Ayurveda Market Overview:

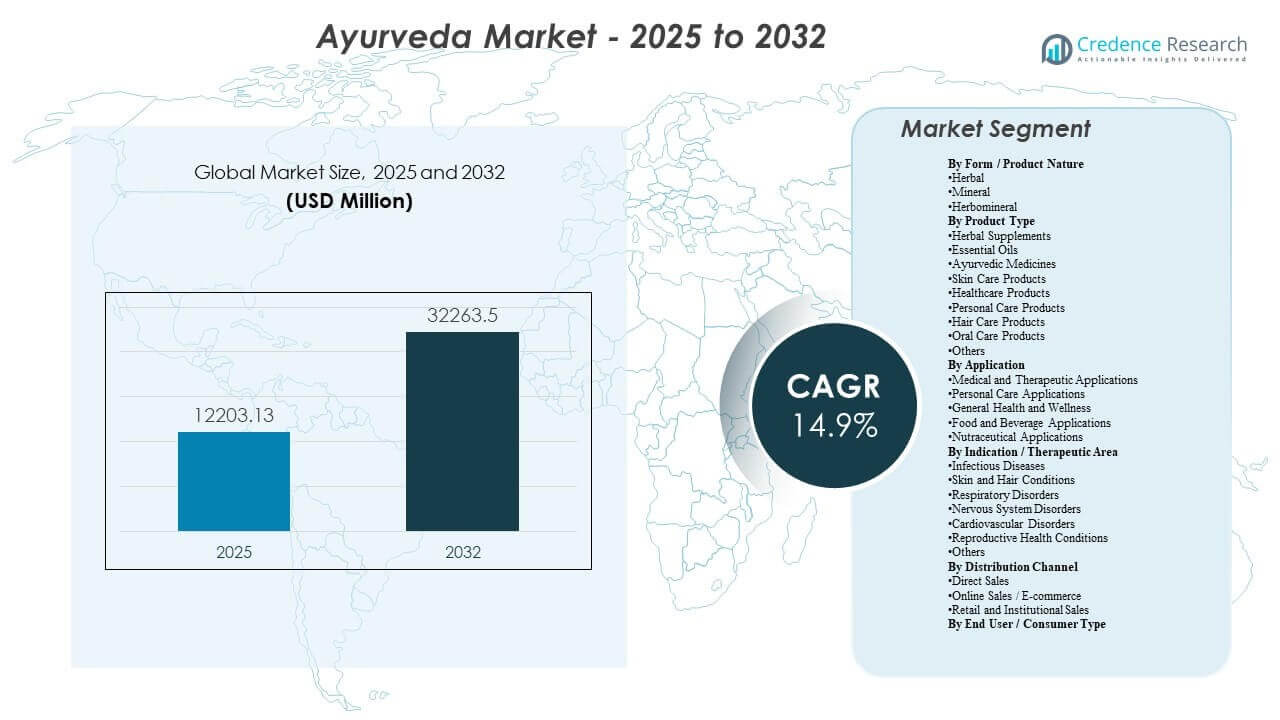

The global Ayurveda Market size was estimated at USD 12,203.13 million in 2025 and is expected to reach USD 32,263.5 million by 2032, growing at a CAGR of 14.9% from 2025 to 2032. Growth is primarily supported by rising consumer preference for natural, plant-based health solutions and the shift toward preventive healthcare routines that sustain repeat purchases across supplements, personal care, and therapy-linked products. Demand is also expanding through broader retail availability and stronger digital discovery, which is accelerating penetration in non-native markets and new consumer cohorts.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Ayurveda Market Size 2025 |

USD 12,203.13 million |

| Ayurveda Market, CAGR |

14.9% |

| Ayurveda Market Size 2032 |

USD 32,263.5 million |

Key Market Trends & Insights

- Asia Pacific accounted for 77.80% share in 2025, reflecting the concentration of demand, manufacturing depth, and cultural familiarity with traditional care across major countries in the region.

- Herbal products led by form with a 68.40% share in 2025, supported by higher consumer comfort with plant-based formats and wide SKU availability across OTC-like use cases.

- Medical and therapeutic use represented 59.80% share in 2025, indicating continued relevance of Ayurveda-led clinical pathways, supervised therapies, and practitioner-guided regimens.

- Retail and institutional sales captured 64.10% share in 2025, emphasizing the role of pharmacies, modern trade, and wellness institutions in building trust and conversion.

- Skin and hair disorders accounted for 24.90% share in 2025, underlining the scale of daily-use personal care adjacencies that pull Ayurveda into frequent consumption cycles.

Segment Analysis

Demand formation in the Ayurveda Market is shaped by a mix of therapeutic and lifestyle-led consumption, with strong overlap between classical remedies and modern wellness formats. Consumer adoption is reinforced by routine-based usage in immunity, digestion, stress support, and dermatology-linked needs, which improves repeat purchase behavior and enlarges the addressable market beyond episodic treatment. Increasing availability of standardized products, greater emphasis on quality assurance, and wider retail penetration are supporting trial in new geographies. Digital channels are also lowering discovery barriers, enabling niche brands and specialized formulations to reach consumers directly.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Product innovation continues to move toward convenient formats such as capsules, tablets, powders, oils, and topical applications that align with modern consumption habits. Brand-led credibility, ingredient transparency, and safety messaging are influencing purchase decisions, especially in international markets and premium segments. Institutions such as clinics, hospitals, and wellness centers contribute to premiumization through bundled services and guided regimens, which also improve consumer confidence in efficacy. Over the forecast period, the market is expected to remain anchored by high-frequency categories such as personal care and supplements, alongside steady therapeutic demand.

By Form / Product Nature Insights

Herbal accounted for the largest share of 68.40% in 2025. Herbal dominance is supported by broad consumer acceptance, strong alignment with clean-label expectations, and easier integration into daily routines through teas, capsules, and topical applications. Wider availability across mass retail and online channels increases accessibility and supports repeat consumption. Strong branding and ingredient familiarity further reinforce herbal preference compared to mineral and herbomineral formats.

By Product Type Insights

Ayurveda Market demand across product types is supported by the expansion of daily-use categories that increase purchase frequency and reduce reliance on purely therapeutic consumption. Herbal supplements and Ayurvedic medicines sustain the core health-driven demand, while personal care, hair care, skin care, and oral care categories pull Ayurveda into routine household consumption. Essential oils benefit from aromatherapy, stress-relief positioning, and premium wellness gifting use cases. Category performance is closely tied to brand trust, formulation standardization, and claims clarity, which influence conversion in both pharmacies and modern trade.

By Application Insights

Medical and Therapeutic Use accounted for the largest share of 59.80% in 2025. Leadership is supported by practitioner-guided regimens, higher consumer willingness to adopt complementary therapies for chronic and lifestyle-related conditions, and growing integration within broader wellness and preventive care frameworks. Institutional influence from clinics, hospitals, and wellness centers improves credibility and encourages structured product adherence. Continued investment in standardized formulations and treatment protocols is also helping sustain therapeutic demand.

By Indication / Therapeutic Area Insights

Skin and Hair Disorders accounted for the largest share of 24.90% in 2025. This leadership is reinforced by high-frequency usage patterns in skincare and haircare, strong consumer preference for botanical ingredients, and the growth of “clean beauty” purchasing behavior. Topicals and personal care products often serve as entry points to Ayurveda for new consumers, supporting broader category trial. Social and digital commerce visibility further accelerates adoption, particularly for problem-solution products such as anti-dandruff, hair fall, acne, and pigmentation support.

By Distribution Channel Insights

Retail and Institutional Sales accounted for the largest share of 64.10% in 2025. This channel leads because pharmacies, specialty stores, supermarkets, and wellness institutions provide trust, product guidance, and easier access to verified brands. Institutional settings also support premium therapies and curated product bundles, increasing ticket size and adherence. Retail visibility improves brand recall and supports impulse-led purchasing in personal care categories. Online growth is increasingly complementary, but retail and institutional networks remain the largest demand funnel.

By End User / Consumer Type Insights

Home settings accounted for the largest share of 62.30% in 2025. Home-led consumption reflects the OTC-like nature of many Ayurveda products and the role of routine wellness in immunity, digestion, and personal care. Household use supports repeat purchases and subscription-like replenishment behavior, particularly for supplements and daily-use personal care items. Institutional demand from wellness centers, clinics, and hospitals continues to support premiumization, but the largest consumption base remains individual consumer usage in home environments.

