Benign Prostatic Hyperplasia Treatment Devices Market Overview:

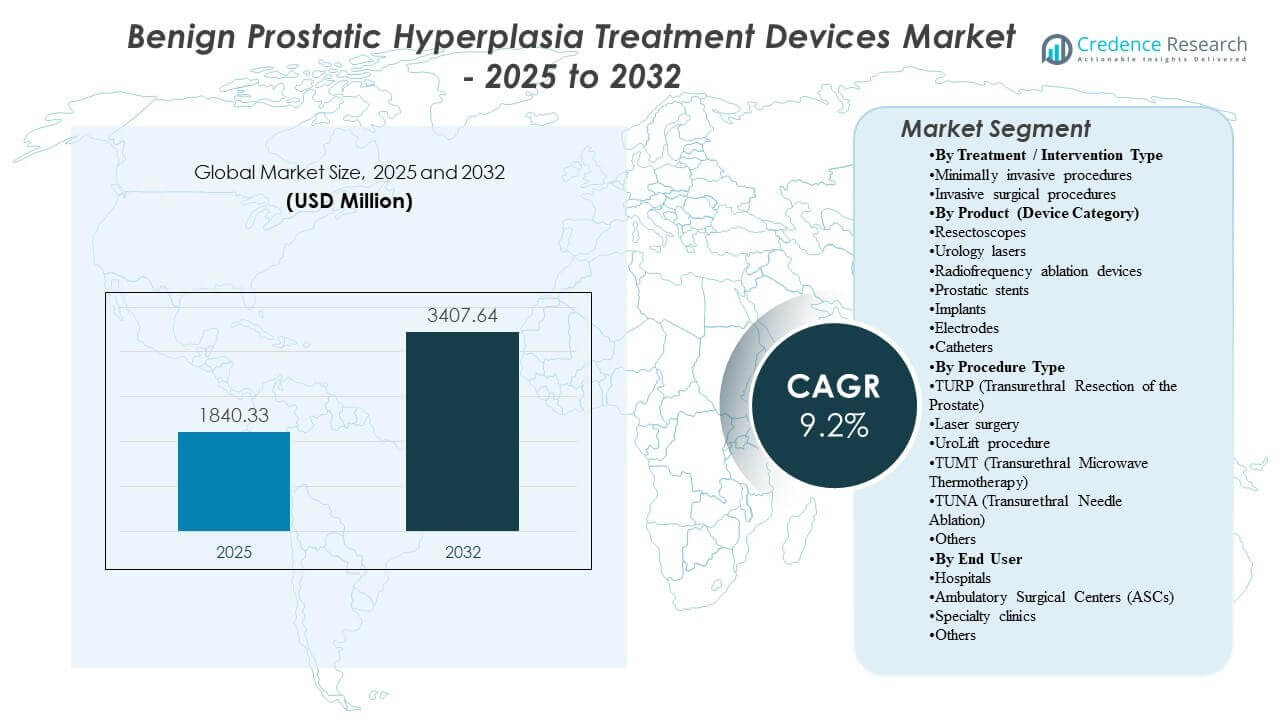

The global Benign Prostatic Hyperplasia Treatment Devices Market size was estimated at USD 1840.33 million in 2025 and is expected to reach USD 3407.64 million by 2032, growing at a CAGR of 9.2% from 2025 to 2032. Growth is primarily supported by rising procedure demand from an expanding aging male population, combined with increased clinical preference for device-enabled options that deliver faster symptom relief than long-term pharmacotherapy in appropriately selected patients. Expanding outpatient capability across urology clinics and ambulatory centers further supports broader adoption of minimally invasive device-based interventions.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Benign Prostatic Hyperplasia Treatment Devices Market Size 2025 |

USD 1840.33 million |

| Benign Prostatic Hyperplasia Treatment Devices Market, CAGR |

9.2% |

| Benign Prostatic Hyperplasia Treatment Devices Market Size 2032 |

USD 3407.64 million |

Key Market Trends & Insights

- The market expands from USD 1840.33 million in 2025 to USD 3407.64 million by 2032, reflecting sustained procedural and device utilization growth.

- The market is projected to grow at a CAGR of 9.2% during 2025–2032, indicating accelerating adoption of device-based BPH management pathways.

- North America accounts for 34.40% share in 2025, supported by higher procedural penetration and established urology infrastructure.

- TURP represents 26% share in 2025 among procedure types, maintaining a benchmark position for definitive tissue removal in moderate-to-severe cases.

- Resectoscopes capture 23% share in 2025 among device categories, reflecting continued reliance on endoscopic resection workflows in surgical management.

