Market Overview

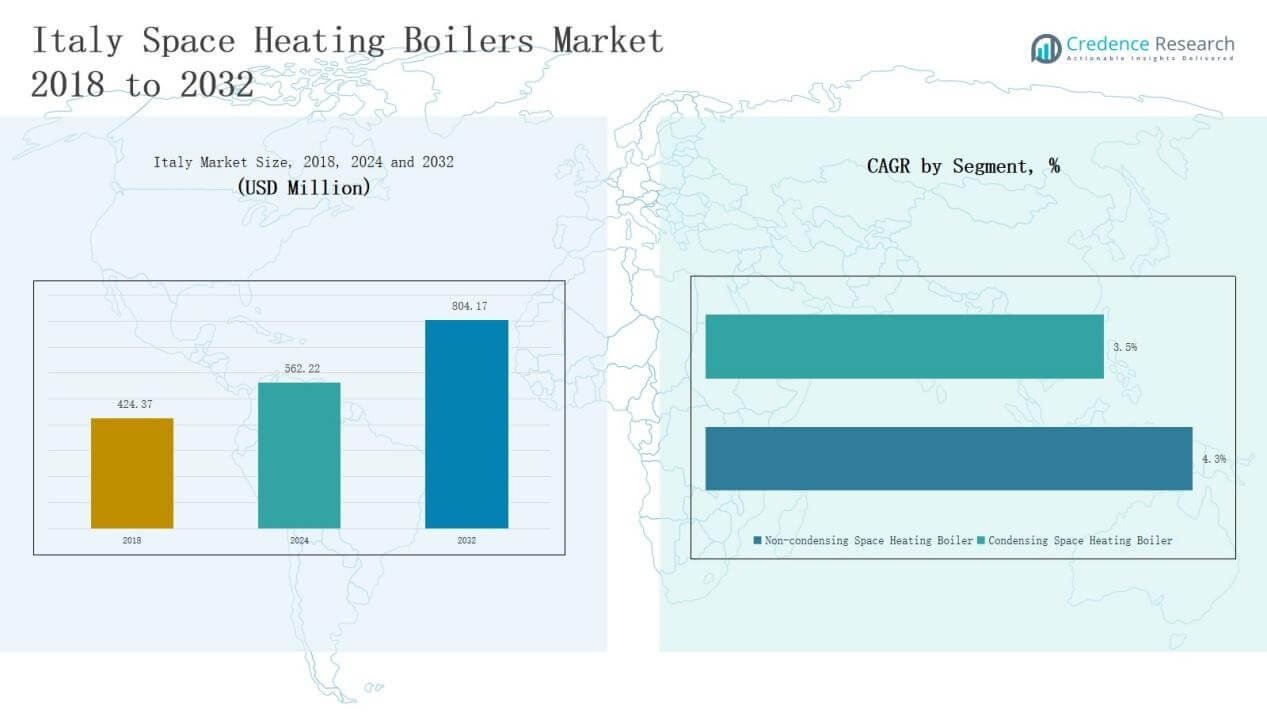

Italy Space Heating Boilers Market size was valued at USD 424.37 million in 2018 to USD 562.22 million in 2024 and is anticipated to reach USD 804.17 million by 2032, at a CAGR of 4.26% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Italy Space Heating Boilers Market Size 2024 |

USD 562.22 Million |

| Italy Space Heating Boilers Market, CAGR |

4.26% |

| Italy Space Heating Boilers Market Size 2032 |

USD 869.2 Million |

The Italy Space Heating Boilers Market is shaped by strong competition among leading companies such as Ferroli S.p.A., Bosch Thermotechnology, Riello Group, Wolf GmbH, Caldaie IN Source, Termal Ltd, Buderus, ZILMET GmbH, Atlantic Group, and De Dietrich Thermique. These players strengthen their positions through advanced condensing technologies, hybrid solutions, and robust distribution networks. Local manufacturers leverage brand recognition and established service support, while global firms focus on digital integration and eco-friendly systems to capture growing demand. Northern Italy leads the market with 38% share in 2024, driven by colder winters, urban housing density, and well-established natural gas infrastructure that supports higher adoption of energy-efficient heating solutions.

Market Insights

- The Italy Space Heating Boilers Market grew from USD 424.37 million in 2018 to USD 562.22 million in 2024 and is forecasted to reach USD 804.17 million by 2032, expanding at 4.26%.

- Condensing boilers dominate with 68% share in 2024, supported by EU efficiency directives, consumer preference for low-emission systems, and government incentives promoting replacement of outdated units.

- Residential applications lead with 61% share in 2024, driven by high household replacement demand, stricter efficiency standards, and dense urban housing; commercial and industrial segments follow with moderate contributions.

- Gas-fired boilers hold 59% share in 2024, supported by Italy’s strong gas infrastructure, while electric and hybrid systems expand, and oil and coal-based options steadily decline under environmental restrictions.

- Northern Italy commands 38% share in 2024, supported by colder winters, urban density, and established gas infrastructure, while Central, Southern, and Island regions contribute 27%, 22%, and 13% respectively.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segment Insights

By Type

Condensing space heating boilers dominate the Italy market with nearly 68% share in 2024. Their leadership is supported by strict EU energy efficiency directives and consumer preference for lower emissions systems. Government incentives for replacing older units further enhance adoption. Non-condensing boilers hold a smaller share due to declining demand and regulatory pressure, limiting their role mainly to legacy installations.

For instance, Ariston launched its Alteas One Net condensing boiler series in Italy, meeting ErP Class A+ efficiency standards and integrating connectivity for remote energy monitoring.

By Application

The residential segment accounts for 61% share in 2024, making it the leading application in Italy. Growth is driven by high household replacement demand, stricter efficiency standards for home heating, and urban housing density. The commercial segment follows, supported by modernization of office buildings and public facilities. Industrial usage remains modest but benefits from retrofitting in manufacturing plants requiring sustainable heating solutions.

For instance, Ariston launched its “LYDOS HYBRID” water heater in Italy, combining heat pump and electric technologies to meet EU energy labeling requirements.

By Operation

Gas-fired space heating boilers lead with 59% share in 2024, backed by Italy’s established gas infrastructure and affordable access. Electric boilers are gaining momentum as clean energy integration expands, though high electricity prices limit wider uptake. Oil-fired boilers retain a niche role in rural areas, while coal-based units continue to decline due to environmental restrictions. Other technologies, including hybrids, show potential as sustainability goals accelerate.

Market Overview

Key Growth Drivers

Rising Energy Efficiency Regulations

The Italy Space Heating Boilers Market is driven by stringent EU and national energy efficiency directives. Policies encourage replacement of outdated heating systems with condensing boilers that cut fuel use and emissions. Financial incentives and tax credits further accelerate household adoption. These regulations not only push modernization but also foster demand for hybrid and eco-friendly systems. Manufacturers align their portfolios with compliance standards, creating consistent growth momentum. Strong consumer awareness of energy savings also strengthens adoption across residential and commercial segments.

Growing Residential Replacement Demand

Italy’s large housing stock and aging boiler systems create strong replacement demand. Many homes continue to use outdated oil or non-condensing boilers, increasing operating costs. Rising consumer focus on comfort and lower utility bills supports the transition to condensing models. Urban density amplifies demand for compact and efficient systems. Government subsidy programs make upgrades financially attractive, driving rapid adoption in metropolitan regions. Replacement cycles are shorter as households prioritize sustainability, creating recurring revenue opportunities for boiler manufacturers.

For instance, Baxi (part of BDR Thermea Group) developed wall-hung condensing boilers such as the Luna Duo-tec E, designed to fit smaller urban apartments while maintaining high performance.

Expansion of Gas Infrastructure

The well-established natural gas distribution network strengthens demand for gas-fired space heating boilers. With gas prices relatively stable compared to oil, consumers prefer gas boilers for cost efficiency. Infrastructure modernization in Northern and Central Italy further supports growth, ensuring reliable supply. The widespread availability of gas fosters both residential and commercial adoption. Combined with incentives for cleaner gas systems, manufacturers benefit from consistent volume sales. This entrenched infrastructure provides a competitive edge against oil and coal alternatives, securing long-term market reliance on gas-fired systems.

For instance, SNAM’s 2024 hydrogen-ready pipeline initiative ensures future adaptability of Italy’s gas grid, giving boiler manufacturers confidence in sustained natural gas reliance while preparing for low-carbon gas integration.

Key Trends & Opportunities

Shift Toward Hybrid and Renewable Integration

Manufacturers are integrating hybrid systems combining gas boilers with renewable technologies like solar thermal or heat pumps. This shift aligns with Italy’s climate goals and EU decarbonization targets. Hybrid solutions enable households and businesses to reduce energy costs while lowering carbon footprints. Technological improvements in digital controls and connectivity make such systems attractive. As sustainability awareness grows, hybrid boilers represent a lucrative growth opportunity. They also position manufacturers to tap government incentives tied to renewable adoption.

For instance, the Vaillant aroTHERM plus heat pump has a Seasonal Coefficient of Performance (SCoP) of up to 5.03 and can draw up to 75% of its energy from the outside air, significantly reducing fossil fuel use.

Digitalization and Smart Boiler Adoption

The Italy Space Heating Boilers Market is witnessing rising demand for digital integration. Smart boilers equipped with IoT sensors, remote monitoring, and energy management capabilities gain traction. Consumers value features such as predictive maintenance, usage tracking, and smartphone control. These advancements not only enhance convenience but also improve efficiency and reduce downtime. Manufacturers investing in smart-enabled product portfolios capture competitive advantage. This digital shift opens opportunities for aftersales service, subscription models, and closer consumer engagement, shaping the market’s future landscape.

For instance, Ariston’s Alteas ONE Net boiler offers A+ energy efficiency and built-in Wi-Fi for remote management via the Ariston NET app, with the potential for homeowners to save up to 25% on energy bills.

Key Challenges

High Installation and Maintenance Costs

Despite efficiency benefits, condensing and hybrid boilers carry higher upfront costs. Installation requires skilled labor, driving additional expense for households and small businesses. Maintenance complexity also increases due to advanced components. These cost barriers slow adoption in price-sensitive regions. Without strong financial incentives, consumers often delay upgrades. Market penetration among lower-income groups remains limited, impacting overall growth pace. Manufacturers face the challenge of balancing affordability with innovation, as cost competitiveness remains central to wider adoption.

Dependence on Fossil Fuels

The market still heavily relies on gas-fired boilers, which represent the majority share. Although cleaner than oil or coal, natural gas remains a fossil fuel with carbon emissions. This reliance creates tension with Italy’s climate neutrality targets. Policymakers may impose stricter restrictions or push rapid transition to alternatives. Such regulatory shifts could disrupt gas boiler demand. Manufacturers must prepare by diversifying into hybrid and electric systems. The fossil fuel dependence therefore creates long-term uncertainty for market stability.

Growing Competition from Alternative Heating Solutions

Alternative technologies such as heat pumps and district heating systems pose strong competition. Heat pumps are gaining traction due to their high efficiency and renewable compatibility. Government programs increasingly support electrification of heating, favoring these alternatives over gas or oil boilers. District heating networks also expand in certain regions, offering centralized and efficient solutions. These substitutes challenge boiler manufacturers to differentiate on performance, reliability, and smart integration. Without innovation, traditional boilers risk losing market share to emerging low-carbon heating solutions.

Regional Analysis

Northern Italy

Northern Italy leads the Italy Space Heating Boilers Market with 38% share in 2024. Cold winters and dense urban centers such as Milan and Turin drive higher demand for efficient heating systems. The region’s well-developed natural gas infrastructure supports widespread use of gas-fired condensing boilers. Strong government incentives encourage replacement of older non-condensing units. Residential users dominate adoption, with rising installations in commercial buildings under energy efficiency upgrades. Manufacturers focus on hybrid solutions to align with strict environmental regulations. It remains the key hub for innovation and sustainable technology integration.

Central Italy

Central Italy holds 27% share in 2024, supported by its mix of urban and semi-urban demand. The region benefits from ongoing retrofitting projects in residential housing and small commercial establishments. Gas infrastructure remains reliable, driving consistent demand for gas-fired boilers. Electric boilers are also gaining momentum in areas with renewable power availability. The market here reflects a balance between replacement demand and new installations. It plays a pivotal role in aligning with national efficiency goals. It continues to attract investments in advanced condensing models.

Southern Italy

Southern Italy accounts for 22% share in 2024, with growth influenced by moderate winters but increasing modernization of housing. Many households transition from oil-fired boilers to cleaner gas or hybrid alternatives. Government-backed rebate programs encourage adoption in both residential and small industrial segments. Limited infrastructure in some rural areas slows market penetration. Urban centers such as Naples provide strong replacement opportunities for high-efficiency boilers. It remains an emerging growth market where hybrid solutions have significant long-term potential.

Islands (Sicily and Sardinia)

The Islands represent 13% share in 2024, reflecting smaller population density and milder climatic conditions. Demand is mainly residential, with reliance on electric boilers where gas pipelines are less developed. Replacement demand is moderate, with consumers shifting from outdated oil systems. Energy policies supporting renewable integration drive interest in hybrid models. Manufacturers face higher distribution and service costs due to geographic constraints. It shows gradual adoption of condensing technology, though overall growth pace is slower compared to mainland regions.

Market Segmentations:

By Type

- Non-condensing Space Heating Boilers

- Condensing Space Heating Boilers

By Application

- Residential

- Commercial

- Industrial

By Operation

- Gas-fired Space Heating Boilers

- Electric Space Heating Boilers

- Oil-fired Space Heating Boilers

- Coal

- Others

By Region

- Northern Italy

- Central Italy

- Southern Italy

- Islands

Competitive Landscape

The Italy Space Heating Boilers Market is highly competitive, with both domestic and international players shaping industry dynamics. Leading companies such as Ferroli S.p.A., Riello Group, Bosch Thermotechnology, Buderus, and Wolf GmbH maintain strong positions through broad product portfolios and advanced condensing technologies. Local firms leverage established distribution networks and long-standing brand presence to secure consumer trust, while global manufacturers emphasize innovation in hybrid systems, digital integration, and eco-friendly solutions. The market reflects consolidation, with players focusing on mergers, partnerships, and strategic alliances to expand their reach and strengthen aftersales support. Government incentives for efficiency upgrades push manufacturers to introduce models that comply with regulatory standards, giving early adopters a competitive advantage. Competition extends across residential, commercial, and industrial segments, where price sensitivity, technological differentiation, and service reliability remain decisive factors. Intense rivalry fosters continuous product development, ensuring that innovation and sustainability remain central to long-term growth in Italy.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Players

- Ferroli S.p.A.

- Bosch Thermotechnology

- Riello Group

- Wolf GmbH

- Caldaie IN Source

- Termal Ltd

- Buderus

- ZILMET GmbH

- Atlantic Group

- De Dietrich Thermique

Recent Developments

- In May 2025, Ariston Group entered a joint venture with Lennox to expand water-heating solutions in North America.

- In June 2025, Ariston Group signed a preliminary agreement to acquire an 80% stake in Zecchi Riscaldatori Elettrici.

- In May 2025, Alpha (part of Italy’s Immergas group) launched a hybrid residential heating solution. It combines an air‑to‑water heat pump (monobloc, up to 16 kW capacity, using R32 refrigerant) with one of its boilers, managed by smart control that optimises efficiency and lowers emissions.

- In July 2025, Cannon Bono Energia, an Italian boiler‑systems manufacturer, showcased innovative boiler solutions at CAITME 2025. The focus was on reliable, efficient, and sustainable systems.

Report Coverage

The research report offers an in-depth analysis based on Type, Application, Operation and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Condensing boilers will continue to lead adoption, driven by stricter energy efficiency rules.

- Residential demand will remain the largest contributor as replacement cycles accelerate.

- Gas-fired boilers will dominate, but hybrid systems will steadily expand market share.

- Electric boilers will grow faster with rising renewable energy integration in power grids.

- Oil-fired and coal-based systems will further decline under environmental restrictions.

- Smart and connected boilers will gain traction as consumers prefer remote monitoring features.

- Northern Italy will sustain its lead, while Southern Italy and Islands show emerging growth.

- Government rebates and tax incentives will play a key role in driving modernization.

- Competition from heat pumps and district heating will pressure boiler manufacturers to innovate.

- Partnerships and product diversification will strengthen positions of both domestic and global players.