Aviation Fuel Market Overview:

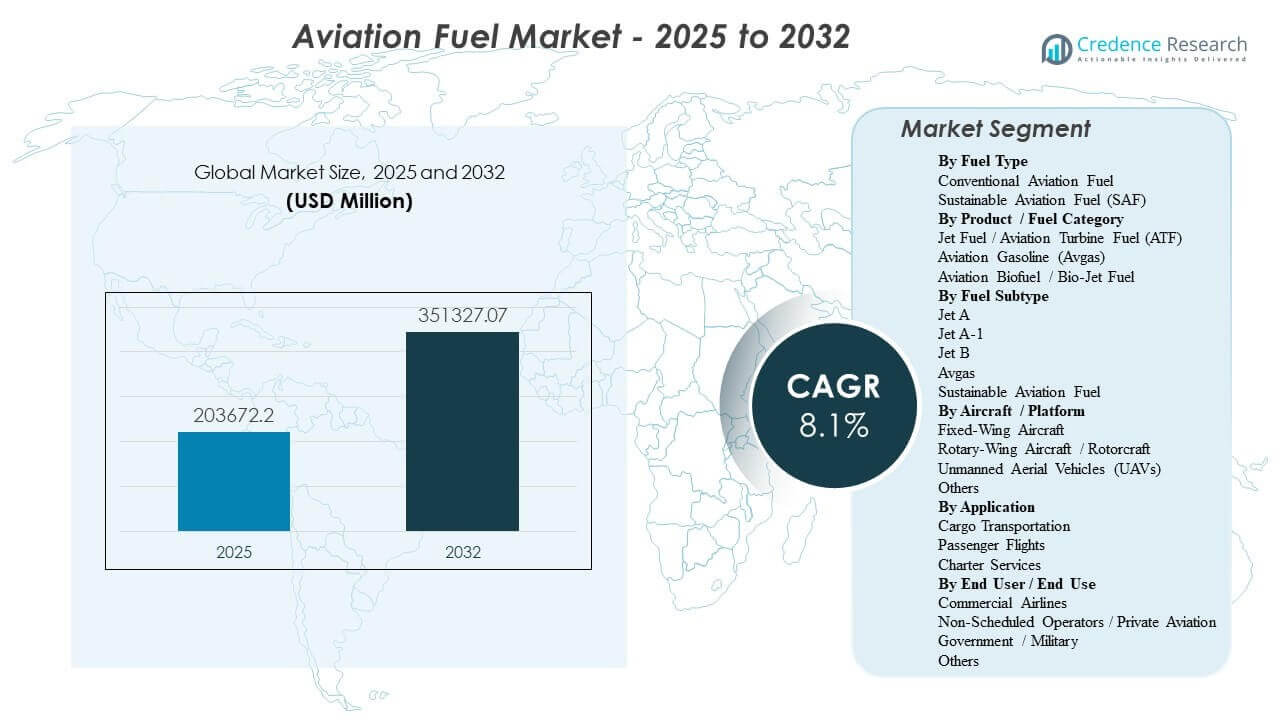

The global Aviation Fuel Market size was estimated at USD 203672.2 million in 2025 and is expected to reach USD 351327.07 million by 2032, growing at a CAGR of 8.1% from 2025 to 2032. Market expansion is primarily driven by sustained growth in passenger and cargo air traffic, which increases jet fuel uplift volumes across major airports and strengthens long-term supply contracting between airlines, fuel suppliers, and airport fuel farms. Asia Pacific remains a central demand engine as route density and fleet utilization rise across key aviation hubs, alongside capacity additions in refining, storage, and hydrant distribution that support higher throughput.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Aviation Fuel Market Size 2025 |

USD 203672.2 Million |

| Aviation Fuel Market, CAGR |

8.1% |

| Aviation Fuel Market Size 2032 |

USD 351327.07 Million |

Key Market Trends & Insights

- The Aviation Fuel Market is projected to expand from USD 203672.2 million in 2025 to USD 351327.07 million by 2032 at an 8.1% CAGR (2025–2032).

- Conventional Aviation Fuel accounted for the largest share of 97.6% in 2025, reflecting continued reliance on established refining and distribution systems.

- Sustainable Aviation Fuel adoption remains early-stage, with 2.4% implied share in 2025 as blending and procurement programs scale from a low base.

- Asia Pacific represented 40.8% of market revenue in 2025, supported by high flight activity growth and expanding airport fueling infrastructure.

- Jet A-1 accounted for the largest share of 70.9% in 2025 among fuel subtypes, supported by broad international standardization and availability.

Segment Analysis

Aviation fuel demand is shaped by a high-volume conventional base and a fast-evolving sustainability overlay. Conventional aviation fuel continues to dominate purchasing behavior because it is universally compatible with current aircraft fleets, supported by deep refinery capacity and standardized airport delivery systems. At the same time, SAF procurement is increasingly visible through long-term offtake agreements and targeted airport availability, though adoption is moderated by cost premiums, limited supply, and uneven blending logistics across regions.

Product and subtype dynamics reinforce this structure. Jet fuel remains the central consumption pool due to the scale of commercial passenger and cargo operations, whereas avgas is structurally limited to piston-engine aircraft in general aviation. Within turbine grades, Jet A-1 leads because it is widely used across international networks and is consistently available at major hubs. Platform and end-user factors further concentrate demand in fixed-wing fleets and commercial airline operations, where flight cycles, route length, and fleet utilization drive the highest fuel burn.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Fuel Type Insights

Conventional Aviation Fuel accounted for the largest share of 97.6% in 2025. Conventional aviation fuel leadership is reinforced by universal fleet compatibility, established refinery outputs, and mature airport fueling infrastructure that supports reliable supply at scale. Airline procurement practices prioritize continuity and predictable quality standards, which keeps conventional fuel central to uplift planning. SAF growth is supported by decarbonization commitments and mandates, but limited production availability and price premiums constrain near-term penetration.

By Product / Fuel Category Insights

Jet Fuel / Aviation Turbine Fuel (ATF) accounted for the largest share of 98.3% in 2026. Jet fuel dominance is driven by the large installed base of turbine aircraft used in passenger and cargo aviation and the high fuel burn associated with long-haul and high-frequency routes. Airport infrastructure such as hydrant systems and fuel farms is primarily designed around jet fuel throughput, reinforcing operational preference. Avgas remains concentrated in general aviation, and aviation biofuel/bio-jet fuel scales mainly through blending and dedicated supply programs at select airports.

By Fuel Subtype Insights

Jet A-1 accounted for the largest share of 70.9% in 2025. Jet A-1 leadership reflects widespread global standardization and broad availability across international airports, which supports consistent airline operations across multi-country networks. Cold-weather performance and operational familiarity also reinforce Jet A-1 selection for many carriers. Sustainable aviation fuel is the key growth lever within subtypes, expanding as blending capabilities and procurement mechanisms mature.

By Aircraft / Platform Insights

Fixed-Wing Aircraft account for the largest share in the Aviation Fuel Market due to the concentration of passenger and cargo operations within fixed-wing fleets. High route density, longer stage lengths, and higher utilization rates make fixed-wing platforms the primary driver of jet fuel consumption. Rotary-wing demand is important in defense, emergency services, and offshore missions, but overall uplift volumes are smaller due to mission profiles and fleet size. UAV activity is expanding across defense and select commercial applications, but fuel consumption remains comparatively limited versus manned fixed-wing aviation.

By Application Insights

Passenger Flights account for the largest share of aviation fuel demand as scheduled commercial operations generate the highest flight frequency and uplift volumes across major hubs. Network carriers and low-cost carriers both contribute to consumption through high aircraft utilization and broad route coverage. Cargo transportation is a strong structural contributor supported by e-commerce, express logistics, and time-critical supply chains, increasing fuel demand for dedicated freighters and belly cargo on passenger routes. Charter services remain smaller but can show higher SAF participation in select premium corridors and business aviation programs.

By End User / End Use Insights

Commercial Airlines account for the largest share of aviation fuel demand due to high flight cycles, large fleet sizes, and the dominance of turbine aircraft in scheduled operations. Airline procurement models emphasize supply security, pricing discipline, and operational reliability, supporting long-term contracts and integrated airport fuel services. Non-scheduled and private aviation grows through fleet expansion and premium service demand, and it can act as an early adopter segment for SAF via targeted programs. Government and military consumption is shaped by strategic readiness, certification pathways, and fuel standard requirements.

Aviation Fuel Market Drivers

Rising passenger and cargo air traffic growth

Passenger travel recovery and route additions increase flight frequency, uplift volumes, and fuel throughput at large airports. Cargo demand expands alongside e-commerce and time-sensitive logistics, increasing utilization of freighters and belly cargo capacity. Higher fleet utilization tightens operational requirements for reliable fueling infrastructure and storage capacity. Fuel suppliers benefit from long-term contracts and recurring demand patterns tied to airline schedules. In addition, expanding airport slot utilization and higher load factors intensify uplift concentration at major hubs, raising the need for scalable storage and hydrant capacity.

Expanding airline fleets and higher utilization rates

Fleet modernization and capacity additions increase the number of aircraft cycles and total fuel burn, particularly in fast-growing aviation corridors. Wider deployment of fuel-efficient aircraft does not eliminate demand growth because traffic expansion offsets efficiency gains. Growth in narrowbody fleets supports short-haul route density, while widebody deployments sustain long-haul uplift volumes. Higher utilization also increases the importance of robust airport fuel farms and hydrant systems. Moreover, tighter turnaround times make fueling speed and reliability a direct operational performance lever for airlines and airports.

- For instance, Airbus states that the A321neo integrates new-generation engines and Sharklet wingtip devices to deliver 20% less fuel burn and CO2 emissions per seat, while offering a range of up to 4,000 nautical miles and capacity for as many as 244 passengers, enabling airlines to raise cycle counts and seat deployment on dense regional and medium-haul routes.

SAF policy support and decarbonization commitments

Government mandates, airline net-zero targets, and corporate travel programs push procurement of lower-carbon aviation fuels. SAF adoption is accelerated where airports enable blending, storage, and distribution without disrupting conventional fuel logistics. Offtake agreements and book-and-claim mechanisms help aggregate demand and improve purchasing flexibility. These factors support a measurable shift in procurement strategies even when supply remains constrained. Additionally, transparent sustainability reporting and lifecycle emissions accounting are increasing the strategic value of certified SAF volumes in airline procurement.

Upgrades in fueling infrastructure and supply-chain resilience

Investment in pipelines, fuel farms, and hydrant networks improves delivery efficiency, reduces congestion from trucking, and strengthens supply reliability. Integrated digital monitoring and quality assurance processes reduce operational risk and enhance compliance. Infrastructure upgrades also support higher peak throughput during seasonal demand spikes. Supply resilience becomes a competitive differentiator for fuel suppliers serving major hubs and defense customers. Further, redundancy planning and diversified sourcing reduce disruption risk from refinery outages and regional logistics constraints.

- For instance, Exolum said its Lima airport fuel facility includes four tanks with combined capacity of approximately 35,000 m³, seven reception islands with advanced filtration systems, six high-capacity pumps, and a 10-kilometre hydrant network connected to 130 aircraft stand positions, while increasing on-site fuel stock autonomy from two days to eight days.

Aviation Fuel Market Challenges

Aviation fuel markets remain exposed to crude oil volatility and refining margin swings, which can create rapid cost changes for airlines and complicate hedging strategies. Supply chain disruptions, including refinery outages and logistics bottlenecks, can tighten availability and raise spot prices, particularly during peak travel periods. Regulatory compliance requirements across jurisdictions add operational complexity for global suppliers and multi-airport airline networks. Infrastructure constraints at congested hubs can also limit throughput expansion and increase the cost of fueling operations. At the same time, tighter environmental compliance expectations can increase investment needs for suppliers and airports to sustain operational continuity.

SAF scale-up faces structural barriers that slow penetration despite strong policy and corporate momentum. Limited feedstock availability, higher production costs, and constrained refining capacity for SAF pathways can restrict consistent supply. Blending, certification, and accounting systems differ across regions, increasing transaction complexity for airlines operating globally. Price premiums remain a central adoption constraint, especially for cost-sensitive carriers and price-competitive routes. In addition, uneven airport-level availability can fragment sourcing, making it difficult for airlines to scale SAF use consistently across networks.

- For instance, Neste started SAF production at its Rotterdam renewables refinery in April 2025, adding up to 500,000 tons per year of SAF capacity and increasing its global SAF production capability to 1.5 million tons, or around 1.875 billion liters, per year, which shows that even major capacity additions still depend on a limited number of large-scale production assets.

Aviation Fuel Market Trends and Opportunities

Aviation fuel procurement is increasingly shifting toward multi-year agreements that bundle conventional supply, SAF access, and associated airport services under unified contracts. This trend supports predictable supply planning and helps airlines coordinate SAF sourcing across priority hubs. Airports and fuel suppliers are also expanding storage and distribution capabilities to accommodate blended fuels and higher throughput requirements. Greater integration of digital quality tracking improves compliance and reduces fueling delays. Additionally, book-and-claim models are gaining traction as a practical mechanism to expand SAF participation beyond locations with direct physical supply.

- For instance, Shell Aviation, Accenture, and Amex GBT reported that Avelia had enrolled more than 57 corporations and airlines by 31 March 2025, executed over 900 retirements, and enabled the injection of more than 33 million gallons of SAF across 17 airports, with blockchain-based tracking designed to improve transparency and help prevent double counting.

Investment opportunities are strengthening around SAF production capacity, blending logistics, and hub-based distribution readiness. Airlines and corporate travel buyers are expanding voluntary procurement programs that can accelerate early volumes where mandates are still developing. Business aviation and select premium routes can act as early demand pools, helping suppliers validate supply models. Regional infrastructure upgrades, including pipelines and fuel farms, further support market expansion and operational efficiency. Moreover, co-processing, modular SAF facilities, and diversified feedstock strategies can improve supply scalability and reduce unit costs over time.

Regional Insights

North America

North America represented 29.1% of market revenue in 2025, supported by a high frequency of domestic flights, strong cargo networks, and mature airport fueling infrastructure. Demand is reinforced by large hub-and-spoke systems and high aircraft utilization across commercial carriers. Infrastructure depth supports reliable fuel delivery and efficient throughput at major airports. SAF momentum is supported by corporate travel programs and the gradual expansion of supply availability at selected hubs.

Europe

Europe accounted for 19.2% of market revenue in 2025, underpinned by dense short-haul connectivity and strong long-haul linkages through major hub airports. Regional demand is influenced by structured decarbonization programs and increasing emphasis on sustainable aviation fuel integration within airport supply chains. Procurement strategies often reflect compliance readiness and network-wide sourcing consistency. Fuel suppliers compete on service integration, hub coverage, and SAF availability.

Asia Pacific

Asia Pacific led with 40.8% of market revenue in 2025, driven by expanding route networks, rising passenger volumes, and broad fleet growth across key aviation markets. Airport infrastructure development supports higher fuel throughput and improves supply reliability as traffic scales. Strong growth in intra-regional travel and expanding cargo activity reinforce uplift volumes across major hubs. The region’s scale creates significant demand pull for both conventional fuel and emerging SAF procurement programs.

Latin America

Latin America held 3.7% of market revenue in 2025, reflecting a smaller share of global flight activity compared with North America, Europe, and Asia Pacific. Demand is concentrated around leading national carriers and key hub airports that connect regional and long-haul routes. Infrastructure expansion and airline capacity growth support steady uplift increases over time. SAF adoption is emerging through pilot programs and early supply initiatives but remains limited by availability and economics.

Middle East & Africa

Middle East & Africa represented 7.2% of market revenue in 2025, shaped by the Middle East’s role as a global long-haul hub region and Africa’s comparatively smaller aviation base. Long-haul transit operations support high uplift volumes at major hub airports and reinforce demand for reliable fuel logistics. Refining capacity and integrated energy supply chains strengthen supply reliability in key markets. SAF readiness is developing through hub-focused programs and growing emphasis on lower-carbon fuel pathways.

Competitive Landscape

Competition in the Aviation Fuel Market is defined by supply reliability, airport network coverage, pricing discipline, and the ability to provide integrated fueling services across multiple geographies. Major suppliers differentiate through long-term contracts with airlines and airports, investments in storage and hydrant infrastructure, and operational capabilities that ensure consistent on-time fueling performance. The market is also seeing increased strategic focus on SAF access, blending logistics, and traceability frameworks that support compliance and corporate decarbonization requirements. As SAF scales, partnerships and offtake agreements increasingly shape competitive positioning across key hubs.

Exxon Mobil Corporation is positioned as a diversified energy supplier with capabilities spanning refining, distribution, and large-scale fuel supply contracting that supports consistent aviation fuel delivery. The company’s scale supports structured procurement engagement with airline and airport customers seeking long-term reliability. Strategic emphasis is increasingly placed on readiness for evolving fuel specifications and lower-carbon aviation pathways, supported by collaboration across supply chains. This approach aligns operational performance with emerging sustainability-linked procurement requirements in aviation fueling.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Exxon Mobil Corporation

- Chevron Corporation

- BP p.l.c. / Air bp

- Shell plc

- TotalEnergies SE

- Indian Oil Corporation Limited

- Bharat Petroleum Corporation Limited

- Abu Dhabi National Oil Company (ADNOC)

- Viva Energy Group

- Avfuel

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In March 2026, Axens and Airbus signed a memorandum of understanding to strengthen cooperation on the development and deployment of sustainable aviation fuel, with the partnership focused on helping scale SAF solutions for the aviation sector.

- In September 2025, launch, Lootah Biofuels announced the introduction of Sustainable Aviation Fuel in the UAE market, making it one of the early local suppliers and marking a notable new product launch in the regional aviation fuel space.

- In February 2025, Boeing and Hindustan Petroleum Corporation Limited (HPCL) joined forces to advance sustainable aviation fuel development in India, highlighting collaboration across the aerospace and energy value chain.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 203672.2 million |

| Revenue forecast in 2032 |

USD 351327.07 million by 2032 |

| Growth rate (CAGR) |

8.1% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Fuel Type Outlook: Conventional Aviation Fuel, Sustainable Aviation Fuel (SAF); By Product / Fuel Category Outlook: Jet Fuel / Aviation Turbine Fuel (ATF), Aviation Gasoline (Avgas), Aviation Biofuel / Bio-Jet Fuel; By Fuel Subtype Outlook: Jet A, Jet A-1, Jet B, Avgas, Sustainable Aviation Fuel; By Aircraft / Platform Outlook: Fixed-Wing Aircraft, Rotary-Wing Aircraft / Rotorcraft, Unmanned Aerial Vehicles (UAVs), Others; By Application Outlook: Cargo Transportation, Passenger Flights, Charter Services; By End User / End Use Outlook: Commercial Airlines, Non-Scheduled Operators / Private Aviation, Government / Military, Others** |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Exxon Mobil Corporation; Chevron Corporation; BP p.l.c. / Air bp; Shell plc; TotalEnergies SE; Indian Oil Corporation Limited; Bharat Petroleum Corporation Limited; Abu Dhabi National Oil Company (ADNOC); Viva Energy Group; Avfuel |

| No. of Pages |

340 |

Segmentation

By Fuel Type

- Conventional Aviation Fuel

- Sustainable Aviation Fuel (SAF)

By Product / Fuel Category

- Jet Fuel / Aviation Turbine Fuel (ATF)

- Aviation Gasoline (Avgas)

- Aviation Biofuel / Bio-Jet Fuel

By Fuel Subtype

- Jet A

- Jet A-1

- Jet B

- Avgas

- Sustainable Aviation Fuel

By Aircraft / Platform

- Fixed-Wing Aircraft

- Rotary-Wing Aircraft / Rotorcraft

- Unmanned Aerial Vehicles (UAVs)

- Others

By Application

- Cargo Transportation

- Passenger Flights

- Charter Services

By End User / End Use

- Commercial Airlines

- Non-Scheduled Operators / Private Aviation

- Government / Military

- Others

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa