Market Overview:

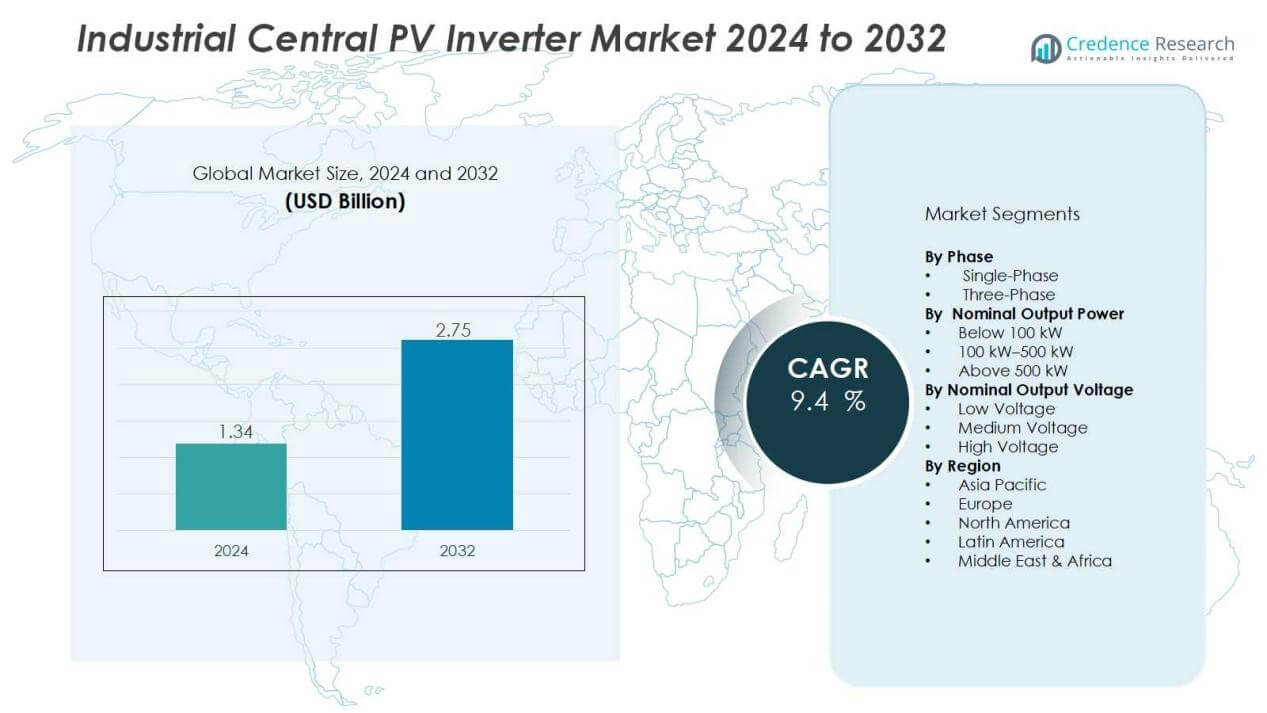

The industrial central pv inverter market size was valued at USD 1.34 billion in 2024 and is anticipated to reach USD 2.75 billion by 2032, at a CAGR of 9.4% during the forecast period (2024-2032).

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Industrial Central PV Inverter Market Size 2024 |

USD 1.34 Billion |

| Industrial Central PV Inverter Market, CAGR |

9.4% |

| Industrial Central PV Inverter Market Size 2032 |

USD 2.75 Billion |

Key drivers include the growing emphasis on decarbonization and renewable energy targets across major economies. Industrial central PV inverters offer high efficiency, grid stability, and cost advantages, making them critical for large-scale solar projects. Advances in digital monitoring, smart grid compatibility, and energy storage integration further enhance their appeal. In addition, supportive policies, tax incentives, and a decline in the levelized cost of solar energy are accelerating investments in industrial-scale photovoltaic installations.

Regionally, Asia-Pacific dominates the market, led by China and India, which are aggressively expanding renewable capacity. Europe follows, supported by strong regulatory frameworks and ambitious solar adoption goals. North America continues to invest in utility-scale projects, driven by favorable state-level incentives and increasing demand for clean energy. Emerging regions such as the Middle East, Latin America, and Africa are also gaining traction with rising solar infrastructure investments and industrial energy diversification.

