Motorcycle Lead Acid Battery Market Overview:

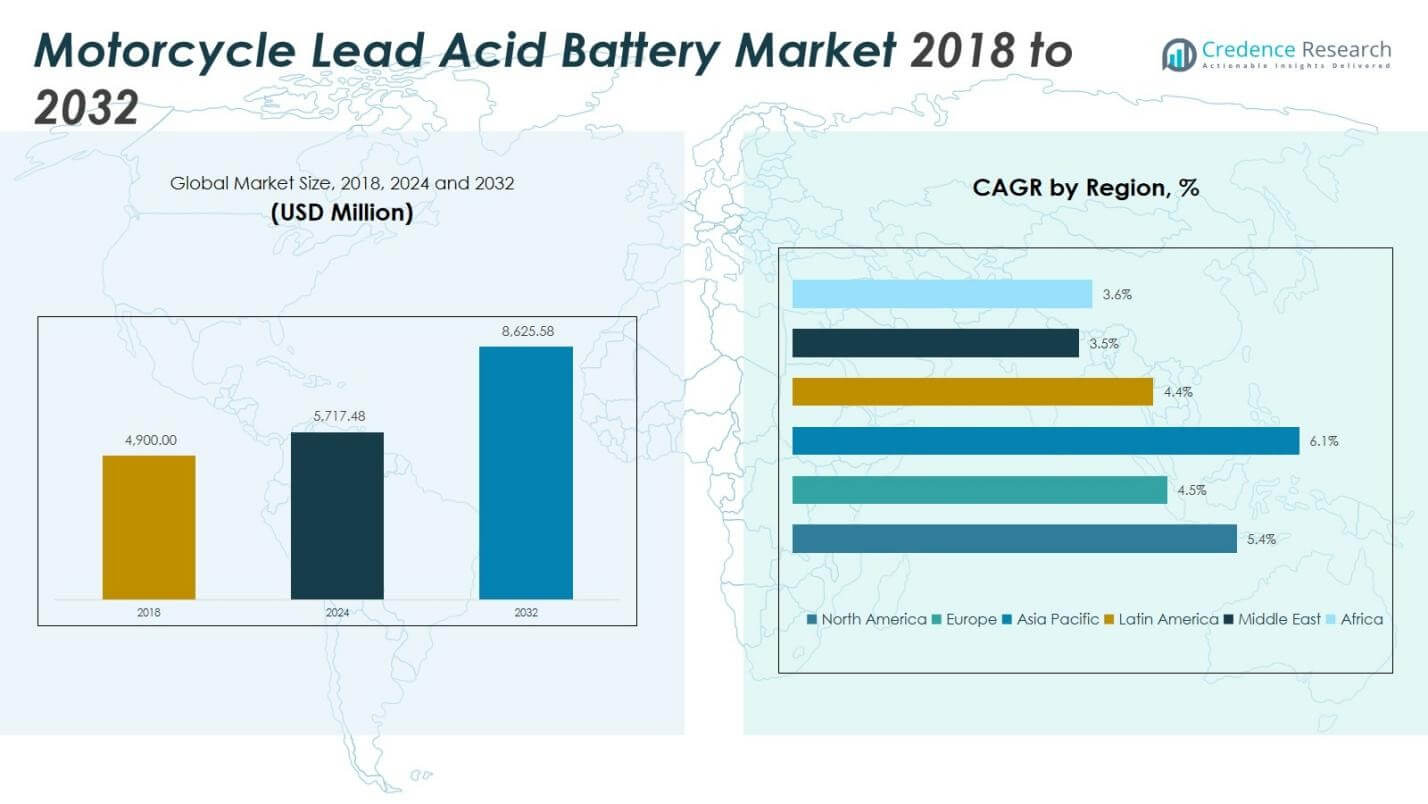

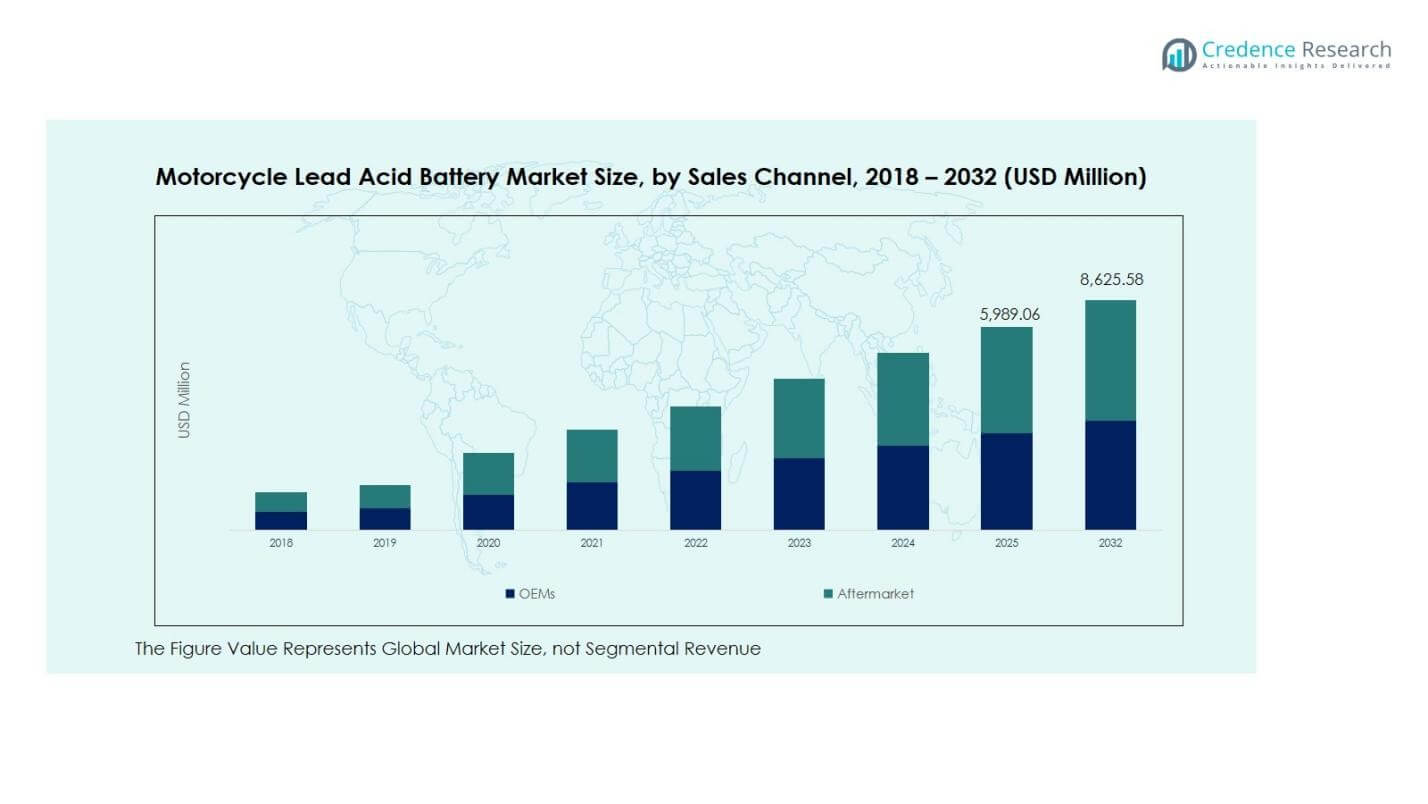

Motorcycle Lead Acid Battery Market size was valued at USD 4,900.00 Million in 2018, increased to USD 5,717.48 Million in 2024, and is anticipated to reach USD 8,625.58 Million by 2032, at a CAGR of 5.35% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Motorcycle Lead Acid Battery Market Size 2024 |

USD 12525 million |

| Motorcycle Lead Acid Battery Market, CAGR |

5.7% |

| Motorcycle Lead Acid Battery Market Size 2032 |

USD 19515 million |

Motorcycle Lead Acid Battery Market Insights

- Growth is driven by rising two-wheeler ownership in emerging economies, expanding commuter mobility, frequent replacement cycles, and cost advantage of lead acid batteries in price-sensitive regions.

