Fresh vegetables Market Overview:

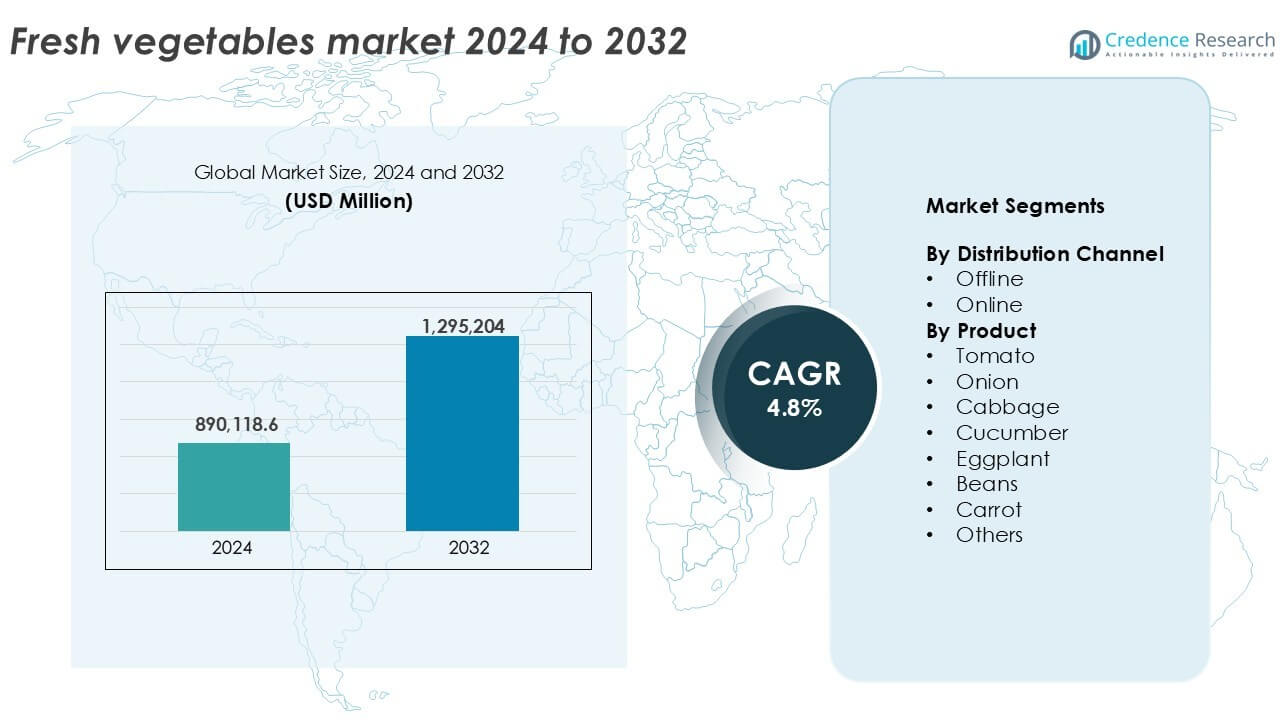

Fresh vegetables market size was valued at USD 890,118.6 million in 2024 and is anticipated to reach USD 1,295,204 million by 2032, at a CAGR of 4.8% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Fresh vegetables Market Size 2024 |

USD 890,118.6 million |

| Fresh vegetables Market, CAGR |

4.8% |

| Fresh vegetables Market Size 2032 |

USD 1,295,204 million |

Fresh vegetables Market Insights

- Rising health awareness and the shift toward plant-based diets are driving global demand for fresh vegetables across both developed and emerging regions.

- Organic and pesticide-free vegetables, along with smart farming practices, are key trends reshaping product offerings and production methods.

- The market remains fragmented, with major players like Dole Food Company, Fresh Del Monte, and C.H. Robinson focusing on supply chain efficiency and sustainability.

- Asia-Pacific leads with over 40% share due to high domestic consumption, while Europe (22%) and North America (18%) follow; among products, tomatoes hold nearly 20% share, and offline channels dominate distribution with over 80% contribution.

