At Home Drug Of Abuse Testing Market Overview:

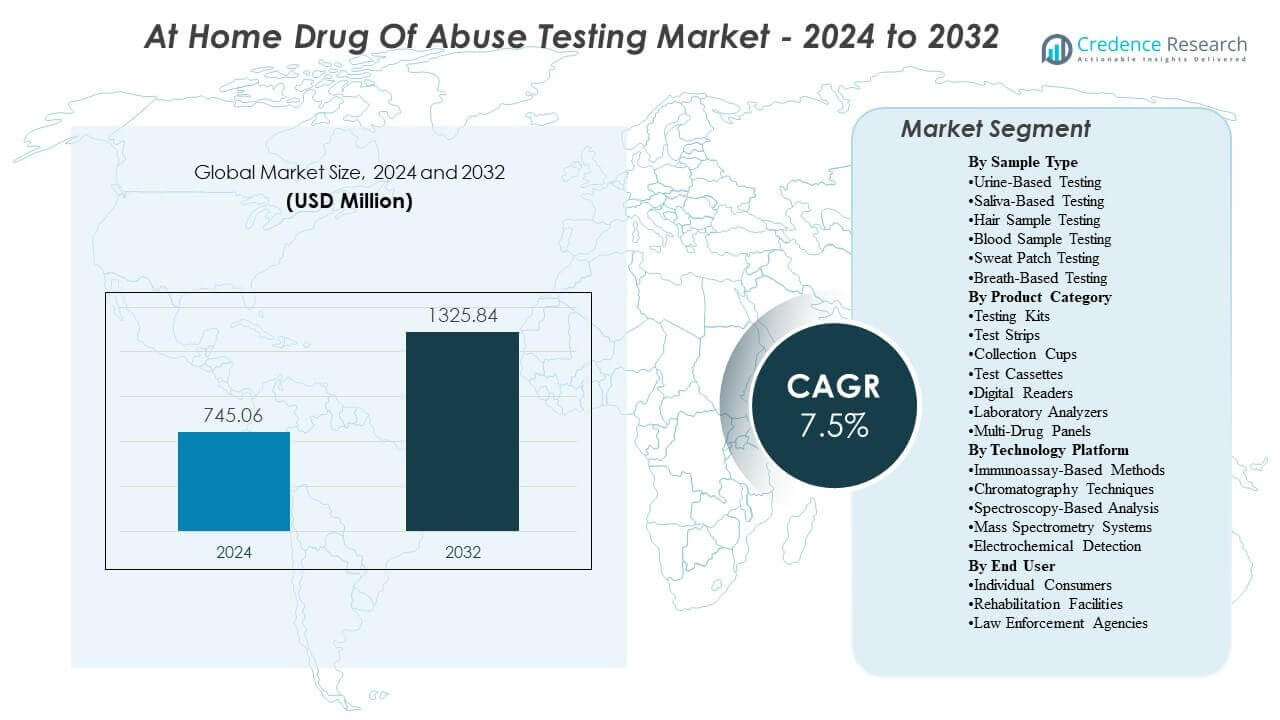

The At Home Drug Of Abuse Testing Market is projected to grow from USD 745.06 million in 2024 to an estimated USD 1325.84 million by 2032, with a compound annual growth rate (CAGR) of 7.5% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| At Home Drug Of Abuse Testing Market Size 2024 |

USD 745.06 Million |

| At Home Drug Of Abuse Testing Market, CAGR |

7.5% |

| At Home Drug Of Abuse Testing Market Size 2032 |

USD 1325.84 Million |

Growth is primarily driven by rising demand for private, convenient screening options across households, employers, and care settings. Increasing awareness of substance misuse risks, coupled with a stronger focus on early detection, supports adoption. Retail and e-commerce availability has improved access and product choice. Advances in rapid immunoassay strips, multi-panel kits, and clearer result interpretation also encourage repeat purchases and broader use.

North America leads due to higher testing awareness, established retail distribution, and wider use in workplace and family settings. Europe follows, supported by public health focus and regulated diagnostics markets that build confidence in product quality.

At Home Drug of Abuse Testing refers to self-administered test kits that detect the presence of illicit or prescription drugs in biological samples such as urine, saliva, hair, or sweat. These kits provide quick, preliminary results for personal monitoring, parental oversight, or recovery support, though confirmatory laboratory testing is often required for clinical or legal decisions.

At Home Drug Of Abuse Testing Market Insights:

- Demand is primarily driven by the need for privacy and convenience, with households, employers, and recovery monitoring use cases supporting repeat purchases and wider routine screening.

- Key restraints center on confidence and usability issues, including false positives/negatives, user error, and confusion between screening results and confirmatory testing requirements.

- North America leads due to established OTC and e-commerce distribution and higher awareness, while Europe remains strong with regulated diagnostics channels and pharmacy reach.

- Asia-Pacific is the main emerging growth region, supported by rapid e-commerce expansion and improving consumer access to home diagnostics, while Latin America and the Middle East & Africa grow more gradually due to affordability and distribution constraints.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Growing Preference for Privacy, Convenience, and Discreet Self-Screening at Home

Consumers increasingly choose at-home drug of abuse tests because they reduce stigma and enable private decision-making. Convenience matters for families managing risk, caregivers monitoring relapse, and individuals seeking reassurance without scheduling clinic visits. Faster access to results can support earlier intervention, especially when paired with counseling or treatment pathways. Demand also rises when test formats are simple, minimally invasive, and easy to interpret.

- For instances, with UNODC reporting that 316 million people used a drug in 2023 and NIDA highlighting that stigma and discrimination can affect care for people with substance use disorders, consumers increasingly choose at-home drugs of abuse tests for private, convenient self-screening that can be read at home within minutes rather than requiring a clinic visit.

Workplace and Family Safety Needs Driving Routine, Preventive Testing Behaviors

Employers, parents, and caregivers use at-home tests to support safety-sensitive routines and to confirm suspected misuse without immediate clinical escalation. In households, testing is often tied to prevention and monitoring, particularly for adolescents and individuals in recovery. These use cases expand volumes beyond one-time screening toward periodic, repeat purchasing. Broader social focus on harm reduction and early identification reinforces this preventive behavior.

- For instance, Quest Diagnostics analysis of more than 8 million workplace drug tests found combined US workforce urine drug positivity at 4.4% in 2024 and for-cause positivity at 33.1% in the general workforce, reinforcing employer, parent, and caregiver use of at-home tests for routine safety and recovery monitoring that can translate into periodic repeat purchasing.

Wider Retail and E-Commerce Availability Improving Access and Product Choice

Distribution expansion through pharmacies, supermarkets, and online marketplaces increases visibility and purchase convenience. E-commerce enables broader geographic reach, easier product comparison, and recurring purchases through reorders or subscriptions. More brands and private-label offerings have widened price bands, supporting adoption across different income groups. Improved packaging, instructions, and customer support also reduce perceived barriers for first-time users.

Product Performance Improvements in Multi-Panel Formats and Faster Turnaround Times

Manufacturers continue improving rapid screening formats with more drug panels, clearer result windows, and shorter processing times. Multi-panel kits increase value perception by enabling screening across multiple substances in one purchase. Better sensitivity and reduced user error, supported by improved sample collection and step-by-step guidance, can increase trust and repeat usage. These product upgrades also help shift demand from single-use testing toward broader household preparedness.

Market Trends and Opportunities:

Shift Toward Multi-Panel and Customizable Panels Supporting Tiered Product Lines

Buyers are shifting toward multi-panel kits that screen more substances in one test, and some demand is emerging for customizable panels by use case. This supports tiered portfolios, from value options to premium multi-panel formats. Clear labeling and simpler interpretation help brands differentiate as panel breadth becomes a key purchase driver. Standardized result presentation can also strengthen repeat-use confidence.

Digital Guidance and Result-Capture Features Enabling Premiumization and Care Pathways

Digital support features such as guided instructions, timers, and result capture are increasingly used to reduce user error and improve confidence. This creates room for premium offerings that include optional readers or app-based guidance. Partnerships with pharmacies, telehealth, or counseling networks can connect screening to confirmatory pathways and care. These models can increase adherence and recurring purchases.

User-Friendly Collection and Packaging Creating Adoption Headroom for First-Time Users

User-friendly collection and packaging are gaining attention, including tamper-evident designs and clearer result windows to reduce misreading. This opens opportunities to broaden adoption among first-time users through better instructions and simplified sample handling. Innovation in alternative sample types and improved sensitivity can expand use cases, if formats remain practical at home. Lower friction across steps supports higher repeat purchase rates.

Online Channel Growth and Replenishment Models Expanding Reach in Emerging Markets

Online channels are increasingly shaping brand selection through reviews and perceived reliability, while bulk packs and replenishment models fit repeat-use segments. Direct-to-consumer strategies can improve education and enable subscription-style reordering. Emerging markets become more accessible as e-commerce and consumer health spending rise, especially with localized panel configurations. Employer and community programs can also drive structured demand when supported by clear protocols.

At Home Drug Of Abuse Testing Market Challenges Analysis

At-home drug tests face trust and accuracy concerns, particularly around false positives, false negatives, and differences in detection windows across substances. Results can be affected by user error, improper sample handling, or misunderstanding of instructions. Many kits are designed for screening rather than confirmation, which can create confusion about how to act on results. In sensitive situations, uncertainty can lead to either delayed intervention or unnecessary escalation.

- For instance, FDA’s 510(k) decision summary for ACON Laboratories’ On Call Multi Drug Home Test Cup describes a visually read lateral flow immunoassay with fixed cutoffs such as THC 50 ng/mL and PCP 25 ng/mL, with results intended to be read at 5 minutes and not after 10 minutes.

Regulatory variability and differing quality standards across markets can complicate product positioning and consumer confidence. Price competition from low-cost offerings may pressure margins and encourage buyers to prioritize cost over reliability. Stigma and privacy concerns can still limit adoption in some cultures or household contexts, even when products are available. Customer support and clear escalation guidance remain challenging, especially when users seek next steps after an unexpected result.

- For instance, FDA clearance documentation for ALFA Scientific Designs’ Instant View Multi-Drug Urine Test Cup and Panel for OTC use states it can screen up to 13 drugs at defined cutoffs such as buprenorphine 10 ng/mL and THC 50 ng/mL, but results are preliminary and intended to be confirmed by chromatography/mass spectrometry, with a 400-participant lay-user study supporting consumer usability.

At Home Drug Of Abuse Testing Market Segmentation Analysis:

The At Home Drug Of Abuse Testing Market can be segmented by sample type, product, technology, and end-user, each shaping adoption and pricing.

By sample type, urine testing remains the most widely used due to familiarity, broad drug-panel availability, and cost efficiency, while saliva testing is gaining share for easier collection and faster screening. Hair testing supports longer detection windows but is less common at home due to perceived complexity and higher cost. Blood, sweat, and breath testing are more niche, typically limited by collection practicality or device dependence in consumer settings.

By product, demand is concentrated in test kits, strips, cups, and cassettes, which address self-screening and repeat monitoring needs; multi-panels are favored where broader coverage is required. Readers and analyzers represent higher-value segments, used where users want clearer interpretation and recordability, but adoption depends on affordability and ease of use.

By technology, immunoassay dominates for rapid screening, while chromatographic formats help improve separation and readability. Spectroscopy, mass spectrometry, and electrochemical approaches are more specialized and typically constrained by cost and device requirements.

By end-user, individuals form the largest base, with rehabilitation centers using tests for ongoing monitoring. Law enforcement demand is selective and often influenced by procedural requirements and confirmatory workflows.

Segmentation:

By Sample Type

- Urine Testing

- Saliva Testing

- Hair Testing

- Blood Testing

- Sweat Testing

- Breath Testing

By Product

- Test Kits

- Strips

- Cups

- Cassettes

- Readers

- Analyzers

- Panels

By Technology

- Immunoassay

- Chromatographic

- Spectroscopy

- Mass Spectrometry

- Electrochemical

By End-User

- Individuals

- Rehabilitation Centers

- Law Enforcement

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America leads the At Home Drug Of Abuse Testing Market, supported by high consumer awareness, dense OTC pharmacy networks, and strong e-commerce penetration. Routine use for household screening, workplace risk management, and recovery monitoring sustains repeat purchasing. In 2024, North America is estimated to hold 42% share, reflecting mature self-testing habits and wide retail availability.

Europe is the second-largest region at an estimated 28% share. Regulated diagnostics frameworks and pharmacy-led distribution strengthen buyer confidence, but adoption varies by country because self-testing norms, enforcement priorities, and purchasing channels differ. Demand is strongest in Western Europe, where product access and willingness to pay are higher and discreet testing is increasingly valued.

Asia-Pacific is the main growth engine with an estimated 20% share in 2024, driven by expanding online marketplaces, rising middle-class health spending, and broader access to multi-panel kits. Many analyses position it as the fastest-growing region as awareness and availability improve. Latin America remains smaller at about 6% share, supported by e-commerce growth and gradual normalization of preventive screening. The Middle East & Africa is the smallest region at roughly 4%, constrained by affordability, uneven distribution, and lower consumer awareness in several markets. Local pricing strategies will also shape uptake.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Abbott Laboratories

- Quest Diagnostics Incorporated

- LabCorp

- Drägerwerk AG & Co. KGaA

- Alere Inc. (part of Abbott)

- OraSure Technologies, Inc.

- Thermo Fisher Scientific Inc.

- Premier Biotech, Inc.

- Confirm BioSciences

- Assure Tech (Hangzhou) Co., Ltd.

- Atlas Medical GmbH

- Psychemedics Corporation

Competitive Analysis:

The At Home Drug of Abuse Testing Market is moderately fragmented, with competition shaped by product reliability, panel breadth, ease of use, and distribution reach. Established diagnostics and rapid-test manufacturers typically compete on validated performance, clear instructions, and consistent supply, while smaller brands and private-label sellers often compete on price and online visibility. Multi-panel urine and saliva formats are common battlegrounds because they drive higher basket value and repeat purchases for monitoring use cases.

Differentiation is increasingly tied to user experience features such as clearer result windows, tamper-evident designs, and optional readers that reduce interpretation errors. Channel strategy is central: brands with strong pharmacy placement and leading e-commerce rankings tend to capture higher volume. Competitive pressure remains high in entry-level strips and cups due to commoditization, while premium segments digital support, enhanced readability, and broader panels offer more room for margin and brand loyalty.

Recent Developments:

- In August 2025, Quest Diagnostics completed the acquisition of select clinical testing assets from Fresenius Medical Care’s Spectra Laboratories enhancing its capabilities in related diagnostic services, though not exclusively at-home drug testing.

- In March 2025, Psychemedics Corporation announced the launch of Quartile Reporting, a reporting enhancement intended to add interpretive context to drug test results for organizational decision-making, reinforcing differentiation in hair drug testing services adjacent to broader screening markets.

- In November 2024, Easy Healthcare Corporation expanded its Easy@Home product line by launching two new drug testing kits a 5-Panel Instant Urine Drug Test and a Nicotine Urine Test available at select Walmart stores and Walmart.com.

Report Coverage:

The research report offers an in-depth analysis based on sample type, product, technology, and end-user. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.