Market Overview

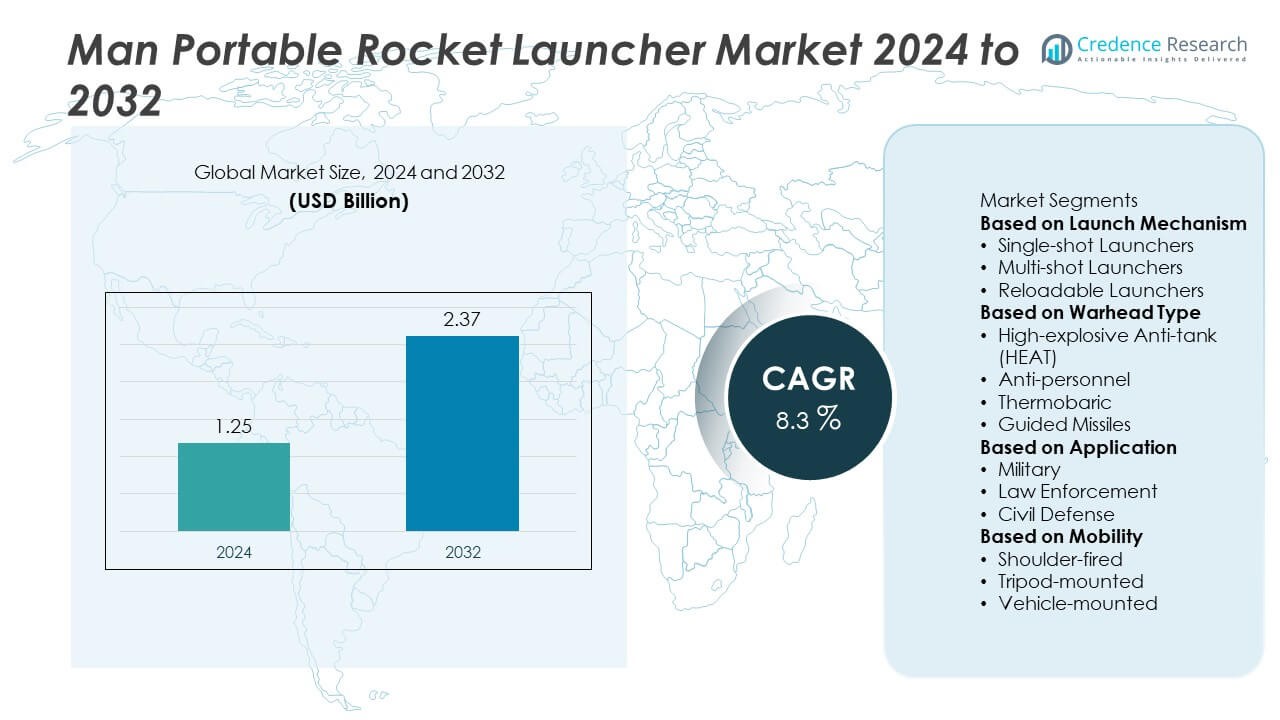

The man portable rocket launcher market was valued at USD 1.25 billion in 2024 and is expected to reach USD 2.37 billion by 2032, growing at a CAGR of 8.3% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Man Portable Rocket Launcher Market Size 2024 |

USD 1.25 Billion |

| Man Portable Rocket Launcher Market, CAGR |

8.3% |

| Man Portable Rocket Launcher Market Size 2032 |

USD 2.37 Billion |

The man portable rocket launcher market is driven by leading players including Huntington Ingalls Industries, MBDA, DRDO, Northrop Grumman, Saab AB, Thales Group, Kongsberg Gruppen, Raytheon Technologies, Rheinmetall AG, and BAE Systems. These companies focus on developing lightweight, precision-guided, and modular systems to meet modern combat needs. North America leads the market with 32% share in 2024, supported by extensive U.S. defense procurement programs and modernization initiatives. Europe follows with 28% share, driven by NATO readiness and joint procurement projects, while Asia-Pacific accounts for 25% share as regional militaries expand capabilities amid growing border tensions and modernization efforts.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The man portable rocket launcher market was valued at USD 1.25 billion in 2024 and is projected to reach USD 2.37 billion by 2032, registering a CAGR of 8.3% during the forecast period.

- Rising defense budgets, territorial disputes, and increasing adoption of lightweight, portable anti-armor systems are driving market growth, with single-shot launchers holding over 45% share.

- Trends include integration of smart targeting systems, modular launcher designs, and precision-guided warheads, enhancing operational efficiency and accuracy in urban and asymmetric warfare.

- The competitive landscape features Huntington Ingalls Industries, MBDA, DRDO, Northrop Grumman, Saab AB, Thales Group, Kongsberg Gruppen, Raytheon Technologies, Rheinmetall AG, and BAE Systems focusing on innovation and long-term contracts.

- North America leads with 32% share, followed by Europe at 28% and Asia-Pacific at 25%, driven by modernization programs, while military applications dominate the market with nearly 70% share in 2024.

Market Segmentation Analysis:

By Launch Mechanism

Single-shot launchers dominate the man portable rocket launcher market, accounting for over 45% share in 2024. Their lightweight design, ease of use, and low training requirement make them ideal for rapid deployment in field operations. Single-shot systems are widely used in infantry missions due to their low cost and ability to be disposed of after firing, reducing maintenance needs. Growing demand for compact and reliable anti-armor weapons in asymmetric warfare is driving adoption. Multi-shot and reloadable launchers are gaining interest in special forces units for their flexibility and sustained fire capability.

- For instance, the reusable RPG-7V1 launcher, designed by Russia’s Bazalt, weighs approximately 7 kg with its standard optical sight and has a tube length of 950 mm. It can fire a variety of ammunition, including the 93 mm diameter PG-7VL high-explosive anti-tank (HEAT) warhead.

By Warhead Type

High-explosive anti-tank (HEAT) warheads lead the market with more than 50% share in 2024. HEAT warheads remain the preferred choice for neutralizing armored vehicles, bunkers, and fortified positions, offering high penetration capabilities against modern armor. Rising investments in next-generation anti-armor solutions, including tandem-charge HEAT warheads for advanced protection systems, are supporting their dominance. Thermobaric warheads are gaining traction for urban combat scenarios, while guided missile warheads are expanding in use with precision-strike capabilities to minimize collateral damage and enhance mission effectiveness in complex battlefield environments.

- For instance, the RPG-30 anti-tank launcher, produced by NPO Bazalt, is designed to defeat a tank’s active protection system (APS) by first firing a smaller precursor rocket to trigger the APS. A brief delay of 0.2 to 0.4 seconds follows before the main 105mm tandem-charge HEAT warhead strikes the now-vulnerable target.

By Application

Military applications hold the largest share, representing nearly 70% of the market in 2024. Defense forces across North America, Europe, and Asia-Pacific are heavily procuring man portable rocket launchers to strengthen infantry firepower. Modernization programs and territorial tensions are fueling demand for advanced launchers with higher accuracy and extended range. Law enforcement agencies are adopting lighter versions for counter-terrorism and riot-control operations. Civil defense use remains limited but is expected to grow in regions facing heightened security threats, where portable launchers are considered vital for national preparedness and rapid response.

Key Growth Drivers

Rising Global Defense Spending

Increasing defense budgets worldwide remain a primary growth driver for the man portable rocket launcher market. Nations are prioritizing modernization of infantry weapons to strengthen rapid-response capabilities and counter evolving threats. The focus on lightweight, high-impact systems for frontline troops fuels large-scale procurement programs. Countries in Asia-Pacific and the Middle East are expanding investments due to regional tensions, creating consistent demand for advanced launchers. This spending supports the development of next-generation systems with better accuracy, longer range, and improved safety features, reinforcing market growth throughout the forecast period.

- For instance, the Saab NLAW system weighs 12.5 kg and features a combat range of 20 to 800 meters, with the time from detecting a target to engagement being approximately 5 seconds. It is built with insensitive munitions and has a shelf life of 20 years.

Growing Asymmetric Warfare and Border Conflicts

The rising frequency of asymmetric warfare, insurgencies, and border skirmishes is boosting demand for man portable rocket launchers. These weapons offer critical firepower for soldiers in complex terrains and urban battlefields, enabling rapid neutralization of armored targets and fortified positions. Lightweight and easy-to-operate launchers provide flexibility for small units, aligning with modern combat strategies. Increased focus on mobility and tactical superiority encourages armies to invest in disposable and reloadable systems. This demand is particularly high in conflict-prone regions where quick deployment and versatility are vital for mission success.

- For instance, MBDA’s Eryx system, mounted on a tripod, handles a total weight of 13 kg missile plus container, with the firing post at 4.5 kg, and hits targets from 50 m to 600 m.

Advancement in Warhead and Guidance Technology

Technological innovation is driving adoption of advanced man portable rocket launchers. Modern systems now feature enhanced guidance mechanisms, including laser and infrared targeting, improving first-shot accuracy and reducing collateral damage. Warheads are being developed with improved penetration, blast effects, and dual-purpose capabilities for multi-role missions. These advancements meet the growing need for precision strikes in urban warfare. Defense contractors are collaborating with governments to integrate smart targeting and network-enabled features, ensuring compatibility with future battlefield requirements. This continuous innovation keeps the market competitive and attractive for defense procurement agencies.

Key Trends & Opportunities

Integration of Smart Targeting Systems

A major trend shaping the market is the integration of smart optics, thermal imagers, and digital fire-control systems. These upgrades enable soldiers to engage targets with higher precision even in low-visibility conditions. The opportunity lies in combining launchers with battlefield management systems for network-centric warfare. Defense manufacturers are also investing in augmented reality (AR)-based targeting interfaces to enhance situational awareness. Adoption of such systems creates demand for modern launchers that are interoperable and future-proof, especially for technologically advanced armies in Europe and North America.

- For instance, Saab’s Carl-Gustaf M4 system can be fitted with its Fire Control Device 558 (FCD 558), which includes sensors for temperature and air pressure and has optical and night-capable cameras. The Carl-Gustaf M4 launcher itself weighs less than 7 kg, and the FCD 558 adds an additional weight of 1.2 kg.

Lightweight and Modular Launcher Designs

The push toward lighter, modular systems is creating opportunities for manufacturers to deliver highly portable solutions. Modular launchers allow troops to switch between warheads for different missions without carrying multiple systems. This trend supports versatility, reducing soldier load and enhancing operational efficiency. The development of reusable and disposable variants caters to both budget-conscious militaries and special forces. Manufacturers focusing on weight reduction through advanced materials like composites and titanium alloys are likely to capture significant contracts over the forecast period.

- For instance, Dynetics developed the GBU-69/B Small Glide Munition, a 27 kg (60 lb) precision-guided weapon, featuring a modular design that enables the integration of different warheads and sensors. Deployed from aircraft like the AC-130 gunship and drones, not as an infantry weapon, its modularity allows for mission flexibility.

Key Challenges

High Development and Procurement Costs

One of the major challenges for the market is the high cost of developing and procuring advanced rocket launcher systems. Incorporating precision-guided technologies, smart optics, and advanced materials significantly increases overall system price. Budget constraints in developing nations often delay procurement plans, limiting market penetration. Even in developed countries, cost overruns and competition with other defense priorities can slow large-scale adoption. This challenge compels manufacturers to focus on cost-effective designs and offer scalable solutions to maintain competitiveness.

Regulatory and Export Restrictions

Strict regulations and export control policies present a significant barrier to market growth. Man portable rocket launchers are classified as sensitive military equipment, requiring extensive approval for international sales. Government-imposed restrictions, compliance with ITAR (International Traffic in Arms Regulations), and risk of proliferation slow cross-border transactions. These factors can delay deals and limit market access for manufacturers targeting emerging economies. Companies must invest in compliance frameworks and build strategic partnerships with governments to overcome these barriers and expand their global footprint.

Regional Analysis

North America

North America leads the market with a 32% share in 2024. Procurement focuses on lightweight, disposable systems for infantry units. U.S. programs emphasize urban warfare readiness and rapid deployment. Canada supports NATO commitments and modernization goals. Demand centers on single-shot HEAT platforms with enhanced optics. Interoperability with allied forces remains a key requirement. Industrial depth accelerates upgrade cycles and sustainment. Border security and training initiatives add steady volumes. Suppliers benefit from multi-year framework contracts.

Europe

Europe holds a 28% share in 2024. Spending rises due to NATO readiness and regional tensions. Eastern members prioritize anti-armor capabilities and stockpile renewal. Western states fund guided and thermobaric options for urban missions. Joint procurements target common training and logistics. Emphasis falls on modular launchers and night-fighting sights. Industry offsets support local assembly and MRO. Environmental and safety rules shape material choices. Cross-border standardization improves deployment flexibility.

Asia-Pacific

Asia-Pacific accounts for a 25% share in 2024. Territorial disputes and modernization plans drive purchases. Forces seek longer range, lower weight, and faster targeting. Single-shot systems dominate infantry squads across diverse terrains. Several programs add thermobaric effects for fortified positions. Indigenous production grows through technology transfer deals. Training ranges expand to support new doctrines. Interoperability with ISR assets gains attention. Lifecycle support contracts secure fleet readiness.

Middle East and Africa

Middle East and Africa capture a 10% share in 2024. Procurement reflects counter-insurgency and border defense priorities. Buyers value rugged, simple launchers for harsh environments. Thermobaric effects see demand in urban operations. Partners fund training and sustainment packages. Stockpile refresh follows evolving threat profiles. Offset clauses encourage regional assembly and spares. Supply chain reliability is a deciding factor. Multi-vendor sourcing reduces delivery risk.

Latin America

Latin America holds a 5% share in 2024. Budgets emphasize affordability and basic anti-armor capability. Forces select disposable systems with minimal maintenance. Law enforcement use remains limited and regulated. Purchases align with peacekeeping and border patrol needs. Training focuses on safety and quick deployment. Regional industry participates mainly through spares and support. Donor programs occasionally bridge capability gaps. Long procurement cycles temper growth.

Market Segmentations:

By Launch Mechanism

- Single-shot Launchers

- Multi-shot Launchers

- Reloadable Launchers

By Warhead Type

- High-explosive Anti-tank (HEAT)

- Anti-personnel

- Thermobaric

- Guided Missiles

By Application

- Military

- Law Enforcement

- Civil Defense

By Mobility

- Shoulder-fired

- Tripod-mounted

- Vehicle-mounted

By Geography

- North America

- Europe

- Germany

- France

- Italy

- U.K.

- Russia

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Rest of Asia-Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East and Africa

Competitive Landscape

The competitive landscape of the man portable rocket launcher market features key players such as Huntington Ingalls Industries, MBDA, DRDO, Northrop Grumman, Saab AB, Thales Group, Kongsberg Gruppen, Raytheon Technologies, Rheinmetall AG, and BAE Systems. These companies focus on developing lightweight, accurate, and modular launcher systems that meet modern battlefield requirements. Strategic priorities include integrating advanced optics, guided munitions, and network-enabled targeting solutions to enhance precision and reduce collateral damage. Partnerships with defense ministries and long-term procurement contracts secure steady revenue streams. Several players invest in local manufacturing and technology transfer programs to strengthen their position in emerging markets. Continuous R&D efforts target improved warhead effectiveness, range, and soldier safety, aligning with growing demand for versatile systems. Competitive intensity remains high, with firms leveraging innovation, aftersales support, and cost-efficient solutions to capture share in modernization and replacement programs globally.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Huntington Ingalls Industries

- MBDA

- DRDO

- Northrop Grumman

- Saab AB

- Thales Group

- Kongsberg Gruppen

- Raytheon Technologies

- Rheinmetall AG

- BAE Systems

Recent Developments

- In June 2025, MBDA was awarded a contract to develop FULGUR, a very short-range air-defence (VSHORAD) missile with a man-portable launcher for the Italian Army. First deliveries are aimed for early 2028.

- In June 2025, MBDA unveiled technical details: the FULGUR missile is ~10 kg, ~1.5 m in length, 70 mm diameter, range ~5 km, supersonic speed, fire-and-forget.

- In February 2025, Thales and Bharat Dynamics Ltd signed an agreement to supply Laser Beam Riding MANPAD (LBRM) / very short-range air defence missiles and launchers to India. The missiles will be partially manufactured in India (≈60%) under “Make in India.”

- In 2025, Raytheon (RTX) with Forterra, Oshkosh Defense, and Ursa Major conducted a successful live-fire of the “DeepStrike™” autonomous mobile launcher at the U.S. Army’s Project Convergence.

Report Coverage

The research report offers an in-depth analysis based on Launch Mechanism, Warhead Type, Application, Mobility and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for lightweight, disposable launchers will rise as infantry modernization programs expand.

- Precision-guided rocket systems will see wider adoption to improve accuracy and reduce collateral damage.

- Integration of digital fire-control and smart optics will become standard for advanced armies.

- Thermobaric and multi-purpose warheads will gain traction for urban and close-combat missions.

- Regional procurement will focus on interoperability and common training standards across allied forces.

- Emerging economies will increase domestic production through technology transfer and joint ventures.

- Lifecycle support contracts and sustainment services will play a larger role in procurement decisions.

- Investments in R&D will drive innovations in range, lethality, and soldier safety.

- Modular designs allowing quick warhead swaps will become a priority for flexibility in missions.

- Global competition will intensify as new entrants offer cost-effective and locally produced launcher systems.