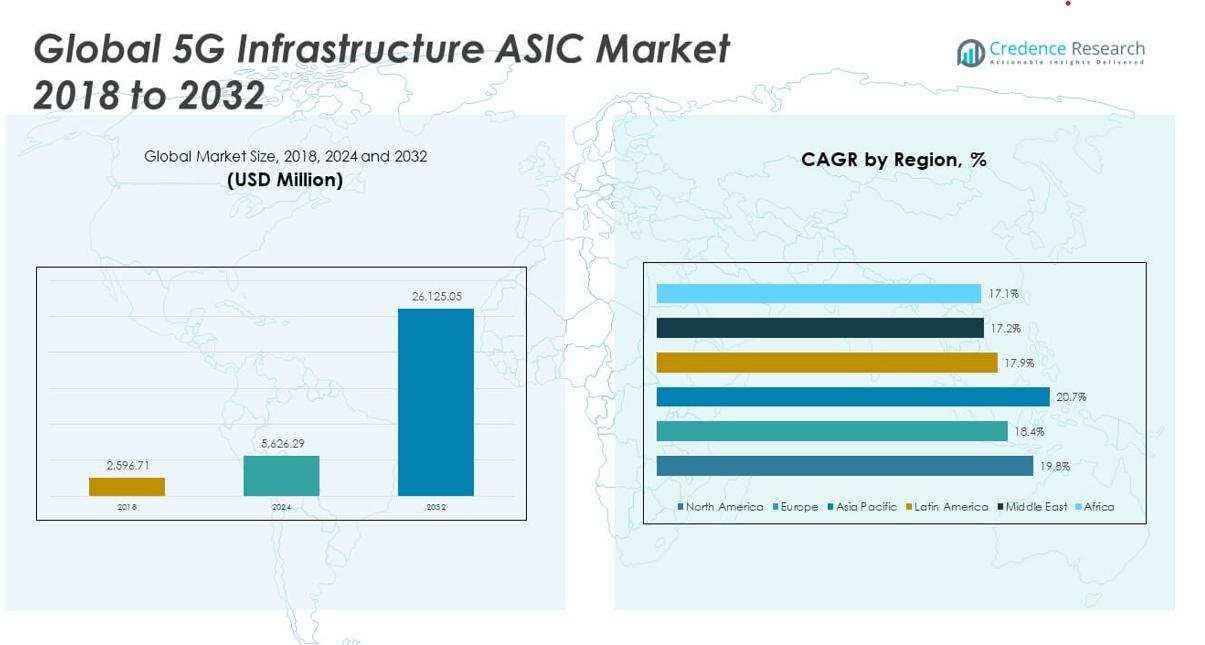

The Global 5G Infrastructure ASIC Market size was valued at USD 2,596.71 million in 2018 to USD 5,626.29 million in 2024 and is anticipated to reach USD 26,125.05 million by 2032, at a CAGR of 19.73% during the forecast period.

The growth of the global 5G infrastructure ASIC market is driven by the rising demand for highly customized and performance-optimized chip solutions to support the rollout of next-generation network infrastructure. As 5G networks evolve to deliver ultra-low latency, high-speed data transmission, and massive connectivity, telecom operators and equipment manufacturers increasingly rely on ASICs to meet specific performance and energy efficiency requirements. The transition from non-standalone to standalone 5G architectures, which enables full-scale deployment of network slicing, virtualized functions, and edge computing, further necessitates the use of specialized integrated circuits. In addition, the proliferation of smart cities, industrial IoT, autonomous vehicles, and immersive technologies such as AR/VR fuels the need for high-speed, low-power chips capable of handling complex workloads in real time. Ongoing investments in research and development by leading semiconductor companies continue to improve the scalability, functionality, and cost-effectiveness of ASICs, reinforcing their importance in 5G infrastructure deployment across diverse applications.

Regionally, the 5G infrastructure ASIC market is witnessing significant activity across Asia-Pacific, North America, and Europe. Asia-Pacific holds a dominant position due to rapid infrastructure development, strong government support, and a well-established ecosystem of telecom and semiconductor manufacturers. Countries in this region are aggressively deploying 5G base stations and accelerating digital transformation initiatives. North America follows closely, supported by substantial investments in next-generation wireless technology by telecom operators, coupled with strong innovation in chip design and edge computing. Europe is experiencing steady growth as regulatory frameworks and public-private partnerships promote the expansion of 5G networks and the adoption of advanced technologies in industrial and consumer sectors. Meanwhile, regions such as the Middle East & Africa and Latin America are gradually entering the 5G phase, with select markets making strategic investments to build the foundational infrastructure needed to support 5G adoption in the coming years.

Market Insights:

- The market was valued at USD 5,626.29 million in 2024 and is projected to reach USD 26,125.05 million by 2032, growing at a strong CAGR of 19.73%.

- Rising demand for performance-optimized ASICs is driven by the need for ultra-low latency and high-speed data transmission in 5G networks.

- The transition to standalone 5G architectures is increasing reliance on custom ASICs for network slicing, edge computing, and virtualization.

- High-bandwidth applications such as smart cities, industrial IoT, and AR/VR are fueling demand for energy-efficient ASICs with real-time processing capabilities.

- Ongoing R&D investments and vertical integration by major semiconductor firms are driving innovation in ASIC packaging, power efficiency, and integration.

- The market faces challenges from high development costs, complex design processes, and limited access to advanced semiconductor fabrication facilities.

- Asia-Pacific leads the market due to rapid infrastructure development and manufacturing strength, while North America and Europe follow with strong investment in edge computing and network modernization.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Rising Demand for High-Performance and Power-Efficient Network Components Fuels ASIC Adoption

The Global 5G Infrastructure ASIC Market is expanding as telecom operators prioritize network components that deliver speed, efficiency, and reliability. ASICs provide optimized hardware solutions for specific 5G functions, including baseband processing, signal modulation, and beamforming. Their ability to outperform general-purpose chips in power consumption and latency makes them essential for 5G base stations and radio access networks. Growing expectations for ultra-reliable low-latency communication and massive machine-type communication drive the need for specialized processing. Standard chipsets often fall short of supporting the stringent performance benchmarks required by modern networks. The demand for tailored silicon solutions positions ASICs at the core of 5G infrastructure deployment.

Transition to Standalone 5G Networks Requires Custom ASIC Architecture

The shift from non-standalone to standalone 5G networks presents new architectural and performance demands on infrastructure hardware. It increases reliance on purpose-built ASICs to support cloud-native 5G cores, dynamic network slicing, and edge computing. These functions demand efficient processing capabilities that general-purpose processors cannot deliver. The Global 5G Infrastructure ASIC Market benefits from this shift by addressing challenges tied to latency, traffic prioritization, and real-time analytics. ASICs help reduce processing bottlenecks while enabling telecom providers to deliver more agile, scalable services. The migration to standalone networks accelerates the need for ASICs that integrate diverse workloads in compact, power-efficient packages.

- For example, Qualcomm’s AI 100ASIC, built on a 7nm process, is engineered for edge inference acceleration in 5G RAN infrastructure. It delivers 2x to 4x higher performance per watt than leading GPU solutions in MLPerf benchmarks, supporting advanced applications such as secondary carrier prediction, antenna tilting, and link adaptation in real-time.

Growth in Data-Intensive Use Cases Drives Custom Silicon Innovation

Emerging 5G-enabled applications across smart cities, autonomous mobility, industrial automation, and immersive media generate massive volumes of data. These applications require processing at the edge with minimal delay, prompting a move toward ASICs designed for real-time data interpretation and transmission. It supports workloads that include machine learning inference, sensor fusion, and high-throughput communication. The Global 5G Infrastructure ASIC Market gains momentum from these use cases that demand specialized, scalable hardware. ASICs offer the configurability and processing depth to sustain the performance of complex applications without overburdening central systems. The increase in bandwidth-hungry services encourages deeper investments in ASIC platforms optimized for specific functions.

- For instance, GlobalFoundriesmanufactures 5G mmWave ASICs at its Malta, NY facility using a 12 nm FD-SOI process, with a monthly capacity of 14,000 wafers. These ASICs are engineered for high-throughput communication and sensor fusion, supporting the bandwidth and processing demands of autonomous vehicles and industrial IoT. The company’s focus on node specialization (<7 nm for AI/ML ASICs, 12-28 nm for automotive/industrial) ensures that each chip is optimized for its intended workload.

Strategic Investments and R&D Drive Technological Advancements in ASICs

Chip manufacturers and telecom infrastructure providers are allocating significant resources toward the development of next-generation ASIC solutions. It reflects a broader industry trend toward vertical integration, where companies develop in-house chipsets for better performance and cost control. Leading players are building custom ASICs to power network elements such as small cells, virtualized RAN, and core network modules. The Global 5G Infrastructure ASIC Market benefits from ongoing innovation in semiconductor design and fabrication, including advancements in lithography, 3D stacking, and energy-efficient architectures. These investments result in highly integrated chips that meet the evolving needs of telecom operators. The focus on long-term strategic differentiation continues to propel ASIC development for 5G infrastructure.

Market Trends:

Integration of AI and ML Capabilities into 5G ASIC Designs Is Reshaping Network Intelligence

Artificial intelligence (AI) and machine learning (ML) are emerging as key design priorities in next-generation ASICs tailored for 5G infrastructure. Network operators require smart silicon that can dynamically manage traffic, detect anomalies, and optimize signal routing without external computation. The integration of AI and ML engines into ASICs enhances autonomous decision-making across base stations and edge nodes. This trend reflects a broader industry push toward self-optimizing networks that improve efficiency and reduce manual intervention. The Global 5G Infrastructure ASIC Market is evolving to meet this need by embedding intelligence directly into hardware. It enables real-time analytics at the silicon level and supports predictive maintenance, anomaly detection, and adaptive network behavior.

- For example, Qualcomm’s AI-driven 5G chipsets utilize dedicated neural processing units (NPUs) that deliver up to 15 TOPS (trillions of operations per second) of AI performance, supporting functions such as predictive maintenance, anomaly detection, and adaptive beamforming at the silicon level.

Expansion of Open RAN Architecture Is Driving Demand for Flexible ASIC Platforms

The rise of Open RAN (Radio Access Network) is changing how ASICs are designed and deployed across 5G networks. Open RAN promotes interoperability among hardware vendors and decouples software from proprietary hardware, creating a more modular architecture. This trend demands that ASICs remain flexible while maintaining high performance and low power consumption. Vendors are now developing ASICs compatible with open standards and software-defined components, allowing greater customization in multi-vendor environments. The Global 5G Infrastructure ASIC Market is adjusting to these changes by supporting open interfaces and scalable chip configurations. It promotes faster innovation and reduces deployment barriers for new market entrants.

- For instance, Ericsson’s Open RAN solutions feature ASIC-based radio units (O-RUs) capable of supporting up to 64T64R (transmit/receive) massive MIMO configurations, with fronthaul data rates exceeding 25 Gbps per port, all while maintaining sub-10W power consumption per antenna element.

Adoption of Advanced Packaging Techniques Is Enhancing ASIC Performance and Density

The demand for higher performance in smaller form factors is leading to the adoption of advanced packaging technologies for 5G ASICs. Techniques such as chiplet integration, system-in-package (SiP), and 3D stacking are enabling greater transistor density and improved thermal efficiency. These packaging innovations support multifunctional designs, combining RF processing, AI logic, and memory within a compact footprint. The Global 5G Infrastructure ASIC Market is leveraging these approaches to produce chips capable of supporting diverse workloads in space-constrained deployments. It allows telecom infrastructure providers to deploy more powerful base stations without increasing energy consumption or size. The trend also improves signal integrity and reduces interconnect delays.

Emergence of Domain-Specific Design Tools Is Accelerating ASIC Customization

Designing ASICs for 5G infrastructure now involves domain-specific electronic design automation (EDA) tools tailored to telecom applications. These tools accelerate time-to-market by simplifying chip customization for specific network functions and deployment scenarios. They offer pre-validated IP blocks, optimized for signal processing, protocol handling, and security features. The Global 5G Infrastructure ASIC Market benefits from these tools by reducing development costs and minimizing design risks. It supports the rapid evolution of chip capabilities in line with changing standards and operator requirements. This trend is fostering a new era of specialized ASIC development tuned to the operational realities of 5G infrastructure.

Market Challenges Analysis:

High Development Costs and Complexity of Custom ASIC Design Limit Market Participation

Designing and manufacturing ASICs for 5G infrastructure involves significant capital investment and technical complexity. The process requires substantial non-recurring engineering (NRE) costs, advanced design tools, and access to cutting-edge semiconductor fabrication facilities. Smaller players face barriers in entering the market due to the high cost of prototyping, testing, and achieving compliance with telecom-grade reliability standards. The Global 5G Infrastructure ASIC Market remains dominated by large semiconductor firms that can absorb these costs and maintain long-term R&D pipelines. It creates an uneven competitive landscape where innovation is often concentrated among a few key vendors. The high risk of obsolescence and long development cycles also deter some companies from aggressively pursuing ASIC development for 5G networks.

Supply Chain Constraints and Geopolitical Pressures Disrupt ASIC Manufacturing and Deployment

The global semiconductor supply chain continues to experience disruptions from material shortages, capacity limitations, and geopolitical tensions. Access to advanced fabrication nodes required for high-performance ASICs is often limited to a few foundries, creating bottlenecks in scaling production. Regulatory restrictions and export controls also affect the availability of critical design tools and manufacturing equipment in certain regions. The Global 5G Infrastructure ASIC Market faces delays in product launches and infrastructure deployments when such constraints arise. It reduces agility in responding to market demand and slows innovation cycles across the ecosystem. These factors introduce operational uncertainty for telecom providers and equipment manufacturers reliant on timely ASIC availability.

Market Opportunities:

Edge Computing and Private 5G Networks Create New Demand for Custom ASIC Solutions

The growing deployment of edge computing and private 5G networks offers strong potential for ASIC vendors to deliver purpose-built solutions. Enterprises across manufacturing, healthcare, logistics, and energy sectors require localized, low-latency processing with secure and reliable connectivity. The Global 5G Infrastructure ASIC Market can address these demands by supplying chips optimized for compact edge nodes and enterprise-grade 5G infrastructure. It enables application-specific performance improvements while reducing dependence on general-purpose processors. The rise of industrial IoT and mission-critical applications strengthens the case for deploying ASICs that support deterministic performance and advanced control functions.

Expansion of mmWave and Small Cell Deployments Enhances Customization Opportunities

The global expansion of millimeter wave (mmWave) and small cell deployments in urban and indoor environments increases the need for highly specialized ASICs. These applications require chips that manage complex signal modulation, power constraints, and frequency coordination within limited space. The Global 5G Infrastructure ASIC Market can capitalize on this trend by offering lightweight, power-efficient designs tailored for dense network topologies. It supports telecom operators in improving coverage and capacity while managing operational costs. This niche allows new entrants and specialized vendors to carve out roles in a competitive yet growing ecosystem.

Market Segmentation Analysis:

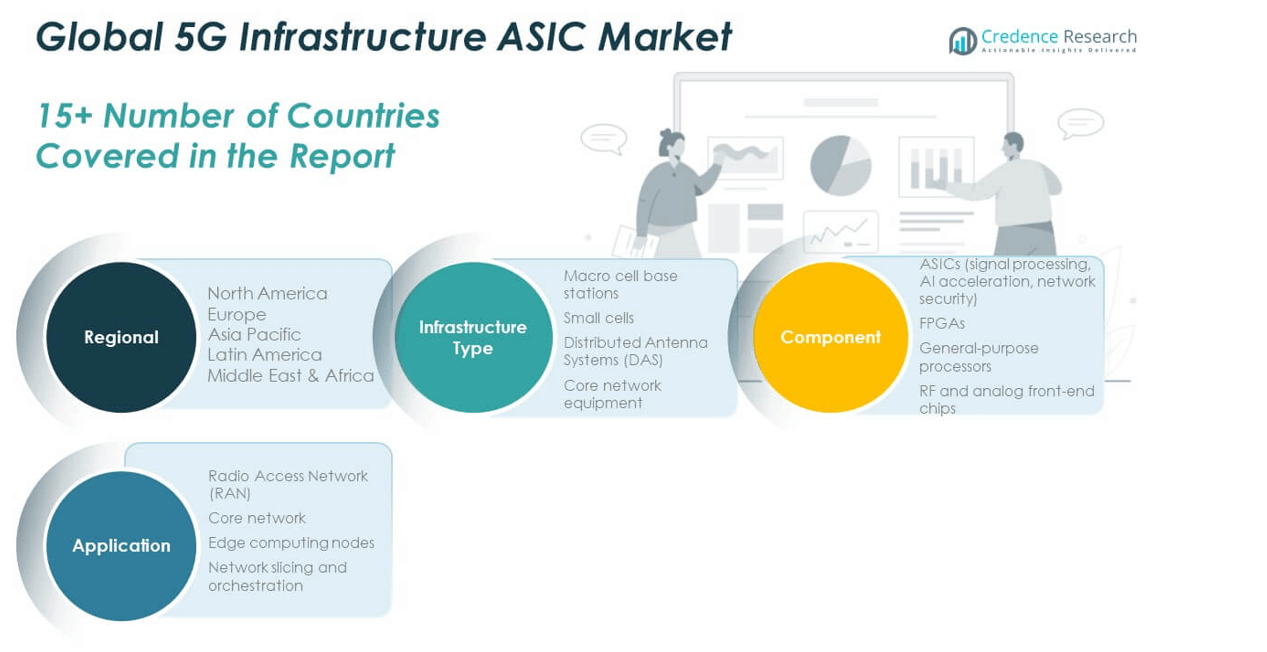

The Global 5G Infrastructure ASIC Market is segmented by infrastructure type, component, and application, each contributing to its growth trajectory.

By infrastructure type, macro cell base stations lead the segment due to their widespread deployment in urban areas for wide-area coverage. Small cells are gaining momentum for localized, high-density connectivity, particularly in indoor and urban environments. Distributed Antenna Systems (DAS) support extended signal coverage in complex environments such as stadiums and airports. Core network equipment is evolving rapidly with the shift to cloud-native, virtualized network architectures requiring advanced ASIC support.

- For instance, CommScope’s Era C-RAN DAS is deployed in large venues like Allegiant Stadium in Las Vegas. The system uses advanced ASIC-driven remote units to provide seamless 5G coverage across 1.8 million square feet, supporting over 65,000 concurrent users and dynamic spectrum allocation for multiple carriers.

By component, ASICs dominate due to their ability to deliver high-performance processing, energy efficiency, and tailored functionality for signal processing, AI acceleration, and network security. FPGAs offer reconfigurability and remain essential for prototyping and low-volume deployments. General-purpose processors serve supplementary roles in network control and management functions, while RF and analog front-end chips ensure signal integrity and performance across diverse frequency bands.

- For example, Marvell’s OCTEON Fusion CNF95xx ASIC is used in Samsung and NEC 5G base stations, delivering up to 200 Gbps L1/L2 processing with integrated AI engines for beamforming and interference mitigation. Marvell’s documentation shows a 40% reduction in power consumption per base station compared to previous generations.

By application, Radio Access Networks (RAN) generate the highest demand for ASICs, driven by rapid deployment of base stations. The core network segment requires scalable and secure processing for data routing and network functions. Edge computing nodes benefit from ASICs that support real-time analytics and low-latency processing. Network slicing and orchestration is an emerging application, requiring ASICs to manage dynamic allocation of resources across virtualized 5G services. The Global 5G Infrastructure ASIC Market aligns its development with these evolving needs across segments.

Segmentation:

By Infrastructure Type

- Macro Cell Base Stations

- Small Cells

- Distributed Antenna Systems (DAS)

- Core Network Equipment

By Component

- ASICs (Signal Processing, AI Acceleration, Network Security)

- FPGAs

- General-Purpose Processors

- RF and Analog Front-End Chips

By Application

- Radio Access Network (RAN)

- Core Network

- Edge Computing Nodes

- Network Slicing and Orchestration

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America

The North America 5G Infrastructure ASIC Market size was valued at USD 745.57 million in 2018 to USD 1,589.90 million in 2024 and is anticipated to reach USD 7,413.90 million by 2032, at a CAGR of 19.8% during the forecast period. North America accounts for a significant share of the Global 5G Infrastructure ASIC Market, holding around 29% of the global revenue in 2024. It benefits from robust telecom investments, extensive 5G rollout by major carriers, and strong demand for custom chipsets that support mmWave and edge computing. The region is home to leading semiconductor companies that focus on developing high-performance ASICs for data centers, base stations, and small cells. Strong support for AI-enabled infrastructure and edge intelligence further drives ASIC adoption. It remains a leader in telecom innovation and benefits from well-established R&D ecosystems and government initiatives. The market continues to grow rapidly, supported by rising enterprise adoption of private 5G networks.

Europe

The Europe 5G Infrastructure ASIC Market size was valued at USD 528.30 million in 2018 to USD 1,087.13 million in 2024 and is anticipated to reach USD 4,629.95 million by 2032, at a CAGR of 18.4% during the forecast period. Europe represents around 20% of the Global 5G Infrastructure ASIC Market in 2024. It benefits from coordinated efforts across the EU to strengthen digital infrastructure, promote Open RAN, and reduce reliance on legacy networks. Countries such as Germany, the UK, and France are driving 5G investments in smart manufacturing, mobility, and public services. European semiconductor firms are aligning ASIC development with energy-efficient and security-compliant designs. The market remains focused on regulatory compliance and interoperability, creating opportunities for ASIC platforms that offer configurability. It also gains from increasing demand for private network infrastructure in industrial and logistics sectors.

Asia Pacific

The Asia Pacific 5G Infrastructure ASIC Market size was valued at USD 1,075.64 million in 2018 to USD 2,421.36 million in 2024 and is anticipated to reach USD 11,965.40 million by 2032, at a CAGR of 20.7% during the forecast period. Asia Pacific dominates the Global 5G Infrastructure ASIC Market with over 44% market share in 2024. It benefits from rapid deployment of 5G base stations, dense urbanization, and the presence of major chipset manufacturers in China, Japan, South Korea, and Taiwan. Government-backed initiatives support infrastructure development at scale, while operators aggressively expand network coverage in rural and metro areas. Regional players develop ASICs tailored to local 5G specifications and frequency bands, accelerating domestic production. The growing adoption of AI, industrial IoT, and connected mobility applications creates sustained demand for performance-optimized chips. It remains the growth engine for global 5G infrastructure deployment.

Latin America

The Latin America 5G Infrastructure ASIC Market size was valued at USD 122.93 million in 2018 to USD 263.04 million in 2024 and is anticipated to reach USD 1,081.39 million by 2032, at a CAGR of 17.9% during the forecast period. Latin America contributes roughly 5% of the Global 5G Infrastructure ASIC Market in 2024. Countries such as Brazil, Mexico, and Chile are gradually rolling out 5G infrastructure with support from international telecom vendors. The market is expanding due to the rising demand for high-speed connectivity in urban areas and industrial zones. Telecom providers seek compact and cost-effective ASICs to support small cell deployments and limited-spectrum networks. It shows potential for future growth as operators invest in coverage expansion and private 5G initiatives. Economic conditions and regulatory developments influence market adoption across the region.

Middle East

The Middle East 5G Infrastructure ASIC Market size was valued at USD 73.03 million in 2018 to USD 144.69 million in 2024 and is anticipated to reach USD 567.34 million by 2032, at a CAGR of 17.2% during the forecast period. The Middle East holds just over 3% of the Global 5G Infrastructure ASIC Market in 2024. Gulf nations such as the UAE, Saudi Arabia, and Qatar are early adopters of 5G and have made strategic investments in telecom modernization. The region is leveraging 5G infrastructure to support smart city development, AI adoption, and national digital strategies. Demand for ASICs is rising in sectors such as oil and gas, logistics, and defense, where real-time communication and reliability are critical. It benefits from partnerships with global chipmakers to deploy advanced hardware solutions. The market continues to attract investment through government-backed innovation programs.

Africa

The Africa 5G Infrastructure ASIC Market size was valued at USD 51.25 million in 2018 to USD 120.17 million in 2024 and is anticipated to reach USD 467.06 million by 2032, at a CAGR of 17.1% during the forecast period. Africa represents under 3% of the Global 5G Infrastructure ASIC Market in 2024. The region remains in early stages of 5G rollout, with pilot deployments underway in South Africa, Nigeria, and Kenya. Market growth is supported by rising mobile data usage and demand for digital connectivity in urban centers. ASIC adoption is limited but expected to increase as operators explore cost-efficient 5G hardware for remote and underserved areas. It offers long-term opportunities through international collaborations, regulatory reforms, and investment in digital infrastructure. The market outlook depends on economic development and technology access across key African economies.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Qualcomm

- Nokia

- Ericsson

- Huawei

- Samsung

- Marvell Technology

- Intel

- Broadcom

- NXP Semiconductors

- MediaTek

Competitive Analysis:

The Global 5G Infrastructure ASIC Market features a competitive landscape dominated by major semiconductor companies, telecom equipment manufacturers, and specialized chip design firms. Key players include Qualcomm, Broadcom, Intel, Samsung Electronics, Huawei, MediaTek, Marvell Technology, and Analog Devices. These companies invest heavily in R&D to develop custom ASICs optimized for 5G base stations, small cells, and network edge devices. It favors vendors capable of delivering low-latency, high-throughput, and energy-efficient designs aligned with evolving telecom standards. Strategic collaborations between chipmakers and telecom operators are accelerating product innovation and shortening deployment cycles. Market participants focus on differentiating through advanced packaging, AI integration, and open architecture support. The presence of vertically integrated firms strengthens competitive positioning, while emerging players target niche segments such as Open RAN and private networks. The market remains dynamic, with technology advancements and regional 5G rollouts shaping competitive priorities and driving long-term growth strategies.

Recent Developments:

- In June 2025, Nokia announced a strategic partnership with Andorix to accelerate the adoption of private 5G and edge networks in North America. This collaboration is focused on providing real estate owners with 5G private cellular platforms, supporting operational technology use cases such as energy management, building operations, and cybersecurity.

- In March 2025, Qualcomm introduced major advancements at Mobile World Congress (MWC) by launching the Qualcomm X85 5G Modem-RF and the Dragonwing cellular infrastructure platform, specifically designed for 5G Open RAN and advanced fixed wireless access. These solutions target industrial, embedded IoT, and networking applications, aiming to deliver enhanced speed, efficiency, and AI-powered connectivity for next-generation 5G infrastructure.

- In January 2025, Extoll announced a partnership with BeammWave and GlobalFoundries to supply SerDes IP for high-speed, low-power ASICs. This collaboration is aimed at supporting BeammWave’s development of mmWave 5G/6G beamforming technology by providing power-efficient, high-speed connectivity.

- In February 2023, Astella Technologies Limited introduced new 5G infrastructure software products at the Mobile World Congress 2023 in Barcelona. This launch reflects the growing momentum in the 5G infrastructure segment, with companies focusing on delivering advanced solutions to support the global rollout of 5G networks.

Market Concentration & Characteristics:

The Global 5G Infrastructure ASIC Market exhibits a moderately high level of concentration, with a few large players holding significant market shares due to their technical expertise, manufacturing capacity, and long-standing partnerships with telecom operators. It is characterized by high entry barriers, driven by complex design requirements, substantial R&D investment, and dependence on advanced semiconductor fabrication processes. The market favors vertically integrated companies that can manage design, testing, and production in-house. Product lifecycles are relatively short, with rapid innovation cycles shaped by evolving 5G standards and deployment needs. It prioritizes performance efficiency, power optimization, and support for domain-specific applications such as AI, edge computing, and mmWave technologies. Competitive differentiation often relies on integration capabilities, IP ownership, and the ability to deliver custom solutions aligned with telecom-grade requirements.

Report Coverage:

The research report offers an in-depth analysis based on infrastructure type, component, and application. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Demand for customized ASICs will rise with the global expansion of standalone 5G networks.

- Increased deployment of private 5G in industrial sectors will create niche opportunities for chip designers.

- AI and machine learning integration in ASICs will drive real-time decision-making at the network edge.

- Open RAN adoption will push development of flexible, standards-compliant ASIC platforms.

- Advancements in packaging technologies will improve chip density and thermal efficiency.

- Emerging markets in Latin America, the Middle East, and Africa will accelerate demand for cost-effective 5G ASIC solutions.

- Strategic partnerships between telecom providers and semiconductor firms will shape product innovation cycles.

- Government incentives and digital infrastructure initiatives will support regional market growth.

- Increased focus on energy efficiency and sustainability will influence next-generation ASIC designs.

- Rising data consumption from IoT, AR/VR, and smart city projects will sustain long-term market momentum.