Market Insights:

- The industrial central PV inverter market was valued at USD 1.34 billion in 2024 and is projected to reach USD 2.75 billion by 2032, growing at a CAGR of 9.4%.

- Rising commitments to renewable energy and decarbonization targets are driving large-scale solar adoption globally.

- High-capacity performance and cost efficiency of central inverters make them the preferred choice for utility-scale projects.

- Advancements in digital monitoring, smart grid compatibility, and fault detection enhance efficiency and reliability.

- Government incentives, tax benefits, and supportive policies continue to accelerate investment in industrial solar infrastructure.

- High upfront costs, complex installation, and maintenance challenges remain significant barriers to wider adoption.

- Asia-Pacific held 46% market share in 2024, followed by Europe at 28% and North America at 19%, with all regions showing strong renewable energy momentum.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Rising Global Focus on Renewable Energy and Decarbonization:

The industrial central PV inverter market benefits directly from rising commitments to renewable energy. Governments and industries are setting ambitious carbon neutrality goals, driving investment in large-scale solar projects. Central PV inverters play a vital role in integrating these projects into the grid with efficiency and stability. It continues to gain traction as industrial players seek reliable solutions for expanding solar capacity.

- For instance, Ingeteam provided 149 INGECON SUN 3Power Series C liquid-cooled central PV inverters for the 640 MWdc Parliament Solar project in Texas, which is expected to produce around 1,100 GWh of clean electricity annually, highlighting the scalability and reliability of modern central PV inverters.

Cost Efficiency and High-Capacity Performance of Central Inverters:

Industrial central PV inverters deliver superior performance for large installations by managing high power output efficiently. Their design reduces the overall balance of system costs, making them a preferred choice for utility-scale projects. These systems enhance project viability by minimizing operational expenses while ensuring consistent performance. The industrial central PV inverter market gains momentum from their ability to optimize large-scale solar operations effectively.

- For instance, Huawei’s SUN2000-215KTL-H3 string inverter model, used in utility-scale solar parks, provides a rated active power of 200 kW with three independent MPPT trackers, maximizing energy harvest and operational efficiency for large solar installations.

Technological Advancements in Grid Integration and Monitoring:

Advancements in digital control, real-time monitoring, and grid-support features strengthen the role of central PV inverters. Modern systems now integrate smart grid compatibility and advanced fault detection to improve reliability. This innovation enhances operational safety, reduces downtime, and ensures compliance with evolving grid codes. It positions central inverters as indispensable in modern energy ecosystems that demand both performance and intelligence.

Supportive Policies, Incentives, and Investment in Solar Infrastructure:

Government incentives, renewable energy targets, and declining solar energy costs encourage large-scale deployment of photovoltaic systems. Subsidies, feed-in tariffs, and tax benefits create a favorable environment for utility and industrial projects. The industrial central PV inverter market benefits from this strong policy framework, attracting global investment. Expansion of solar parks and infrastructure projects further fuels demand for high-capacity central inverters worldwide.

Market Trends:

Market Trends:

Growing Integration of Digital Technologies and Smart Grid Compatibility:

The industrial central PV inverter market is witnessing a shift toward advanced digital integration and smart grid compatibility. Manufacturers are embedding IoT, AI-driven analytics, and remote monitoring capabilities to enhance system performance and reduce downtime. Real-time data collection and predictive maintenance tools enable operators to identify potential issues early and maintain operational efficiency. It is also evolving to meet stricter grid codes by supporting features such as voltage regulation, frequency response, and reactive power control. These capabilities ensure grid stability while enabling large-scale solar projects to contribute to reliable energy distribution. Growing demand for intelligent energy management platforms continues to push central inverter innovation in this direction.

- For instance, Huawei’s SUN2000 Series central inverters integrate AI-powered fault detection and multi-MPPT tracking, enabling predictive maintenance with failure prediction accuracy reaching 85%, which helps reduce downtime significantly

Expansion of Utility-Scale Projects and Hybrid Energy Systems:

Large-scale solar farms and hybrid renewable projects are driving significant momentum for the industrial central PV inverter market. Central inverters provide the efficiency and high power handling required for multi-megawatt installations, making them a preferred choice in utility-scale deployments. It is also gaining relevance in hybrid systems that combine solar with wind or energy storage, ensuring consistent output and grid resilience. Global investment in renewable infrastructure has expanded, particularly in Asia-Pacific, the Middle East, and Latin America, where industrial-scale solar adoption is accelerating. Vendors are responding by developing modular, high-capacity designs that support scalable growth in these projects. Rising demand for hybrid and utility-scale solutions underscores the central inverter’s role in the future of industrial solar power.

