Luer Lock Connector Market Overview:

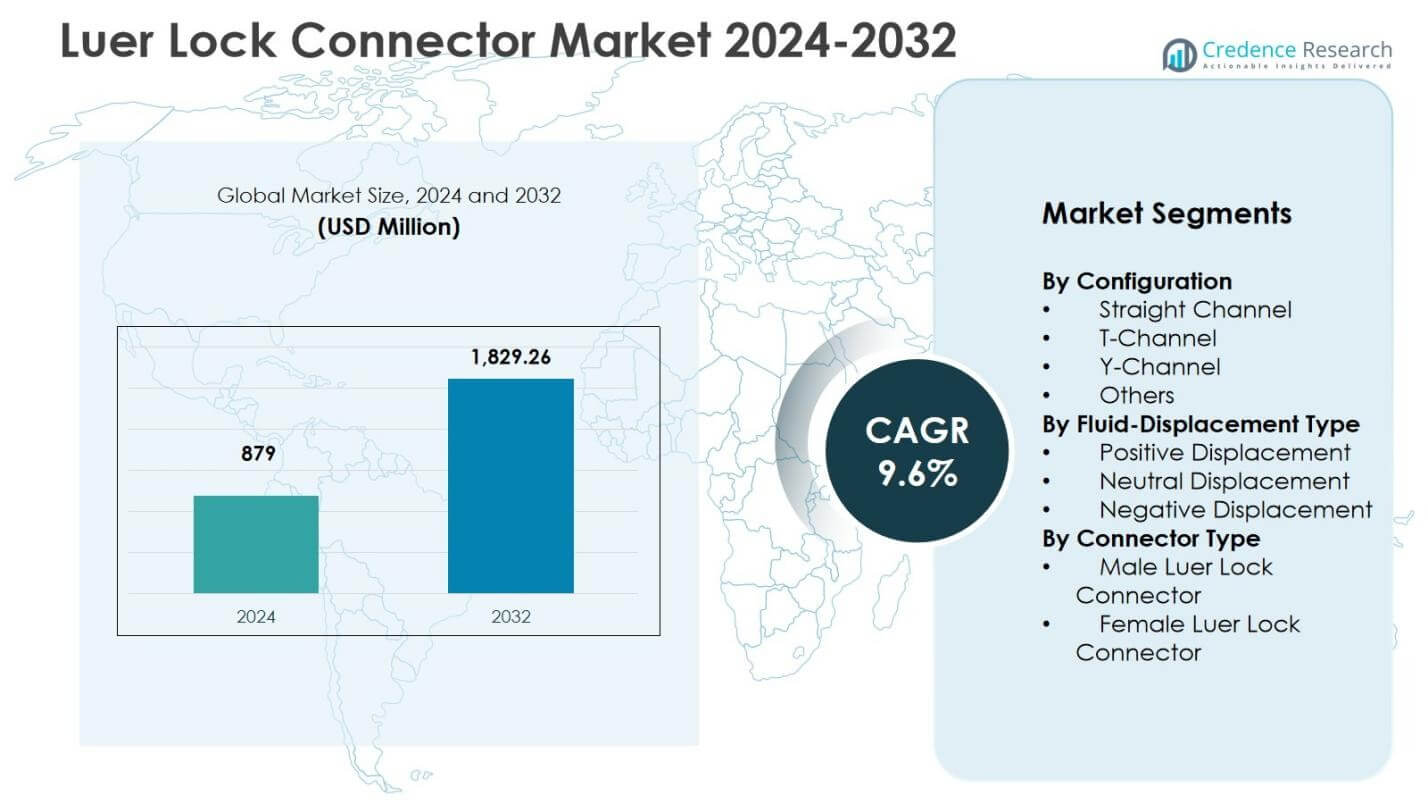

Luer Lock Connector Market size was valued USD 879 Million in 2024 and is anticipated to reach USD 1,829.26 Million by 2032, at a CAGR of 9.6% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Luer Lock Connector Market Size 2024 |

USD 879 million |

| Luer Lock Connector Market, CAGR |

9.6% |

| Luer Lock Connector Market Size 2032 |

USD 1,829.26 million |

Luer Lock Connector Market Insights

- Market growth is driven by rising infusion therapy usage, expanding adoption of vascular access devices, and increasing demand for secure fluid-management systems across hospitals, ambulatory centers, and home-care treatment environments.

- Market trends include greater adoption of needle-free and closed-system connectors, rising focus on infection-prevention designs, and growing integration of standardized connector formats across infusion pumps, syringes, and catheter-based administration systems.

- Leading players strengthen their positions through product innovation, OEM partnerships, and compliant connector design, while competition intensifies due to pricing pressure and the presence of low-cost regional manufacturers across emerging healthcare markets.

- Regional analysis shows North America held a 34.6% share in 2024, Europe accounted for 28.3%, and Asia-Pacific recorded 24.1%, while the Female Luer Lock Connector segment led the market with a 52.8% share in 2024.

Luer Lock Connector Market Segmentation Analysis:

By Configuration

The Luer Lock Connector Market by configuration is led by the Straight Channel segment, which accounted for 46.2% share in 2024, driven by its widespread use in IV infusion lines, syringes, and drug delivery systems where secure sealing and ease of alignment are essential. T-Channel and Y-Channel connectors collectively gain traction in multi-line infusion and critical-care workflows, while the Others category caters to niche clinical setups. Growth across configurations is supported by expanding hospital procedural volumes, increased adoption of closed-system transfer applications, and continuous emphasis on patient safety and leak-free fluid management.

- For instance, B. Braun’s Safeflow needle-free injection/infusion valve uses a straight fluid path that supports fast drug delivery, blood sampling, and infusions while forming a closed system designed to prevent microbial ingress and minimize needlestick risk in everyday IV therapy.

By Fluid-Displacement Type

In the Luer Lock Connector Market, the Neutral Displacement segment dominated with a 41.5% share in 2024, supported by its strong adoption in infusion therapy due to reduced catheter occlusion risk, lower infection probability, and compatibility with antimicrobial stewardship initiatives. Positive Displacement connectors hold a significant role in specialized infusion protocols, while Negative Displacement devices continue to serve legacy systems in cost-sensitive facilities. Market growth across displacement types is driven by rising central-line usage, hospital standardization toward needle-free safety systems, and clinical demand for connectors that improve line integrity and minimize thrombotic complications.

- For instance, ICU Medical’s MicroClave connector features a straight fluid path and split-septum design that minimizes blood reflux into the catheter during connection or disconnection, reducing thrombotic occlusion risk.

By Connector Type

By connector type, the Female Luer Lock Connector segment accounted for 52.8% share in 2024, emerging as the dominant sub-segment due to its critical role in IV sets, catheter hubs, and medication administration assemblies that require secure mating with multiple device interfaces. Male Luer Lock Connectors maintain strong demand across syringes, extension sets, and monitoring lines, supported by expanding outpatient and home-care infusion use. Growth across connector types is driven by rising procedural intensity in acute and ambulatory settings, increasing adoption of standardized connection systems, and regulatory focus on preventing misconnections and fluid-path failures.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Key Growth Drivers

Rising Procedural Volumes in Infusion and Drug-Delivery Applications

Growth in the Luer Lock Connector Market is strongly driven by the expanding use of infusion therapy, central venous access devices, and syringe-based drug delivery across hospitals, ambulatory centers, and home-care settings. Increasing prevalence of chronic conditions such as cancer, diabetes, and cardiovascular disease continues to elevate patient dependency on long-term intravenous treatment and vascular access procedures, thereby accelerating connector adoption. Healthcare providers increasingly standardize secure Luer Lock interfaces to reduce leakage, enhance dosing precision, and maintain fluid-path integrity. This rising procedural intensity, combined with broader adoption of closed infusion systems, significantly strengthens market demand across clinical environments.

- For instance, Baxter launched the Arisure Closed System Transfer Device in 2018, featuring a closed male Luer valve that locks onto syringes or administration sets via simple Luer lock motion.

Regulatory Emphasis on Patient Safety and Misconnection Prevention

Stringent safety regulations and international standards that mandate secure, leak-proof, and error-resistant medical connections are a major growth catalyst for the Luer Lock Connector Market. Healthcare authorities and accreditation bodies promote the use of standardized connector designs to prevent accidental misconnections, cross-contamination, and catheter-related complications. Hospitals and device manufacturers increasingly shift toward compliant, validated Luer Lock systems to align with safety initiatives and risk-management frameworks. This regulatory alignment not only supports product replacement cycles and procurement upgrades but also encourages adoption of advanced connectors with antimicrobial features, enhanced sealing capabilities, and compatibility with infection-control protocols.

- For instance, GVS Luer Lock connectors adhere to ISO 80369-7 with pyrogenicity below 0.25 EU/ml and operation up to 50°C. Available in clear polypropylene for EtO or gamma sterilization, they feature vented caps to prevent contamination in multipurpose medical applications.

Expansion of Home-Care, Ambulatory, and Outpatient Infusion Services

The rapid shift toward decentralized healthcare delivery is driving higher demand for safe and user-friendly Luer Lock connectors across home-infusion, outpatient therapy, and ambulatory care services. Growth in self-administration of biologics, wearable infusion pumps, and chronic-care management increases the need for connectors offering ease of handling, secure locking mechanisms, and compatibility with portable devices. Elderly patient populations and value-based care models further accelerate this transition, as providers prioritize solutions that support continuity of care beyond hospital environments. These dynamics contribute to rising procurement of standardized Luer Lock interfaces across non-hospital treatment ecosystems, reinforcing sustained market expansion.

Key Trends & Opportunities

Increasing Adoption of Needle-Free and Closed-System Connector Designs

A key trend shaping the Luer Lock Connector Market is the accelerating transition toward needle-free, closed-system, and antimicrobial-enhanced connectors that reduce infection risk, minimize blood reflux, and improve clinical workflow safety. Healthcare organizations prioritize designs that support central-line infection-prevention initiatives, reduce occlusion events, and enhance compatibility with high-pressure infusion systems and multi-line therapy setups. This shift creates opportunities for manufacturers to integrate advanced materials, precision sealing technologies, and ergonomic geometries that support both hospital and home-care environments. Vendors leveraging innovation in neutral-displacement and low-dead-space connectors are well positioned to capture emerging demand across high-acuity and chronic-care applications.

- For instance, BD’s MaxPlus needle-free connector employs positive displacement technology with a solid access surface, aiding in reducing central line-associated bloodstream infections (CLABSIs). It supports power injection up to 325 PSI at 10 ml/s and features anti-reflux properties to prevent blood reflux upon disconnection.

Product Customization, Material Innovation, and OEM Partnerships

The market is witnessing increasing opportunities in customized connector engineering, material optimization, and collaborative development with medical-device OEMs. Advancements in biocompatible polymers, lightweight housing structures, and durable locking threads enable product differentiation for specialized infusion sets, catheter assemblies, and diagnostic devices. Manufacturers increasingly engage in co-development partnerships to design application-specific connectors tailored to performance, sterility, and regulatory needs. Growing emphasis on supply-chain reliability and cost-efficient precision molding further strengthens vendor collaboration opportunities. As device integration expands across infusion pumps, syringes, and extension sets, tailored connector solutions create sustained avenues for premium product positioning and long-term OEM contracts.

- For instance, Onanon partnered with a medical device manufacturer to create MagConnect, a magnetic connector for hearing aids addressing dexterity challenges in elderly users. The design enables effortless alignment and secure attachment behind the ear, improving patient satisfaction and daily usability.

Key Challenges

Risk of Product Misconnections, Occlusions, and Clinical Complications

Despite widespread adoption, the Luer Lock Connector Market faces challenges related to potential misconnections, fluid-path misalignment, and catheter occlusion incidents in complex therapy environments. Variations in device compatibility, improper handling, or connector wear can increase the risk of leakage, flow disruption, and patient-safety concerns, prompting hospitals to enforce strict training and procedural controls. These risks heighten the regulatory and quality-assurance burden on manufacturers, requiring rigorous validation, labeling precision, and post-market surveillance. Ensuring consistent performance across diverse clinical conditions and multi-device interfaces remains a critical challenge for both product designers and healthcare providers.

Pricing Pressure, Standardization Requirements, and Procurement Constraints

Manufacturers in the Luer Lock Connector Market operate under strong pricing pressure due to bulk procurement models, standardization policies, and cost-sensitive purchasing environments across hospitals and public-health systems. Commoditization of basic connector formats restricts margin expansion, while ongoing compliance with evolving safety standards increases engineering and certification costs. Competition from low-cost regional suppliers further intensifies market pressure, particularly in emerging economies. Balancing affordability with design innovation, sterility assurance, and material quality remains a key operational challenge, compelling vendors to optimize production efficiency while sustaining product reliability and regulatory alignment.

Regional Analysis

North America

North America held a 34.6% share in 2024 in the Luer Lock Connector Market, driven by strong penetration of infusion therapy, advanced hospital infrastructure, and high adherence to safety regulations across the United States and Canada. The region benefits from rapid adoption of closed-system and neutral-displacement connectors supported by stringent infection-control protocols and device-standardization initiatives. Growth is reinforced by rising procedural volumes in oncology, critical care, and outpatient infusion services, alongside expanding home-care therapy adoption. Leading medical-device manufacturers and OEM partnerships further strengthen regional demand, supported by continuous product innovation and favorable reimbursement ecosystems.

Europe

Europe accounted for a 28.3% share in 2024, supported by structured healthcare policies, strong emphasis on patient-safety standards, and broad implementation of needle-free and leak-proof connector systems across hospitals and ambulatory care centers. Demand is fueled by increasing use of vascular access devices, chronic-disease infusion therapies, and national infection-prevention frameworks across Germany, France, the United Kingdom, and Nordic countries. The region also benefits from collaborative R&D programs between healthcare providers and device manufacturers, encouraging upgrades to compliant connector platforms. Growing procurement of standardized Luer Lock interfaces across public-health and specialty-care networks continues to sustain market expansion.

Asia-Pacific

Asia-Pacific recorded a 24.1% share in 2024, emerging as the fastest-growing region due to expanding hospital capacity, rising healthcare investments, and increasing procedural volumes in China, India, Japan, and Southeast Asia. Market growth is supported by rapid adoption of infusion therapy, strengthening clinical safety guidelines, and rising demand for cost-efficient yet reliable Luer Lock connectors in both public and private healthcare settings. Expanding home-care and ambulatory treatment ecosystems further stimulate procurement, while domestic manufacturing capabilities enable wider product accessibility. Ongoing government initiatives to improve infection control and standardize medical connections continue to accelerate regional market development.

Latin America

Latin America accounted for a 7.2% share in 2024, driven by increasing hospital modernization, rising access to infusion and critical-care services, and gradual transition toward standardized Luer Lock connector systems across Brazil, Mexico, and Argentina. Growth is influenced by expanding adoption of chronic-disease treatment programs and rising demand for secure fluid-management solutions in public-health networks. Procurement initiatives prioritize affordable yet compliant connector technologies, encouraging collaboration with regional distributors and OEM suppliers. While budget constraints and uneven regulatory adoption present challenges, strengthening infection-control awareness and healthcare infrastructure upgrades continue to support steady market uptake across key markets.

Middle East & Africa

The Middle East & Africa region held a 5.8% share in 2024, supported by ongoing investments in tertiary-care hospitals, oncology centers, and intensive-care infrastructure across the Gulf Cooperation Council countries and select African economies. Demand for Luer Lock connectors is driven by increasing procedural activity, greater emphasis on patient-safety compliance, and gradual integration of closed-system and needle-free infusion technologies. Growth is further reinforced by multinational vendor partnerships, healthcare expansion projects, and rising adoption of standardized connectors in urban healthcare hubs. Although market penetration varies across sub-regions, continued capacity development and clinical modernization initiatives contribute to incremental demand growth.

Luer Lock Connector Market Segmentations:

By Configuration

- Straight Channel

- T-Channel

- Y-Channel

- Others

By Fluid-Displacement Type

- Positive Displacement

- Neutral Displacement

- Negative Displacement

By Connector Type

- Male Luer Lock Connector

- Female Luer Lock Connector

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

Competitive landscape in the Luer Lock Connector Market features key players such as Becton, Dickinson and Company (BD), Baxter International Inc., Braun Melsungen AG, ICU Medical Inc., Smiths Medical, Merit Medical Systems, Nordson Corporation, TE Connectivity, Elcam Medical, and Qosina Corporation. These companies focus on product reliability, safety-compliant designs, and strong OEM partnerships to strengthen their market presence. The landscape is shaped by continuous innovation in neutral-displacement and closed-system connectors, supported by investments in precision molding, biocompatible materials, and leak-prevention technologies. Leading manufacturers emphasize regulatory alignment, infection-control capabilities, and compatibility across infusion systems to secure large hospital procurement contracts. Strategic initiatives such as portfolio expansions, geographic distribution strengthening, and collaboration with catheter and infusion-device manufacturers further enhance positioning. At the same time, pricing pressure from regional suppliers and standardization trends intensify competition, encouraging players to differentiate through performance consistency, product certification strength, and service-driven value propositions across acute care, ambulatory care, and home-infusion applications.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Recent Developments

- In September 2025, ICU Medical Inc. received new FDA 510(k) clearance for its Clave™ portfolio of needlefree IV connectors, enhancing infection-control labeling claims and supporting broader clinical adoption of its connector technology.

- In May 2025, ICU Medical, Inc. and Otsuka Pharmaceutical Factory, Inc. completed a joint venture to expand IV solutions manufacturing and innovation capacity in North America, aimed at strengthening production and supply chain resilience.

- In April 2022, Qosina announced a new line of Luer Lock connectors made from Vydyne resin to address a global Zytel nylon shortage.

Report Coverage

The research report offers an in-depth analysis based on Configuration, Fluid-Displacement Type, Connector Type, End User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will witness growing adoption of neutral-displacement and closed-system connectors to enhance patient safety and infection-control outcomes.

- Manufacturers will increasingly focus on material innovation, precision engineering, and durability to improve connector performance and reliability.

- Demand will rise across home-care and ambulatory infusion settings as decentralized healthcare delivery continues to expand.

- Integration with smart infusion systems and device-standardization initiatives will strengthen compatibility across clinical environments.

- Regulatory alignment and safety compliance requirements will drive product upgrades and replacement cycles in hospitals and clinics.

- OEM partnerships and co-development programs will expand as device manufacturers seek application-specific connector solutions.

- Emerging markets will experience accelerated adoption driven by healthcare infrastructure development and procedural growth.

- Sustainability considerations and cost-efficient manufacturing practices will gain importance in procurement decisions.

- Competitive differentiation will increasingly shift toward performance validation, certification strength, and user-centric design.

- Continuous emphasis on risk prevention and misconnection reduction will reinforce the strategic importance of standardized Luer Lock interfaces.