| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Industrial Drum Market Size 2024 |

USD 13,124.5 million |

| Industrial Drum Market, CAGR |

5.73% |

| Industrial Drum Market Size 2032 |

USD 20,452.1 million |

Market Overview:

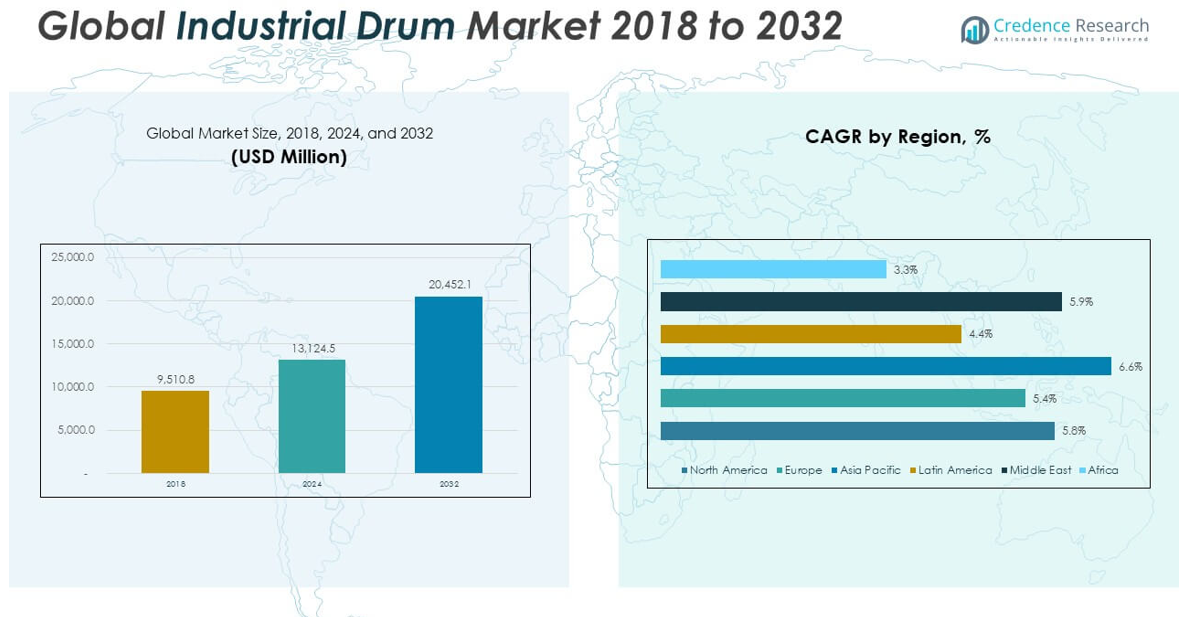

The Global Industrial Drum Market size was valued at USD 9,510.8 million in 2018 to USD 13,124.5 million in 2024 and is anticipated to reach USD 20,452.1 million by 2032, at a CAGR of 5.73% during the forecast period.

Several key drivers are fueling the growth of the industrial drum market. Chief among them is the rapid industrialization occurring in emerging economies, which is leading to increased consumption of chemicals, lubricants, and processed foods—products that require durable and compliant packaging. The rising emphasis on safety and sustainability in packaging is also contributing to market expansion. Companies are adopting environmentally friendly materials such as recyclable plastics and fiber drums, as well as reusable steel drums, to align with global regulatory frameworks and reduce their carbon footprint. Technological advancements have further enhanced the appeal of modern drums. Manufacturers are incorporating features like RFID tracking, smart sensors, and corrosion-resistant coatings to improve supply chain transparency, ensure safe transportation of hazardous materials, and optimize inventory management. Additionally, cost-efficiency, reusability, and product standardization across geographies continue to make industrial drums a preferred choice for logistics and storage in multiple industries.

From a regional perspective, the Asia-Pacific region dominates the industrial drum market and is expected to continue as the fastest-growing region throughout the forecast period. Countries such as China and India are experiencing robust growth in manufacturing, chemicals, and agriculture—key industries driving drum demand. North America holds a significant share of the global market, supported by mature chemical and pharmaceutical industries and a strong regulatory environment that mandates secure and compliant packaging. The U.S. continues to invest in smart containment technologies and digital drum monitoring systems to enhance logistics efficiency. Europe also remains a critical region, with strong sustainability mandates under the European Union’s circular economy initiatives pushing demand for reusable and recyclable drums. Meanwhile, Latin America and the Middle East & Africa show moderate but steady growth, fueled by expanding oil and gas activities, agriculture, and infrastructure development. Overall, the global industrial drum market presents a stable and promising outlook, driven by regulatory alignment, industrial diversification, technological advancement, and growing sustainability consciousness.

Market Insights:

- The Global Industrial Drum Market was valued at USD 9,510.8 million in 2018, reached USD 13,124.5 million in 2024, and is anticipated to reach USD 20,452.1 million by 2032, growing at a CAGR of 5.73% during the forecast period.

- Rapid industrialization in emerging economies is significantly increasing the consumption of chemicals, lubricants, and processed foods, all of which require durable and compliant packaging solutions like industrial drums.

- Rising global emphasis on safety and sustainability is driving the adoption of recyclable plastic drums, fiber drums, and reusable steel drums, aligned with regulatory frameworks and environmental goals.

- Manufacturers are enhancing drum design by incorporating RFID tracking, GPS sensors, and corrosion-resistant coatings, improving safety, transparency, and inventory control across global supply chains.

- Volatile raw material prices, especially for steel, plastic resins, and fiberboard, along with ongoing supply chain disruptions, are impacting production costs and operational planning.

- The Asia-Pacific region dominates the market and is projected to remain the fastest-growing region, with China and India leading demand from manufacturing, chemical, and agricultural sectors.

- Latin America, the Middle East, and Africa are emerging as promising markets, supported by growth in oil and gas, agriculture, and infrastructure development, offering strong long-term potential.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Strong Demand from Chemical, Oil & Gas, and Pharmaceutical Industries Continues to Drive Volume and Revenue Growth:

The Global Industrial Drum Market is experiencing robust demand from key end-use industries including chemicals, oil and gas, and pharmaceuticals. These sectors rely heavily on secure, leak-proof, and regulatory-compliant containers for transporting hazardous, sensitive, or high-value materials. Industrial drums offer standardized and durable packaging, making them ideal for handling large volumes of liquids, powders, and viscous substances. In the chemical sector alone, drums account for a substantial portion of bulk packaging due to their compatibility with solvents, acids, and reagents. Pharmaceutical companies also favor drums for storing active ingredients and intermediates under sterile or controlled conditions. The oil and gas sector further boosts demand by using steel and composite drums for lubricants, additives, and specialized fluids across upstream and downstream activities.

- For instance, drum liners with multi-layer construction introduced in 2023 are now widely used in the petrochemical and pharmaceutical sectors, providing enhanced chemical resistance and leak prevention, which are critical for safe handling and storage in these industries.

Sustainability Initiatives and Regulatory Pressures Are Encouraging Adoption of Reusable and Eco-Friendly Drums:

Rising environmental awareness and global regulatory frameworks are influencing companies to shift toward reusable and recyclable drum solutions. Regulatory bodies such as the EPA in the U.S. and the European Chemicals Agency enforce guidelines that mandate safe containment, reduced waste, and traceability in industrial packaging. This shift supports increased use of fiber and high-density polyethylene (HDPE) drums, which provide environmental benefits without compromising performance. Many end users are prioritizing closed-loop systems where drums are cleaned, refurbished, and reused, thereby reducing lifecycle emissions and waste disposal costs. Reusability not only meets sustainability goals but also lowers total cost of ownership, which appeals to industries with high-volume packaging needs. The Global Industrial Drum Market is adapting quickly to these dynamics through innovations in material composition and process efficiency.

- For instance, Mauser Packaging Solutions’ Recover Syst-M program reconditions and reuses industrial drums, helping customers avoid over 1.5 million metric tons of carbon emissions in 2019 through their closed-loop system.

Technological Advancements in Smart Packaging and Material Engineering Are Enhancing Drum Utility and Safety:

Technological innovation is transforming the industrial drum landscape, with manufacturers integrating smart features and advanced materials. RFID tags, GPS-enabled sensors, and tamper-evident closures are being added to drums to ensure supply chain visibility and real-time monitoring of contents. These technologies help industries mitigate risks associated with spillage, contamination, and theft during transport or storage. On the materials front, advancements in polymer science are producing lighter yet stronger drums, which improve handling efficiency while reducing freight costs. Composite drums with multi-layer barriers offer superior resistance to corrosive substances and extreme temperatures, expanding their application range. It is also enabling compliance with stricter cross-border transport regulations, which enhances the market’s global competitiveness.

Global Trade Expansion and Demand for Bulk Transport Are Supporting Market Penetration in Emerging Economies:

Expanding international trade and industrialization in emerging economies are amplifying the need for reliable bulk packaging solutions. Countries in Asia-Pacific, Latin America, and Africa are witnessing increased production in chemicals, agriculture, and food processing, all of which require robust containment. Industrial drums provide a standardized and cost-effective method for global bulk shipments, which helps streamline logistics across ports and warehouses. The Global Industrial Drum Market benefits from this trend by expanding its reach into new regions where regulatory frameworks are evolving and demand for modern packaging is rising. Growth in export-oriented manufacturing and infrastructure investments are also prompting suppliers to scale production and localize drum manufacturing. These developments are reinforcing long-term demand and creating new opportunities for innovation and value-added services.

Market Trends:

Shift Toward Customization and Application-Specific Design Is Reshaping Product Offerings:

The Global Industrial Drum Market is witnessing a growing trend toward customization and application-specific drum configurations. End users across various industries now demand drums tailored to specific storage conditions, chemical properties, and transport requirements. Manufacturers are responding with customizable features such as enhanced linings, venting mechanisms, and drum geometries optimized for stackability and space efficiency. This trend supports operations in sectors like food processing, where hygiene requirements differ from those in oil and gas or construction. It is also driving product differentiation, allowing companies to offer niche solutions that align with customer expectations. Custom-built drum solutions are increasing customer loyalty and creating new revenue streams in an otherwise standardized product category.

- For instance, the introduction of customized drum liners with anti-static properties and leak-proof seals has improved operational safety and efficiency in sectors handling hazardous chemicals and pharmaceuticals, addressing industry-specific requirements for contamination prevention and regulatory compliance.

Integration of Digital Platforms for Inventory, Lifecycle, and Logistics Management Is Accelerating:

Digitalization is transforming how businesses manage industrial drums across supply chains. Companies are increasingly integrating digital platforms to track drum usage, schedule maintenance, and manage reverse logistics. IoT-based solutions allow real-time monitoring of drum location, fill levels, and environmental exposure, improving operational visibility and inventory optimization. It also helps reduce instances of lost, misused, or expired containers, improving overall asset management. In response, manufacturers and logistics providers are embedding digital features directly into drum systems, supporting smart warehousing and automated replenishment models. The Global Industrial Drum Market is aligning with this trend by partnering with software firms to offer drum management as a service.

- For instance, Mauser Packaging Solutions’ Recover Syst-M enables scheduling of empty packaging collection and tracking of reconditioned drums, supporting efficient asset management and circular economy initiatives.

Growth in E-Commerce and Small-Scale Industrial Packaging Needs Is Driving Demand for Mid-Sized Drums:

E-commerce-driven distribution models are influencing packaging preferences, especially among small and medium enterprises (SMEs) and direct-to-consumer industrial suppliers. This shift is fueling demand for mid-sized industrial drums ranging from 50 to 150 liters, which are more manageable, adaptable, and cost-effective for short-distance shipments or lower-volume applications. These drums support diversified logistics strategies, including third-party fulfillment centers and regional storage hubs. The Global Industrial Drum Market is expanding its product lines to cater to this growing base of small-volume users who require the durability of large drums but with better handling convenience. Manufacturers are developing ergonomic designs and quick-seal mechanisms to meet these changing needs efficiently.

Emergence of Hybrid and Collapsible Drums for Space and Cost Optimization in Logistics:

Space-saving designs and collapsible drum systems are gaining traction across industries seeking to optimize storage and return logistics. Hybrid drums that combine plastic bodies with steel reinforcements offer the benefits of both durability and lightweight handling. Foldable or stackable drums are particularly useful in sectors with high reverse logistics volumes, such as agriculture and automotive manufacturing. These innovations reduce storage space when drums are not in use and lower freight costs during returns. The Global Industrial Drum Market is embracing this trend to address growing demand for sustainable and efficient packaging that supports circular economy goals. Manufacturers are also investing in modular drum systems that allow easy repairs and part replacement, extending product lifespan and enhancing reusability.