- For Instance, In 2014, the 170 MW (AC) Centinela Solar Energy Facility in Imperial County, California, began commercial operation. The project was developed by LS Power, with Fluor Corporation as the EPC contractor.

Market Challenges Analysis:

High Initial Costs and Complex Installation Requirements:

The industrial central PV inverter market faces a challenge from its high upfront costs and complex installation needs. Large-capacity inverters demand significant capital investment, which can deter small and mid-sized industrial players. Installation often requires specialized expertise, raising project timelines and overall expenses. It also demands reliable infrastructure, such as advanced cooling systems and protective enclosures, to function efficiently. These factors make central inverters less attractive compared to modular string inverters in certain cases. The financial burden remains a key obstacle, particularly in emerging markets with limited funding support.

Maintenance Complexity and Grid Integration Barriers:

Maintenance and operational complexity also challenge the industrial central PV inverter market. Central inverters handle large volumes of power, making them vulnerable to higher downtime risks in case of failure. Repairs often involve costly replacements and extended service interruptions, affecting project returns. It must also adapt to evolving grid codes, voltage standards, and integration requirements, which vary across regions. This adds compliance challenges for manufacturers and project developers. Dependence on stable policy support and evolving energy regulations further influences adoption rates. These challenges highlight the need for innovation in design and service strategies to sustain growth.

Market Opportunities:

Expansion of Utility-Scale Solar Projects and Energy Infrastructure:

The industrial central PV inverter market has strong opportunities in the growing number of utility-scale solar projects worldwide. Governments and private investors are accelerating renewable energy capacity to meet ambitious carbon reduction targets. Central inverters, with their high efficiency and ability to manage multi-megawatt systems, are ideally suited for these projects. It benefits from large solar park developments in Asia-Pacific, the Middle East, and Latin America, where industrial energy demand is rapidly increasing. Expansion of supportive policies and financing models further drives adoption in these regions. The scale of infrastructure investment ensures long-term demand for central inverters in large industrial applications.

Integration with Energy Storage and Hybrid Renewable Systems:

Hybrid energy systems combining solar, wind, and storage create new avenues for the industrial central PV inverter market. Central inverters that integrate seamlessly with energy storage can deliver stable output and enhance grid reliability. It becomes a vital solution for regions with intermittent energy supply, enabling higher renewable penetration. Growing demand for microgrids, industrial backup solutions, and grid resilience creates additional prospects. Technological advancements in modular designs and smart control also open pathways for innovative product offerings. These opportunities position central inverters as central to the next phase of global renewable adoption.

Market Segmentation Analysis:

By Phase:

The industrial central PV inverter market is primarily segmented into single-phase and three-phase systems. Three-phase inverters dominate due to their ability to handle higher loads and deliver stable power for utility-scale and industrial projects. Single-phase models find use in smaller installations, but large solar farms and industrial operations rely on the efficiency of three-phase systems. It benefits from the scalability and reliability these inverters provide, aligning with rising demand for large-capacity projects.

- For Instance, For large-scale solar installations, Fronius offers high-power three-phase inverters like the Tauro series, with models such as the Tauro ECO supporting power outputs up to 100 kW.

By Nominal Output Power:

Segmentation by nominal output power highlights the growing preference for high-capacity inverters exceeding 500 kW. These systems are widely deployed in utility-scale solar parks and industrial applications requiring robust performance. Mid-range units between 100 kW and 500 kW maintain demand in medium-sized projects. It is this wide capacity coverage that supports diverse energy requirements across industries. Increasing investment in large-scale renewable projects continues to favor higher power-rated inverters.

- For instance, in July 2024, Sungrow’s SG3150HV-MV central inverter delivered a nominal output power of 3 150 kW at the Ashalim solar PV plant in Israel.

By Nominal Output Voltage:

By nominal output voltage, the market spans low-voltage, medium-voltage, and high-voltage categories. Medium- and high-voltage inverters dominate large-scale applications due to their ability to connect directly with grids and reduce transmission losses. Low-voltage systems remain relevant for smaller industrial setups with limited capacity needs. It gains strong growth from the shift toward higher voltage solutions that enhance efficiency and reduce infrastructure costs. This segmentation reflects the market’s alignment with grid modernization and industrial energy requirements.

Segmentations:

By Phase:

By Nominal Output Power:

- Below 100 kW

- 100 kW–500 kW

- Above 500 kW

By Nominal Output Voltage:

- Low Voltage

- Medium Voltage

- High Voltage

By Region:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis:

Asia-Pacific :

Asia-Pacific accounted for 46% market share in 2024, making it the largest regional contributor. The region benefits from massive solar capacity additions in China, India, and Southeast Asia. The industrial central PV inverter market gains momentum here due to supportive government policies, declining solar energy costs, and rising industrial demand. It is further strengthened by large-scale solar park developments and ambitious renewable energy targets. Expansion of utility-scale projects and manufacturing hubs ensures sustained demand for central inverters. Strong policy-driven investments keep Asia-Pacific at the forefront of global adoption.

Europe:

Europe captured 28% market share in 2024, supported by strict carbon reduction goals and strong regulatory frameworks. The industrial central PV inverter market in the region benefits from established infrastructure, grid modernization, and supportive incentives. It is driven by rapid integration of renewable energy into national grids and emphasis on sustainability. Countries such as Germany, Spain, and Italy lead utility-scale solar adoption, creating steady demand for central inverters. Rising interest in hybrid renewable projects with storage integration further adds to growth prospects. The regional focus on decarbonization and energy independence secures Europe’s stable position.

North America:

North America recorded 19% market share in 2024, making it one of the fastest-growing markets. The industrial central PV inverter market is driven by rising demand for clean energy across the United States and Canada. It benefits from federal tax incentives, state-level renewable portfolio standards, and large corporate solar investments. The region is witnessing significant growth in utility-scale solar farms, particularly in states with strong solar resources. Technological innovations and grid modernization efforts support greater adoption of central inverters. Expanding renewable infrastructure and favorable investment climate ensure continued growth in North America.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Delta Electronics, Inc

- Emerson Electric Co.

- Eaton

- Fimer Group

- Omron Corporation

- Power Electronics S.L.

- Hitachi Hi-Rel Power Electronics Private Limited

- SMA Solar Technology AG

- Siemens Energy

- SunPower Corporation

Competitive Analysis:

The industrial central PV inverter market is highly competitive with global players driving innovation and scale. Key companies include Delta Electronics, Inc., Emerson Electric Co., Eaton, Fimer Group, Omron Corporation, and Power Electronics S.L. These firms compete on efficiency, reliability, and advanced grid-support features that align with the needs of utility-scale solar projects. It is characterized by rapid adoption of digital monitoring, modular designs, and higher power ratings to meet diverse industrial demands. Strategic initiatives such as product launches, partnerships, and expansion into emerging markets strengthen their positions. Competition also focuses on service models, ensuring reduced downtime and improved lifecycle management for large solar installations. This dynamic environment pushes companies to prioritize technological leadership, cost efficiency, and compliance with evolving grid standards.

Recent Developments:

- In June 2025, Eaton and Siemens Energy joined forces to accelerate the provision of power and technology solutions for large-scale data centers.

- In January 2025, Fimer Group was officially acquired by MA Solar Italy Limited, affiliated with the McLaren Applied Group, completing an important restructuring and enabling over €50 million investment in growth and innovation.

Report Coverage:

The research report offers an in-depth analysis based on Phase, Nominal Output Power, Nominal Output Voltage and Region. It details leading Market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current Market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven Market expansion in recent years. The report also explores Market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on Market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the Market.

Future Outlook:

- The industrial central PV inverter market will see rising adoption from growing utility-scale solar projects worldwide.

- It will benefit from government-backed renewable targets and financing models that support large solar infrastructure.

- Manufacturers will focus on digital integration, including IoT and AI, to enhance efficiency and monitoring.

- Grid-supportive features such as voltage control, frequency regulation, and reactive power management will become standard.

- The market will expand through hybrid renewable systems that integrate solar, wind, and energy storage.

- It will gain from rapid investments in solar parks across Asia-Pacific, the Middle East, and Latin America.

- North America and Europe will maintain steady demand, supported by policy incentives and grid modernization.

- Vendors will invest in modular and scalable central inverter designs to meet diverse project requirements.

- It will face ongoing challenges in installation complexity and maintenance, driving innovation in service models.

- The competitive landscape will evolve with mergers, partnerships, and product launches focused on efficiency and reliability.