Segment Analysis

Device demand in benign prostatic hyperplasia care is shaped by the balance between symptom severity, prostate anatomy, patient preference, and the care setting where the procedure is performed. Minimally invasive approaches continue to gain traction due to shorter recovery, lower anesthesia requirements, and feasibility in outpatient or short-stay settings, which improves patient throughput and reduces facility burden. Procedure selection remains closely linked to durability expectations and the need to preserve sexual function, which influences adoption patterns across implant-based and thermal modalities.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Product utilization reflects the continued role of established endoscopic systems alongside newer platforms. Resectoscopes remain closely tied to TURP volumes and hospital-based surgical capability, supporting consistent baseline demand. Laser and thermal systems benefit from precision, hemostasis, and broader applicability across patient profiles, supporting incremental adoption in facilities investing in advanced urology suites.

End-user mix is influenced by where diagnosis, counselling, and procedure execution are concentrated. Hospitals continue to anchor complex workflows and high-acuity cases, whereas ambulatory surgical centers and specialty clinics grow in relevance as outpatient procedure protocols mature. Competitive strategies increasingly focus on evidence generation, workflow simplification, and training models that reduce adoption friction for new modalities.

By Treatment / Intervention Type Insights

Minimally invasive procedures represent the leading intervention approach in 2025 due to shorter recovery timelines, reduced hospitalization requirements, and growing patient preference for tissue-sparing options. Outpatient feasibility supports higher procedure throughput and improves access for suitable patients managed through urology clinics and ambulatory centers. Technology improvements in ablation, implants, and energy delivery expand candidacy and reduce barriers to adoption. Invasive surgical procedures continue to serve patients requiring definitive tissue removal or management of more complex clinical profiles.

By Product (Device Category) Insights

Resectoscopes accounted for the largest share of 23% in 2025. Demand is supported by broad availability of endoscopic surgical infrastructure and the continued procedural relevance of TURP in hospital urology departments. Standardization of resection workflows and clinician familiarity sustain consistent device utilization for surgical candidates. Adjacent growth is supported by increasing placement of urology lasers and thermal platforms that expand minimally invasive treatment capacity in outpatient-aligned settings.

By Procedure Type Insights

TURP (Transurethral Resection of the Prostate) accounted for the largest share of 26% in 2025. The procedure retains benchmark status due to established clinical history, predictable symptom relief, and widespread availability of endoscopic capability across hospitals. Durable outcomes expectations continue to support TURP selection for moderate-to-severe symptoms and cases requiring definitive tissue removal. Adoption of alternative procedures is influenced by recovery preferences, anesthesia requirements, and sexual function preservation considerations.

By End User Insights

Hospitals represent the leading end-user setting in 2025, supported by concentration of diagnostic pathways, surgical capability, and capital equipment required for TURP and advanced endoscopic workflows. The hospital setting also supports management of higher-acuity patients and cases requiring inpatient monitoring. Ambulatory surgical centers and specialty clinics gain relevance as minimally invasive procedures shift into outpatient settings. Procedure migration is reinforced by care pathway redesign and patient demand for convenience and faster discharge.

Market Drivers

Rising aging male population and increasing BPH symptom burden

Benign prostatic hyperplasia prevalence increases with age, expanding the pool of patients progressing from pharmacotherapy to procedural care. Higher diagnosis rates and improved symptom recognition support earlier referral into urology pathways. Demand rises as patients seek durable symptom relief and quality-of-life improvement. Growing awareness of minimally invasive options increases patient willingness to consider device-based intervention.

- For instance, Boston Scientific’s Rezūm water-vapor therapy showed a near 48% mean IPSS reduction at 5 years, along with 45% QoL improvement and 44% Qmax improvement, and reported a 4.4% surgical retreatment rate in the final 5-year sham-controlled trial outcomes.

Shift toward minimally invasive procedures and outpatient care pathways

Minimally invasive modalities support shorter recovery and reduced hospital stays, aligning with system-level efficiency goals. Outpatient capability improves patient throughput and lowers total care burden for suitable candidates. Technology refinements improve precision and reduce complication profiles, strengthening clinician confidence. Expansion of ambulatory and specialty urology centers increases availability of office-based and short-stay procedures.

Continuous innovation in device platforms and procedural techniques

Newer platforms improve workflow efficiency, energy delivery control, and procedure consistency, supporting adoption across a wider clinician base. Device design improvements focus on reducing retreatment risk, simplifying training, and improving patient experience. Broader patient applicability strengthens utilization economics for installed systems. Innovation supports differentiation across implants, ablation, and endoscopic resection ecosystems.

- For instance, PROCEPT BioRobotics’ Aquablation in the 5-year WATER randomized clinical trial showed a larger IPSS reduction versus TURP over follow-up (-14.1 vs. -10.8) and reported a lower rate of early (3-month) CD1P/CD2-or-higher events (risk difference -23.1%).

