1. Preface

1.1. Report Description

1.1.1. Purpose of the Report

1.1.2. Target Audience

1.1.3. USP and Key Offerings

1.2. Research Scope

1.3. Market Introduction

2. Executive Summary

2.1. Market Snapshot: Global Bunker Fuel Market

2.1.1. Global Bunker Fuel Market, By Fuel Type

2.1.2. Global Bunker Fuel Market, By Vessel Type

2.1.3. Global Bunker Fuel Market, By Region

2.2. Insights from Primary Respondents

3. Market Dynamics & Factors Analysis

3.1. Introduction

3.1.1. Global Bunker Fuel Market Value, 2019-2032, (US$ Mn)

3.1.2. Y-o-Y Growth Trend Analysis

3.2. Market Dynamics

3.2.1. Bunker Fuel Market Drivers

3.2.2. Bunker Fuel Market Restraints

3.2.3. Bunker Fuel Market Opportunities

3.2.4. Major Bunker Fuel Industry Challenges

3.3. Growth and Development Patterns

3.4. Investment Feasibility Analysis

3.5. Market Opportunity Analysis

3.5.1. Fuel Type

3.5.2. Vessel Type

3.5.3. Geography

4. Market Competitive Landscape Analysis

4.1. Company Market Share Analysis, 2023

4.1.1. Global Bunker Fuel Market: Company Market Share, Value 2023

4.1.2. Global Bunker Fuel Market: Top 6 Company Market Share, Value 2023

4.1.3. Global Bunker Fuel Market: Top 3 Company Market Share, Value 2023

4.2. Global Bunker Fuel Market: Company Revenue Share Analysis, 2023

4.3. Company Assessment Metrics, 2023

4.3.1. Stars

4.3.2. Emerging Leaders

4.3.3. Pervasive Players

4.3.4. Participants

4.4. Startups/ SMEs Assessment Metrics, 2023

4.4.1. Progressive Companies

4.4.2. Responsive Companies

4.4.3. Dynamic Companies

4.4.4. Starting Blocks

4.5. Strategic Development

4.5.1. Acquisition and Mergers

4.5.2. New Product Launch

4.5.3. Regional Expansion

4.5.4. Partnerships

4.6. Key Player Product Matrix

4.7. Potential for New Players in the Global Bunker Fuel Market

5. Premium Insights

5.1. STAR (Situation, Task, Action, Results) Analysis

5.2. Porter’s Five Forces Analysis

5.2.1. Threat of New Entrants

5.2.2. Bargaining Power of Buyers/Consumers

5.2.3. Bargaining Power of Suppliers

5.2.4. Threat of Substitute Types

5.2.5. Intensity of Competitive Rivalry

5.3. PESTEL Analysis

5.3.1. Political Factors

5.3.2. Economic Factors

5.3.3. Social Factors

5.3.4. Technological Factors

5.3.5. Environmental Factors

5.3.6. Legal Factors

5.4. Key Market Trends

5.4.1. Demand Side Trends

5.4.2. Supply Side Trends

5.5. Value Chain Analysis

5.6. Technology Analysis

5.6.1. Research and development in the global market

5.6.2. Patent Analysis

5.6.3. Emerging technologies and their potential disruption to the market

5.7. Consumer Behaviour Analysis

5.7.1. Consumer Preferences and Expectations

5.7.2. Factors Influencing Consumer Buying Decisions

5.7.2.1. North America

5.7.2.2. Europe

5.7.2.3. Asia Pacific

5.7.2.4. Latin America

5.7.2.5. Middle East and Africa

5.7.3. Consumer Pain Points

5.8. Analysis and Recommendations

5.9. Adjacent Market Analysis

6. Market Positioning of Key Players, 2023

6.1. Company market share of key players, 2023

6.2. Competitive Benchmarking

6.3. Market Positioning of Key Vendors

6.4. Geographical Presence Analysis

6.5. Major Strategies Adopted by Key Players

6.5.1. Key Strategies Analysis

6.5.2. Mergers and Acquisitions

6.5.3. Partnerships

6.5.4. Product Launch

6.5.5. Geographical Expansion

6.5.6. Others

7. Impact Analysis of COVID 19 and Russia – Ukraine War on Bunker Fuel Market

7.1. Ukraine-Russia War Impact

7.1.1. Uncertainty and Economic Instability

7.1.2. Supply chain disruptions

7.1.3. Regional market shifts

7.1.4. Shift in government priorities

7.2. COVID-19 Impact Analysis

7.2.1. Supply Chain Disruptions

7.2.2. Demand Fluctuations

7.2.3. Shift in Product Mix

7.2.4. Reduced Industrial Activity

7.2.5. Regional Impact Analysis

7.2.5.1. North America

7.2.5.2. Europe

7.2.5.3. Asia Pacific

7.2.5.4. Latin America

7.2.5.5. Middle East and Africa

8. Global Bunker Fuel Market, By Fuel Type

8.1. Global Bunker Fuel Market Overview, by Fuel Type

8.1.1. Global Bunker Fuel Market Revenue Share, By Fuel Type, 2023 Vs 2032 (in %)

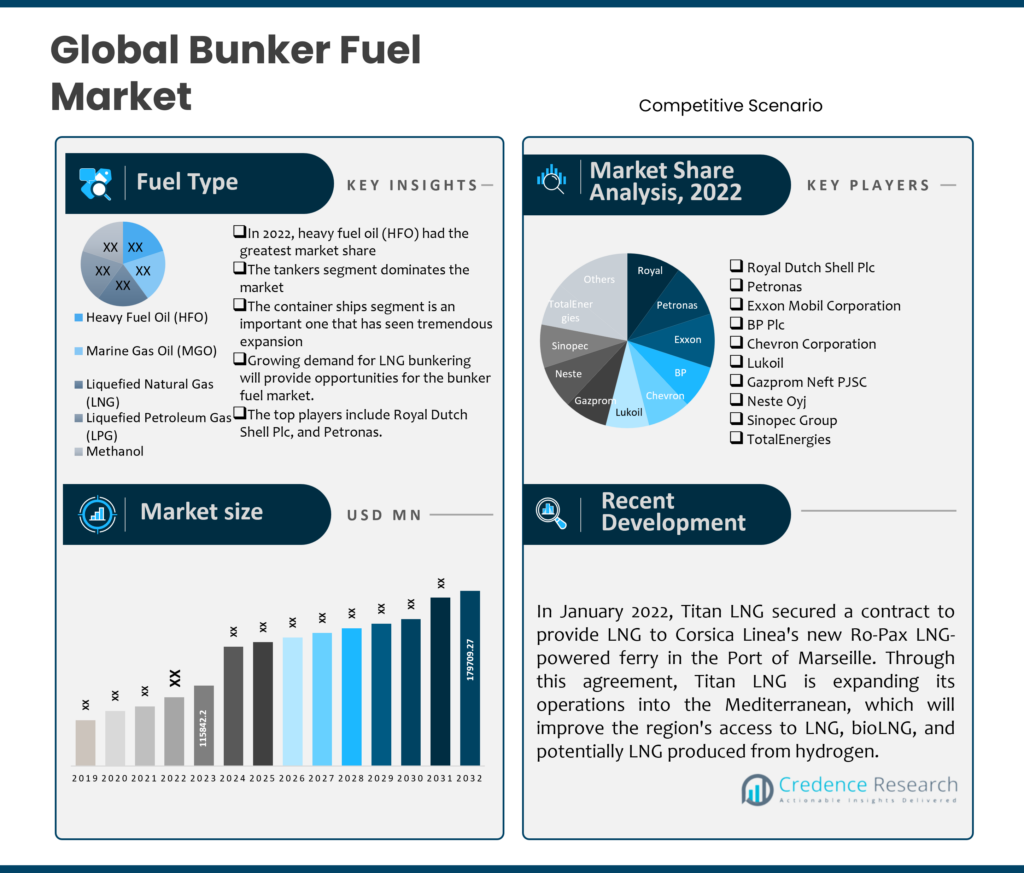

8.2. Heavy Fuel Oil (HFO)

8.2.1. Global Bunker Fuel Market, By Heavy Fuel Oil (HFO), By Region, 2019-2032 (US$ Mn)

8.2.2. Market Dynamics for Heavy Fuel Oil (HFO)

8.2.2.1. Drivers

8.2.2.2. Restraints

8.2.2.3. Opportunities

8.2.2.4. Trends

8.3. Marine Gas Oil (MGO)

8.3.1. Global Bunker Fuel Market, By Marine Gas Oil (MGO), By Region, 2019-2032 (US$ Mn)

8.3.2. Market Dynamics for Marine Gas Oil (MGO)

8.3.2.1. Drivers

8.3.2.2. Restraints

8.3.2.3. Opportunities

8.3.2.4. Trends

8.4. Liquefied Natural Gas (LNG)

8.4.1. Global Bunker Fuel Market, By Liquefied Natural Gas (LNG), By Region, 2019-2032 (US$ Mn)

8.4.2. Market Dynamics for Liquefied Natural Gas (LNG)

8.4.2.1. Drivers

8.4.2.2. Restraints

8.4.2.3. Opportunities

8.4.2.4. Trends

8.5. Liquefied Petroleum Gas (LPG)

8.5.1. Global Bunker Fuel Market, By Liquefied Petroleum Gas (LPG), By Region, 2019-2032 (US$ Mn)

8.5.2. Market Dynamics for Liquefied Petroleum Gas (LPG)

8.5.2.1. Drivers

8.5.2.2. Restraints

8.5.2.3. Opportunities

8.5.2.4. Trends

8.6. Methanol

8.6.1. Global Bunker Fuel Market, By Methanol, By Region, 2019-2032 (US$ Mn)

8.6.2. Market Dynamics for Methanol

8.6.2.1. Drivers

8.6.2.2. Restraints