- Market trends include technological improvements in VRLA and maintenance-free batteries, enhanced durability, heat- and vibration-resistant designs, and expanding adoption in commercial delivery and utility two-wheeler applications.

- Key players such as GS Yuasa Corporation, Exide Industries Ltd., Clarios, Amara Raja Batteries Ltd., and Camel Group Co., Ltd. dominate through strong distribution networks, localized production, and robust aftermarket partnerships.

- Regional analysis shows Asia Pacific leading with 44.3% share, followed by Europe at 22.42%, North America at 20.85%, Latin America 6.04%, Middle East 2.56%, and Africa 3.83%, reflecting high two-wheeler penetration and urban mobility growth.

Motorcycle Lead Acid Battery Market Segmentation Analysis:

By Vehicle Type

The Motorcycle Lead Acid Battery Market by vehicle type is led by the Motorcycles segment with a 71.6% share in 2024, driven by its widespread use in commuter transportation, strong demand in Asia Pacific, and high adoption in cost-sensitive markets where affordability and reliability remain priority factors. Lead acid batteries retain dominance in motorcycles due to low replacement cost, maintenance compatibility, and proven durability across varied riding conditions. The Scooters segment accounted for the remaining 28.4% share, supported by increasing urban mobility demand, delivery fleet expansion, and rising penetration in Southeast Asia and European city-commuting markets.

- For instance, GS Yuasa supplies high-performance lead-acid batteries like the YB16AL-A2 model, a Yumicron conventional battery designed for Ducati Monster and Superbike models as well as Yamaha Virago, featuring advanced high-cranking performance from special separators.

By Sales Channel

The market by sales channel is dominated by the Aftermarket segment with a 61.3% share in 2024, supported by frequent replacement cycles, large in-use vehicle populations, and strong availability of low-cost batteries across repair shops and retail networks in emerging economies. High operating intensity in tropical regions accelerates battery wear, reinforcing aftermarket demand. The OEMs segment held a 38.7% share, sustained by steady two-wheeler production in India, China, and ASEAN countries, where factory-fitted batteries benefit from standardized integration, warranty-linked purchases, and strong demand across commuter and entry-level motorcycle models.

- For instance, Tata Green Batteries partnered with TVS Motor for aftermarket supply, offering co-branded high-performance VRLA batteries available at TVS dealerships and workshops nationwide to simplify replacements for existing customers.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Key Growth Drivers

Rising Two-Wheeler Ownership and Expanding Commuter Mobility Demand

The Motorcycle Lead Acid Battery Market grows strongly due to rising two-wheeler ownership across emerging economies, driven by urbanization, increasing disposable incomes, and demand for affordable daily transportation. Motorcycles and scooters remain essential mobility modes in densely populated regions, creating sustained demand for reliable and cost-effective battery solutions. Lead acid batteries maintain a strong position because they offer durability, easy availability, and compatibility with commuter and utility motorcycles. Continuous fleet expansion, rising vehicle parc, and frequent battery replacement cycles strengthen revenue growth. Government support for affordable transport, expanding delivery and ride-sharing fleets, and increasing rural mobility adoption further accelerate the need for motorcycle lead acid batteries.

- For instance, Amaron’s AP-BTZ4L 12V 4Ah Pro Bike Rider battery serves scooters from various brands, with 48-month warranties catering to urbanization-driven ownership growth. Its sealed VRLA design fits commuter models, boosting replacement cycles in ride-sharing operations.

Cost Advantage, Service Availability, and Strong Aftermarket Ecosystem

The market benefits significantly from the cost advantage of lead acid batteries compared with advanced chemistries, reinforcing their dominance in price-sensitive developing markets. Wide service availability, established distribution networks, and strong support from independent repair workshops enhance consumer preference for lead acid batteries across the replacement ecosystem. High compatibility with legacy motorcycle platforms and standardized specifications reduce maintenance costs and enable quick product replacement. The robust aftermarket network across Asia Pacific, Latin America, and Africa ensures continuous product circulation and high replacement volumes. Demand is further supported by aging two-wheeler fleets, rising daily usage intensity, and reliance on low-cost maintenance solutions by commuter vehicle owners.

- For instance, GS Yuasa operates extensive training programs through its GS Yuasa Academy, partnering with the Institute of the Motor Industry to accredit workshop technicians across Asia, Europe, and other regions, ensuring reliable service for motorcycle battery maintenance and replacement.

Growing Utility, Delivery, and Commercial Two-Wheeler Applications

Expanding use of motorcycles and scooters in logistics, food delivery, courier operations, and last-mile transportation increases demand for durable and low-maintenance lead acid batteries. Commercial two-wheeler fleets operate under high-frequency usage conditions, resulting in accelerated replacement cycles and higher aftermarket consumption. Fleet operators and delivery businesses prioritize cost efficiency, reliability, and service continuity, which strengthens preference for lead acid technology in conventional motorcycles. Rapid growth of e-commerce-linked mobility, urban micro-delivery networks, and fleet-based transport platforms increases battery consumption intensity. Rising adoption of motorcycles for utility, security patrol, and municipal services in developing countries further contributes to recurring lead acid battery demand across operational vehicle segments.

Key Trends & Opportunities

Shift Toward Enhanced Lead Acid Battery Technology and Product Innovation

A key trend in the Motorcycle Lead Acid Battery Market is the development of improved flooded and VRLA lead acid battery designs that offer longer service life, better vibration resistance, and enhanced cold-cranking performance. Manufacturers focus on strengthening product durability to support high-usage commuter environments and commercial two-wheeler operations. Opportunities emerge through the integration of heat-resistant materials, improved grid structures, and advanced separators, which enhance reliability in tropical climates and harsh road conditions. Growth in performance-oriented motorcycles and premium commuter segments also creates scope for technologically upgraded lead acid variants that deliver higher output stability while retaining strong cost competitiveness in price-sensitive markets.

- For instance, Yuasa’s YTZ high-performance maintenance-free AGM batteries feature radial plate grid designs for motorcycles. They deliver up to 30% more CCA than standard AGM types in a compact form, with exceptional vibration and corrosion resistance plus multi-angle mounting capabilities.

Expanding Growth Prospects in Emerging Markets and Rural Mobility Segments

Significant opportunities arise from rapid two-wheeler penetration across rural and semi-urban areas, where motorcycles represent a primary transportation mode for households, agriculture support, and local trade activities. Expanding electrification of mobility infrastructure and increasing economic participation in developing regions stimulate long-term vehicle fleet growth and recurring battery replacement demand. Market players gain strategic advantage by strengthening dealer networks, localized manufacturing, and aftermarket distribution channels in high-growth economies across Asia Pacific, Africa, and Latin America. Government investments in road infrastructure, delivery services, and micro-enterprise mobility adoption create favorable conditions for sustained expansion of motorcycle lead acid battery consumption across new and underserved geographic territories.

- For instance, Amara Raja’s Amaron brand expands aftermarket reach in deep rural India with 23 branches and 2,000+ service hubs, facilitating lead acid battery replacements for motorcycles amid rising electrification and economic activity in semi-urban zones.

Key Challenges

Growing Penetration of Lithium-Ion Alternatives and Technology Transition Risk

The Motorcycle Lead Acid Battery Market faces challenges from increasing adoption of lithium-ion batteries in premium motorcycles, electric two-wheelers, and technologically advanced vehicle platforms. Automotive manufacturers gradually shift toward lighter, maintenance-free, and high-energy-density battery solutions, particularly in urban mobility ecosystems and performance-oriented segments. Policy incentives supporting electric mobility accelerate the technology transition risk for traditional lead acid batteries. Although cost remains a key advantage, long-term competitiveness weakens as lithium-ion prices decline and charging ecosystems expand. Market participants must respond through innovation, value-enhanced lead acid solutions, and strategic positioning in cost-driven applications to mitigate substitution pressure across future product cycles.

Environmental Compliance, Recycling Requirements, and Safety Regulations

Environmental concerns and regulatory compliance obligations present major challenges for the market, as lead-based products require strict handling, recycling, and disposal controls. Strengthening sustainability policies, hazardous material regulations, and extended producer responsibility frameworks increase operational costs for manufacturers and recyclers. Informal recycling practices in developing economies create safety risks and regulatory non-compliance issues, prompting governments to tighten enforcement measures. Market participants must invest in formal recycling infrastructure, supply-chain transparency, and environmentally responsible manufacturing processes to maintain market credibility. Rising expectations for eco-friendly material management and circular economy alignment drive the need for cleaner production standards across the motorcycle lead acid battery value chain.

Regional Analysis

North America

North America accounted for 20.85% share of the Motorcycle Lead Acid Battery Market in 2024, with the market increasing from USD 1,043.70 Million in 2018 to USD 1,192.63 Million in 2024, and it is projected to reach USD 1,795.00 Million by 2032 at a CAGR of 5.4%. Growth is driven by a steady rise in motorcycle ownership for recreational and commuter use, strong aftermarket replacement demand, and the presence of structured service networks. Aging two-wheeler fleets and high vehicle usage intensity in the U.S. and Mexico continue to support recurring battery replacement consumption and enhance revenue contribution from the region.

Europe

Europe represented 22.42% share of the Motorcycle Lead Acid Battery Market in 2024, growing from USD 1,149.05 Million in 2018 to USD 1,282.28 Million in 2024, and is expected to reach USD 1,813.55 Million by 2032 at a CAGR of 4.5%. Market performance is supported by the increasing popularity of motorcycles for leisure touring, urban commuting, and delivery services across major economies. Lead acid batteries remain widely adopted due to cost efficiency and compatibility with conventional motorcycle platforms, while expanding aftermarket networks and periodic replacement cycles sustain revenue growth across Southern and Eastern European countries.

Asia Pacific

Asia Pacific dominated the Motorcycle Lead Acid Battery Market with the largest 44.30% share in 2024, increasing from USD 2,116.80 Million in 2018 to USD 2,531.96 Million in 2024, and projected to reach USD 4,047.99 Million by 2032 at a CAGR of 6.1%. Growth is driven by high two-wheeler penetration in India, China, Indonesia, and Vietnam, where motorcycles serve as a primary mobility mode. Large in-use vehicle populations, frequent replacement demand, rising commercial delivery applications, and strong aftermarket ecosystems reinforce the dominance of lead acid batteries across commuter and utility motorcycle segments in the region.

Latin America

Latin America accounted for 6.04% share of the Motorcycle Lead Acid Battery Market in 2024, expanding from USD 298.90 Million in 2018 to USD 345.28 Million in 2024, and forecast to reach USD 481.91 Million by 2032 at a CAGR of 4.4%. Market growth is supported by increasing motorcycle adoption for urban commuting, affordability-driven mobility choices, and the expansion of informal and organized repair networks. Replacement battery purchases remain strong in Brazil and Argentina due to rising vehicle usage intensity, economic reliance on two-wheelers, and the dominance of cost-efficient lead acid technology in everyday transportation fleets.

Middle East

The Middle East held 2.56% share of the Motorcycle Lead Acid Battery Market in 2024, rising from USD 137.20 Million in 2018 to USD 146.33 Million in 2024, and is expected to reach USD 190.67 Million by 2032 at a CAGR of 3.5%. Demand is influenced by utility-oriented motorcycle applications, security patrol fleets, and commercial delivery services in urban centers. Hot climatic conditions lead to accelerated battery wear, driving recurring aftermarket replacement consumption. Growing mobility needs in emerging Gulf economies and expansion of service distribution channels continue to support stable regional demand for motorcycle lead acid batteries.

Africa

Africa accounted for 3.83% share of the Motorcycle Lead Acid Battery Market in 2024, increasing from USD 154.35 Million in 2018 to USD 219.00 Million in 2024, and projected to reach USD 296.45 Million by 2032 at a CAGR of 3.6%. Market expansion is driven by rising motorcycle usage for public transport, commercial mobility, and rural commuting across East and West African economies. Lead acid batteries remain preferred due to affordability and ease of maintenance, while growing motorcycle taxi services, expanding aftermarket networks, and aging vehicle fleets contribute to consistent replacement-driven battery demand across the region.

Motorcycle Lead Acid Battery Market Segmentations:

By Vehicle Type

By Sales Channel

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

Competitive landscape analysis in the Motorcycle Lead Acid Battery Market is shaped by leading players such as GS Yuasa Corporation, Exide Industries Ltd., Clarios, Amara Raja Batteries Ltd., Camel Group Co., Ltd., Leoch International Technology Ltd., Tianneng Battery Group Co., Ltd., Tata Green Batteries, Yuasa Battery Inc., and PT. GS Battery. The market reflects strong consolidation, with established manufacturers leveraging extensive distribution networks, localized production capabilities, and robust aftermarket partnerships to maintain volume advantage across high-demand regions. Competition centers on pricing efficiency, product durability, lifecycle performance, and service availability, particularly in commuter and utility two-wheeler segments where cost-sensitive consumer adoption remains dominant. Players focus on expanding replacement battery portfolios, enhancing heat- and vibration-resistant designs, and strengthening regional supply chains to support recurring aftermarket demand. Strategic priorities include capacity expansion in Asia Pacific, dealership network reinforcement, and technology upgrades in VRLA and maintenance-free variants to improve reliability while preserving the cost advantage that sustains lead acid battery preference in global motorcycle fleets.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- GS Yuasa Corporation

- Exide Industries Ltd.

- Clarios (formerly Johnson Controls)

- Amara Raja Batteries Ltd.

- Camel Group Co., Ltd.

- Leoch International Technology Ltd.

- Tianneng Battery Group Co., Ltd.

- Tata Green Batteries

- Yuasa Battery Inc.

- PT. GS Battery

Recent Developments

- In May 2025, GS Yuasa Battery Ltd. announced plans to renew its high‑performance ECO.R Revolution series, enhancing service life and starting power for battery applications, supporting broader battery portfolio innovation.

- In July 2025, Varroc launched VRLA batteries for two-wheelers in the aftermarket segment, offering maintenance-free options from 2.5AH to 9AH with a 48-month pro-rata warranty.

- In January 2024, Ipower Batteries Private Ltd. launched graphene‑series lead‑acid batteries in India designed for faster charging, enhanced energy efficiency, and longer life compared to traditional lead‑acid units.

- In June 2024, Amara Raja signed a licensing deal with China’s Gotion for lithium battery cell manufacturing and partnered for LFP cell production, while also securing agreements with OEMs including Ather Energy and Piaggio India to supply lithium‑ion batteries.

Report Coverage

The research report offers an in-depth analysis based on Vehicle Type, Sales Channel and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Motorcycle lead acid battery demand will continue to grow due to expanding two-wheeler ownership in emerging markets.

- Replacement cycles will remain a key revenue driver as aging motorcycle fleets require frequent battery changes.

- Aftermarket channels will dominate sales, supported by extensive service networks and independent workshops.

- Technological improvements in VRLA and maintenance-free lead acid batteries will enhance performance and reliability.

- Asia Pacific will remain the largest regional market due to high two-wheeler penetration and urban mobility growth.

- Cost advantage will sustain lead acid batteries in price-sensitive markets despite rising lithium-ion adoption.

- Commercial and delivery fleet applications will increase recurring battery consumption.

- Strategic expansions by key players will strengthen regional distribution and production capabilities.

- Environmental and recycling regulations will influence manufacturing and supply chain practices.

- Growth opportunities will expand in rural mobility segments and semi-urban transportation markets.