Market Challenges Analysis:

Volatile Raw Material Prices and Supply Chain Disruptions Are Increasing Cost Pressures:

The Global Industrial Drum Market faces a significant challenge from fluctuating raw material costs, particularly steel, plastic resins, and fiberboard. These inputs are sensitive to global commodity cycles, geopolitical instability, and energy price volatility. Manufacturers must frequently adjust pricing structures, which can affect profitability and customer retention. Supply chain disruptions caused by port delays, container shortages, and regional instability further complicate procurement and lead times. These factors collectively hinder production planning and inventory management for drum manufacturers and their clients. It creates unpredictability in pricing contracts and adds complexity to long-term strategic planning across the value chain.

Intensifying Environmental Regulations and Disposal Complexities Are Limiting Market Flexibility:

Evolving environmental regulations are posing compliance challenges for drum manufacturers and users. Governments and international bodies are tightening restrictions on the use of hazardous materials, chemical residues, and improper disposal of used drums. This is particularly impactful for plastic drums, which face mounting scrutiny over recyclability and landfill contribution. Companies must invest in post-use collection, cleaning, and recycling infrastructure, which increases operational overhead. The Global Industrial Drum Market must balance durability with end-of-life sustainability, requiring innovation in design and materials. It also faces growing pressure to standardize drum designs for easier recycling and reuse, which may limit flexibility in custom manufacturing.

Market Opportunities:

Rising Demand for Sustainable and Circular Packaging Solutions Is Opening New Avenues for Innovation:

The Global Industrial Drum Market has an opportunity to capitalize on the global shift toward sustainable and circular packaging models. Governments and industries are promoting reusable and recyclable containers to reduce waste and carbon emissions. Drum manufacturers can differentiate by offering closed-loop systems, biodegradable materials, and easily recyclable designs. Companies that align with ESG standards and invest in cleaner production methods will gain preference in procurement decisions. It also encourages partnerships with recycling firms and logistics providers to streamline end-of-life drum management. Demand for environmentally responsible packaging continues to rise across sectors, including chemicals, agriculture, and food processing.

Expanding Industrialization in Emerging Economies Is Driving Long-Term Market Potential:

Rapid industrial growth in regions such as Asia-Pacific, Latin America, and Africa offers untapped opportunities for drum manufacturers. Expanding sectors like chemicals, construction, and agro-processing require robust bulk packaging solutions. The Global Industrial Drum Market can benefit by localizing production, adapting to regional compliance standards, and building supply chains in these high-growth areas. Governments are also investing in infrastructure and trade, which supports demand for high-capacity transport containers. It presents strong prospects for volume growth and market penetration. Drum manufacturers entering these markets early can secure strategic advantages and long-term contracts.

Market Segmentation Analysis:

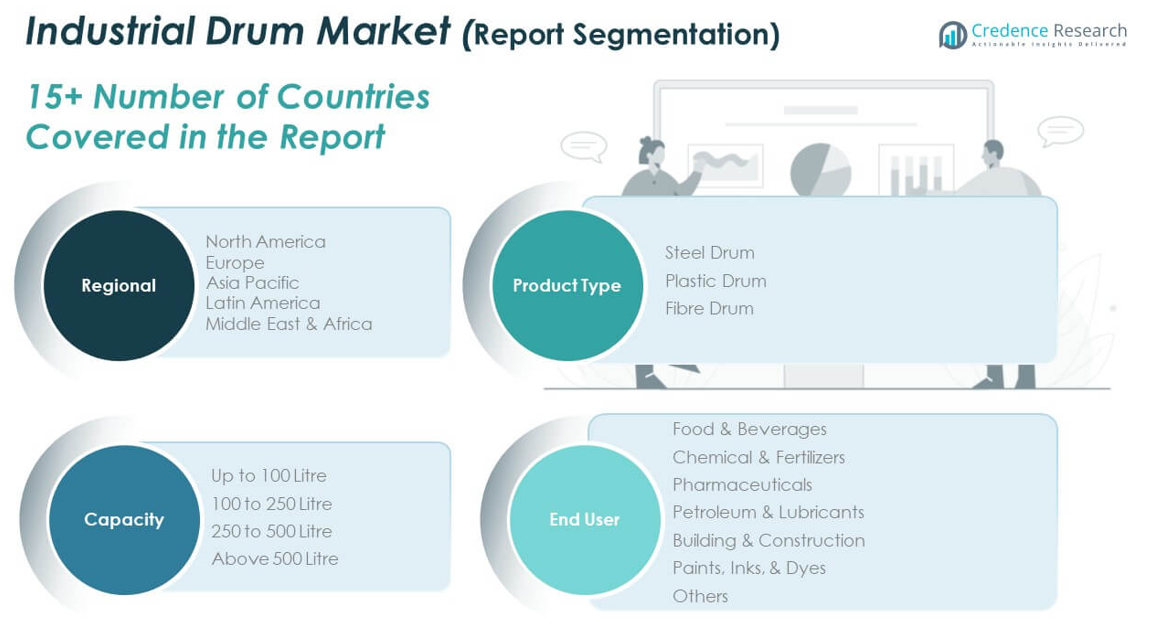

By Product Type

The Global Industrial Drum Market is segmented into steel, plastic, and fibre drums. Steel drums dominate due to their superior durability, resistance to high pressure, and compatibility with hazardous materials, making them the preferred choice in heavy-duty industries. Plastic drums, particularly HDPE variants, are widely used in food, pharmaceuticals, and chemicals because of their corrosion resistance and lightweight design. Fibre drums serve specialized applications where dry, non-hazardous goods are stored or shipped, offering cost-effectiveness and environmental benefits.

- For instance, Greif’s EcoBalance™ drums are made with more than 75% recycled HDPE, maintaining a Y1.6 liquid UN rating for performance while supporting sustainability goals.

By Capacity

Capacity-wise, 100 to 250 litre drums hold the largest market share, widely adopted for standard industrial operations across sectors. 250 to 500 litre drums are preferred for high-volume applications, especially in chemicals and petroleum. Up to 100 litre drums cater to niche needs and portable applications. The above 500 litre category is growing steadily due to rising demand in bulk exports and large-scale logistics, where container efficiency and cost per litre are key considerations.

- For instance, drum liners and reconditioning programs such as those offered by Mauser Packaging Solutions support a wide range of drum sizes, ensuring that both small and large capacity drums can be reused and recycled efficiently within industrial supply chains.

By End User

Among end users, chemical and fertilizers lead the market, driven by stringent safety regulations and bulk handling needs. Petroleum and lubricants follow closely, supported by consistent demand for steel drums in upstream and downstream supply chains. Food & beverages and pharmaceuticals are expanding rapidly, requiring contamination-free packaging. Sectors like building & construction, paints, inks, & dyes, and others contribute to steady demand across regional and global supply chains.

Segmentation:

By Product Type

- Steel Drum

- Plastic Drum

- Fibre Drum

By Capacity

- Up to 100 Litre

- 100 to 250 Litre

- 250 to 500 Litre

- Above 500 Litre

By End User

- Food & Beverages

- Chemical & Fertilizers

- Pharmaceuticals

- Petroleum & Lubricants

- Building & Construction

- Paints, Inks, & Dyes

- Others

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America

The North America Industrial Drum Market size was valued at USD 2,716.29 million in 2018 to USD 3,762.42 million in 2024 and is anticipated to reach USD 5,892.24 million by 2032, at a CAGR of 5.8% during the forecast period. The region holds a significant 28.7% share of the Global Industrial Drum Market. It benefits from advanced infrastructure, well-established manufacturing sectors, and strict regulatory compliance regarding hazardous material packaging. The United States leads regional demand, driven by the chemicals, pharmaceuticals, and oil & gas industries. Adoption of smart drums with RFID and sensor-based technologies is increasing in the logistics segment. Demand for reusable and environmentally friendly drum solutions is also rising, aligning with corporate sustainability goals. Suppliers in this region emphasize innovation and adherence to safety and environmental standards.

Europe

The Europe Industrial Drum Market size was valued at USD 2,968.33 million in 2018 to USD 4,015.73 million in 2024 and is anticipated to reach USD 6,090.63 million by 2032, at a CAGR of 5.4% during the forecast period. Europe accounts for around 30% of the global market, driven by strong regulatory frameworks and sustainability initiatives. Countries such as Germany, France, and the UK dominate regional consumption, especially in chemicals, paints, and construction materials. The European Union’s push for circular economy practices is encouraging the use of recyclable and reusable drum products. Composite and fibre drums are gaining preference in industries seeking lighter, low-emission packaging options. Drum manufacturers are investing in cleaner technologies and automation to improve cost-efficiency and product standardization. Regional demand reflects a balance of environmental policy and industrial productivity.

Asia Pacific

The Asia Pacific Industrial Drum Market size was valued at USD 2,251.21 million in 2018 to USD 3,281.50 million in 2024 and is anticipated to reach USD 5,477.07 million by 2032, at a CAGR of 6.6% during the forecast period. Asia Pacific holds a 25% share of the Global Industrial Drum Market and is the fastest-growing regional segment. China and India are major contributors, with expanding manufacturing, agricultural, and chemical sectors driving high-volume consumption. The region benefits from rising exports, growing logistics networks, and increasing adoption of bulk packaging standards. Local players are scaling up drum production to meet domestic and international demand. Regulatory improvements in waste management and packaging compliance are boosting the adoption of reusable and safe drum types. Rapid urbanization and industrialization continue to fuel new growth avenues for regional suppliers.

Latin America

The Latin America Industrial Drum Market size was valued at USD 824.59 million in 2018 to USD 1,063.09 million in 2024 and is anticipated to reach USD 1,501.18 million by 2032, at a CAGR of 4.4% during the forecast period. Latin America represents nearly 8% of the Global Industrial Drum Market. Brazil leads regional demand, followed by Argentina and Chile, supported by growth in oil and gas, food processing, and chemical industries. Adoption of cost-efficient drum types such as fibre and HDPE drums is expanding across sectors. Infrastructure development and trade agreements are improving the flow of industrial goods, boosting packaging needs. Challenges remain in regulatory harmonization and supply chain efficiency, but manufacturers are increasingly localizing production. Regional expansion is also supported by foreign investment in bulk logistics and industrial storage solutions.

Middle East

The Middle East Industrial Drum Market size was valued at USD 486.00 million in 2018 to USD 677.41 million in 2024 and is anticipated to reach USD 1,069.64 million by 2032, at a CAGR of 5.9% during the forecast period. The region holds a share of approximately 5% in the global market, with strong demand from petroleum, lubricants, and chemicals. Countries such as Saudi Arabia, UAE, and Qatar lead drum consumption, supported by large-scale refinery and downstream activities. Steel and composite drums dominate, driven by performance in high-temperature and corrosive material handling. Demand for industrial drums is rising in export packaging as the region diversifies beyond oil dependency. Government-led industrial development projects are boosting domestic production and logistics infrastructure. Manufacturers are focusing on drum reusability and compliance with hazardous goods transport regulations.

Africa

The Africa Industrial Drum Market size was valued at USD 264.40 million in 2018 to USD 324.36 million in 2024 and is anticipated to reach USD 421.31 million by 2032, at a CAGR of 3.3% during the forecast period. Africa currently holds a modest 2% share of the Global Industrial Drum Market. South Africa is the largest contributor, followed by Egypt and Nigeria. The region shows growing demand in agriculture, mining, and construction, which use drums for storage and transport of fertilizers, chemicals, and bulk solids. Local production capacity remains limited, leading to a reliance on imports and joint ventures. Demand is rising for affordable and lightweight drum options suitable for regional logistics challenges. Long-term market growth depends on infrastructure upgrades and regulatory improvements to support bulk industrial trade.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Key Player Analysis:

- Myers Container, LLC

- Greif Inc.