8.6.2.3. Opportunities

8.6.2.4. Trends

9. Global Bunker Fuel Market, By Vessel Type

9.1. Global Bunker Fuel Market Overview, by Vessel Type

9.1.1. Global Bunker Fuel Market Revenue Share, By Vessel Type, 2023 Vs 2032 (in %)

9.2. Container Ships

9.2.1. Global Bunker Fuel Market, Container Ships, By Region, 2019-2032 (US$ Mn)

9.2.2. Market Dynamics for Container Ships

9.2.2.1. Drivers

9.2.2.2. Restraints

9.2.2.3. Opportunities

9.2.2.4. Trends

9.3. Bulk Carriers

9.3.1. Global Bunker Fuel Market, By Bulk Carriers, By Region, 2019-2032 (US$ Mn)

9.3.2. Market Dynamics for Bulk Carriers

9.3.2.1. Drivers

9.3.2.2. Restraints

9.3.2.3. Opportunities

9.3.2.4. Trends

9.4. Tankers

9.4.1. Global Bunker Fuel Market, By Tankers, By Region, 2019-2032 (US$ Mn)

9.4.2. Market Dynamics for Tankers

9.4.2.1. Drivers

9.4.2.2. Restraints

9.4.2.3. Opportunities

9.4.2.4. Trends

9.5. LNG Carriers

9.5.1. Global Bunker Fuel Market, By LNG Carriers, By Region, 2019-2032 (US$ Mn)

9.5.2. Market Dynamics for LNG Carriers

9.5.2.1. Drivers

9.5.2.2. Restraints

9.5.2.3. Opportunities

9.5.2.4. Trends

9.6. Passenger Vessels

9.6.1. Global Bunker Fuel Market, By Passenger Vessels, By Region, 2019-2032 (US$ Mn)

9.6.2. Market Dynamics for Passenger Vessels

9.6.2.1. Drivers

9.6.2.2. Restraints

9.6.2.3. Opportunities

9.6.2.4. Trends

9.7. Offshore Support Vessels (OSVs)

9.7.1. Global Bunker Fuel Market, By Offshore Support Vessels (OSVs), By Region, 2019-2032 (US$ Mn)

9.7.2. Market Dynamics for Offshore Support Vessels (OSVs)

9.7.2.1. Drivers

9.7.2.2. Restraints

9.7.2.3. Opportunities

9.7.2.4. Trends

10. Global Bunker Fuel Market, By Region

10.1. Global Bunker Fuel Market Overview, by Region

10.1.1. Global Bunker Fuel Market, By Region, 2023 Vs 2032 (in%)

10.2. Fuel Type

10.2.1. Global Bunker Fuel Market, By Fuel Type, 2019-2032 (US$ Mn)

10.3. Vessel Type

10.3.1. Global Bunker Fuel Market, By Vessel Type, 2019-2032 (US$ Mn)

11. North America Bunker Fuel Market Analysis

11.1. Overview

11.1.1. Market Dynamics for North America

11.1.1.1. Drivers

11.1.1.2. Restraints

11.1.1.3. Opportunities

11.1.1.4. Trends

11.2. North America Bunker Fuel Market, by Fuel Type, 2019-2032(US$ Mn)

11.2.1. Overview

11.2.2. SRC Analysis

11.3. North America Bunker Fuel Market, by Vessel Type, 2019-2032(US$ Mn)

11.3.1. Overview

11.3.2. SRC Analysis

11.4. North America Bunker Fuel Market, by Country, 2019-2032 (US$ Mn)

11.4.1. North America Bunker Fuel Market, by Country, 2023 Vs 2032 (in%)

11.4.2. U.S.

11.4.3. Canada

11.4.4. Mexico

12. Europe Bunker Fuel Market Analysis

12.1. Overview

12.1.1. Market Dynamics for Europe

12.1.1.1. Drivers

12.1.1.2. Restraints

12.1.1.3. Opportunities

12.1.1.4. Trends

12.2. Europe Bunker Fuel Market, by Fuel Type, 2019-2032(US$ Mn)

12.2.1. Overview

12.2.2. SRC Analysis

12.3. Europe Bunker Fuel Market, by Vessel Type, 2019-2032(US$ Mn)

12.3.1. Overview

12.3.2. SRC Analysis

12.4. Europe Bunker Fuel Market, by Country, 2019-2032 (US$ Mn)

12.4.1. Europe Bunker Fuel Market, by Country, 2023 Vs 2032 (in%)

12.4.2. UK

12.4.3. France

12.4.4. Germany

12.4.5. Italy

12.4.6. Spain

12.4.7. Benelux

12.4.8. Russia

12.4.9. Rest of Europe

13. Asia Pacific Bunker Fuel Market Analysis

13.1. Overview

13.1.1. Market Dynamics for Asia Pacific

13.1.1.1. Drivers

13.1.1.2. Restraints

13.1.1.3. Opportunities

13.1.1.4. Trends

13.2. Asia Pacific Bunker Fuel Market, by Fuel Type, 2019-2032(US$ Mn)

13.2.1. Overview

13.2.2. SRC Analysis

13.3. Asia Pacific Bunker Fuel Market, by Vessel Type, 2019-2032(US$ Mn)

13.3.1. Overview

13.3.2. SRC Analysis

13.4. Asia Pacific Bunker Fuel Market, by Country, 2019-2032 (US$ Mn)

13.4.1. Asia Pacific Bunker Fuel Market, by Country, 2023 Vs 2032 (in%)

13.4.2. China

13.4.3. Japan

13.4.4. India

13.4.5. South Korea

13.4.6. South East Asia

13.4.7. Rest of Asia Pacific

14. Latin America Bunker Fuel Market Analysis

14.1. Overview

14.1.1. Market Dynamics for Latin America

14.1.1.1. Drivers

14.1.1.2. Restraints

14.1.1.3. Opportunities

14.1.1.4. Trends

14.2. Latin America Bunker Fuel Market, by Fuel Type, 2019-2032(US$ Mn)

14.2.1. Overview

14.2.2. SRC Analysis

14.3. Latin America Bunker Fuel Market, by Vessel Type, 2019-2032(US$ Mn)

14.3.1. Overview

14.3.2. SRC Analysis

14.4. Latin America Bunker Fuel Market, by Country, 2019-2032 (US$ Mn)

14.4.1. Latin America Bunker Fuel Market, by Country, 2023 Vs 2032 (in%)

14.4.2. Brazil

14.4.3. Argentina

14.4.4. Rest of Latin America

15. Middle East Bunker Fuel Market Analysis

15.1. Overview

15.1.1. Market Dynamics for Middle East

15.1.1.1. Drivers

15.1.1.2. Restraints

15.1.1.3. Opportunities

15.1.1.4. Trends

15.2. Middle East Bunker Fuel Market, by Fuel Type, 2019-2032(US$ Mn)

15.2.1. Overview

15.2.2. SRC Analysis

15.3. Middle East Bunker Fuel Market, by Vessel Type, 2019-2032(US$ Mn)

15.3.1. Overview

15.3.2. SRC Analysis

15.4. Middle East Bunker Fuel Market, by Country, 2019-2032 (US$ Mn)

15.4.1. Middle East Bunker Fuel Market, by Country, 2023 Vs 2032 (in%)

15.4.2. UAE

15.4.3. Saudi Arabia

15.4.4. Rest of Middle East

16. Africa Bunker Fuel Market Analysis

16.1. Overview

16.1.1. Market Dynamics for Africa

16.1.1.1. Drivers

16.1.1.2. Restraints

16.1.1.3. Opportunities

16.1.1.4. Trends

16.2. Africa Bunker Fuel Market, by Fuel Type, 2019-2032(US$ Mn)

16.2.1. Overview

16.2.2. SRC Analysis

16.3. Africa Bunker Fuel Market, by Vessel Type, 2019-2032(US$ Mn)

16.3.1. Overview

16.3.2. SRC Analysis

16.4. Africa Bunker Fuel Market, by Country, 2019-2032 (US$ Mn)

16.4.1. Africa Bunker Fuel Market, by Country, 2023 Vs 2032 (in%)

16.4.2. South Africa

16.4.3. Egypt

16.4.4. Rest of Africa

17. Company Profiles

17.1. Royal Dutch Shell Plc

17.1.1. Company Overview

17.1.2. Products/Services Portfolio

17.1.3. Geographical Presence

17.1.4. SWOT Analysis

17.1.5. Financial Summary

17.1.5.1. Market Revenue and Net Profit (2019-2023)

17.1.5.2. Business Segment Revenue Analysis

17.1.5.3. Geographical Revenue Analysis

17.2. Petronas

17.3. Exxon Mobil Corporation

17.4. BP Plc

17.5. Chevron Corporation

17.6. Lukoil

17.7. Gazprom Neft PJSC

17.8. Neste Oyj

17.9. Sinopec Group

17.10. TotalEnergies

17.11. Others

18. Research Methodology

18.1. Research Methodology

18.2. Phase I – Secondary Research

18.3. Phase II – Data Modelling

18.3.1. Company Share Analysis Model

18.3.2. Revenue Based Modelling

18.4. Phase III – Primary Research

18.5. Research Limitations

18.5.1. Assumptions

List of Figures

FIG. 1 Global Bunker Fuel Market: Research Methodology

FIG. 2 Market Size Estimation – Top Down & Bottom up Approach

FIG. 3 Global Bunker Fuel Market Segmentation

FIG. 4 Global Bunker Fuel Market, by Fuel Type, 2023 (US$ Mn)

FIG. 5 Global Bunker Fuel Market, by Vessel Type, 2023 (US$ Mn)

FIG. 6 Global Bunker Fuel Market, by Geography, 2023 (US$ Mn)

FIG. 7 Attractive Investment Proposition, by Fuel Type, 2023

FIG. 8 Attractive Investment Proposition, by Vessel Type, 2023

FIG. 9 Attractive Investment Proposition, by Geography, 2023

FIG. 10 Global Market Share Analysis of Key Bunker Fuel Market Manufacturers, 2023

FIG. 11 Global Market Positioning of Key Bunker Fuel Market Manufacturers, 2023

FIG. 12 Global Bunker Fuel Market Value Contribution, By Fuel Type, 2023 & 2032 (Value %)

FIG. 13 Global Bunker Fuel Market, by Heavy Fuel Oil (HFO), Value, 2019-2032 (US$ Mn)

FIG. 14 Global Bunker Fuel Market, by Marine Gas Oil (MGO), Value, 2019-2032 (US$ Mn)

FIG. 15 Global Bunker Fuel Market, by Liquefied Natural Gas (LNG), Value, 2019-2032 (US$ Mn)

FIG. 16 Global Bunker Fuel Market, by Liquefied Petroleum Gas (LPG), Value, 2019-2032 (US$ Mn)

FIG. 17 Global Bunker Fuel Market, by Methanol, Value, 2019-2032 (US$ Mn)

FIG. 18 Global Bunker Fuel Market Value Contribution, By Vessel Type, 2023 & 2032 (Value %)

FIG. 19 Global Bunker Fuel Market, by Container Ships, Value, 2019-2032 (US$ Mn)