Ayurveda Market Drivers

Rising preference for natural and preventive healthcare

Consumer preference is shifting toward plant-based and traditional health solutions that are perceived as supportive for long-term wellness. Ayurveda benefits from this shift because it spans both therapeutic and lifestyle categories such as supplements, stress support, digestion, skincare, and haircare. Preventive usage increases repeat purchasing frequency and supports portfolio expansion into functional and daily-use formats. This dynamic is reinforced by growing interest in holistic health routines and non-invasive wellness interventions. As awareness expands, entry-level personal care and supplement products often act as gateways into broader Ayurveda consumption.

- For instance, Dabur reported that its health supplements portfolio, led by Chyawanprash and honey, reached over 100 million annual consumer touchpoints in India, with internal data indicating that more than 60% of repeat purchases are linked to preventive, daily-use consumption occasions rather than episodic illness use.

Expansion of retail availability and modern trade penetration

Growth is supported by the widening presence of Ayurveda products in pharmacies, supermarkets, specialty wellness outlets, and institutional wellness ecosystems. Retail and institutional channels help address trust barriers, improve product education, and increase conversion through visibility and guidance. Broader shelf space allocation and improved merchandising enable Ayurveda brands to compete effectively with mainstream FMCG and OTC alternatives. Institutional networks such as wellness centers and clinics also enable bundled regimens that strengthen adherence. This channel breadth supports both mass-market and premium offerings across multiple product types.

Digital discovery and e-commerce-led assortment expansion

E-commerce and digital marketing are improving access to niche and premium Ayurveda products by extending assortment beyond what traditional retail typically carries. Online retail supports direct-to-consumer brand scaling, subscription replenishment, and cross-border availability that accelerates adoption in non-native markets. Digital discovery through content-led marketing increases first-time trials, especially for personal care and supplement products. Price transparency and reviews also increase consumer confidence for repeat purchases. Over time, omnichannel strategies are likely to become the standard route-to-market for leading brands.

Portfolio diversification into daily-use adjacencies

Ayurveda brands are increasingly extending product portfolios into high-frequency categories such as skin care, hair care, oral care, and personal hygiene. Daily-use categories expand addressable demand and reduce dependence on episodic therapeutic consumption. This diversification enables stronger brand stickiness and improves lifetime value through routine replenishment. It also supports premiumization via specialized formulations, targeted solutions, and ingredient-led differentiation. As innovation continues, product convenience and standardized quality will remain central to competitive positioning.

- For instance, Patanjali has leveraged its Ayurveda positioning to build a portfolio spanning hundreds of SKUs across categories like toothpaste, shampoos, soaps, and skincare, supported by widespread distribution through both general trade and major e-commerce platforms such as Amazon, Flipkart, BigBasket, Grofers, and Paytm Mall.

Ayurveda Market Challenges

Quality consistency, standardization, and ingredient traceability remain major challenges across Ayurveda Market value chains, particularly as products scale into international markets. Variability in raw material quality, differences in formulation practices, and inconsistent clinical validation can weaken consumer trust and restrict institutional adoption. Regulatory complexity around labeling, health claims, and safety testing can also extend time-to-market and increase compliance costs. These barriers are most pronounced for export-oriented growth and premium therapeutic positioning.

- For instance, DNA barcoding of commercial Ashwagandha samples showed that only 77% of products were authentic, while 23% contained adulterants or substitutions, with powdered products far more affected than roots, underscoring the scale of raw material variability and traceability gaps that global regulators closely scrutinize.

Market fragmentation and intense competition add pressure on pricing, shelf space, and digital visibility, especially across supplements and personal care categories. New entrants often compete on claims and marketing rather than differentiated evidence or supply chain strength, which can create trust issues for consumers. Counterfeit risks and inconsistent product authentication can further impact brand credibility in high-demand categories. To sustain growth, companies typically need stronger quality assurance systems, credible messaging, and differentiated product innovation anchored in safety and efficacy.

Ayurveda Market Trends and Opportunities

Premiumization is emerging as an important trend as consumers increasingly seek specialized formulations, targeted outcomes, and higher-perceived quality in supplements and personal care categories. Premium products often command higher margins through ingredient transparency, clean-label positioning, and improved sensorial experiences in topicals and oils. This trend is supported by the expansion of wellness centers and spa-led ecosystems that encourage curated regimens and bundled offerings. Premium categories are also more likely to benefit from gifting use cases and subscription purchasing.

- For instance, Himalaya Wellness reports that its herbal healthcare and personal care portfolio now spans over 500 SKUs across tablets, capsules, topicals, and oils, enabling more targeted benefit platforms such as stress support, liver health, and dosha-specific skincare within premium sub-lines.

Integration of Ayurveda into broader wellness ecosystems presents opportunities across nutraceuticals, functional foods, and lifestyle-led personal care lines. Product formats that combine convenience with trusted formulations are expected to perform strongly, particularly in urban markets and among younger consumers. Partnerships that strengthen distribution, expand portfolio adjacency, and improve digital conversion can accelerate growth for both established and emerging brands. Over the forecast period, international market expansion is likely to be shaped by quality assurance, certification, and culturally adapted positioning.

Regional Insights

North America

North America accounted for 9.60% share in 2025, supported by strong demand for dietary supplements, wellness retail expansion, and rising interest in integrative health routines. The region benefits from large consumer segments seeking botanical alternatives for stress, sleep, digestion, and immune support. E-commerce and specialty retail play central roles in discovery and conversion, especially for premium and niche offerings. Brand credibility, third-party testing, and clear labeling are critical drivers of purchase decisions in this region.

Europe

Europe accounted for 7.30% share in 2025, with demand concentrated in herbal supplements, personal care, and aromatherapy-linked categories. Adoption is shaped by strong consumer interest in natural products alongside a generally stricter environment for health claims and labeling compliance. Specialty retail and pharmacy channels remain important for trust-led conversion, while online platforms expand access to niche formulations. Product positioning that emphasizes quality, transparency, and safety is particularly important for scaling across multiple European markets.

Asia Pacific

Asia Pacific accounted for 77.80% share in 2025, reflecting the region’s deep cultural adoption, large consumer base, and extensive manufacturing and distribution ecosystems. India remains the anchor market due to strong domestic consumption across therapeutic and daily-use categories, supported by widespread availability and institutional care pathways. Regional growth is reinforced by expanding modern retail, rising disposable income, and greater penetration of branded products. Cross-border e-commerce and wellness tourism further contribute to demand spillover across key Asia Pacific markets.

Latin America

Latin America accounted for 2.60% share in 2025, with adoption primarily driven by natural personal care, wellness oils, and supplement-led positioning. Awareness of Ayurveda is growing but remains less entrenched than local traditional herbal practices, which can slow conversion in therapeutic categories. Online channels expand access to specialized products, while premium personal care acts as an entry point for new consumers. Growth is expected to be linked to brand-led trust building, improved availability, and targeted positioning for beauty and wellness routines.

Middle East & Africa

Middle East & Africa accounted for 2.70% share in 2025, supported by urban wellness ecosystems, spa-led demand, and growing consumer interest in natural personal care. Wellness centers and resorts in the Gulf markets contribute to premiumization and service-led adoption, which also drives product sales. Retail availability is improving through modern trade and pharmacy expansion, while e-commerce increases access to imported and niche brands. Longer-term growth will depend on quality assurance, trust-led branding, and stronger institutional integration.

Competitive Landscape

Competition in the Ayurveda Market is shaped by portfolio breadth, brand trust, quality assurance practices, and channel strength across retail and digital platforms. Established companies use diversified product lines spanning healthcare and personal care to capture high-frequency demand and expand consumer lifetime value. Differentiation is increasingly driven by standardized formulations, ingredient sourcing transparency, and category-specific innovation in supplements and daily-use personal care. Partnerships, acquisitions, and distribution expansion remain common strategies to accelerate scale and strengthen category positioning.

Dabur Ltd. typically competes through a broad Ayurveda-aligned portfolio across healthcare and personal care categories, supported by strong distribution coverage and brand recognition. Portfolio adjacency in hair care, personal care, and wellness solutions enables wider shelf presence and high-frequency purchase behavior. The company’s strategy often emphasizes product accessibility across mass retail while also supporting premium offerings through targeted brand extensions. Channel execution and trust-led positioning remain central to sustaining share in crowded categories such as supplements, hair care, and skincare.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Dabur Ltd.

- Patanjali Ayurved Ltd.

- Himalaya Wellness Company

- Baidyanath Group

- Emami Ltd.

- Vicco Laboratories

- Kerala Ayurveda Ltd.

- Biotique

- Amrutanjan Health Care Ltd.

- Charak Pharma Pvt. Ltd.

- Organic India

- Hamdard Laboratories

- Maharishi Ayurveda

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments

- In July 2025, SuanNutra Group’s company Gonmisol signed an exclusive European distribution agreement with India‑based K. Patel Phyto Extractions for an Ayurvedic ingredient portfolio, aiming to develop EFSA‑aligned, traceable Ayurvedic ingredients tailored for European and UK supplement formulators and to translate traditional Ayurveda into modern wellness products for the region.

- In July 2025, Apollo AyurVAID, a precision Ayurveda hospital network based in India, launched India’s first “Tested Safe” Ayurveda product portfolio, introducing around 50 SKUs spanning classical formulations, OTC products, and medical foods, as part of a strategic foray beyond clinical care to build a full‑stack, evidence‑based Ayurveda enterprise with nationwide reach and a medium‑term revenue aspiration of about Rs. 500 crore from products.

- In February 2025, Sabinsa announced the acquisition of Nature’s Formulary, a long‑established US Ayurvedic supplements company, with both firms highlighting that the deal will combine Nature’s Formulary’s expertise in Ayurvedic formulations with Sabinsa’s R&D and global infrastructure to deliver high‑quality, transformative wellness solutions worldwide.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 12,203.13 million |

| Revenue forecast in 2032 |

USD 32,263.5 million |

| Growth rate (CAGR) |

14.9% |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Form / Product Nature Outlook: Herbal, Mineral, Herbomineral; By Product Type Outlook: Herbal Supplements, Essential Oils, Ayurvedic Medicines, Skin Care Products, Healthcare Products, Personal Care Products, Hair Care Products, Oral Care Products, Others; By Application Outlook: Medical and Therapeutic Use, Personal Care, General Healthcare and Wellness, Food and Beverages, Nutraceuticals; By Indication / Therapeutic Area Outlook: Infectious Diseases, Skin and Hair Disorders, Respiratory Disorders, Nervous System Disorders, Cardiovascular Disorders, Reproductive Health Disorders, Others; By Distribution Channel Outlook: Direct Sales, Online Retail / E-commerce, Retail and Institutional Sales; By End User / Consumer Type Outlook: Individual Consumers, Wellness Centers and Spas, Ayurvedic Clinics and Hospitals, Adults, Geriatric Population, Children, Pregnant Women |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Dabur Ltd., Patanjali Ayurved Ltd., Himalaya Wellness Company, Baidyanath Group, Emami Ltd., Vicco Laboratories, Kerala Ayurveda Ltd., Biotique, Amrutanjan Health Care Ltd., Charak Pharma Pvt. Ltd., Organic India, Hamdard Laboratories, Maharishi Ayurveda |

| No. of Pages |

340 |

Segmentation

BY FORM / PRODUCT NATURE

- Herbal

- Mineral

- Herbomineral

BY PRODUCT TYPE

- Herbal Supplements

- Essential Oils

- Ayurvedic Medicines

- Skin Care Products

- Healthcare Products

- Personal Care Products

- Hair Care Products

- Oral Care Products

- Others

BY APPLICATION

- Medical and Therapeutic Use

- Personal Care

- General Healthcare and Wellness

- Food and Beverages

- Nutraceuticals

BY INDICATION / THERAPEUTIC AREA

- Infectious Diseases

- Skin and Hair Disorders

- Respiratory Disorders

- Nervous System Disorders

- Cardiovascular Disorders

- Reproductive Health Disorders

- Others

BY DISTRIBUTION CHANNEL

- Direct Sales

- Online Retail / E-commerce

- Retail and Institutional Sales

BY END USER / CONSUMER TYPE

- Individual Consumers

- Wellness Centers and Spas

- Ayurvedic Clinics and Hospitals

- Adults

- Geriatric Population

- Children

- Pregnant Women

BY REGION

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa