| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Asia Pacific Bentonite Market Size 2024 |

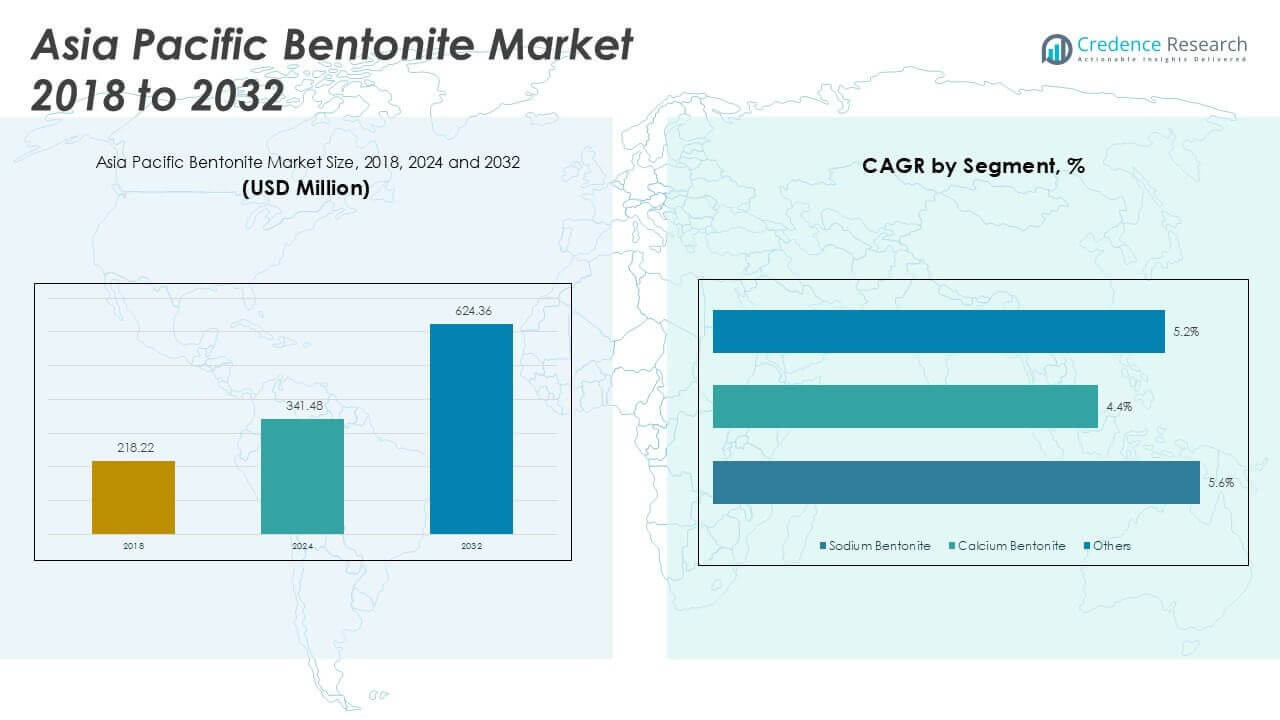

USD 341.48 million |

| Asia Pacific Bentonite Market, CAGR |

7.35% |

| Asia Pacific Bentonite Market Size 2032 |

USD 624.36 million |

Market Overview

The Asia Pacific Bentonite market size was valued at USD 218.22 million in 2018, increased to USD 341.48 million in 2024, and is anticipated to reach USD 624.36 million by 2032, at a CAGR of 7.35% during the forecast period.

In the Asia Pacific bentonite market, key players such as Ashapura Group, Kunimine Industries, Imerys, and Clariant AG dominate through extensive mining operations, diverse product portfolios, and strong regional distribution. Ashapura Group, with its significant reserves and export strength, holds a prominent position, particularly in India. Kunimine Industries leads in Japan, focusing on high-grade bentonite for industrial applications. Imerys and Clariant AG leverage technological innovation and application-specific product development to serve niche markets across Southeast Asia. Regionally, China emerges as the leading market, accounting for 38.6% of the total regional share in 2024, followed by India with 29.7%. These countries benefit from strong industrial bases, robust construction activity, and growing oil & gas operations, making them the primary growth centers for bentonite consumption in the region.

Market Insights

- The Asia Pacific bentonite market was valued at USD 218.22 million in 2018, reached USD 341.48 million in 2024, and is projected to hit USD 624.36 million by 2032, growing at a CAGR of 7.35% during the forecast period.

- Market growth is primarily driven by increasing demand from construction, oil & gas drilling, and foundry applications, supported by rapid industrialization and urban infrastructure development in emerging economies.

- Rising environmental awareness and the shift toward natural, eco-friendly materials are boosting bentonite use in water treatment, cosmetics, and agriculture, creating new opportunities for diversification.

- The market is moderately consolidated, with leading players such as Ashapura Group, Kunimine Industries, Imerys, and Clariant AG competing through product innovation and expansion strategies.

- Regionally, China holds the largest market share at 38.6%, followed by India at 29.7%; by application, foundry sands remain the dominant segment due to rising demand for precision casting across the automotive and heavy machinery sectors.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Market Segmentation Analysis:

By Product Type

In the Asia Pacific bentonite market, sodium bentonite holds the largest market share due to its superior swelling properties, high absorbency, and strong binding capabilities. This product type is widely used in drilling mud, iron ore pelletizing, and sealing applications, making it highly demanded in industrial and construction sectors across the region. Calcium bentonite, though less absorbent, is favored in applications such as cat litter and personal care due to its natural absorbency and mildness. The “others” category includes modified or activated bentonites, catering to niche uses such as water treatment and pharmaceuticals.

- For instance, Ashapura Group operates one of Asia’s largest sodium bentonite processing facilities in Gujarat, with an annual production capacity exceeding 700,000 metric tons, supplying to over 70 countries worldwide.

By Application

Foundry sands represent the dominant application segment in the Asia Pacific bentonite market, accounting for a significant market share. The rapid growth of the automotive and heavy machinery industries in countries like China and India drives demand for high-quality foundry molds, where bentonite is used as a binder. Drilling mud is another key segment, propelled by ongoing oil and gas exploration activities. Applications like cat litter, civil engineering, and refining continue to grow steadily due to rising urbanization, construction projects, and industrial processing needs. The “others” segment includes agricultural and environmental uses.

- For instance, Imerys supplies bentonite formulations used in more than 20 million tons of casting sand annually through its high-performance foundry product line across Asia.

Market Overview

Expanding Construction and Infrastructure Activities

The rapid urbanization and infrastructure development across Asia Pacific countries, particularly China, India, and Southeast Asia, are significantly boosting demand for bentonite. Its application in civil engineering for waterproofing, tunneling, and foundation works makes it a vital material for large-scale construction projects. Government initiatives promoting smart cities, transport networks, and housing schemes are further fueling the use of bentonite-based construction solutions, contributing to market expansion.

- For instance, Clariant AG developed its Bentosund product line for tunneling and civil engineering, which has been deployed in over 35 major infrastructure projects, including a 22-kilometer metro tunnel project in Southeast Asia.

Rising Oil & Gas Exploration Activities

Bentonite plays a critical role as a drilling fluid additive in oil and gas exploration. The Asia Pacific region, with increasing energy needs and exploration investments in offshore and onshore drilling, especially in India, China, and Australia, is witnessing a surge in bentonite consumption. Its viscosity, suspension, and filtration control properties make it indispensable in drilling mud formulations, positioning it as a key material for oilfield services and boosting market growth.

- For instance, Kunimine Industries manufactures bentonite for drilling fluids with a production capacity of approximately 180,000 tons annually, supplying major petroleum projects across Japan and the broader Asia Pacific basin.

Growing Demand in Foundry and Metallurgy Sectors

The foundry sector is a significant end-user of bentonite in the region, utilizing it as a binder in molding sands. With the growth of the automotive and heavy equipment industries, demand for high-quality cast components is on the rise. Bentonite’s thermal stability and bonding properties make it ideal for casting applications. This, combined with industrial expansion in emerging economies, is driving consistent demand from metallurgy and foundry operations.

Key Trends & Opportunities

Increasing Adoption of Natural and Eco-Friendly Products

Environmental sustainability trends are pushing industries to adopt natural materials like bentonite in wastewater treatment, refining, and agricultural applications. Its non-toxic, biodegradable nature makes it a favorable choice for green construction materials and organic farming. This growing inclination towards environmentally friendly solutions presents substantial growth opportunities, especially as regulatory bodies across the region tighten environmental standards.

- For instance, Cimbar Performance Minerals introduced a low-carbon bentonite product line certified for use in LEED-compliant green buildings, and it has been used in over 12 million square meters of eco-certified construction area globally.

Rising Use in Cosmetics and Personal Care

Bentonite is increasingly utilized in personal care products due to its absorbent and detoxifying properties. The growing beauty and wellness industry in countries such as South Korea, Japan, and India is expanding the demand for bentonite in face masks, creams, and cleansers. As consumers shift toward products with natural ingredients, bentonite’s profile as a safe, effective compound creates new opportunities for manufacturers and suppliers in the personal care segment.

- For instance, Wyo-Ben supplies pharmaceutical-grade bentonite that is used in over 150 personal care and dermatology product formulations across Asia, with production batches consistently tested for 99.9% purity compliance under USP standards.

Key Challenges

Price Volatility and Supply Chain Disruptions

Bentonite prices in the Asia Pacific region are subject to fluctuations due to mining regulations, raw material availability, and transportation costs. Export restrictions, geopolitical tensions, and disruptions in logistics particularly from major producers like India and China—can impact consistent supply. These factors create price instability, which may hinder long-term supply contracts and limit market growth for smaller players.

Environmental Concerns Related to Mining Activities

Although bentonite is naturally occurring and eco-friendly, its extraction process involves open-pit mining, which raises environmental concerns. Land degradation, habitat disruption, and dust pollution can attract stricter regulations from environmental authorities. These compliance requirements often increase operational costs for mining companies, acting as a constraint on production scalability and regional expansion.

Substitution from Alternative Materials in Certain Applications

In specific industrial applications, alternative materials such as synthetic binders or polymers may offer similar or superior performance compared to bentonite. Technological advancements and cost-effectiveness of substitutes in construction, drilling fluids, or personal care could shift demand away from bentonite. This trend poses a challenge, especially for traditional bentonite suppliers that must innovate or diversify to remain competitive.

Regional Analysis

China

China accounts for the largest share of the Asia Pacific bentonite market, holding approximately 38.6% of the regional market in 2024. This dominance stems from its extensive use in construction, tunneling, and iron ore pelletizing operations. The country’s vast infrastructure development, robust industrial activity, and demand from foundry and drilling sectors sustain high bentonite consumption. Additionally, government-driven urban expansion and environmental remediation efforts continue to bolster its leading position in the market.

India

India holds the second-largest share in the regional market, contributing around 29.7% in 2024. Its strong presence is supported by abundant bentonite reserves, active mining operations, and high demand across foundry, oil & gas, and civil engineering sectors. Domestic production capacity meets both internal consumption and export requirements. Government investments in infrastructure and industrial development projects further reinforce India’s critical role in shaping the regional bentonite landscape.

Bangladesh

Bangladesh represents approximately 7.5% of the Asia Pacific bentonite market in 2024. The market is growing steadily due to rising demand from construction, agriculture, and wastewater treatment sectors. Rapid urbanization, infrastructure upgrades, and adoption of bentonite in green building materials are key contributors to growth. Although relatively smaller, Bangladesh’s increasing focus on industrial development presents long-term potential for expansion.

Vietnam

Vietnam holds a 6.2% share of the regional bentonite market in 2024. The country is experiencing increasing demand from infrastructure development, manufacturing, and cosmetic industries. Applications in civil engineering, oil & gas drilling, and personal care products are expanding rapidly. Vietnam’s push for industrial modernization and improved urban planning contributes to a favorable environment for bentonite market growth.

Rest of Asia

The Rest of Asia segment, comprising Indonesia, Malaysia, Thailand, the Philippines, and others, collectively accounts for 18.0% of the regional bentonite market in 2024. Market demand is driven by diverse applications in oilfield services, agriculture, personal care, and construction. These countries are witnessing steady infrastructure investments, urban growth, and environmental initiatives, all of which contribute to consistent bentonite usage across multiple industries.

Market Segmentations:

By Product Type

- Sodium Bentonite

- Calcium Bentonite

- Others

By Application

- Foundry Sands

- Iron Ore Pelletizing

- Drilling Mud

- Cat Litter

- Civil Engineering

- Refining

- Others

By Geography

- China

- India

- Bangladesh

- Vietnam

- Rest of Asia

Competitive Landscape

The Asia Pacific bentonite market features a moderately consolidated competitive landscape, with both regional and global players actively competing through capacity expansion, product differentiation, and strategic partnerships. Major companies such as Ashapura Group, Kunimine Industries, and Imerys lead the market by leveraging their extensive mining operations, vertically integrated supply chains, and strong distribution networks. Local producers in India and China benefit from abundant reserves and cost-effective production, offering competitive pricing in both domestic and export markets. Multinational firms like Clariant AG and Bentonite Performance Minerals focus on specialized applications, including personal care, pharmaceuticals, and environmental solutions, to differentiate their offerings. Continuous investment in R&D, sustainable mining practices, and customization of bentonite grades for diverse industrial uses are key competitive strategies. Moreover, increasing demand from construction, oil & gas, and foundry sectors is prompting companies to strengthen their presence across high-growth markets in Southeast Asia and South Asia.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Wyo-Ben

- Kunimine Industries

- Black Hills Bentonite

- Bentonite Performance Minerals

- Cimbar Performance Minerals

- Ashapura Group

- Imerys

- Clariant AG

Recent Developments

- In January 2024, GHCL Limited signed an MoU worth USD ~413 million for investments in Gujarat, India. A total investment of around USD 113 million out of the USD 413 million has been allocated for mining bentonite and sands in Saurashtra region of Gujarat. Bentonite and sand are part of overburden found during lignite mining. Bentonite will be marketed to various industries, primarily for use as a raw material in fertilizers, foundries, cosmetics, and pharmaceuticals, among others.

- In January 2024, Laviosa Chimica Mineraria SpA, a leading firm in mineral-based products, announced the appointment of NAGASE Specialty Materials NA LLC (NSM) as an exclusive distributor of bentonite rheology additives in the U.S. The collaboration aims to diversify Laviosa’s mineral technology portfolio and reach newer demographics.

- In July 2023, Clariant, an eco-friendly specialty chemical company, announced the addition of plastic-free Desi Pak ECO moisture-adsorbing packets to its range of highly adsorbent, natural clay solutions that help manufacturers and suppliers protect sealed packaged goods from water damage. The product utilizes pure bentonite clay and offers highly efficient moisture adoption.

- In April 2023, Phoslock Environmental Technologies, a leading global environmental technology corporation specializing in application of bentonite to mitigate excessive nutrient levels in water bodies resulting from agricultural runoff, industrial discharges, and sewage treatment processes, is seeking to extend its operational footprint in Casper.

- In November 2022, Bentoproduct, a Bosnian enterprise specializing in manufacturing of bentonite-based products, initiated a takeover proposal for Nemetali, a domestic mining company. Further, Securities Commission of Bosnia and Herzegovina’s Serb Republic has granted approval for this bid.

Market Concentration & Characteristics

The Asia Pacific Bentonite Market exhibits moderate market concentration, with a mix of global corporations and regional producers shaping its competitive structure. A few key players, including Ashapura Group, Kunimine Industries, Imerys, and Clariant AG, command significant market share due to their integrated operations, diverse product lines, and established customer bases. It remains supply-sensitive, with large bentonite reserves concentrated in India and China, enabling cost-efficient production and export capabilities. The market is characterized by price competitiveness, regional sourcing advantages, and varying product grades tailored for specific industrial applications. It supports a broad range of end-use sectors, including construction, oil and gas, foundry, and personal care. Local players in emerging economies compete by offering low-cost, application-specific products, while multinational firms focus on innovation, sustainability, and expanding their application footprint. Import and export dynamics, infrastructure investment, and regulatory frameworks significantly influence regional consumption patterns and pricing. The structure continues to evolve as demand shifts toward value-added and environment-friendly bentonite formulations.

Report Coverage

The research report offers an in-depth analysis based on Product Type, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The Asia Pacific bentonite market is expected to witness steady growth driven by rising construction and infrastructure development across emerging economies.

- Increasing oil and gas exploration activities in India, China, and Southeast Asia will continue to boost demand for bentonite-based drilling fluids.

- Foundry applications will remain a significant driver, supported by growth in automotive and heavy machinery manufacturing.

- Rising environmental awareness will promote the use of bentonite in water treatment and soil stabilization projects.

- The cosmetics and personal care sector will offer new opportunities with growing consumer preference for natural ingredients.

- Governments’ focus on sustainable mining and regulatory compliance will shape future production and export strategies.

- Advancements in bentonite modification and processing will enable its use in high-performance industrial applications.

- Market players will increasingly invest in capacity expansion and regional distribution to meet growing local demand.

- Competition from alternative materials in select applications may encourage innovation and product differentiation.

- Digitalization and automation in mining operations are expected to improve supply chain efficiency and cost control.