Fresh vegetables Market Segmentation Analysis:

By Distribution Channel

The offline segment dominates the fresh vegetables market, accounting for over 80% of total revenue in 2024. Traditional retail formats, including supermarkets, hypermarkets, and local vendors, maintain strong consumer trust due to product freshness and immediate availability. In many developing regions, local wet markets remain the preferred choice for daily fresh produce. Consumers value the ability to inspect vegetables physically before purchase. Offline channels also benefit from established cold-chain logistics and bulk purchase options, particularly for institutional buyers like restaurants and caterers. This segment continues to thrive on habitual buying behavior and ease of access. The online segment is gaining traction, driven by rising internet penetration and shifting consumer preferences for convenience. It accounted for a smaller share but posted the fastest growth rate. Urban consumers increasingly opt for mobile grocery apps and e-commerce platforms for weekly vegetable deliveries. Subscription-based fresh produce services and same-day delivery models enhance appeal. The segment is further supported by digital payment integration and targeted promotions by online retailers. Growing demand for contactless shopping post-pandemic continues to support online growth.

- For instance, Whole Foods Market operates 500+ stores globally with fresh produce sections where consumers inspect vegetables in person.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Product

Tomato emerged as the leading product segment, capturing nearly 20% of the fresh vegetables market share in 2024. High consumption in both raw and cooked forms drives steady demand across regions. Tomatoes are essential in multiple cuisines and processed food sectors. Their short harvesting cycle and year-round availability boost volume production. Export potential further adds to its dominance. Onion follows closely, driven by its staple use in daily cooking, especially in Asian and Middle Eastern countries. Price volatility in onion supply often influences national food inflation trends. Other notable product segments include cabbage, cucumber, and beans, each with significant regional consumption patterns. Carrot and eggplant maintain consistent demand due to their wide usage in both domestic and commercial kitchens. The “Others” category includes seasonal and regional varieties that contribute to market diversity. Innovation in greenhouse farming and vertical cultivation supports consistent supply across multiple vegetable types. Climate-resilient seed development and government support for horticulture continue to fuel production across all categories.

- For instance, Onion follows closely in production prominence, with global onion and shallot output exceeding 110 million tonnes in 2022, underscoring its staple role in diets worldwide.

Key Growth Drivers

Rising Global Health Awareness and Plant-Based Diets

The shift towards healthier lifestyles is significantly driving demand for fresh vegetables. Consumers are increasingly adopting plant-based diets for weight management, disease prevention, and overall wellness. Vegetables are rich in vitamins, minerals, and antioxidants, aligning with growing consumer focus on natural nutrition. The expansion of veganism and vegetarianism across Western and Asian markets fuels steady volume growth. Food service providers and meal-kit companies now prominently include fresh vegetable offerings in their menus, amplifying visibility and consumption. This trend is also reinforced by government campaigns promoting daily vegetable intake to combat non-communicable diseases. Schools, hospitals, and corporate cafeterias are integrating fresh produce into meal plans, further expanding institutional demand.

- For instance, campaigns such as National Fruits & Veggies Month in the U.S. promote daily vegetable intake and educate on health benefits through outreach in stores, schools, and social media.

Expansion of Organized Retail and Cold Chain Infrastructure

The fresh vegetables market is benefiting from the rise of organized retail and improved cold chain systems. Supermarkets and hypermarkets are expanding aggressively in urban and semi-urban regions, offering cleaner, better-packaged, and visually appealing fresh produce sections. These modern retail formats enable efficient inventory management and reduce post-harvest losses. In parallel, government and private investments in cold storage, refrigerated transport, and supply chain digitization have strengthened distribution efficiency. Enhanced shelf-life and reduced spoilage risks allow year-round availability of seasonal vegetables across wider geographies. These developments are particularly impactful in emerging economies, were supply chain gaps earlier limited market potential.

- For instance, modern cold chain networks reduce spoilage by maintaining controlled temperatures from farm to retail, protecting quality and extending shelf life.

Urbanization and Growth in Middle-Class Disposable Income

Urbanization is reshaping consumption patterns, driving higher demand for convenience-focused and high-quality fresh produce. A growing urban middle class with rising disposable incomes is willing to pay premium prices for hygienically packed, pesticide-free, and organic vegetables. Demand is also increasing for exotic and imported vegetables, supported by international trade liberalization and diversified diets. Dual-income households seek ready-to-cook options, including pre-cut and pre-washed vegetables. Retailers respond with value-added offerings to meet time-constrained urban lifestyles. This shift fuels revenue growth and opens premium product segments. In countries like China, India, and Indonesia, rapid urban growth directly boosts consumption and supports robust retail expansion.

Key Trends & Opportunities

Growth of Organic and Pesticide-Free Vegetables

Consumer preference is steadily shifting towards chemical-free and organic produce due to concerns over food safety and environmental sustainability. Organic vegetables are gaining shelf space in both offline and online retail channels. Certifications, traceability solutions, and QR-code labeling improve consumer confidence. Startups and agri-tech companies are entering the space with farm-to-fork models and direct-to-consumer platforms. Urban farming, rooftop gardens, and hydroponics are enabling pesticide-free production in city environments. Governments are promoting organic farming through subsidies and training programs. As consumer awareness deepens, the organic vegetable segment is expected to become a mainstream growth opportunity across multiple geographies.

- For instance, Gotham Greens grows leafy greens up to 30 times more per acre than traditional farming via controlled, pesticide‑free greenhouses.

Rising Adoption of Smart Farming and Agri-Tech Solutions

Technology adoption is transforming vegetable farming practices, creating long-term market opportunities. Precision agriculture, automated irrigation, drone surveillance, and AI-based yield forecasting tools are improving productivity and reducing waste. Controlled environment agriculture (CEA) systems like greenhouses and vertical farms are gaining traction in urban areas, ensuring consistent supply and quality. Agri-tech startups offer real-time crop monitoring and supply chain integration services that enhance farmer profitability and buyer confidence. Government support for digital agriculture initiatives, especially in Asia-Pacific and Europe, further boosts adoption. These innovations also enable better forecasting and supply management, addressing demand surges and minimizing seasonal fluctuations.

Key Challenges

High Post-Harvest Losses and Supply Chain Inefficiencies

A major challenge in the fresh vegetables market is the high level of post-harvest losses due to inadequate storage and transportation. Perishable nature of vegetables makes them vulnerable to spoilage during handling, particularly in hot and humid climates. Many developing regions lack cold storage facilities and efficient logistics, resulting in up to 30–40% produce loss before reaching the consumer. Inefficiencies in aggregation, sorting, and packaging further erode value. Farmers often sell at low prices due to limited access to market infrastructure. Despite advancements in cold chain solutions, adoption remains limited in rural belts. These systemic gaps hinder profit margins and limit market expansion.

Price Volatility Due to Climatic and Input Cost Factors

Fresh vegetable prices are highly sensitive to climatic conditions, pest infestations, and shifts in input costs like seeds, fertilizers, and labor. Erratic monsoons, droughts, floods, and temperature fluctuations affect planting and harvesting cycles, disrupting supply consistency. Price instability makes demand forecasting and inventory planning difficult for retailers and suppliers. Farmers face income uncertainty, leading to cautious production behavior and market exit risks. Input cost inflation further impacts small and marginal farmers, who struggle with shrinking margins. This volatility affects both producer stability and consumer affordability, constraining long-term growth prospects in several regional markets.

Regional Analysis

North America

North America held over 18% market share in the global fresh vegetables market in 2024. The U.S. remains the primary contributor, driven by high per capita consumption, widespread use in foodservice, and strong demand for organic produce. Increasing awareness of healthy eating and the rise of plant-based diets support stable demand across retail and institutional channels. Supermarkets dominate distribution, while e-commerce grocery delivery gains traction in urban areas. Cold chain infrastructure and vertical farming technology adoption are also rising. Canada and Mexico contribute steadily through exports and regional trade under frameworks like USMCA.

Europe

Europe accounted for approximately 22% of the fresh vegetables market in 2024, led by countries such as Germany, France, Italy, and Spain. Consumers in the region favor locally sourced, seasonal, and organic vegetables, supported by strong regulatory standards and sustainability-driven policies. The market benefits from widespread retail penetration and efficient supply chains. Demand for pesticide-free produce and packaged fresh-cut vegetables is growing. Eastern European countries also show rising production capacity. Government subsidies and EU-backed farming initiatives further promote vegetable cultivation. Urban rooftop farms and indoor growing systems are expanding, enhancing supply consistency across the region.

Asia-Pacific

Asia-Pacific dominated the global fresh vegetables market with over 40% share in 2024, driven by large-scale production and consumption in China and India. Dietary staples in many Asian countries rely heavily on vegetables, both raw and cooked. Rapid urbanization, rising disposable income, and expanding middle-class population continue to boost demand. Traditional markets dominate, but modern trade channels and online grocery services are growing. Government support for horticulture, technological farming practices, and investment in rural cold storage improve market efficiency. Southeast Asia and Japan also show steady demand, with imports of high-value or off-season produce becoming more common.

Latin America

Latin America held nearly 8% of the global fresh vegetables market in 2024, supported by year-round growing conditions and strong export capacity. Brazil and Mexico are key producers, catering to both domestic consumption and foreign markets, especially the U.S. The region benefits from fertile land, low-cost labor, and increasing investment in irrigation and greenhouse farming. Domestic consumption grows steadily, aided by urbanization and rising health awareness. However, challenges such as infrastructure gaps and price volatility limit growth. Supermarkets gain market share, but traditional open markets remain dominant across rural and peri-urban areas.

Middle East & Africa

The Middle East & Africa region accounted for around 6% market share in 2024. Consumption is increasing due to urban population growth, rising food security concerns, and government-backed agricultural diversification. Countries like Egypt, South Africa, and the UAE invest in greenhouse farming, hydroponics, and controlled environment agriculture to overcome water scarcity and arid conditions. Imports meet a large part of regional demand, especially in the Gulf Cooperation Council (GCC) countries. Retail and foodservice channels grow steadily, particularly in urban centers. However, limited cold chain infrastructure and fragmented local production still pose market constraints.

Fresh vegetables Market Segmentations:

By Distribution Channel

By Product

- Tomato

- Onion

- Cabbage

- Cucumber

- Eggplant

- Beans

- Carrot

- Others

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The fresh vegetables market is highly fragmented, featuring a blend of global agribusiness giants, regional exporters, and vertically integrated growers. Leading players like Dole Food Company, Fresh Del Monte, and C.H. Robinson Worldwide, Inc. leverage extensive distribution networks and supply chain infrastructure to maintain consistent quality and year-round availability. These companies focus on sustainability, traceability, and pesticide-free offerings to align with evolving consumer demands. Mid-sized firms such as Tanimura & Antle and Keelings specialize in product innovation and efficient farm-to-retail models. Regional players including BelOrta and Goknur Gida strengthen market presence through export-oriented strategies. Companies like Fruitable Fresh Sdn Bhd. and Mirak Group cater to rising demand in Asia and the Middle East with greenhouse cultivation and hydroponic farming. Investments in cold storage, smart logistics, and digital integration are central to competitiveness. Strategic partnerships, certification programs, and private-label supply agreements continue shaping the competitive dynamics across both mature and emerging markets.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Fruitable Fresh Sdn Bhd.

- BelOrta

- Fresh Del Monte

- Tanimura & Antle

- H. Robinson Worldwide, Inc.

- Global Fresh Trading FZE

- Keelings

- FreshPoint Inc.

- Mirak Group

- Goknur Gida

- Dole Food Company, Inc.

Recent Developments

- In April 2025, AI-powered tech enabler GrubMarket completed the acquisition of Nogales-based Delta Fresh Produce, a leading distributor specialising in tomatoes, cucumbers, peppers, grapes, watermelons, and various other fresh produce commodities sourced from Mexico. Delta Fresh manages an extensive farming and distribution network across Mexico, including over 900 acres of open-field production, 1,400 acres of indoor production, and state-of-the-art packing facilities across Baja, Sonora, Sinaloa, and Central Mexico.

- In February 2025, Coupang launched its Premium Fresh service for superior quality fresh foods in Korea. “Premium Fresh” offers over 500 products across 12 categories, including fruits, seafood, vegetables, meat, eggs, and dairy products. Fruits, seafood, and vegetables that meet Coupang’s premium quality standards in terms of quality and size will bear the “Premium Fresh” label, ensuring the highest quality for customers through a stringent inspection process.

- In February 2024, Wholesale Produce Supply LLC (WPS Fresh), a fresh produce logistics and inventory management solutions provider to grocery wholesalers, foodservice distributors, and other customers, acquired the assets of G.O. Corporation, a processor of fresh-cut produce. The company performs value-added services such as ripening, grading, fresh-cutting, washing, sorting, and packaging.

Report Coverage

The research report offers an in-depth analysis based on Distribution Channel, Product and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for organic and pesticide-free vegetables will continue rising across global urban markets.

- Online grocery platforms will gain a larger share in fresh vegetable distribution.

- Smart farming techniques like hydroponics and vertical farming will expand production capacity.

- Cold chain infrastructure investments will improve shelf life and reduce post-harvest losses.

- Health-conscious consumers will drive demand for value-added, ready-to-cook vegetable products.

- Regional trade and cross-border vegetable exports will grow with improved logistics.

- Government support for sustainable agriculture will boost domestic production levels.

- Retailers will increase private-label vegetable offerings to enhance profit margins.

- Climate-resilient crop varieties will be adopted to manage weather-related supply risks.

- Strategic partnerships and farm-to-retail integration will strengthen competitive positioning.