Africa Bunkering Market Overview:

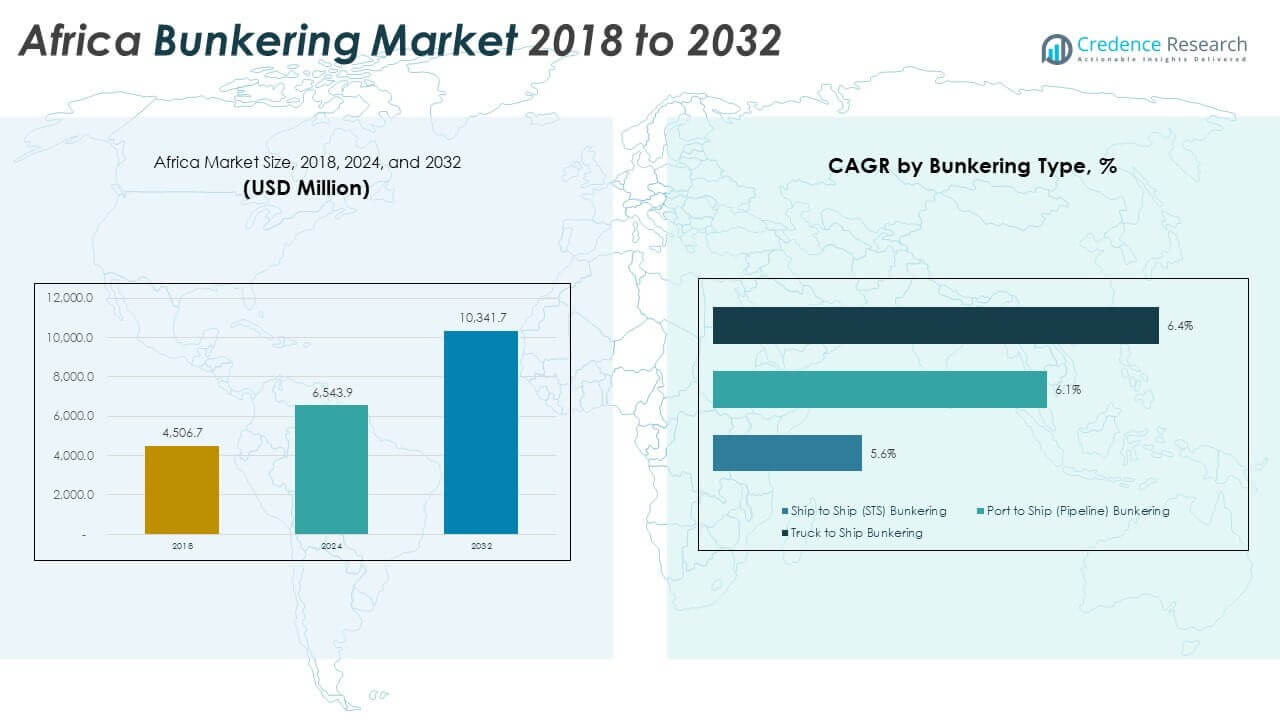

The Africa Bunkering Market size was valued at USD 4,506.70 million in 2018 to USD 6,543.90 million in 2024 and is anticipated to reach USD 10,341.70 million by 2032, at a CAGR of 5.87% during the forecast period.

Strong growth in the market is driven by rising offshore exploration, increasing port modernization, and wider adoption of cleaner marine fuels.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Africa Bunkering Market Size 2024 |

USD 6,543.90 million |

| Africa Bunkering Market, CAGR |

5.87% |

| Africa Bunkering Market Size 2032 |

USD 10,341.70 million |

Africa Bunkering Market Insights

- North Africa (38%), West Africa (32%), and South & East Africa (30%) hold the largest shares due to strong trade corridors, active offshore operations, and well-developed port infrastructure that attract high vessel traffic and diverse fuel demand.

- East Africa emerges as the fastest-growing subregion with its rising share supported by port modernization, stronger coastal logistics, and increasing vessel movement across Indian Ocean trade lanes.

- Ship-to-Ship bunkering leads segment growth with a CAGR of 6.4%, supported by offshore vessel activity and flexible fueling demand across deep-water routes.

- Port-to-Ship (6.1%) and Truck-to-Ship (5.6%) show stable expansion as ports upgrade pipeline systems and smaller coastal fleets rely on truck-based fueling across emerging marine hubs.

Africa Bunkering Market Drivers

Strong Expansion of Maritime Trade Lanes and Vessel Traffic Growth Across Key African Ports

Rising vessel movement across major African corridors strengthens bunker fuel consumption and drives wider service requirements. Growing cargo volumes through Suez-linked and Atlantic trade routes support consistent demand for marine fuels. The Africa Bunkering Market gains momentum as port throughput increases across major coastal countries. It encourages suppliers to expand storage and fueling capacity to match higher vessel calls. Shipping companies rely on predictable fueling points to maintain schedules and reduce transit delays. Port authorities introduce digital systems that improve documentation and visibility. Investment in dredging projects supports entry of larger vessels that require higher fuel volumes. Stronger maritime trade creates stable long-term demand for bunker suppliers. Coastal expansion programs reinforce regional competitiveness.

- For instance, the Tanger Med Port Complex surpassed 11.1 million TEUs in 2025 after major capacity upgrades, while APM Terminals MedPort Tangier expanded its own capacity to 5.2 million TEUs with advanced auto-mooring and digital planning systems that cut vessel idle time by nearly one hour per call.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Rising Offshore Exploration and Production Activity Supporting Fuel Demand for Supply Vessels and Floating Units

Growing offshore drilling programs increase the need for continuous fuel support for supply fleets and workboats. Exploration projects off West and East Africa create stronger reliance on marine fuels for round-the-clock operations. It pushes suppliers to maintain reliable logistics networks that meet offshore timelines. Support vessels require efficient refueling to manage long distances between bases and offshore fields. Fuel distributors increase safety standards to secure offshore delivery operations. Oilfield expansion strengthens coastal support hubs and boosts regional bunker storage development. Marine logistics companies invest in high-capacity vessels to ensure stable supply. Strong offshore activity shapes long-term growth for service providers. Fuel demand stays resilient across exploration cycles.

- For instance, MODEC’s FPSO operations offshore Ghana require continuous marine fuel support for fleets servicing the Jubilee and TEN fields, supporting hundreds of supply-vessel trips annually.

Shift Toward Cleaner Marine Fuels Driven by IMO Regulations and Low-Sulfur Fuel Adoption

Stricter emission norms push operators to adopt low-sulfur fuels and cleaner blends across regional ports. Compliance with IMO 2020 standards strengthens interest in advanced bunker formulations. The Africa Bunkering Market sees growing investment in sulfur-compliant fuels that reduce environmental risk. It encourages refiners to upgrade systems to deliver higher-quality outputs. Shippers prefer ports with reliable availability of compliant fuels. Supply chains adapt their storage infrastructure to prevent contamination and maintain product quality. Fuel testing standards improve trust between buyers and suppliers. Cleaner fuel transition supports long-term market modernization. Regulatory alignment boosts regional competitiveness.

Port Modernization Programs Driving Infrastructure Expansion and Enhanced Fueling Efficiency

Major African ports invest in berths, storage terminals, and automation systems to support efficient fueling operations. These upgrades shorten turnaround times for vessels that require quick refueling. It creates a reliable ecosystem that attracts more shippers seeking predictable fueling services. Improved port layouts reduce congestion and improve truck and barge movement. Digital scheduling tools improve slot management and strengthen operational transparency. Investment in new pipelines and storage tanks raises supply stability. Terminal operators adopt modern metering systems for accurate fuel measurement. Infrastructure upgrades reinforce safety standards across fueling zones. Strong modernization momentum elevates regional competitiveness.

Africa Bunkering Market Trends

Greater Adoption of Digital Bunkering Platforms and Automated Fuel Management Systems

Port authorities and bunker suppliers implement digital systems to streamline booking and documentation. Digital platforms reduce human error and strengthen trust between buyers and sellers. The Africa Bunkering Market gains visibility through wider use of automated metering and fuel tracking tools. It supports faster verification of quantity and quality for each delivery. Suppliers adopt blockchain-supported systems to document transactions securely. Automation reduces dispute risks and strengthens compliance in regulated ports. Remote monitoring tools help suppliers track fleet movement and plan fueling cycles. Growing digitalization improves operational reliability. Market participants move toward paperless processes.

- For instance,TFG Marine has equipped its bunker barges in South Africa with Coriolis Mass Flow Meters (MFM), achieving a measurement precision of ±0.5%, which significantly eliminates the “cappuccino effect” (air entrainment) compared to traditional manual sounding tape methods.

Growing Interest in LNG, Biofuels, and Alternative Fuels for Maritime Decarbonization Pathways

Global decarbonization targets encourage shippers to explore cleaner marine energy sources. LNG bunkering gains early traction in ports with supportive infrastructure plans. It pushes suppliers to study long-term storage and safety requirements. Biofuels emerge as a flexible alternative for operators seeking lower emissions. Early pilot projects in North and West Africa open opportunities for blended solutions. Shipowners test dual-fuel engines to reduce carbon footprints. Suppliers assess the viability of green ammonia and methanol in future plans. Cleaner fuel experimentation shapes strategic direction. Environmental targets influence long-term planning.

Expansion of Strategic Bunkering Hubs Driven by Geopolitical Positioning and Trade Route Alignment

African coastal nations position their ports to attract global shipping lines seeking strategic refueling points. Strong demand along the Mediterranean and Indian Ocean routes supports development of major hubs. The Africa Bunkering Market benefits from the continent’s location near key global corridors. It encourages investment in multipurpose terminals that support both cargo and fuel operations. Governments promote regulatory clarity to attract international bunker suppliers. Port clusters evolve into transit centers for long-haul vessels. Operators expand capacity to handle different fuel grades. Geographic advantage strengthens growth momentum. Competitive positioning increases regional visibility.

- For instance, Namibia’s National Oil Storage Facility at the Port of Walvis Bay expanded to a capacity of 75 million liters, strengthening the port’s role as a regional bunkering hub and enabling Namport to handle rising fuel demand linked to increased rerouting of vessels around the Cape of Good Hope.

Growing Integration of Safety, Compliance, and Quality-Control Technologies Across Bunkering Operations

Bunker suppliers invest in safety systems that minimize contamination and enhance product integrity. New testing technologies improve real-time detection of impurities. It supports stronger trust among long-distance vessel operators. Quality-control protocols strengthen inspections at storage terminals. Regulatory bodies introduce stricter compliance checks for blending and transfer operations. Fuel sampling automation lowers procedural risks. Training programs for bunkering crews become more structured. Safety upgrades improve reliability across fueling zones. The trend supports consistent market improvement.

Africa Bunkering Market Challenges Analysis

Infrastructure Limitations and Supply Chain Inefficiencies Constrain Fuel Availability and Delivery Performance

Many African ports face constraints linked to limited storage capacity and outdated fueling systems. These gaps restrict the ability to serve large vessels that require fast turnaround. The Africa Bunkering Market operates within complex supply networks that struggle with inconsistent delivery timelines. It pushes suppliers to manage high operational costs across multiple logistics layers. Congestion at major ports weakens delivery efficiency and slows vessel scheduling. Limited pipeline networks increase reliance on trucks and barges, which raises risk exposure. Maintenance delays disrupt fuel flow and reduce supply reliability. Some regions lack advanced metering systems that ensure accurate transfer. Infrastructure gaps hinder competitive growth.

Regulatory Inconsistencies, Price Volatility, and High Compliance Costs Impact Supplier Profitability

Different regulatory frameworks across coastal nations create uncertainty for suppliers planning long-term operations. Compliance with environmental rules raises operational spending for many companies. The Africa Bunkering Market faces challenges linked to unstable fuel pricing influenced by global crude fluctuations. It forces operators to adjust procurement cycles frequently. Limited enforcement mechanisms in some regions weaken transparency. Taxation differences across borders complicate pricing structures. Suppliers face slow permitting processes in select jurisdictions. Price swings force buyers to shift sourcing strategies. These barriers reduce market predictability.

Africa Bunkering Market Opportunities

Expansion of Clean Fuel Infrastructure and Alternative Fuel Adoption Across Emerging African Ports

Growing interest in LNG, biofuel blends, and low-sulfur products opens opportunities for suppliers to diversify portfolios. The Africa Bunkering Market can expand through investment in clean fuel storage and transfer systems. It strengthens long-term competitiveness across ports seeking alignment with global decarbonization trends. Governments explore incentives to attract early-stage projects that support cleaner fuel adoption. New terminals designed for multiproduct handling create flexible growth pathways. International partnerships help ports gain technical expertise. Operators can secure first-mover advantages in new fuel categories. Cleaner energy adoption encourages more vessel calls. The opportunity supports sustainable expansion.

Strategic Port Modernization, Regional Collaboration, and Technology Integration Driving New Growth Paths

Modernization programs create strong openings for suppliers investing in advanced bunkering equipment. It enables smoother coordination between cargo operations and marine fueling. Digital platforms support efficient scheduling and real-time delivery oversight. Cross-border cooperation strengthens trade routes and improves regional competitiveness. Multinational fuel companies show rising interest in African coastal markets. New pipeline projects increase supply stability in high-demand zones. Workforce development increases skill levels in fueling operations. Growing transparency boosts investor confidence. These opportunities reinforce overall market advancement.

Africa Bunkering Market Segmentation Analysis

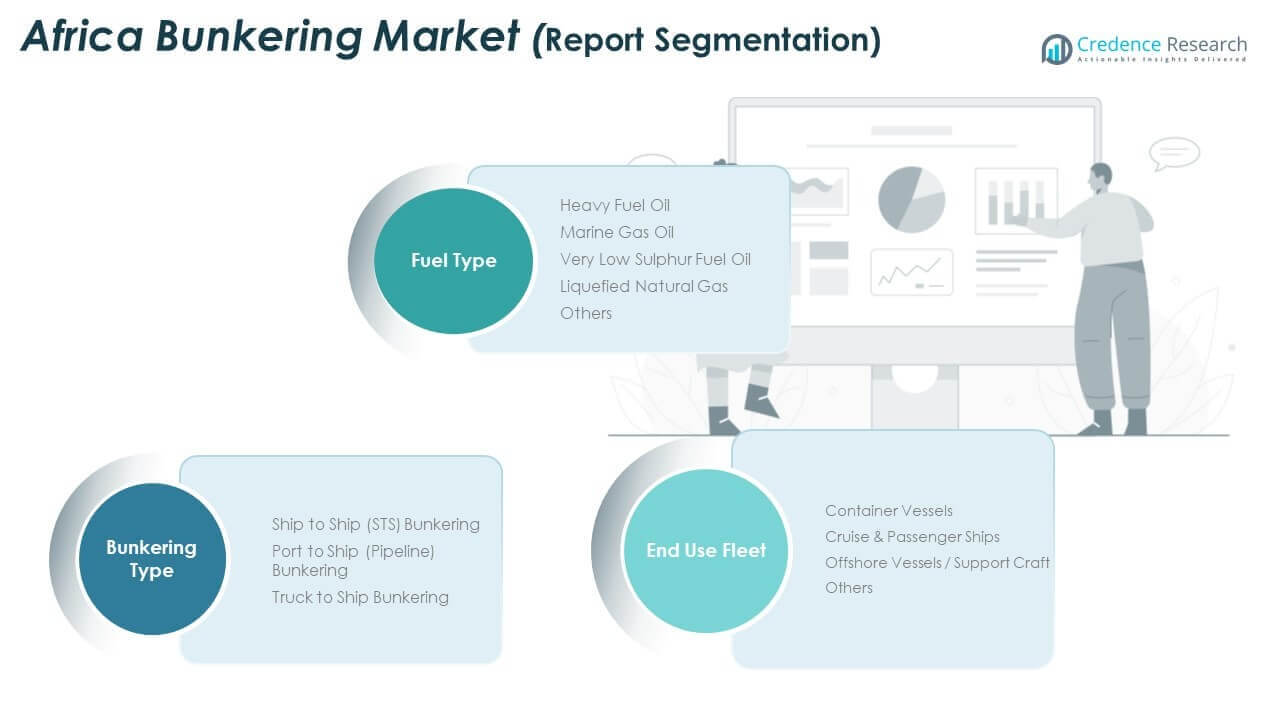

By Bunkering Type

Ship to Ship (STS) bunkering holds strong influence in the Africa Bunkering Market because it supports offshore routes and reduces congestion at busy ports. It offers flexibility for tankers and long-haul vessels that require efficient mid-sea fueling. Port to Ship bunkering grows with modern pipeline systems that improve flow control and lower operational risks. It strengthens vessel turnaround across upgraded terminals. Truck to Ship bunkering supports smaller fleets and emerging ports where infrastructure remains limited. It offers fast access to multiple fuel grades and helps coastal markets maintain supply continuity.

By Fuel Type

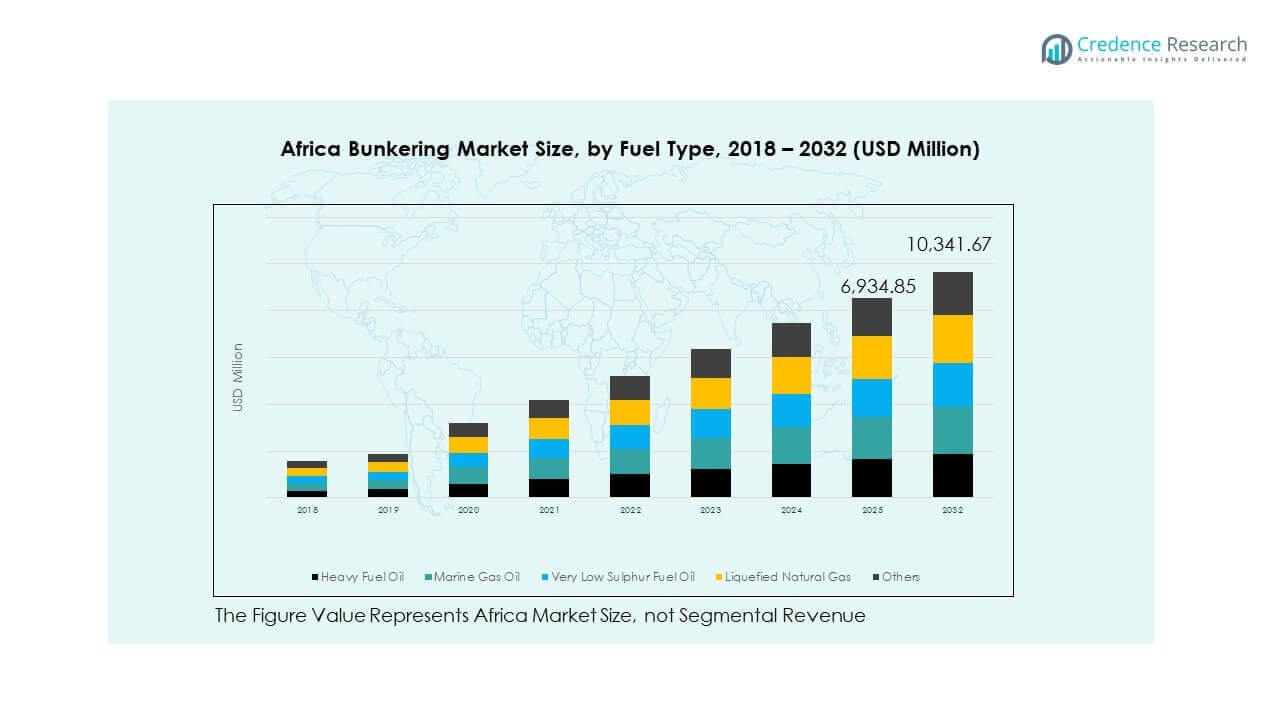

Heavy Fuel Oil continues to serve older vessels that use conventional propulsion systems, and it stays relevant across high-volume trading routes. Marine Gas Oil gains traction due to emission norms that encourage cleaner operations, and the Africa Bunkering Market supports rising demand through wider refinery output. Very Low Sulphur Fuel Oil drives compliance with IMO regulations and builds strong presence at major ports handling global fleets. Liquefied Natural Gas enters early adoption phases and supports long-term decarbonization plans. Other fuels, including biofuel blends, gain attention as shipping companies test sustainable alternatives.

- For instance, Vitol Bunkers expanded its VLSFO (0.50% sulfur) supply network in the West Africa region by deploying specialized offshore bunker tankers, ensuring ISO 8217:2017–compliant fuel quality through certified testing and controlled blending processes that support international liner operations.

By End Use Fleet

Container vessels generate strong demand due to steady trade movement and predictable scheduling across major African corridors. It encourages ports to maintain reliable inventories of compliant fuels. Cruise and passenger ships require premium-grade fuels to maintain safety and meet environmental rules, and tourism-linked development supports this segment. Offshore support vessels rely on continuous fueling for exploration, drilling, and maintenance activities, creating stable long-term demand. Other fleets, including patrol craft and fishing vessels, depend on flexible bunkering methods that support quick access across coastal regions and emerging marine hubs.

- For instance, Maersk Line has strengthened its bunkering efficiency at the Port of Algeciras and the Tanger Med hub through automated berth-planning and vessel-scheduling systems, enabling ultra-large container ships to refuel and resume transit along the North African coast with significantly reduced operational delays.

Segmentation

By Bunkering Type

- Ship to Ship (STS) Bunkering

- Port to Ship (Pipeline) Bunkering

- Truck to Ship Bunkering

By Fuel Type

- Heavy Fuel Oil

- Marine Gas Oil

- Very Low Sulphur Fuel Oil

- Liquefied Natural Gas

- Others

By End Use Fleet

- Container Vessels

- Cruise & Passenger Ships

- Offshore Vessels / Support Craft

- Others

Regional Analysis

North Africa

North Africa holds the largest share of the Africa Bunkering Market, accounting for nearly 38% of total regional revenue. Strong maritime traffic through the Suez Canal strengthens bunker demand in Egypt and supports steady growth across major ports. Morocco and Tunisia expand capacity to attract transit vessels navigating Mediterranean routes. The region invests in cleaner fuel storage to meet rising international compliance needs. It benefits from established port networks that provide predictable fueling services. Strong geopolitical positioning increases vessel stopovers across key corridors. North Africa maintains long-term strategic influence in regional bunkering activities.

West Africa

West Africa captures close to 32% of the Africa Bunkering Market due to offshore exploration activity and strong crude export routes. Nigeria and Ghana lead demand with active offshore support fleets that require continuous fueling. The region expands supply chains to support deep-water projects and vessel traffic linked to LNG and crude shipments. It strengthens market presence through flexible Ship to Ship operations near offshore fields. Regional ports invest in terminal upgrades to secure more international transit calls. Strong energy sector activity influences consumption patterns and supports stability. West Africa continues to grow due to its high concentration of maritime and offshore operations.

South & East Africa

South and East Africa combined hold roughly 30% of the Africa Bunkering Market, driven by strong port infrastructure and trade-linked marine activity. South Africa leads this subregion with Durban, Cape Town, and Richards Bay serving as major bunkering hubs for east–west trade routes. It offers reliable multi-fuel availability and supports large container vessels operating on long-haul networks. East Africa, led by Kenya and Tanzania, shows rising momentum through port modernization and increasing coastal shipping volumes. Growing logistics corridors strengthen the region’s demand base and attract global shipping lines. Strategic positioning along Indian Ocean routes supports long-term expansion. South and East Africa continue to rise as competitive bunkering clusters.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Competitive Analysis

The Africa Bunkering Market features a mix of global bunkering companies, regional suppliers, and integrated energy firms competing for strategic fueling hubs. Market leaders focus on expanding supply reliability, improving service consistency, and strengthening operational visibility across high-traffic ports. It maintains competitive movement driven by infrastructure upgrades and evolving fuel standards. Global players leverage scale advantages to secure long-term contracts with major shipping lines, while regional firms use localized knowledge to offer flexible delivery solutions. Companies invest in compliant low-sulfur fuels and real-time digital platforms to differentiate service quality. Pricing remains highly sensitive to crude movements, prompting suppliers to refine procurement strategies and expand storage capacity in key locations. Competition intensifies near offshore clusters where support vessels require predictable fueling timelines. Monjasa, Minerva Bunkering, Bunker One, and Dan-Bunkering hold strong positions through integrated supply chains and diversified marine fuel portfolios. These firms expand physical footprints across West, North, and South Africa to strengthen operational control. Local suppliers such as GOIL PLC, Vivo Energy, and Africa Bunkering & Shipping compete through tailored fueling services and regional partnerships. It drives innovation in delivery methods, including growth in Ship to Ship operations near offshore fields.

Recent Developments

- In May 2025, Vitol Bunkers launched barge-based marine fuel operations in West Africa, delivering VLSFO and MGO offshore at Dakar, Senegal, and Lomé, Togo. The flexible, port-independent model targets commercial shipping and offshore operators, with plans to expand fuel offerings. This enhances Vitol’s global network in Africa.

- In April 2025, GFS became the first physical supplier in West Africa to offer fully digitalized bunker operations by joining Ofiniti’s FuelBoss platform. They also deployed a new tanker equipped with flow meters and e-BDN capabilities for offshore and platform supply. This innovation supports efficient, tech-enabled deliveries in the region.

Report Coverage

The research report offers an in-depth analysis based on Bunkering Type, Fuel Type, and End Use Fleet. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Growing vessel traffic across major African corridors will strengthen fuel demand and support wider service expansion across regional ports.

- Rising investments in port modernization will elevate operational efficiency and attract more international shipping lines seeking reliable fueling options.

- Cleaner fuel adoption driven by compliance standards will reshape product portfolios and accelerate the shift toward low-sulfur and alternative fuels.

- Digital platforms for fuel tracking and documentation will improve transparency and reduce operational disputes across bunkering operations.

- Expansion of offshore exploration will create steady demand for support vessels that require consistent fueling cycles near deep-water fields.

- LNG and biofuel pilot projects will gain traction as shipping companies explore long-term decarbonization pathways.

- Competition among global and regional suppliers will intensify, prompting wider investment in storage, metering, and automated systems.

- Strategic positioning of North African and West African ports will strengthen their role as leading bunkering hubs on global trade routes.

- Truck-to-ship fueling will remain important in emerging coastal markets that continue to upgrade their infrastructure gradually.

- Collaborations between port authorities, refiners, and marine fuel suppliers will shape future service models and enhance regional integration.