- Sicagen India Ltd

- Balmer Lawrie & Co. Ltd

- Time Technoplast Ltd

- Schutz GmbH & Co. KGaA

- Mauser Packaging Solutions

- TPL Plastech Limited

- Peninsula Drums

- Eagle Manufacturing Company

Competitive Analysis:

The Global Industrial Drum Market is moderately fragmented, with a mix of multinational corporations and regional manufacturers competing across materials, capacities, and end-use applications. Key players such as Greif Inc., Mauser Packaging Solutions, and Schutz GmbH & Co. KGaA dominate the market with broad product portfolios, global distribution networks, and strong investments in automation and sustainability. It continues to attract regional firms like Time Technoplast Ltd, Sicagen India Ltd, and Peninsula Drums, which focus on cost-effective solutions and localized supply. Competition centers around pricing, regulatory compliance, material innovation, and environmental performance. Companies are also adopting RFID-enabled smart drums and reusability features to gain a competitive edge. Strategic partnerships, capacity expansions, and mergers are shaping growth trajectories, particularly in high-demand regions such as Asia Pacific and North America. The market rewards suppliers that offer customized solutions, efficient logistics support, and consistent product quality across a variety of industrial applications.

Recent Developments:

- In May 2025, Elkhart Plastics, a Myers Industries company, launched the new E-Series to its TUFF line, offering a durable and sustainable intermediate bulk container (IBC) designed for secure liquid handling across industrial sectors. The E-Series features a rotomolded, impact-resistant base, optimized drainage, and a valve connection that is 30% stronger than comparable brands, reflecting Myers’ commitment to innovation and long-term value in industrial packaging.

- On February 14, 2025, Sicagen India Ltd. announced the sale of its speciality chemicals division’s defoamer business to PennWhite India Private Limited. The transaction includes intellectual property rights and the existing book of business, strengthening PennWhite’s presence in the Indian defoamer market, particularly in the fertilizer segment.

- On January 21, 2025, Time Technoplast Ltd. expanded its Middle East operations by inaugurating a new facility in Saudi Arabia for the production of IBCs and plastic drums, reinforcing its presence in the region and supporting growing demand for industrial packaging solutions.

- In November 2024, Balmer Lawrie & Co. Ltd. signed an agreement with GATX India for leasing three rakes of BFNS 22.9t wagons to transport finished steel products for Steel Authority of India (SAIL), marking Balmer Lawrie’s entry into rail logistics and expanding its capabilities in long-distance cargo movement across India.

- On March 26, 2024, Greif Inc. completed the acquisition of Ipackchem Group SAS, integrating 1,400 new colleagues and expanding its global industrial packaging portfolio. This move supports Greif’s “Build to Last” strategy and is expected to be immediately accretive to EBITDA margins, with targeted $7 million in synergies and further growth in the specialty packaging segment.

Market Concentration & Characteristics:

The Global Industrial Drum Market exhibits a moderately concentrated structure, with a few large players holding significant market share alongside numerous regional and niche manufacturers. It is characterized by product standardization, high durability requirements, and compliance with strict transportation and safety regulations. Steel and plastic drums dominate, driven by demand from chemicals, oil and gas, and food sectors. The market favors manufacturers with scalable operations, integrated logistics, and the ability to meet varied end-user needs. Customization, reusability, and adherence to environmental standards are key competitive factors. It also reflects stable demand cycles, long-term supply contracts, and growing interest in circular packaging models. Market participants that invest in innovation, localized production, and digital tracking technologies remain well-positioned in both mature and emerging regions.

Report Coverage:

The research report offers an in-depth analysis based on by product type, capacity, and end user. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Demand for industrial drums will grow steadily due to rising global manufacturing and bulk transport needs.

- Asia Pacific will remain the fastest-growing region, driven by industrial expansion in China and India.

- Sustainability initiatives will increase the adoption of reusable, recyclable, and eco-friendly drum materials.

- Steel drums will maintain dominance in hazardous and heavy-duty applications due to their durability.

- Plastic drums will see increased use in food, pharmaceutical, and water-based chemical sectors.

- Smart drums with RFID, sensors, and GPS features will gain traction for supply chain visibility.

- Regulatory compliance will drive innovation in material safety, traceability, and lifecycle management.

- Emerging markets in Africa and Latin America will offer new opportunities for volume-based growth.

- Partnerships and mergers will shape competitive strategies, especially in capacity expansion and distribution.

- Customization and application-specific designs will create value in niche industrial packaging segments.