Expanding urology infrastructure and procedural capacity in emerging regions

Investment in hospital modernization and specialty care expands access to interventional BPH treatment in developing markets. Growth in trained urologist capacity increases procedural volumes and device utilization. Increasing penetration of endoscopic and laser equipment supports broader modality availability. The trend supports long-run demand growth as access gaps narrow in high-population regions.

Market Challenges

Device adoption faces competition from pharmacotherapy, which remains a common first-line approach for many patients and can delay conversion into procedural care. Coverage variability and procedure reimbursement differences across healthcare systems influence patient access and provider adoption, especially for newer modalities. Capital equipment requirements and training needs can slow uptake in smaller facilities, creating uneven penetration across regions and care settings. Procedural choice also depends on patient selection and anatomy, which can limit addressable volume for specific modalities.

Clinical decision-making complexity creates additional barriers. Providers must balance symptom severity, durability expectations, sexual function preservation goals, and comorbidity constraints, which can slow standardization of newer procedures. Real-world outcomes variability across centers can impact confidence in switching from established approaches. Supply chain considerations for specialized components and maintenance support can further affect purchasing decisions in cost-sensitive markets.

- For instance, Boston Scientific’s Rezūm™ water vapor thermal therapy pivotal 5-year data reported IPSS reduced 48%, Qmax improved 44%, and a 4.4% surgical retreatment rate, with no reports of device- or procedure-related sexual dysfunction—metrics that directly inform “durability vs. function preservation” trade-offs during procedure selection and patient counseling.

Market Trends and Opportunities

Outpatient and office-based procedural growth continues to reshape care delivery, creating opportunity for device platforms optimized for shorter procedures, simplified workflows, and reduced anesthesia requirements. Expansion of ambulatory surgical centers and specialty clinics increases the relevance of solutions designed for repeatable, high-throughput use. Evidence development focused on durability, retreatment reduction, and patient-reported outcomes remains central to adoption acceleration. Procedure standardization and training programs represent a key lever for scaling utilization beyond high-volume academic centers.

Technology convergence across imaging, energy control, and procedural robotics supports differentiation and premium positioning in advanced care settings. Product portfolios that integrate capital equipment, consumables, and service contracts strengthen long-term account value. Emerging markets offer incremental growth as urology infrastructure expands and diagnosis rates improve. Partnerships that accelerate clinician training and improve affordability pathways can unlock new patient pools currently managed primarily with medication.

- For instance, Intuitive Surgical reported its da Vinci installed base reached 10,189 systems as of March 31, 2025, with worldwide da Vinci procedures growing approximately 17% year-over-year in Q1 2025 and 367 systems placed in the quarter (including 147 da Vinci 5 systems), illustrating how scaled robotics platforms can pull utilization through standardized instrument workflows across sites of care.

Regional Insights

North America

North America held 34.40% share in 2025, supported by strong urology infrastructure, high diagnosis rates, and broad access to minimally invasive and surgical BPH interventions. The region benefits from established reimbursement pathways that support procedural adoption and device utilization in both hospitals and outpatient settings. Adoption is reinforced by clinical awareness, patient demand for faster symptom relief, and availability of advanced endoscopic and ablation platforms. Competitive intensity is high due to rapid technology uptake and demand for durable outcomes.

Europe

Europe captured 25.40% share in 2025, reflecting mature healthcare systems and consistent procedural capacity across leading countries. Hospitals remain central to surgical volumes, with outpatient growth supported by evolving care pathways and increasing utilization of minimally invasive options. Demand is influenced by guideline-led practice patterns, access to endoscopic infrastructure, and emphasis on recovery and safety profiles. Procurement discipline and cost-effectiveness considerations shape adoption pace for newer platforms.

Asia Pacific

Asia Pacific accounted for 26.10% share in 2025, supported by demographic scale, rising diagnosis, and improving access to urology services. Growth is reinforced by investment in hospital capacity, expansion of specialty centers, and gradual migration toward minimally invasive approaches in urban markets. Adoption patterns vary by country based on reimbursement, affordability, and procedural infrastructure availability. The region offers long-term expansion potential as access gaps narrow and procedural volumes rise.

Latin America

Latin America represented 7.20% share in 2025, with demand concentrated in larger economies where private healthcare capacity supports interventional urology services. Device penetration remains uneven due to reimbursement variability and differences in facility-level access to advanced platforms. Urban specialty clinics and tertiary hospitals anchor procedural volumes, supporting steady utilization of established surgical workflows. Opportunities remain linked to infrastructure investment and broader access to minimally invasive options.

Middle East & Africa

Middle East & Africa contributed 6.90% share in 2025, driven by higher-spend markets and centers of excellence in specialty care. Device adoption is supported by investment in advanced hospital systems and growth of private healthcare in select countries. Penetration remains constrained in many markets by affordability, limited specialist density, and variable access to endoscopic infrastructure. Market expansion is expected to be uneven, with growth pockets centered around modernized urology hubs.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Competitive Landscape

Competition in the benign prostatic hyperplasia treatment devices market is shaped by technology differentiation, clinical evidence depth, and the ability to integrate smoothly into existing urology workflows. Leading companies compete through platform innovation across endoscopic resection, lasers, implants, and ablation modalities, supported by training programs and procedural standardization initiatives. Commercial strategies emphasize account penetration in hospitals and rapid adoption in ambulatory settings where outpatient procedures are expanding. Portfolio breadth, service capability, and evidence-based positioning remain key differentiators across tender-driven and relationship-driven purchasing environments.

Boston Scientific Corporation maintains a strong position through a broad urology portfolio aligned with minimally invasive procedural adoption and outpatient care migration. The company approach typically emphasizes clinical evidence generation, physician training, and workflow design that supports repeatable procedure execution across varied care settings. Portfolio integration across devices and supporting accessories strengthens account value and supports long-term utilization. Expansion strategies often focus on increasing addressable patient pools and simplifying procedural pathways for broader clinician uptake.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Boston Scientific Corporation

- Teleflex Incorporated

- Olympus (Olympus Corporation / Olympus America)

- KARL STORZ

- Cook (Cook Medical / Cook Group)

- Richard Wolf GmbH

- Dornier MedTech

- Lumenis

- Medtronic plc

- PROCEPT BioRobotics Corporation

- Coloplast (Coloplast A/S / Coloplast Group)

- CONMED Corporation

- Quanta System S.p.A.

- Laborie

- SonaCare Medical LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments

- In February 2025, Olympus APAC announced a milestone for its iTind device with expanded availability across major Asia-Pacific markets, noting an upcoming Korea launch scheduled for March. In the same update, Olympus described iTind as a minimally invasive BPH procedure and highlighted physician training support as part of the regional roll-out.

- In June 2025, Teleflex announced it signed an MoU with Fortis Hospitals Bengaluru to create a UroLift Center of Education in India. In this collaboration, the parties stated the program is designed to provide hands-on training for urologists to support safe delivery and appropriate patient selection for the UroLift System.

- In September 2025, Olympus announced an iTind Center of Excellence Program aimed at advancing minimally invasive treatment for symptoms due to urinary outflow obstruction secondary to BPH.

- In December 2025, Boston Scientific communicated the launch of the Rezūm EVO Water Vapour Therapy Console as a next-generation console intended to be used with the current Rezūm delivery device. In the same release, Boston Scientific emphasized design changes such as reduced footprint and improved mobility to support use across different care settings

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 1840.33 million |

| Revenue forecast in 2032 |

USD 3407.64 million |

| Growth rate (CAGR) |

9.2% |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Treatment / Intervention Type Outlook: Minimally invasive procedures, Invasive surgical procedures; By Product (Device Category) Outlook: Resectoscopes, Urology lasers, Radiofrequency ablation devices, Prostatic stents, Implants, Electrodes, Catheters; By Procedure Type Outlook: TURP, Laser surgery, UroLift procedure, TUMT, TUNA, Others; By End User Outlook: Hospitals, Ambulatory Surgical Centers (ASCs), Specialty clinics, Others |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

| Boston Scientific Corporation; Teleflex Incorporated; Olympus (Olympus Corporation / Olympus America); KARL STORZ; Cook (Cook Medical / Cook Group); Richard Wolf GmbH; Dornier MedTech; Lumenis; Medtronic plc; PROCEPT BioRobotics Corporation; Coloplast (Coloplast A/S / Coloplast Group); CONMED Corporation; Quanta System S.p.A.; Laborie; SonaCare Medical LLC |

|

| No. of Pages |

340 |

Segmentation

BY TREATMENT / INTERVENTION TYPE

- Minimally invasive procedures

- Invasive surgical procedures

BY PRODUCT (DEVICE CATEGORY)

- Resectoscopes

- Urology lasers

- Radiofrequency ablation devices

- Prostatic stents

- Implants

- Electrodes

- Catheters

BY PROCEDURE TYPE

- TURP (Transurethral Resection of the Prostate)

- Laser surgery

- UroLift procedure

- TUMT (Transurethral Microwave Thermotherapy)

- TUNA (Transurethral Needle Ablation)

- Others

BY END USER

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Specialty clinics

- Others

BY REGION

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa