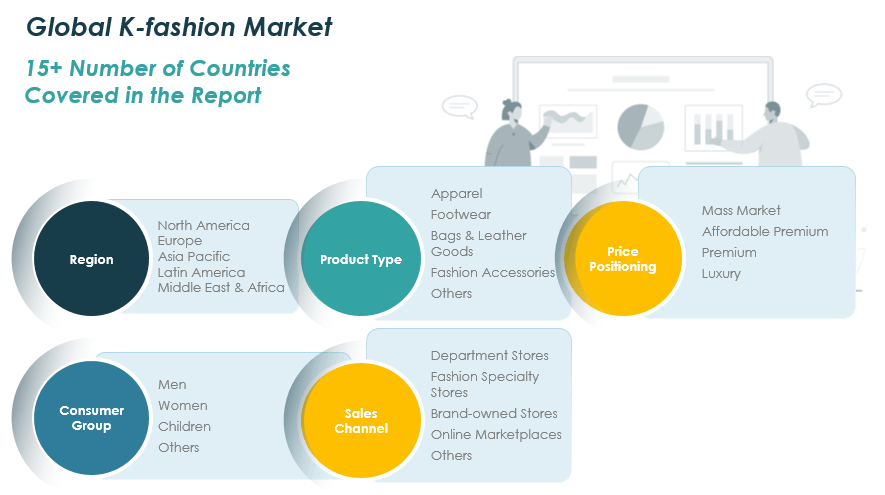

Global K-fashion Market By Product Type (Apparel, Footwear, Bags and Leather Goods, Fashion Accessories, Others); By Price Positioning (Mass Market, Affordable Premium, Premium, Luxury); By Consumer Group (Men, Women, Children, Others); By Sales Channel (Department Stores, Fashion Specialty Stores, Brand-Owned Stores, Online Marketplaces, Others); By Region (North America, Europe, Asia Pacific, Latin America, Middle East and Africa) – Growth, Share, Opportunities & Competitive Analysis, 2021–2032

The global K-fashion market size was valued at USD 31,551.37 million in 2021 and reached USD 34,953.85 million in 2025. It is anticipated to reach USD 50,952.56 million by 2032, growing at a CAGR of 5.53% from 2025 to 2032. This growth is supported by the expansion of cross-border e-commerce and digital fashion platforms, which allow Korean brands to reach overseas consumers directly and scale beyond conventional retail channels.

REPORT ATTRIBUTE

DETAILS

Historical Period

2021-2024

Base Year

2025

Forecast Period

2025-2032

K-fashion Market Size 2025

USD 34,953.85 million

K-fashion Market, CAGR

5.53%

K-fashion Market Size 2032

USD 50,952.56 million

Invest Korea notes that K-fashion is expected to access new international markets through cross-border e-commerce, while online and mobile fashion sales have expanded as brands strengthen their digital sales strategies. Additionally, public-sector export and logistics support is improving the ability of Korean designer-fashion brands to serve global buyers. In 2025, KOTRA launched a program providing eligible fashion companies with logistics infrastructure, fulfillment support, overseas-market access, and platform-based viral marketing across key international markets.

K-fashion Market Insights

Market growth is supported by the global Korean Wave, online fashion marketplaces, creator-led styling trends, brand-owned retail expansion and rising demand for Korean apparel, footwear and accessories.

Apparel holds the strongest product position because Korean fashion brands gain global visibility through streetwear, casualwear, contemporary womenswear, K-pop styling and digital-first merchandising.

Affordable Premium is gaining traction as consumers seek Korean fashion brands that offer trend-focused design, better quality perception and accessible pricing compared with luxury labels.

Asia Pacific is projected to record the fastest regional CAGR at 5.4%, supported by cultural proximity, strong digital commerce, cross-border shopping and rapid adoption of Korean style trends.

K-fashion Market Segment Insights

By Product Type

Apparel

Footwear

Bags and Leather Goods

Fashion Accessories

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

By product type, Apparel held the strongest position in 2025, supported by strong demand for Korean streetwear, casualwear, womenswear, menswear and seasonal fashion drops. K-fashion apparel benefits from strong visual appeal across social media, celebrity styling, music videos, dramas and influencer-led content. Footwear is gaining momentum as Korean brands expand into sneakers, casual shoes and lifestyle footwear that appeal to young consumers. Bags and Leather Goods support premium and affordable premium demand through minimalist design, functional styling and fashion-forward positioning. Fashion Accessories continue to gain traction across jewelry, eyewear, scarves, hats and small lifestyle products. Others include niche lifestyle products and collaboration-led fashion categories.

By price positioning

Mass Market

Affordable Premium

Premium

Luxury

By price positioning, Mass Market held a strong position in 2025 because Korean fashion remains accessible through online marketplaces, department stores and fashion specialty platforms. Affordable Premium is expected to gain strong momentum as consumers seek better design, brand identity and quality without paying luxury prices. Premium K-fashion brands are building stronger global recognition through curated stores, international pop-ups, fashion weeks and influencer partnerships. Luxury remains smaller but strategically important as Korean designers expand into global fashion capitals and collaborate with celebrities and cultural figures. Growth across price tiers reflects the ability of K-fashion brands to serve both trend-driven value buyers and higher-spending style-conscious consumers.

By consumer group

Men

Women

Children

Others

By consumer group, Women held the strongest position in 2025 because Korean fashion platforms and brands have deep strength in womenswear, beauty-linked styling and trend-driven apparel. Women’s demand is supported by dresses, outerwear, knitwear, casualwear, accessories, bags and footwear. Men represent a growing consumer group as Korean menswear, streetwear and gender-fluid styling gain international attention. Children’s fashion remains smaller but relevant through family-oriented brands, character collaborations and lifestyle products. Others include unisex, gender-neutral and youth-focused fashion categories that align with Korean street style and digital culture. Demand across consumer groups will grow as K-fashion broadens from niche fandom shopping into mainstream global fashion consumption.

By Sales Channel

Department Stores

Fashion Specialty Stores

Brand-Owned Stores

Online Marketplaces

By sales channel, Online Marketplaces held a strong position in 2025 because they help Korean brands reach global consumers without relying only on physical retail. Platforms support product discovery, cross-border transactions, influencer campaigns, reviews and curated brand storytelling. Department Stores remain important for premium positioning, brand credibility and offline customer experience. Fashion Specialty Stores support curated discovery and help emerging Korean designers build awareness. Brand-Owned Stores are gaining importance as leading companies seek better margins, customer data and direct fan engagement. Other channels include pop-up stores, social commerce, multi-brand boutiques and event-linked retail formats.

Key market drivers

Korean Wave and Global Style Influence

The Korean Wave is strengthening global demand for K-fashion by making Korean streetwear, clean tailoring, layered outfits, contemporary accessories and youth-led styling instantly recognizable across entertainment and social channels. K-pop performers, drama casts, creators and beauty-led content increasingly influence how international shoppers discover silhouettes, brands and seasonal looks, giving Korean labels a cultural connection that can reduce the effort required to build awareness abroad.

This influence extends from apparel into bags, footwear, jewelry and lifestyle accessories, particularly when brands translate celebrity visibility into distinctive product design and consistent storytelling. The opportunity is not confined to a single region, as K-fashion increasingly reaches consumers in Asia Pacific, North America, Europe, Latin America, the Middle East and Africa through digitally amplified fandoms. A notable retail example came when Nordstrom introduced eight Korean designers through its KFashion Pop-In, with products ranging from 45 to 640 US dollars across stores in the United States and Canada. Continued Korean cultural visibility should therefore support international consideration and strengthen the global commercial relevance of K-fashion through 2032.

Online Marketplaces and Cross-border Commerce

Online marketplaces and cross-border commerce are broadening K-fashion’s international reach by enabling Korean brands to sell directly to overseas consumers without first building costly wholesale or store networks. Mobile-led platforms combine product discovery, influencer referrals, targeted merchandising and real-time customer feedback, allowing emerging designers to assess demand and refine assortments by country. These capabilities are especially important for mass-market and affordable-premium labels, which can use localized languages, payment options, delivery services and return processes to make Korean fashion more accessible to global buyers.

Digital storefronts also give brands greater control over visual presentation, pricing, customer data and campaign timing than conventional multibrand distribution. The scale of platform-led brand development is evident in Coor, which generated more than 10 billion won in sales on Musinsa before expanding into physical outlets at Hyundai Department Store locations. As marketplaces continue to improve fulfillment and customer-service infrastructure, they will remain a practical export route for K-fashion companies seeking international reach while preserving agile merchandising and direct consumer engagement.

Affordable Premium and Designer Brand Expansion

Affordable-premium and designer K-fashion brands are gaining momentum as consumers seek distinctive design, flexible styling and stronger perceived quality without moving into traditional luxury price levels. Korean labels can compete effectively by introducing fast design refreshes, recognizable visual identities and products that move comfortably between streetwear, casualwear and occasion dressing. This creates a broad value ladder encompassing accessible fashion, affordable premium offerings and high-end designer collections, enabling companies to serve varied spending profiles while sustaining aspirational brand appeal. International fashion weeks, celebrity placements, retail pop-ups and collaborations can further accelerate recognition, but durable growth will depend on fit consistency, fabric quality, reliable fulfilment and locally relevant brand storytelling.

Matin Kim’s Japan strategy demonstrates the scale of ambition possible for a successful affordable-premium label: its five-year distribution partnership with Musinsa Global through 2029 carries a Japan sales target of 250 billion won. Brands that combine accessible prices with disciplined product quality and selective global retail partnerships should be best positioned to build repeat purchasing and long-term value.

Retail Experience and Pop-up-led Discovery

Retail experience and pop-up-led discovery are essential to K-fashion expansion because physical settings allow consumers to assess fit, fabric, finish and styling in ways that digital channels cannot fully replicate. Short-term stores also create urgency around exclusive drops, bring online communities into branded spaces and generate highly shareable content that can extend campaigns beyond the host location. Department stores provide credibility and established customer traffic for emerging labels, while specialty and brand-owned stores enable deeper storytelling, higher-margin selling and richer customer relationships.

The most effective model combines digital audience building with targeted offline placements in culturally relevant shopping districts, then uses shopper feedback to guide market-entry decisions. Hyundai Department Store’s The Hyundai Global initiative shows the operational advantage of this approach, stating that it can reduce the cost of opening overseas stores by more than 30 percent while managing customs, logistics and inventory for participating Korean brands. As K-fashion brands enter new cities, pop-ups and carefully chosen retail partners will remain pivotal tools for building trust, visibility and localized demand.

Key Trends and Opportunities

Global expansion of Korean designer platforms

Global expansion of Korean designer platforms is becoming a major opportunity as marketplaces and curated retailers introduce more Korean brands to international consumers. Platforms can aggregate small and midsize labels, reduce discovery friction and provide integrated logistics support. This model helps K-fashion brands enter markets such as Japan, China, Southeast Asia, North America, Europe and the Middle East without building full local infrastructure immediately. Designers benefit from data-driven merchandising, localized campaigns and cross-border fulfillment. Consumers gain access to wider assortments across Apparel, Footwear, Bags and Leather Goods and Fashion Accessories. This opportunity will remain strong as online retail becomes the main gateway for global K-fashion discovery.

K-pop, influencer and social commerce strengthen demand

K-pop, influencer and social commerce are strengthening demand by converting cultural attention into fashion purchases. Consumers often seek looks inspired by artists, actors, creators and Korean street-style influencers. Social media shortens the path from discovery to purchase, especially for Apparel, Fashion Accessories and Bags and Leather Goods. Live commerce, creator storefronts and style content help brands promote new collections and limited drops. This trend supports fast product cycles and higher engagement among Gen Z and millennial consumers. Brands that align merchandising with social content and influencer credibility will be better positioned to scale globally.

Sustainable and gender-fluid fashion gains relevance

Sustainable and gender-fluid fashion is gaining relevance as younger consumers seek values-driven and flexible styling. Korean brands are increasingly using minimalist silhouettes, unisex fits, recycled materials, lower-waste production and durable wardrobe staples to support differentiated positioning. Gender-neutral styling fits K-fashion’s broader appeal because many Korean streetwear and designer labels already emphasize oversized cuts, layering and fluid silhouettes. Sustainability can also help brands compete in Europe and North America where consumer scrutiny and retail requirements are stronger. The opportunity remains early but important for Premium, Affordable Premium and Luxury positioning. Brands with transparent sourcing, clear product quality and authentic storytelling will gain stronger long-term trust.

Key Market Challenges

Short trend cycles and inventory risk

Short trend cycles and inventory risk remain key challenges for the global K-fashion market. K-fashion demand often moves quickly across social media, celebrity looks and seasonal drops. Fast-moving trends can create overstock risk when brands scale production before demand is confirmed. Smaller designers may struggle to balance product freshness with inventory discipline. Online marketplaces also face pressure to keep assortments updated while avoiding excessive discounting. Brands need better demand forecasting, flexible sourcing and controlled drop strategies to manage this challenge. Companies with strong data systems and agile merchandising will hold an advantage.

Global competition and brand differentiation

Global competition and brand differentiation create pressure across all price tiers. K-fashion brands compete with Japanese, Chinese, European, U.S. and local fashion labels in every target market. Many brands use similar streetwear, minimalist or contemporary design cues, which can make differentiation harder. International consumers may also know K-culture but not individual Korean fashion labels. Brands must invest in storytelling, fit consistency, quality, styling content and reliable customer service to build loyalty. Companies that depend only on trend visibility may struggle to sustain repeat purchases. Distinct brand identity will become critical as K-fashion moves into more crowded global retail channels.

Cross-border logistics and localization barriers

Cross-border logistics and localization barriers can slow international growth. Fashion products require accurate sizing, reliable fulfillment, return handling, customs management and localized customer support. Differences in body fit, climate, style preferences and shopping behavior can affect sell-through across regions. Shipping costs and return complexity can reduce margins for online marketplaces and brand-owned stores. Smaller Korean brands may lack resources to manage localized marketing, translations and compliance. Platforms and retailers that provide integrated logistics, local merchandising and customer support will help reduce these barriers.

Regional Analysis

Asia Pacific

Asia Pacific is projected to grow at a CAGR of 5.4% from 2025 to 2032, supported by cultural proximity, strong Korean Wave influence and high digital commerce adoption. Japan, China, Southeast Asia and South Korea remain important markets for Apparel, Footwear, Bags and Leather Goods and Fashion Accessories. Consumers in the region respond strongly to Korean celebrity styling, social commerce, online marketplaces and pop-up stores. Department Stores, Fashion Specialty Stores and Brand-Owned Stores also support offline discovery in major cities. Asia Pacific will remain the fastest-growing region because K-fashion has strong cultural recognition and platform-led distribution in the region.

North America

North America is projected to grow at a CAGR of 4.7% from 2025 to 2032, supported by K-pop fandom, digital shopping, streetwear culture and growing awareness of Korean designer brands. The U.S. and Canada offer strong opportunities for online marketplaces, brand-owned e-commerce and selective pop-up retail. Apparel, accessories and footwear are expected to benefit from social media discovery and celebrity-led styling. Affordable Premium and Premium brands can gain traction among consumers seeking differentiated design outside mainstream fashion labels. Growth will depend on localized sizing, returns, shipping reliability and brand storytelling. North America will remain a high-value expansion market for Korean fashion platforms and designer labels.

Europe

Europe is projected to grow at a CAGR of 3.6% from 2025 to 2032, supported by rising interest in Korean design, fashion week exposure, K-pop fandom and online retail access. European consumers are style-conscious and often value quality, sustainability and brand identity, which supports Premium and Affordable Premium positioning. Growth varies by country because fashion preferences, retail channels and purchasing power differ across the region. Online marketplaces and specialty stores can help Korean brands enter fragmented markets without heavy physical retail investment. Sustainability and product quality will be important for long-term acceptance. Europe offers steady growth but requires stronger localization and brand differentiation.

Africa

Africa is projected to grow at a CAGR of 3.3% from 2025 to 2032, supported by young consumers, mobile-first retail behavior and rising exposure to Korean entertainment. Market scale remains smaller than Asia Pacific, North America and Europe, but long-term potential is emerging through online retail and social commerce. Apparel and accessories are likely to serve as entry categories because they align with youth fashion and digital trend adoption. Price sensitivity will shape demand, making Mass Market and Affordable Premium products more relevant. Growth will depend on logistics, payment access and local retail partnerships. Africa represents an early-stage opportunity for K-fashion expansion.

Latin America

Latin America is projected to grow at a CAGR of 3.2% from 2025 to 2032, supported by active K-pop fandoms, social media engagement and rising demand for Korean lifestyle products. Apparel, accessories and bags can gain traction through online marketplaces, influencer campaigns and localized product drops. Price sensitivity and import logistics remain important constraints. Spanish and Portuguese localization will help brands improve customer engagement and conversion. Pop-up stores and event-linked retail can create awareness in major cities. Latin America offers steady growth potential as Korean entertainment and youth fashion culture continue to expand.

Middle East

The Middle East is projected to grow at a CAGR of 3.0% from 2025 to 2032, supported by young consumers, premium mall retail, social media influence and rising interest in Korean culture. Gulf markets offer opportunities for Premium and Affordable Premium brands, especially through pop-up stores, department stores and online marketplaces. Apparel, bags and accessories can gain demand where Korean style aligns with modest, layered or contemporary fashion preferences. Brand localization and cultural fit will be important for product selection. Online retail will support broader access outside major retail hubs. The region offers selective but attractive opportunities for K-fashion brands with strong positioning.

In April 2025, MUSINSA reported that its Global Store transactions in Japan rose 114% year over year in the first quarter, supported by user growth and stronger demand for K-fashion brands.

In July 2025, MUSINSA was designated as an official trade company for K-fashion and outlined plans to accelerate global expansion across Japan, China, Thailand and Southeast Asia through online and offline channels.

In October 2025, W Concept expanded its overseas push by strengthening a dedicated global team and revamping its global business strategy.

In July 2024, F&F Co., Ltd. announced plans to expand Discovery Expedition across China, Japan and Southeast Asia, with a plan to grow its China store network by the end of 2025.

Report Coverage

The research report offers an in-depth analysis based on product type, price positioning, consumer group, sales channel and region. It details leading market players, providing an overview of their business positioning, fashion portfolios, retail channels, digital platforms and strategic relevance in the global K-fashion ecosystem. The report includes insights into the competitive environment, market trends, growth drivers, restraints and opportunities.

It also examines Korean Wave influence, online marketplaces, affordable premium positioning, designer brand expansion, pop-up retail, social commerce and cross-border fashion demand as major factors shaping market development. The report assesses the impact of regional demand patterns, brand localization, product differentiation, inventory risk and logistics complexity on market growth. It provides strategic recommendations for fashion brands, retailers, online marketplaces, department stores, investors, licensing partners and new entrants seeking to navigate the global K-fashion market.

Future Outlook

Demand for K-fashion will continue to rise as Korean culture, celebrity styling and digital fashion platforms influence global consumers.

Apparel will remain the leading product type because it anchors Korean streetwear, casualwear, womenswear, menswear and designer fashion demand.

Footwear and Fashion Accessories will gain traction as brands expand lifestyle collections and cross-category styling.

Affordable Premium will grow as consumers seek differentiated Korean design at accessible price points.

Women will remain the leading consumer group, while men and unisex fashion categories will gain momentum through streetwear and gender-fluid styling.

Online Marketplaces will remain a leading sales channel because they support cross-border discovery and scalable brand access.

Brand-Owned Stores and pop-up formats will become more important for customer experience, exclusive drops and premium positioning.

Asia Pacific will remain the fastest-growing region, while North America will remain a high-value expansion market.

Sustainability and product quality will become more important as Korean brands expand into Europe and premium global channels.

Competitive intensity will increase as K-fashion brands compete on design identity, fit, digital marketing, logistics, localization and retail partnerships.

Table of Contents (The complete Toc, LoF and LoT are available in the sample report)

12.1.7. Global K-fashion Revenue By Price Positioning

12.1.8. Consumer Group

12.1.9. Global K-fashion Revenue By Consumer Group

12.1.10. Sales Channel

12.1.11. Global K-fashion Revenue By Sales Channel

CHAPTER NO. 13: NORTH AMERICA K-FASHION MARKET – COUNTRY ANALYSIS

13.1. North America K-fashion Overview by Country Segment

13.1.1. North America K-fashion Revenue Share By Region

13.2. North America

13.2.1. North America K-fashion Revenue By Country

13.2.2. Product Type

13.2.3. North America K-fashion Revenue By Product Type

13.2.4. Price Positioning

13.2.5. North America K-fashion Revenue By Price Positioning

13.2.6. Consumer Group

13.2.7. North America K-fashion Revenue By Consumer Group

13.2.8. Sales Channel

13.2.9. North America K-fashion Revenue By Sales Channel

13.3. U.S.

13.4. Canada

13.5. Mexico

CHAPTER NO. 14: EUROPE K-FASHION MARKET – COUNTRY ANALYSIS

14.1. Europe K-fashion Overview by Country Segment

14.1.1. Europe K-fashion Revenue Share By Region

14.2. Europe

14.2.1. Europe K-fashion Revenue By Country

14.2.2. Product Type

14.2.3. Europe K-fashion Revenue By Product Type

14.2.4. Price Positioning

14.2.5. Europe K-fashion Revenue By Price Positioning

14.2.6. Consumer Group

14.2.7. Europe K-fashion Revenue By Consumer Group

14.2.8. Sales Channel

14.2.9. Europe K-fashion Revenue By Sales Channel

14.3. UK

14.4. France

14.5. Germany

14.6. Italy

14.7. Spain

14.8. Russia

14.9. Rest of Europe

CHAPTER NO. 15: ASIA PACIFIC K-FASHION MARKET – COUNTRY ANALYSIS

15.1. Asia Pacific K-fashion Overview by Country Segment

15.1.1. Asia Pacific K-fashion Revenue Share By Region

15.2. Asia Pacific

15.2.1. Asia Pacific K-fashion Revenue By Country

15.2.2. Product Type

15.2.3. Asia Pacific K-fashion Revenue By Product Type

15.2.4. Price Positioning

15.2.5. Asia Pacific K-fashion Revenue By Price Positioning

15.2.6. Consumer Group

15.2.7. Asia Pacific K-fashion Revenue By Consumer Group

15.2.8. Sales Channel

15.2.9. Asia Pacific K-fashion Revenue By Sales Channel

15.3. China

15.4. Japan

15.5. South Korea

15.6. India

15.7. Australia

15.8. Southeast Asia

15.9. Rest of Asia Pacific

CHAPTER NO. 16: LATIN AMERICA K-FASHION MARKET – COUNTRY ANALYSIS

16.1. Latin America K-fashion Overview by Country Segment

16.1.1. Latin America K-fashion Revenue Share By Region

16.2. Latin America

16.2.1. Latin America K-fashion Revenue By Country

16.2.2. Product Type

16.2.3. Latin America K-fashion Revenue By Product Type

16.2.4. Price Positioning

16.2.5. Latin America K-fashion Revenue By Price Positioning

16.2.6. Consumer Group

16.2.7. Latin America K-fashion Revenue By Consumer Group

16.2.8. Sales Channel

16.2.9. Latin America K-fashion Revenue By Sales Channel

16.3. Brazil

16.4. Argentina

16.5. Rest of Latin America

CHAPTER NO. 17: MIDDLE EAST K-FASHION MARKET – COUNTRY ANALYSIS

17.1. Middle East K-fashion Overview by Country Segment

17.1.1. Middle East K-fashion Revenue Share By Region

17.2. Middle East

17.2.1. Middle East K-fashion Revenue By Country

17.2.2. Product Type

17.2.3. Middle East K-fashion Revenue By Product Type

17.2.4. Price Positioning

17.2.5. Middle East K-fashion Revenue By Price Positioning

17.2.6. Consumer Group

17.2.7. Middle East K-fashion Revenue By Consumer Group

17.2.8. Sales Channel

17.2.9. Middle East K-fashion Revenue By Sales Channel

17.3. GCC Countries

17.4. Israel

17.5. Turkey

17.6. Rest of Middle East

CHAPTER NO. 18: AFRICA K-FASHION MARKET – COUNTRY ANALYSIS

18.1. Africa K-fashion Overview by Country Segment

18.1.1. Africa K-fashion Revenue Share By Region

18.2. Africa

18.2.1. Africa K-fashion Revenue By Country

18.2.2. Product Type

18.2.3. Africa K-fashion Revenue By Product Type

18.2.4. Price Positioning

18.2.5. Africa K-fashion Revenue By Price Positioning

18.2.6. Consumer Group

18.2.7. Africa K-fashion Revenue By Consumer Group

18.2.8. Sales Channel

18.2.9. Africa K-fashion Revenue By Sales Channel

18.3. South Africa

18.4. Egypt

18.5. Rest of Africa

CHAPTER NO. 19: COMPANY PROFILES

19.1. Samsung C&T Corporation, Fashion Group

19.1.1. Company Overview

19.1.2. Product Portfolio

19.1.3. Financial Overview

19.1.4. Recent Developments

19.1.5. Growth Strategy

19.1.6. SWOT Analysis

19.2. LF Corporation

19.3. Handsome Corporation

19.4. F&F Co., Ltd.

19.5. E-Land World Limited

19.6. Shinsegae International Inc.

19.7. Kolon Industries FnC

19.8. MUSINSA Co., Ltd.

19.9. W Concept Korea Co., Ltd.

19.10. Others

Request A Free Sample

We prioritize the confidentiality and security of your data. Our promise: your information remains private.

Ready to Transform Data into Decisions?

Request Your Sample Report and Start Your Journey of Informed Choices

Providing the strategic compass for industry titans.

Frequently Asked Questions:

What is the current market size for the global K-fashion market and what is its projected size in 2032?

The global K-fashion market was valued at USD 34,953.85 million in 2025 and is projected to reach USD 50,952.56 million by 2032.

At what CAGR is the global K-fashion market projected to grow?

The global K-fashion market is projected to grow at a CAGR of 5.53% from 2025 to 2032.

Which product type segment is expected to lead the global K-fashion market?

Apparel is expected to lead the market, supported by Korean streetwear, casualwear, contemporary womenswear, menswear and celebrity-led styling.

Which price positioning segment supports strong market demand?

Affordable Premium supports strong market demand because consumers seek distinctive Korean design, better quality perception and accessible pricing.

Which sales channel holds a strong position in the market?

Online Marketplaces hold a strong position because they enable cross-border product discovery, curated brand access and scalable global distribution.

Who are the leading companies in the global K-fashion market?

The leading companies include Samsung C&T Corporation, Fashion Group, LF Corporation, Handsome Corporation, F&F Co., Ltd., E-Land World Limited, Shinsegae International Inc., Kolon Industries FnC, MUSINSA Co., Ltd., W Concept Korea Co., Ltd. and Others.

Which region is projected to grow fastest?

Asia Pacific is projected to grow fastest, with a CAGR of 5.4% from 2025 to 2032.

About Author

Rajdeep Kumar Deb

Lead Analyst – Consumer & Finance

Rajdeep brings a decade of consumer goods and financial services insight to strategic market analysis.

The global K-character market size was valued at USD 3,722.94 million in 2021 and reached USD 4,557.70 million in 2025. According to Credence Research it is anticipated to reach USD 9,501.53 million by 2032, growing at a CAGR of 11.07% from 2025 to 2032.

The global K-content market size was valued at USD 100.13 billion in 2021 and reached USD 109.56 billion in 2025. It is anticipated to reach USD 152.67 billion by 2032 according to Credence Research, growing at a CAGR of 4.85% from 2025 to 2032.

The hand sanitizer dispenser market was valued at USD 101 million in 2024 and is anticipated to reach USD 281.6 million by 2032, registering a CAGR of 13.71% during the forecast period.

The Germany gift card market was valued at USD 11,288 million in 2024 and is projected to reach USD 36,247.34 million by 2032, registering a CAGR of 15.7% during the forecast period.

Recovery Footwear Market size was valued USD 4118.6 million in 2024 and is anticipated to reach USD 6862.48 million by 2032, at a CAGR of 6.59% during the forecast period.

Sewing Thread Market size was valued USD 8758.6 million in 2024 and is anticipated to reach USD 12266.18 million by 2032, at a CAGR of 4.3% during the forecast period.

Personalized Skin Care Products Market size was valued USD 30588.6 million in 2024 and is anticipated to reach USD 56157.68 million by 2032, at a CAGR of 7.89% during the forecast period.

The Russia Air Conditioner Market size was valued at USD 1,570.05 MN in 2021 and reached USD 1,875.13 MN in 2025. It is anticipated to reach USD 2,609.37 MN by 2032, growing at a CAGR of 4.8% from 2025 to 2032.

The Italy Air Conditioner Market size was valued at USD 2,329.47 MN in 2021 and reached USD 2,812.26 MN in 2025. It is anticipated to reach USD 3,992.62 MN by 2032, growing at a CAGR of 5.13% from 2025 to 2032.

The Spain Air Conditioner Market size was valued at USD 1,860.88 MN in 2021 and reached USD 2,222.47 MN in 2025. It is anticipated to reach USD 3,092.71 MN by 2032, growing at a CAGR of 4.8% during the forecast period.

K-12 Instructive Toy Market size was valued at USD 12,448.6 million in 2024 and is anticipated to reach USD 19,543.66 million by 2032, growing at a CAGR of 5.8% during the forecast period.

The Hotel Revenue Management System (RMS) market was valued at USD 16,845.30 million in 2024 and is anticipated to reach USD 32,115.4 million by 2032, expanding at a CAGR of 8.4% during the forecast period.

Licence Option

The report comes as a view-only PDF document, optimized for individual clients. This version is recommended for personal digital use and does not allow printing. Use restricted to one purchaser only.

$4999

To meet the needs of modern corporate teams, our report comes in two formats: a printable PDF and a data-rich Excel sheet. This package is optimized for internal analysis. Unlimited users allowed within one corporate location (e.g., regional office).

$5999

The report will be delivered in printable PDF format along with the report’s data Excel sheet. This license offers 100 Free Analyst hours where the client can utilize Credence Research Inc. research team. Permitted for unlimited global use by all users within the purchasing corporation, such as all employees of a single company.

Thank you for the data! The numbers are exactly what we asked for and what we need to build our business case.

Materials Scientist (privacy requested)

The report was an excellent overview of the Industrial Burners market. This report does a great job of breaking everything down into manageable chunks.