Advanced Therapy Medicinal Products (ATMP) CDMO Market Overview:

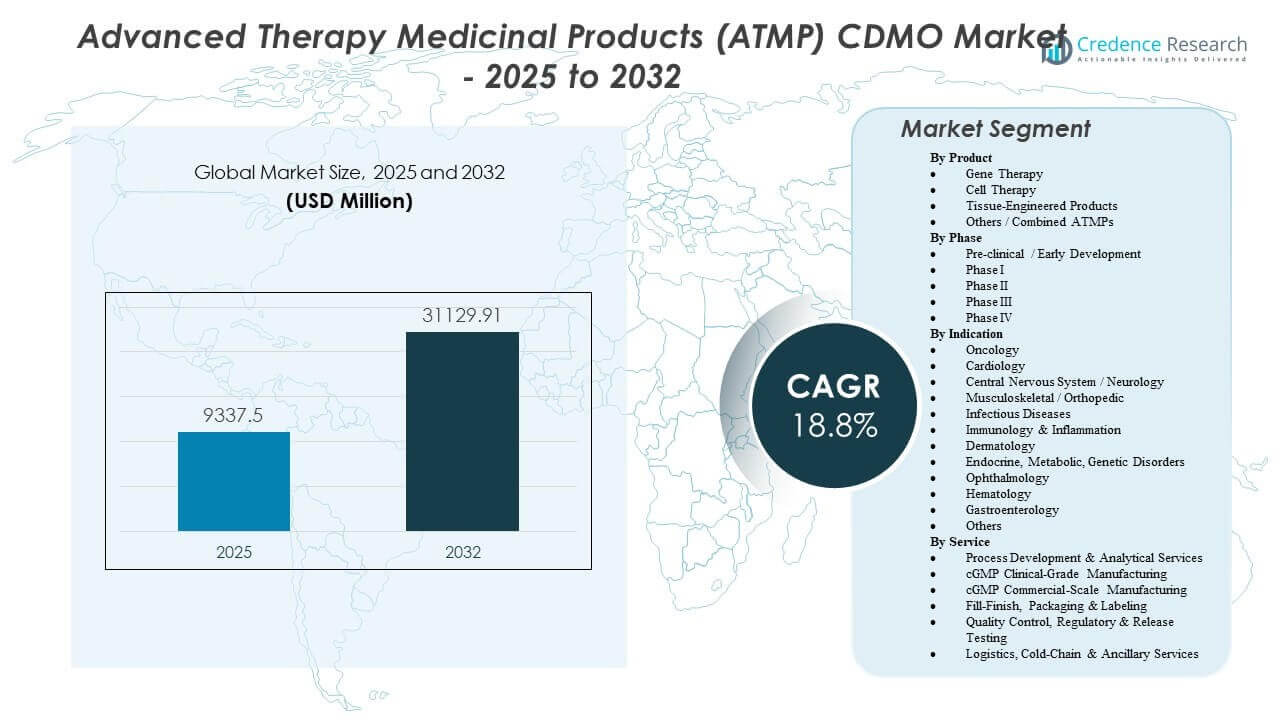

The Advanced Therapy Medicinal Products (ATMP) CDMO Market is projected to grow from USD 9,337.5 million in 2025 to an estimated USD 31,129.91 million by 2032, with a compound annual growth rate (CAGR) of 18.8% from 2025 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Advanced Therapy Medicinal Products (ATMP) CDMO Market Size 2025 |

USD 9,337.5 million |

| Advanced Therapy Medicinal Products (ATMP) CDMO Market, CAGR |

18.8% |

| Advanced Therapy Medicinal Products (ATMP) CDMO Market Size 2032 |

USD 31,129.91 million |

Advanced Therapy Medicinal Products (ATMP) CDMO Market Insights:

- Strong clinical pipelines and increasing commercialization of ATMPs fuel demand for viral vectors, scalable cell therapy production, and specialized GMP services across global developers.

- High capital needs, limited in-house expertise, and complex regulatory requirements remain key restraints that push sponsors toward outsourcing but create operational challenges for smaller firms.

- North America leads the market due to a mature biotech ecosystem and advanced manufacturing capabilities, while Europe follows with strong regulatory frameworks and established vector hubs.

- Asia Pacific emerges as the fastest-growing region, supported by expanding GMP infrastructure, strategic investments, and increasing involvement of regional biotech players in ATMP development.

Advanced Therapy Medicinal Products (ATMP) CDMO Market Drivers

Rapid Expansion Of Cell And Gene Therapy Clinical Programs Across Major Therapeutic Areas

Cell and gene therapy pipelines continue to expand across oncology and rare diseases. Sponsors advance more candidates into Phase II and Phase III trials. This shift increases demand for clinical-grade and commercial manufacturing capacity. The Advanced Therapy Medicinal Products (ATMP) CDMO Market gains momentum from this pipeline depth. Developers require scalable viral vector and cell processing platforms. Commercial readiness demands validated and reproducible production systems. Long-term contracts secure supply continuity for approved therapies. Strong investor support further fuels outsourcing activity.

- For instance, Novartis reported over 6,000 global patients treated with its CAR-T therapy Kymriah®, reflecting rising clinical and commercial demand.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Limited In-House Manufacturing Capabilities Among Emerging Biotech Companies

Many small and mid-sized biotech firms lack GMP infrastructure. Internal manufacturing facilities require high upfront capital and regulatory expertise. Sponsors prefer experienced CDMOs to manage complex production workflows. Outsourcing reduces operational risk and accelerates development timelines. Specialized partners provide vector engineering and analytical support. Flexible capacity allows clients to adapt to trial outcomes. Strategic partnerships improve efficiency across development stages. Asset-light strategies strengthen financial discipline.

Complex Regulatory Requirements And Stringent Quality Standards

ATMP products face strict regulatory oversight across major markets. Documentation demands detailed validation and quality data. CDMOs offer regulatory knowledge and inspection readiness. Sponsors rely on established quality systems to reduce approval risk. Standardized procedures support consistent product performance. Compliance expertise enhances credibility with authorities. Risk mitigation becomes central in advanced clinical phases. Strong quality frameworks drive outsourcing preference.

Growing Commercialization Of Approved Advanced Therapies

Approved gene and cell therapies move into broader patient access programs. Commercial supply requires stable and high-volume production capacity. CDMOs invest in expanded GMP suites to meet this need. Sponsors prioritize reliable manufacturing partners. Technology transfer from clinical to commercial scale requires expertise. Lifecycle management supports sustained market presence. Post-approval commitments increase operational complexity. Commercial growth sustains long-term CDMO demand.

- For instance, Catalent Cell & Gene Therapy scaled AAV manufacturing for Zolgensma at its Harmans, Maryland facility, a 200,000-square-foot site equipped with 18 cGMP suites that supports Novartis’ global gene therapy programs.

Advanced Therapy Medicinal Products (ATMP) CDMO Market Trends

Shift Toward End-To-End Integrated Service Offerings

Clients seek single partners that manage development through commercialization. CDMOs expand portfolios to include analytics, fill-finish, and logistics. Integrated models improve coordination across project stages. Sponsors reduce vendor fragmentation and oversight burden. Comprehensive services strengthen client retention. Vertical integration enhances competitive differentiation. Multi-year strategic alliances replace short-term contracts. Consolidated service models improve operational efficiency.

Adoption Of Automation And Closed Manufacturing Platforms

Automation improves precision in cell expansion and vector production. Closed systems reduce contamination risk and manual variability. Robotics enhance reproducibility across patient-specific batches. Digital controls strengthen process oversight. Automation reduces dependence on manual intervention. Standardized systems support scalable allogeneic production. Technology upgrades drive higher facility utilization. Operational efficiency improves through smart manufacturing tools.

Geographic Diversification Of Manufacturing Footprint

CDMOs expand into Asia Pacific and emerging biotech hubs. Regional facilities reduce logistics risk and delivery time. Governments support biotech investment through incentives. Local capacity strengthens supply chain resilience. Sponsors seek diversified production networks. Cross-border partnerships accelerate market entry. Regional expertise enhances regulatory alignment. Geographic spread improves global competitiveness.

- For instance, FUJIFILM Diosynth Biotechnologies expanded its global capabilities by acquiring the large-scale biologics facility in Hillerød, Denmark, which includes six 15,000-liter stainless-steel bioreactors and supports major commercial biologics manufacturing for global clients.

Investment In Next-Generation Vector And Cell Platforms

Innovation in AAV and lentiviral systems increases efficiency. High-yield production platforms improve scalability. Allogeneic cell therapies gain attention for broader use. Advanced analytics enhance process optimization. Novel bioreactor systems improve output consistency. Platform technologies shorten development timelines. Continuous improvement drives service differentiation. Innovation focus secures long-term growth potential.

- For instance, AGC Biologics introduced its BravoAAV™ and ProntoLVV™ platforms, using scalable suspension bioprocesses of up to 2,000 L for AAV and 1,000 L for LVV to boost vector production efficiency. These templated systems cut GMP readiness timelines to about nine months, supporting faster advancement of gene therapy programs.

Advanced Therapy Medicinal Products (ATMP) CDMO Market Challenges Analysis

Capacity Constraints And Supply Chain Bottlenecks In Viral Vector Production

Viral vector supply remains limited in several regions. Lead times for plasmids and raw materials extend project timelines. Facility expansion requires regulatory inspections and validation. The Advanced Therapy Medicinal Products (ATMP) CDMO Market faces pressure to meet urgent demand. Cold chain logistics add complexity for global distribution. Specialized workforce shortages slow expansion plans. Quality compliance standards remain strict and resource intensive. Sponsors expect rapid turnaround and consistent output. Balancing demand and supply remains a key challenge.

Regulatory Variability And High Cost Structures Across Global Markets

Regulatory pathways differ across major regions. Documentation standards demand extensive validation data. Compliance audits require dedicated quality teams. High operating costs impact pricing strategies. Smaller developers face funding pressure during clinical delays. Currency volatility affects cross-border contracts. Intellectual property risks complicate partnerships. Contract negotiations involve detailed risk-sharing terms. These factors increase operational strain on CDMOs.

Advanced Therapy Medicinal Products (ATMP) CDMO Market Opportunities

Expansion Into Emerging Biotech Hubs And Regional Manufacturing Platforms

Emerging biotech clusters invest in advanced biologics infrastructure. Governments provide incentives to attract ATMP facilities. The Advanced Therapy Medicinal Products (ATMP) CDMO Market can expand through regional partnerships. Local production reduces logistics risk and cost. Regional GMP sites support faster patient access. Joint ventures create shared investment models. Technology transfer programs strengthen local expertise. Early entry into new markets secures long-term contracts. Geographic diversification improves resilience.

Growth Of Allogeneic Platforms And Next-Generation Vector Technologies

Allogeneic therapies aim for scalable off-the-shelf production. Standardized cell lines simplify manufacturing workflows. Novel vector platforms improve transduction efficiency. High-capacity suspension systems enhance output. Advanced analytics shorten release timelines. Personalized medicine trends support niche therapy production. Digital twins improve process optimization. Strategic investments in innovation create differentiation. These developments open new revenue pathways for CDMOs.

Advanced Therapy Medicinal Products (ATMP) CDMO Market Segmentation Analysis:

By Product

The product landscape covers gene therapy, cell therapy, tissue-engineered products, and combined ATMPs. In the Advanced Therapy Medicinal Products (ATMP) CDMO Market, gene therapy holds strong demand due to viral vector-based platforms such as AAV and lentiviral systems. These vectors support rare disease and oncology pipelines. Cell therapy includes CAR-T, stem cell, and non-stem cell formats across autologous and allogeneic models. Autologous therapies require patient-specific manufacturing, while allogeneic platforms aim for scale. Tissue-engineered products rely on scaffolds and matrices for structural repair. Hybrid gene-cell therapies and biodegradable scaffolds expand complex treatment options.

- For instance, WuXi Advanced Therapies launched the OXGENE TESSA™ technology for AAV manufacturing, which eliminates the need for plasmid transfection and has demonstrated a 10-fold increase in AAV yield compared to traditional triple transfection methods.

By Phase

Development phases range from pre-clinical and early development to Phase I through Phase IV. Early-stage programs focus on process design and safety validation. Phase I and II emphasize dose optimization and controlled batch production. Phase III requires larger volumes and validated GMP systems. Phase IV supports post-approval supply and lifecycle management. Sponsors increase outsourcing at later phases to secure commercial readiness. Risk mitigation and regulatory compliance become critical in advanced stages. CDMOs align capacity with clinical progression.

By Indication

Oncology leads due to high adoption of CAR-T and gene-modified therapies. Cardiology and neurology expand through regenerative and gene-based programs. Musculoskeletal and orthopedic segments use tissue-engineered scaffolds for repair. Infectious diseases and immunology leverage gene editing and immune modulation. Dermatology and ophthalmology support localized gene delivery models. Endocrine and genetic disorders rely on durable gene correction. Hematology remains central to viral vector and stem cell demand. Gastroenterology and other indications create niche manufacturing needs.

By Service

Service offerings span process development to logistics support. Process development and analytical services build scalable and compliant workflows. cGMP clinical-grade manufacturing supports early and mid-stage trials. Commercial-scale production requires validated facilities and robust supply systems. Fill-finish, packaging, and labeling ensure product integrity. Quality control and regulatory testing maintain compliance standards. Cold-chain logistics manage temperature-sensitive materials. Integrated service models improve efficiency across development cycles.

- For instance, Thermo Fisher Scientific’s Patheon services introduced the Quick to Care™ program, integrating drug substance and drug product manufacturing with clinical packaging to streamline early development workflows. The platform enables emerging biotech companies to accelerate readiness for clinical supply by consolidating steps that traditionally require multiple service partners.

Segmentation:

By Product

- Gene Therapy

- Viral Vector-based

- Cell Therapy

- CAR-T

- Stem Cell

- Non-Stem Cell

- Autologous

- Allogeneic

- Tissue-Engineered Products

- Others / Combined ATMPs

- Hybrid Gene-Cell

- Biodegradable Scaffolds

By Phase

- Pre-clinical / Early Development

- Phase I

- Phase II

- Phase III

- Phase IV

By Indication

- Oncology

- Cardiology

- Central Nervous System / Neurology

- Musculoskeletal / Orthopedic

- Infectious Diseases

- Immunology & Inflammation

- Dermatology

- Endocrine, Metabolic, Genetic Disorders

- Ophthalmology

- Hematology

- Gastroenterology

- Others

By Service

- Process Development & Analytical Services

- cGMP Clinical-Grade Manufacturing

- cGMP Commercial-Scale Manufacturing

- Fill-Finish, Packaging & Labeling

- Quality Control, Regulatory & Release Testing

- Logistics, Cold-Chain & Ancillary Services

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America holds the largest share of the Advanced Therapy Medicinal Products (ATMP) CDMO Market, accounting for nearly 45% of global revenue. Strong biotech funding and a high concentration of gene and cell therapy developers support this dominance. The United States leads regional growth with advanced GMP infrastructure and clear regulatory pathways. Canada supports expansion through research grants and academic collaborations. Europe captures around 30% of the market, driven by Germany, the U.K., and France. Robust EMA frameworks and cross-border research programs strengthen regional capacity. The region benefits from established viral vector and cell processing hubs.

Asia Pacific represents close to 20% of global share and records the fastest expansion rate. China and Japan invest heavily in gene therapy production and domestic biotech innovation. South Korea and India expand GMP capacity through public and private partnerships. Government incentives encourage technology transfer and facility development. Lower operating costs attract international outsourcing contracts. Skilled workforce availability improves technical output. Regional players pursue strategic alliances with Western biotech firms.

Latin America and the Middle East & Africa collectively account for nearly 5% of the market. Brazil and Mexico lead activity in Latin America through clinical research initiatives. GCC countries invest in advanced healthcare infrastructure and biotechnology parks. South Africa supports regional clinical trial networks. Market penetration remains limited due to regulatory gaps and funding constraints. Local partnerships help global CDMOs enter emerging markets. Gradual policy reforms aim to attract foreign investment.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Lonza Group

- Catalent Inc.

- Thermo Fisher Scientific (Patheon)

- AGC Biologics

- FUJIFILM Diosynth Biotechnologies

- Charles River Laboratories

- Oxford Biomedica PLC

- WuXi Advanced Therapies

- Minaris Regenerative Medicine

- Aldevron

- Samsung Biologics

- Rentschler Biopharma SE

- CELONIC Group

- Eurofins Scientific SE

- RoslinCT

- Andelyn Biosciences

- BlueReg

- CGT Catapult

- Curia Global Inc.

- Bio Elpida by Polyplus

Competitive Analysis:

The Advanced Therapy Medicinal Products (ATMP) CDMO Market features a mix of specialized biotech manufacturers and diversified global CDMOs. Leading players focus on viral vector scale-up, cell therapy automation, and integrated service models. Companies invest in capacity expansion across North America and Europe to secure long-term contracts. Strategic acquisitions strengthen technical expertise in AAV and lentiviral platforms. Partnerships with biotech startups create early access to high-potential pipelines. Firms compete on regulatory track record, turnaround time, and quality compliance. Integrated offerings that span process development to commercial manufacturing provide a strong edge. Price competition remains secondary to technical capability and reliability. Capacity expansion and geographic diversification shape long-term competitive positioning.

Recent Developments:

- In January 2024, Pluri, an Israel-based biotech company, launched PluriCDMO, a new division offering cell therapy manufacturing services as a contract development and manufacturing organization (CDMO), featuring a 47,000-square-foot GMP facility.

- In January 2024, Charles River Laboratories International Inc. introduced its off-the-shelf Rep/Cap plasmid offering to streamline adeno-associated virus (AAV)-based gene therapy programs.

Report Coverage:

The research report offers an in-depth analysis based on Product, Phase, Indication, Service and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Demand for integrated development and commercial manufacturing platforms will strengthen long-term outsourcing partnerships.

- Expansion of allogeneic cell therapy programs will improve scalability and standardization across production sites.

- Automation and closed-system technologies will enhance batch consistency and reduce operational risk.

- Viral vector innovation will increase transduction efficiency and improve manufacturing yields.

- Strategic alliances between CDMOs and biotech startups will accelerate early-stage program transitions.

- Regional manufacturing hubs in Asia Pacific will attract cross-border clinical supply contracts.

- Advanced analytics and digital quality systems will support regulatory compliance and data integrity.

- Investment in modular GMP facilities will provide flexible capacity for multi-product pipelines.

- Growth in rare disease and oncology pipelines will sustain high-value service contracts.

- Cold-chain logistics and specialized distribution networks will expand to support global commercialization.