Market Overview:

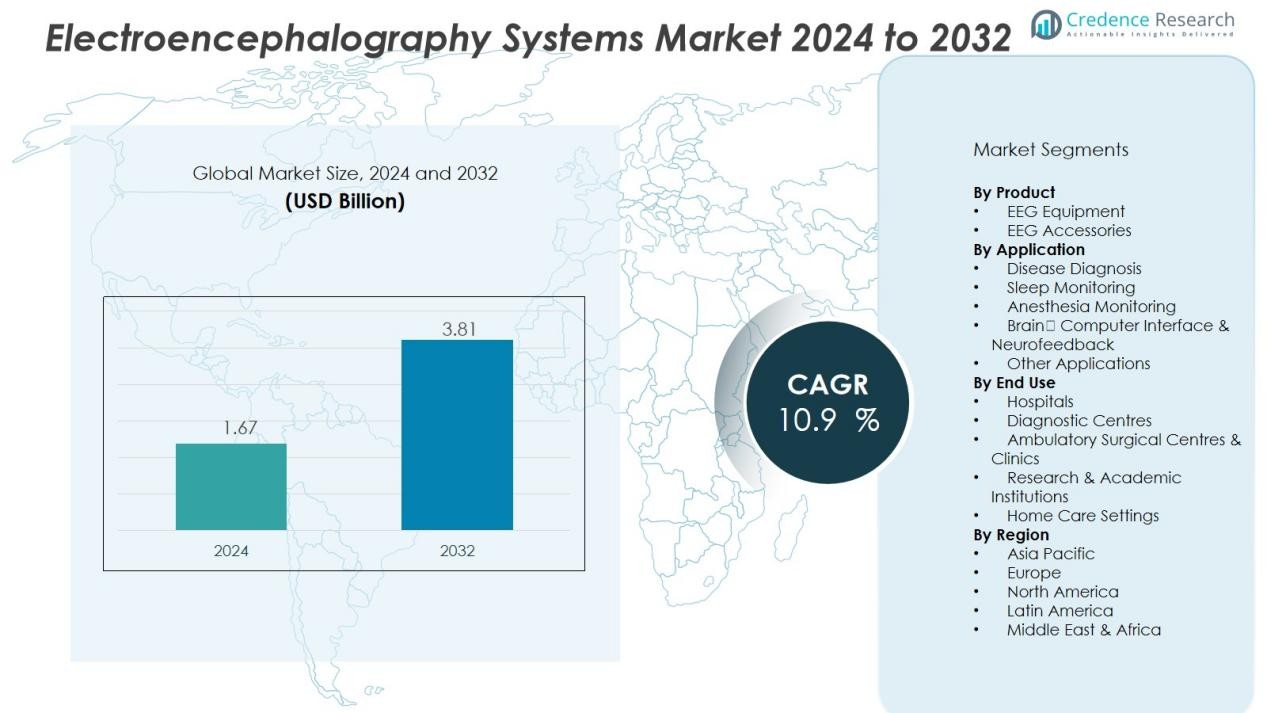

The Electroencephalography Systems Market size was valued at USD 1.67 billion in 2024 and is anticipated to reach USD 3.81 billion by 2032, at a CAGR of 10.9 % during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Electroencephalography Systems Market Size 2024 |

USD 1.67 Billion |

| Electroencephalography Systems Market, CAGR |

10.9 % |

| Electroencephalography Systems Market Size 2032 |

USD 3.81 Billion |

Several key factors are driving the market’s expansion. The growing incidence of neurological diseases, coupled with increasing awareness and advancements in diagnostic technologies, has heightened the demand for EEG systems. Technological innovations, including portable, wearable EEG devices, wireless connectivity, and cloud-based analytics, have made EEG systems more accessible and user-friendly. Additionally, the expanding healthcare infrastructure and improved reimbursement policies, particularly in emerging markets, are facilitating the wider adoption of EEG systems in clinical settings and home-monitoring applications.

Regionally, North America holds the largest market share due to its advanced healthcare infrastructure, high prevalence of neurological conditions, and strong insurance reimbursement frameworks. The Asia Pacific region is expected to experience the highest growth, fueled by increasing healthcare access, rising patient awareness, and a growing burden of neurological diseases in countries like China and India. Europe follows with steady growth, while markets in Latin America and the Middle East & Africa are emerging with promising potential driven by expanding healthcare investments.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights:

- The Electroencephalography Systems Market was valued at USD 1.67 billion in 2024 and is projected to reach USD 3.81 billion by 2032, growing at a CAGR of 10.9% during the forecast period.

- North America holds the largest market share at approximately 35.5%, driven by advanced healthcare infrastructure, a high prevalence of neurological disorders, and robust reimbursement policies.

- Europe commands about 26% of the market share, supported by an aging population, rising neurodegenerative diseases, and government investments in neurological health.

- Asia Pacific is the fastest-growing region, with a market share estimated between 20-25%, driven by increasing healthcare spending, expanding diagnostic infrastructure, and rising neurological disorder awareness, especially in China and India.

- In terms of segment distribution, the EEG equipment segment is the largest, while hospitals dominate the end-use segment, holding a significant share due to their widespread use of EEG systems in neurology departments.

Market Drivers:

Rising Prevalence of Neurological Disorders Driving Demand

The increasing prevalence of neurological disorders such as epilepsy, Alzheimer’s disease, Parkinson’s disease, and sleep disorders is a significant driver for the Electroencephalography Systems Market. With an aging global population, the incidence of conditions that affect brain function has been rising steadily. These disorders require accurate diagnosis and continuous monitoring, fueling the demand for EEG systems that can detect and track neurological abnormalities in patients. The ongoing growth in the number of patients seeking neurological care directly supports the expansion of this market.

- The Nihon Kohden’s EEG-1200 System is a widely used and reliable piece of advanced EEG technology, utilized in major neurology centers for neurological disorder evaluation, including the diagnosis of epilepsy, cerebrovascular accidents, and sleep disorders.

Technological Advancements Enhancing EEG System Capabilities

Recent technological advancements have played a crucial role in advancing the Electroencephalography Systems Market. The development of portable and wearable EEG devices offers greater accessibility to patients, especially in home settings. These innovations improve the convenience and efficiency of neurological monitoring, particularly for conditions that require long-term observation. Advances in wireless EEG systems and cloud-based analytics further optimize data management, making it easier to capture, store, and analyze brain activity remotely.

- For Instance, The Muse S by Interaxon offers continuous streaming data for long-term monitoring, including sleep tracking, with a recording capacity of up to 10 hours per session. The original claim of a 24-hour recording capacity is incorrect, as official specifications state a maximum of 10 hours of continuous use on a single charge

Increasing Healthcare Infrastructure and Accessibility

Expanding healthcare infrastructure across the globe is helping increase the availability of EEG systems. As healthcare facilities, especially in emerging markets, are modernizing, the need for advanced diagnostic equipment like EEG systems is rising. Governments and private organizations are investing in healthcare to address the growing burden of neurological conditions. This investment not only increases the accessibility of EEG systems but also drives their adoption in both urban and rural areas where medical care has traditionally been limited.

Growing Awareness and Acceptance of EEG Technology

There is a noticeable increase in public and healthcare provider awareness regarding the importance of early diagnosis and management of neurological diseases. This growing acceptance of EEG technology encourages its widespread use in hospitals, clinics, and even at-home settings. As both patients and healthcare providers recognize the benefits of EEG systems for monitoring brain activity and diagnosing neurological disorders, the demand for these systems continues to rise, propelling market growth.

Market Trends:

Expansion of Portable and Wearable Platforms Enhancing Monitoring Capabilities

The Electroencephalography Systems Market is witnessing a shift toward portable and wearable platforms that support real‑time monitoring outside hospital settings. These systems reduce setup time, simplify electrode placement, and enable extended monitoring in ambulatory care or at home. It integrates wireless connectivity and mobile interfaces to transmit brain‑wave data to cloud or centralized repositories, enabling remote neurologist review. The trend supports chronic neurological disorder management, where continuous observation provides greater insight than episodic, inpatient testing. Markets report that portable modalities will grow at higher CAGR compared to traditional stationary systems.

- For Instance, The Cerebra EEG-based sleep system’s automated algorithm achieved 83% epoch-by-epoch agreement with manual scoring by human experts, facilitating home-based sleep monitoring for patients.

Integration of Artificial Intelligence and Advanced Analytics Driving Diagnostic Efficiency

The market also trends toward integration of artificial intelligence (AI), machine learning, and advanced analytics into EEG systems to enhance interpretation speed and accuracy. It incorporates algorithms that detect abnormal wave‑patterns, reduce artefacts, and support triage of neurological events, enabling clinicians to make more informed decisions. AI‑enhanced systems assist in reducing dependency on highly specialised technologists by automating post‑processing and reporting. These innovations address workforce constraints in neurodiagnostic services and aid scalability of EEG offerings. Research further explores interpretability and robustness of AI in EEG applications, reflecting growing emphasis on trustworthy analytics.

- For Instance, Natus autoSCORE, FDA 510(k) clearance for routine EEG, LTM, ambulatory EEG. Last data point: 30,000+ labeled EEG recordings used in training.

Market Challenges Analysis:

High Acquisition Costs and Infrastructure Barriers Hinder Broad Adoption

The Electroencephalography Systems Market faces significant challenges due to the high cost of advanced EEG devices, consumables and supporting infrastructure. Many healthcare facilities, particularly in emerging economies, find the initial investment prohibitive and must weigh competing priorities for funding. It also requires dedicated space, trained personnel and reliable power and network connectivity, which may not be available in under‑resourced settings. Limited access to such systems stalls volume deployment and delays return on investment. Restricted access in developing regions therefore constrains market penetration and slows uptake.

Complexity of Data Interpretation and Regulatory & Privacy Constraints Limit Utilisation

Clinicians using EEG systems must manage complex signal patterns, artefacts and non‑stationary data, which demand specialised training and strong analytic workflows. It imposes a reliance on expert technologists and neurologists who interpret results, thereby elevating labour costs and limiting scalability. Strict regulatory requirements around medical device approval and stringent data privacy and security obligations further complicate deployment and increase operational burden. It can deter smaller clinics from adopting EEG technology and slow implementation of new features or applications. These factors combine to create an environment where system utilisation lags behind equipment availability.

Market Opportunities:

Expansion of Home‑Monitoring and Tele‐Neurology Applications Enables New Growth

The Electroencephalography Systems Market presents substantial opportunities for vendors and healthcare providers through the expansion of home‑monitoring and tele‑neurology applications. Remote EEG systems allow clinicians to monitor patients outside traditional hospital settings, reducing patient travel and freeing up hospital resources. It enables continuous observation of chronic neurological conditions, which improves patient outcomes and lowers overall healthcare costs. Growing adoption of telehealth platforms and reimbursement policy shifts support increased deployment of EEG systems in home environments. Equipment manufacturers can capitalise on this shift by offering user‑friendly, portable devices designed for remote use. Health systems that integrate these solutions into care pathways can extend neurologic diagnostics into underserved or rural regions.

Leveraging AI‑Driven Solutions and Brain‑Computer Interface Innovations Strengthens Market Prospect

Another major opportunity lies in leveraging artificial intelligence (AI) and brain‑computer interface (BCI) technologies to elevate system capabilities and open new applications. The market can benefit from advanced algorithms that assist in detecting subtle brainwave abnormalities, thus enhancing diagnostic accuracy and workflow efficiency. It allows providers to offer new services in neurorehabilitation, cognitive assessment and sleep‑disorder monitoring. Vendors that integrate AI and BCI functions into their platforms will differentiate themselves and address unmet clinical demands. Research and investment momentum in neurotechnology also signals potential for novel product categories and collaborations. It positions the market to expand beyond traditional use cases and capture value in emerging therapeutic and consumer‑health segments.

Market Segmentation Analysis:

By Product

The market divides into equipment and accessories categories. Equipment includes high‑channel EEG systems such as 32‑channel, 40‑channel and multi‑channel configurations, which command growing interest because they deliver more detailed spatial brain‑activity data. The accessories segment covers electrodes, caps, amplifiers and software modules that support device operation and signal processing. Demand for accessories expands as clinicians upgrade existing systems rather than replace entire platforms. It strengthens overall market volume and creates recurring revenue streams for manufacturers.

- For Instance, Emotiv’s FLEX 2 system is a 32-channel wireless EEG head cap with a sampling rate of 256 Hz, enabling higher-resolution real-time brain data capture for research and clinical settings. While the device internally samples at 2048 Hz, the data provided is at 256 samples per second.

By Application

Application use cases include disease diagnosis, sleep monitoring, anesthesia monitoring and other neurology‑related processes. The disease diagnosis segment takes a leading position because EEG remains a staple for identifying epilepsy, Alzheimer’s and other brain disorders. Growth in sleep disorder prevalence and longer‑term ambulatory monitoring offers additional applications for systems outside the traditional hospital environment. It encourages diversification of coverage beyond inpatient neurology units. Increased focus on brain‑computer interfaces and neurofeedback also opens novel application frontiers.

- For Instance, Masimo pulse oximetry technology involving 49 children with Down Syndrome to screen the risk of obstructive sleep apnea (OSA) demonstrated a sensitivity of 92% for identifying those at high risk for OSA, based on specific oxygen desaturation index (ODI) parameters.

By End‑Use

End‑use segments comprise hospitals, diagnostic centres, ambulatory surgical clinics, research institutes and home‑care settings. Hospitals hold the largest share due to their extensive use of EEG systems in neurology departments and emergency care. Diagnostic centres and clinics follow, offering EEG services in outpatient settings. The home‑care and ambulatory monitoring segment shows fastest growth thanks to portable system adoption and remote‑monitoring trends. It gives providers new models for delivering neurodiagnostic services beyond conventional infrastructure.

Segmentations:

By Product

- EEG Equipment

- EEG Accessories

By Application

- Disease Diagnosis

- Sleep Monitoring

- Anesthesia Monitoring

- Brain‑Computer Interface & Neurofeedback

- Other Applications

By End‑Use

- Hospitals

- Diagnostic Centres

- Ambulatory Surgical Centres & Clinics

- Research & Academic Institutions

- Home‑Care Settings

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America Region

Market share in North America stands at approximately 35.5% of the global market. The Electroencephalography Systems Market benefits from advanced healthcare infrastructure, high adoption of diagnostic technologies, and robust reimbursement policies. It draws strength from well-established neurology departments, extensive clinical research, and significant incidence of epilepsy and other neurological disorders. It also gains from a strong presence of key device manufacturers and a solid distribution network across medical facilities. Demand in this region remains high, driven by both hospital‑based use and outpatient neurology services. Manufacturers often target this market first due to relatively smoother regulatory approval pathways and greater willingness among providers to invest in cutting‑edge diagnostic equipment.

Europe Region

Market share in Europe is around 26% of the global share. The region’s demand in the Electroencephalography Systems Market stems from an aging population, rising prevalence of neurodegenerative diseases, and governmental support for neurological health initiatives. Providers in the region upgrade EEG systems to meet higher standards of data quality and connectivity, including remote monitoring and tele‑neurology modules. It experiences incremental growth due to increasing private‑clinic activity and research institution investments in neurotechnology. Regulatory complexity and varied reimbursement frameworks across countries pose hurdles, yet the overall trend supports gradual expansion of EEG system deployment.

Asia Pacific Region

Market share in Asia Pacific is projected to grow strongly, currently estimated between 20‑25% of the global market. The Electroencephalography Systems Market sees rising opportunity in countries such as China and India, driven by increasing healthcare spending, expanding diagnostic infrastructure, and growing awareness of neurological disorders. It also benefits from the adoption of portable and wearable EEG systems suitable for home‑care and satellite clinics, which addresses resource constraints in rural zones. Local manufacturers and international players introduce cost‑effective solutions to meet price‑sensitive demand. Challenges include variable regulatory frameworks and reimbursement uncertainty, but the growth trajectory remains positive given the large population base and unmet clinical needs.

Key Player Analysis:

- Natus Medical, Inc.

- Medtronic

- Nihon Kohden America, Inc.

- Brain Products GmbH

- Neurosoft

- Compumedics Ltd.

- Electrical Geodesics, Inc.

- ANT Neuro

- Lifelines neuro

- Mitsar

- Micromed

- Cadwell Laboratories, Inc.

- EBNeuro

- Magstim EGI

- Emotiv

Competitive Analysis:

The competitive landscape for the Electroencephalography Systems Market features several established players such as Natus Medical, Inc., Medtronic, Nihon Kohden America, Inc., Brain Products GmbH, Neurosoft, Compumedics Ltd., and Electrical Geodesics, Inc.. In this group, Natus Medical stands out for its broad EEG portfolio covering routine, ambulatory and ICU applications, backed by strong software integration and global support infrastructure.

Each competitor differentiates via specific strengths: Medtronic leverages its global scale and neurological therapy ecosystem, whereas Nihon Kohden capitalises on deep heritage in neurodiagnostic equipment. Brain Products focuses on high‑end research applications, Neurosoft emphasises cost‑effective systems for emerging markets, Compumedics targets both clinical and research segments with high‑channel‑count solutions, and Electrical Geodesics delivers dense‑array EEG innovations for advanced neuroimaging.

It becomes crucial for companies to maintain technological leadership, expand regional reach and secure reimbursement pathways. Firms that can integrate cloud analytics, offer portable/home‑monitoring solutions and simplify workflows will gain competitive advantage. Price pressure and regulatory complexity demand agile strategy and strong value proposition in this market.

Recent Developments:

- In September, 2025, Natus Medical acquired Holberg EEG to integrate advanced AI-powered EEG technology into its neurodiagnostics portfolio.

- In January, 2025, Medtronic entered an exclusive U.S. distribution agreement for Contego’s vascular revascularization products, with an option to acquire the company in the future.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage:

The research report offers an in-depth analysis based on Product, Application, End‑Use and Region. It details leading Market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current Market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven Market expansion in recent years. The report also explores Market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on Market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the Market.

Future Outlook:

- Home‑care and remote monitoring adoption will increase significantly, enabling neurologic diagnostics beyond hospital settings.

- Wearable and portable EEG devices will gain traction, offering mobility and convenience for both patients and providers.

- Artificial intelligence and machine‑learning integration will enhance signal interpretation, reduce manual workload and improve diagnostic accuracy.

- Brain‑computer interface (BCI) applications will grow, driving new use cases in rehabilitation, neurofeedback and assistive technologies.

- Emerging markets will attract investment thanks to rising healthcare infrastructure, greater neurological disease awareness and cost‑effective device solutions.

- Cloud‑connected EEG platforms will enable centralized data access, multi‑center collaboration and remote expert review.

- Customizable and modular EEG systems will allow providers to scale up or specialise according to clinical requirements.

- Partnerships between device manufacturers, software firms and clinical institutions will accelerate innovation and broaden market reach.

- Regulatory clarity and improved reimbursement pathways will support wider adoption and faster deployment of advanced EEG solutions.

- Consumer‑health and wellness segments will adopt simplified EEG tools for sleep tracking, mental‑wellness monitoring and cognitive assessment.