FIG. 20 Global Bunker Fuel Market, by Bulk Carriers, Value, 2019-2032 (US$ Mn)

FIG. 21 Global Bunker Fuel Market, by Tankers, Value, 2019-2032 (US$ Mn)

FIG. 22 Global Bunker Fuel Market, by LNG Carriers, Value, 2019-2032 (US$ Mn)

FIG. 23 Global Bunker Fuel Market, by Passenger Vessels, Value, 2019-2032 (US$ Mn)

FIG. 24 Global Bunker Fuel Market, by Offshore Support Vessels (OSVs), Value, 2019-2032 (US$ Mn)

FIG. 25 North America Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 26 U.S. Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 27 Canada Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 28 Mexico Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 29 Europe Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 30 Germany Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 31 France Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 32 U.K. Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 33 Italy Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 34 Spain Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 35 Benelux Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 36 Russia Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 37 Rest of Europe Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 38 Asia Pacific Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 39 China Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 40 Japan Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 41 India Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 42 South Korea Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 43 South-East Asia Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 44 Rest of Asia Pacific Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 45 Latin America Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 46 Brazil Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 47 Argentina Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 48 Rest of Latin America Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 49 Middle East Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 50 UAE Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 51 Saudi Arabia Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 52 Rest of Middle East Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 53 Africa Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 54 South Africa Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 55 Egypt Bunker Fuel Market, 2019-2032 (US$ Mn)

FIG. 56 Rest of Africa Bunker Fuel Market, 2019-2032 (US$ Mn)

List of Tables

TABLE 1 Market Snapshot: Global Bunker Fuel Market

TABLE 2 Global Bunker Fuel Market: Market Drivers Impact Analysis

TABLE 3 Global Bunker Fuel Market: Market Restraints Impact Analysis

TABLE 4 Global Bunker Fuel Market, by Competitive Benchmarking, 2023

TABLE 5 Global Bunker Fuel Market, by Geographical Presence Analysis, 2023

TABLE 6 Global Bunker Fuel Market, by Key Strategies Analysis, 2023

TABLE 7 Global Bunker Fuel Market, by Heavy Fuel Oil (HFO), By Region, 2019-2023 (US$ Mn)

TABLE 8 Global Bunker Fuel Market, by Heavy Fuel Oil (HFO), By Region, 2024-2032 (US$ Mn)

TABLE 9 Global Bunker Fuel Market, by Marine Gas Oil (MGO), By Region, 2019-2023 (US$ Mn)

TABLE 10 Global Bunker Fuel Market, by Marine Gas Oil (MGO), By Region, 2024-2032 (US$ Mn)

TABLE 11 Global Bunker Fuel Market, by Liquefied Natural Gas (LNG), By Region, 2019-2023 (US$ Mn)

TABLE 12 Global Bunker Fuel Market, by Liquefied Natural Gas (LNG), By Region, 2024-2032 (US$ Mn)

TABLE 13 Global Bunker Fuel Market, by Liquefied Petroleum Gas (LPG), By Region, 2019-2023 (US$ Mn)

TABLE 14 Global Bunker Fuel Market, by Liquefied Petroleum Gas (LPG), By Region, 2024-2032 (US$ Mn)

TABLE 15 Global Bunker Fuel Market, by Methanol, By Region, 2019-2023 (US$ Mn)

TABLE 16 Global Bunker Fuel Market, by Methanol, By Region, 2024-2032 (US$ Mn)

TABLE 17 Global Bunker Fuel Market, by Container Ships, By Region, 2019-2023 (US$ Mn)

TABLE 18 Global Bunker Fuel Market, by Container Ships, By Region, 2024-2032 (US$ Mn)

TABLE 19 Global Bunker Fuel Market, by Bulk Carriers, By Region, 2019-2023 (US$ Mn)

TABLE 20 Global Bunker Fuel Market, by Bulk Carriers, By Region, 2024-2032 (US$ Mn)

TABLE 21 Global Bunker Fuel Market, by Tankers, By Region, 2019-2023 (US$ Mn)

TABLE 22 Global Bunker Fuel Market, by Tankers, By Region, 2024-2032 (US$ Mn)

TABLE 23 Global Bunker Fuel Market, by LNG Carriers, By Region, 2019-2023 (US$ Mn)

TABLE 24 Global Bunker Fuel Market, by LNG Carriers, By Region, 2024-2032 (US$ Mn)

TABLE 25 Global Bunker Fuel Market, by Passenger Vessels, By Region, 2019-2023 (US$ Mn)

TABLE 26 Global Bunker Fuel Market, by Passenger Vessels, By Region, 2024-2032 (US$ Mn)

TABLE 27 Global Bunker Fuel Market, by Offshore Support Vessels (OSVs), By Region, 2019-2023 (US$ Mn)

TABLE 28 Global Bunker Fuel Market, by Offshore Support Vessels (OSVs), By Region, 2024-2032 (US$ Mn)

TABLE 29 Global Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 30 Global Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 31 Global Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 32 Global Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 33 Global Bunker Fuel Market, by Region, 2019-2023 (US$ Mn)

TABLE 34 Global Bunker Fuel Market, by Region, 2024-2032 (US$ Mn)

TABLE 35 North America Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 36 North America Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 37 North America Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 38 North America Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 39 North America Bunker Fuel Market, by Country, 2019-2023 (US$ Mn)

TABLE 40 North America Bunker Fuel Market, by Country, 2024-2032 (US$ Mn)

TABLE 41 United States Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 42 United States Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 43 United States Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 44 United States Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 45 Canada Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 46 Canada Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 47 Canada Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 48 Canada Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 49 Mexico Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 50 Mexico Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 51 Mexico Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 52 Mexico Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 53 Europe Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 54 Europe Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 55 Europe Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 56 Europe Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 57 Europe Bunker Fuel Market, by Country, 2019-2023 (US$ Mn)

TABLE 58 Europe Bunker Fuel Market, by Country, 2024-2032 (US$ Mn)

TABLE 59 Germany Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 60 Germany Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 61 Germany Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 62 Germany Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 63 France Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 64 France Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 65 France Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 66 France Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 67 United Kingdom Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 68 United Kingdom Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 69 United Kingdom Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 70 United Kingdom Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 71 Italy Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 72 Italy Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 73 Italy Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 74 Italy Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 75 Spain Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 76 Spain Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 77 Spain Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 78 Spain Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 79 Benelux Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 80 Benelux Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 81 Benelux Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 82 Benelux Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 83 Russia Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 84 Russia Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 85 Russia Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 86 Russia Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 87 Rest of Europe Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 88 Rest of Europe Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 89 Rest of Europe Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 90 Rest of Europe Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 91 Asia Pacific Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 92 Asia Pacific Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 93 Asia Pacific Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 94 Asia Pacific Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 95 China Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 96 China Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 97 China Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 98 China Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 99 Japan Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 100 Japan Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 101 Japan Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 102 Japan Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 103 India Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 104 India Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 105 India Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 106 India Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 107 South Korea Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 108 South Korea Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 109 South Korea Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 110 South Korea Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 111 South-East Asia Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 112 South-East Asia Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 113 South-East Asia Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 114 South-East Asia Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 115 Rest of Asia Pacific Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 116 Rest of Asia Pacific Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 117 Rest of Asia Pacific Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 118 Rest of Asia Pacific Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 119 Latin America Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 120 Latin America Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 121 Latin America Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 122 Latin America Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 123 Brazil Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 124 Brazil Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 125 Brazil Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 126 Brazil Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 127 Argentina Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 128 Argentina Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 129 Argentina Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 130 Argentina Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 131 Rest of Latin America Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 132 Rest of Latin America Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 133 Rest of Latin America Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 134 Rest of Latin America Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 135 Middle East Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 136 Middle East Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 137 Middle East Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 138 Middle East Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 139 UAE Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 140 UAE Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 141 UAE Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 142 UAE Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 143 Saudi Arabia Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 144 Saudi Arabia Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 145 Saudi Arabia Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 146 Saudi Arabia Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 147 Rest of Middle East Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 148 Rest of Middle East Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 149 Rest of Middle East Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 150 Rest of Middle East Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 151 Africa Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 152 Africa Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 153 Africa Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 154 Africa Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 155 South Africa Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 156 South Africa Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 157 South Africa Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 158 South Africa Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 159 Egypt Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 160 Egypt Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 161 Egypt Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 162 Egypt Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)

TABLE 163 Rest of Africa Bunker Fuel Market, by Fuel Type, 2019-2023 (US$ Mn)

TABLE 164 Rest of Africa Bunker Fuel Market, by Fuel Type, 2024-2032 (US$ Mn)

TABLE 165 Rest of Africa Bunker Fuel Market, by Vessel Type, 2019-2023 (US$ Mn)

TABLE 166 Rest of Africa Bunker Fuel Market, by Vessel Type, 2024-2032 (US$ Mn)