Angola Power EPC Market Overview:

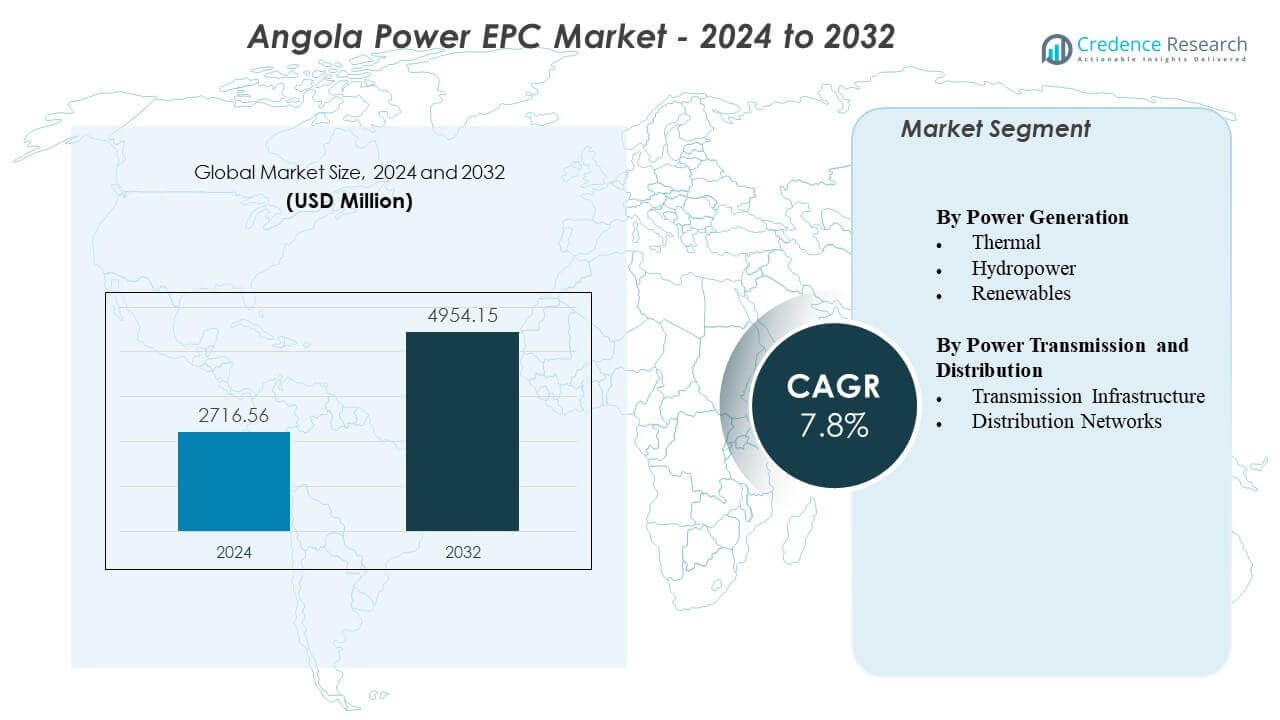

The Angola Power EPC Market is projected to grow from USD 2716.56 million in 2024 to an estimated USD 4954.15 million by 2032, with a compound annual growth rate (CAGR) of 7.8% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Angola Power EPC Market Size 2024 |

USD 2716.56 million |

| Angola Power EPC Market, CAGR |

7.8% |

| Angola Power EPC Market Size 2032 |

USD 4954.15 million |

Strong market drivers include rising demand for new hydropower capacity, growing adoption of solar plants and modernization efforts targeting outdated transmission assets. Developers advance grid reinforcement to reduce system losses and improve stability for industrial and urban regions. EPC activity rises with government-backed investment plans that encourage private participation and foreign partnerships. Contractors expand their scope as hybrid energy systems and storage projects gain importance. The market benefits from structured financing support that helps accelerate large-scale projects. It continues to attract global engineering firms due to clear long-term investment direction.

Regional activity is most concentrated in northern Angola, where major hydropower assets and dense urban clusters create sustained EPC demand. Central provinces emerge as important development zones due to new renewable installations and growing industrial requirements. Southern regions gain momentum through cross-border transmission planning and electrification of remote communities. It expands EPC opportunities tied to network strengthening and modular generation projects. Inland areas adopt new distribution upgrades to improve service reliability. This regional diversification supports a balanced project pipeline across the country.

Angola Power EPC Market Insights:

- The Angola Power EPC Market is projected to grow from USD 2716.56 million in 2024 to USD 4954.15 million by 2032, supported by a 7.8% CAGR driven by sustained investment in national power infrastructure.

- Demand strengthens due to expanding hydropower development, rising solar adoption and grid modernization efforts aimed at improving reliability for industrial and urban zones.

- Market restraints include aging network components, complex project financing requirements and logistical challenges in transporting heavy equipment to remote construction sites.

- Regional activity is led by northern Angola due to dense demand centers and major hydropower assets, while central provinces show rising EPC momentum through new renewable and grid projects.

- Southern and eastern regions continue to emerge as EPC opportunities grow through rural electrification programs, cross-border transmission planning and distribution system upgrades.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Angola Power EPC Market Drivers

Strong Expansion of Generation Capacity Across Key Hydropower and Solar Projects

The Angola Power EPC Market gains strong momentum from rapid growth in power generation projects. Developers focus on hydropower expansion to meet long-term demand and strengthen base-load supply. EPC contractors receive steady work from turbine upgrades, dam reinforcement and power evacuation structures. New solar projects support grid diversification and reduce dependence on hydropower in dry seasons. The government pushes for higher electrification targets, which encourages new capacity across several provinces. Foreign investors support project financing, which helps EPC firms secure long tenure projects. It shapes a steady pipeline of work across engineering and construction phases. EPC timelines remain strong due to clear investment priorities.

- For instance, Andritz Hydro GmbH delivered Francis turbines in African hydropower projects operating at 94–96% hydraulic efficiency, supported by digitally controlled wicket-gates that improve part-load performance by up to 4%.

Grid Modernization Programs That Improve Network Stability and System Reliability

Grid modernization efforts drive consistent investment activity in the Angola Power EPC Market. Transmission upgrades increase system resilience and reduce power losses in dense urban zones. EPC firms gain contracts for new substations, digital controls and replacement of outdated components. The government increases focus on stable supply to industrial nodes across Luanda and inland regions. It helps developers plan phased expansion aligned with rising consumption patterns. Several modernization programs target improved load management and reduced outage frequency. Contractors support advanced protection systems that improve fault response. Investment continues because demand growth strains legacy networks.

- For instance, Siemens AG 8DN8 GIS technology reduces substation footprint by up to 60% and extends maintenance intervals to more than 10 years, enabling high-density deployment in constrained urban sites. Siemens SIPROTEC relays record fault-clearing responses in 14–18 milliseconds, improving grid fault isolation accuracy.

Large-Scale Electrification Commitments That Expand Power Access Across Provinces

National electrification plans shape strong EPC demand throughout the Angola Power EPC Market. The government targets wider access in rural and semi-urban regions that face supply gaps. EPC developers receive priority for transmission corridors and community grid extensions. It raises project volume for distribution works that support remote clusters. Electrification targets align with growth in housing, industry and commercial activity. Contractors support meter rollouts and low-voltage upgrades across expanding settlements. Local workforce participation grows under national development policies. Power access goals ensure long-term continuity in EPC projects.

Foreign Partnerships and Technology Transfer Programs That Support Complex Project Delivery

Rising collaboration with global engineering partners strengthens project execution across the Angola Power EPC Market. International firms support advanced hydropower design, digital monitoring tools and modern grid equipment. Joint ventures help local firms improve execution quality and meet global performance standards. It creates a competitive EPC environment that supports efficient project timelines. Technology transfer programs encourage adoption of modular substations and automated control systems. Contractors gain structured training for complex transmission and renewable projects. Foreign lenders support long-cycle investments that improve sector stability. Market confidence increases with better governance and transparent contracting.

Angola Power EPC Market Trends

Shift Toward Hybrid Energy Integration and Flexible Grid Solutions Across Provinces

A clear shift toward hybrid integration shapes new activity in the Angola Power EPC Market. Developers plan hybrid systems that combine hydropower with solar fields for improved year-round output. EPC firms design flexible grid solutions that manage variable inputs from new renewable sites. It helps operators reduce strain on legacy hydropower assets during peak periods. Developers explore battery storage to stabilize grid flows in vulnerable regions. Hybrid concepts support smoother load balancing across expanding urban zones. Contractors adapt engineering practices to meet diverse resource mixes. The trend gains momentum with strong policy support.

- For instance, utility hybrid systems using Siemens AG Fluence-engineered battery blocks show response times of 150–300 milliseconds for frequency regulation, maintaining grid deviation below 0.1 Hz in field tests.

Growing Use of Digital Engineering Tools and Remote Monitoring Technologies

Digital capabilities influence project execution across the Angola Power EPC Market. EPC firms employ advanced modeling platforms to streamline design phases for large assets. Remote monitoring helps operators manage grid behavior and system health. It reduces operational bottlenecks linked to aging equipment. Digital twins support predictive maintenance strategies for hydropower and substations. Contractors rely on automation tools to improve safety across construction phases. Improved data access guides planning for new transmission routes. The trend encourages higher project transparency for investors.

Rise of Regional Power Trade Ambitions Driving Transmission Corridor Development

Regional trade ambitions guide transmission expansion within the Angola Power EPC Market. New corridors support future integration with southern African power networks. EPC firms gain steady opportunities for high-voltage line construction and cross-border link upgrades. It enables grid operators to prepare for long-distance load movement. Engineers introduce reinforced conductors to support higher transmission capacity. Several corridors open new access routes for renewable clusters in remote areas. Contractors plan phased construction tailored to regional energy trade frameworks. The trend builds stability for long-term EPC contracting.

Increased Participation of Private Engineering Groups in Utility-Scale Project Delivery

Private engineering firms hold a growing presence across the Angola Power EPC Market. Independent developers secure generation projects backed by diversified financing models. EPC contractors support private-led solar, gas backup and substation programs. It broadens competition and improves project delivery timelines. Private groups adopt global standards that improve installation quality. Several firms expand local teams to support multi-site operations. Vendor partnerships strengthen procurement processes across different project stages. The market trend continues due to strong interest from regional infrastructure investors.

- For instance, private operators installing 1500V solar systems with Huawei or Sungrow utility inverters report BOS cost savings of 8–12% and yield improvements of 1–2% due to extended string lengths and reduced DC losses.

Angola Power EPC Market Challenges Analysis

Infrastructure Limitations and Operational Barriers That Slow Project Execution Timelines

Infrastructure gaps create structural challenges within the Angola Power EPC Market. Many regions lack adequate transport networks that support movement of heavy construction materials. EPC contractors face delays linked to limited port handling capacity for large turbines and transformers. It increases logistical planning complexity for remote project sites. Weather disruptions raise risks for construction scheduling across hydropower zones. Grid bottlenecks hinder integration of new capacity into the national network. Skilled labor shortages limit deployment of advanced systems. Developers face long approval cycles that extend project preparation phases.

Financial Constraints and Regulatory Hurdles That Affect EPC Investment Confidence

Financial limitations remain central to challenges in the Angola Power EPC Market. Several large projects require long-term capital that depends on external funding. EPC firms face uncertainty when tariff adjustments move slowly. It lowers private interest in long-cycle projects. Regulatory clarity varies across provinces, which creates inconsistencies in project planning. Contract structuring often requires lengthy negotiation due to risk allocation concerns. Foreign investors expect stronger payment guarantees for utility-scale projects. Currency fluctuations increase cost pressure for imported equipment.

Market Opportunities

Expansion of Renewable Corridors and Distributed Power Solutions Across Emerging Regions

Growing demand for renewable corridors strengthens opportunity across the Angola Power EPC Market. New solar fields create EPC scope for transmission extensions and substation packages. It supports diversification of power supply across underserved provinces. Distributed solutions gain traction in zones with weak grid coverage. EPC contractors deliver modular systems that reach remote communities faster. Many regions show strong solar potential that supports future hybrid programs. Developers use renewable clusters to stabilize supply in growing towns. Investment interest grows due to lower project risk at smaller scales.

Modernization of Aging Hydropower Assets and Deployment of Advanced Grid Technologies

Hydropower modernization creates long-cycle EPC opportunities within the Angola Power EPC Market. Contractors engage in turbine upgrades, spillway reinforcement and monitoring system deployment. It helps improve efficiency and increase reliable output during peak periods. Grid operators adopt advanced control systems that support better load balancing. EPC firms deliver automated substations with improved protection features. Modernization reduces system losses and strengthens national energy security. Several projects open new roles for local engineering teams. This activity expands future training and technology adoption across the sector.

Angola Power EPC Market Segmentation Analysis:

By Power Generation Segments

Thermal, hydropower and renewable projects form the core generation base of the Angola Power EPC Market, each driving distinct engineering needs. Thermal plants support grid stability during low-water seasons and help maintain reliable output for industrial zones. EPC contractors manage turbine work, boiler systems and fuel-handling structures while developers plan efficiency upgrades that extend plant life. Hydropower remains the dominant segment due to large-scale dams that supply most national electricity. EPC firms handle civil works, powerhouse engineering and evacuation lines that connect remote hydropower sites to major load centers. Renewable energy gains traction as solar fields expand across high-irradiation regions, supported by inverter systems, grid tie-ins and hybrid storage concepts that reduce pressure on hydropower assets. It creates new opportunities for EPC players focused on modular and scalable generation solutions.

- For instance, the GE LM6000 aeroderivative turbine has demonstrated fleet reliability above 99% in heavy industrial duty, with more than 1,300 units deployed globally. The turbine delivers up to 56 MW with fast-start capability under 10 minutes, which supports grid stability during peak load. GE reports efficiency gains of 38–41% in simple-cycle mode, depending on site elevation and ambient temperature.

By Transmission and Distribution Segments

Transmission infrastructure remains essential for strengthening power flow across provinces and supports long-distance evacuation from major hydropower plants. EPC firms design and construct high-voltage corridors, new substations and advanced control systems that improve grid stability. This segment grows with national plans to extend cross-border connectivity and support future regional power trade. Distribution networks form the last critical layer, driving EPC activity across urban and rural zones that seek higher electrification rates. Contractors deliver low-voltage upgrades, feeder extensions and network rehabilitation to reduce losses and improve supply reliability. It supports commercial growth in dense cities and enables rural communities to gain access to stable electricity. Both transmission and distribution segments continue to expand with ongoing modernization programs and rising consumption across Angola.

- For instance, preassembled pole-mounted transformer units reduce on-site labor requirements by 30–40%, accelerating rural electrification timelines. In field deployments, installation windows dropped from several days to under 12 hours in stable terrain. Modular panels also cut wiring errors due to standardized factory assembly.

Segmentation:

By Power Generation

- Thermal

- Hydropower

- Renewables

By Power Transmission and Distribution

- Transmission Infrastructure

- Distribution Networks

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

Northern Angola holds the largest share of the Angola Power EPC Market, accounting for nearly 38–40% due to the concentration of major hydropower assets and transmission expansion programs. Luanda and surrounding provinces drive EPC demand through urban load growth and industrial expansion. It supports continuous grid modernization and new substations across dense consumption areas. Developers focus on upgrading hydropower evacuation routes to strengthen supply stability. The region attracts foreign EPC groups due to its infrastructure scale and investment visibility. Long-term electrification goals reinforce sustained EPC activity here.

Central Angola represents roughly 30–32% of the market share and supports major EPC activity linked to large renewable and hydropower projects. The region benefits from strong resource availability and new corridors that connect generating zones to inland demand centers. It drives multi-phase EPC work involving transmission reinforcement and hybrid generation planning. Developers invest in grid reliability programs to reduce outage frequency. It supports steady project flow for engineering firms engaged in both generation and network upgrades. Growing commercial activity strengthens regional electricity demand.

Southern and Eastern Angola together account for about 28–30% of the market, driven by emerging EPC needs in rural electrification and cross-border transmission planning. These areas support new solar clusters and long-distance line construction that links remote grids to national nodes. It enables EPC contractors to expand modular solutions for communities with limited access. Mining and commercial projects in selected provinces increase power consumption and require network expansion. EPC firms gain opportunities through ongoing government-led electrification programs. Future projects in these regions will strengthen national grid coverage and reduce supply gaps.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Isolux Corsan SA

- Gesto-Energia SA

- Anglo Belgian Corporation

- AEE Power Corporation

- AE Energia

- General Electric Co

- Siemens AG

- Andritz Hydro GmbH

Competitive Analysis:

Competition in the Angola Power EPC Market is shaped by a mix of international EPC firms, regional contractors and global OEMs that supply advanced technologies. Major players such as Isolux Corsan, AEE Power and Gesto-Energia support complex hydropower and transmission projects. It strengthens project execution capabilities across generation and network infrastructure. OEMs such as Siemens AG, General Electric and Andritz Hydro supply turbines, grid automation systems and control technologies that enhance project performance. Local players like AE Energia continue to expand participation in distribution upgrades and electrification projects. Competitive intensity rises as foreign firms partner with local companies to meet technical and regulatory expectations. The market maintains strong momentum due to consistent investment in modernization and expansion programs across provinces.

Recent Developments:

- In June 2024, Aker Solutions secured a long-term frame agreement with Azule Energy for engineering, procurement, and construction services. The deal builds on their Angola track record since 1998, with execution primarily in Luanda and Aberdeen.

Report Coverage:

The research report offers an in-depth analysis based on Power Generation and Power Transmission and Distribution. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Hydropower expansion will continue to anchor long-term EPC activity, supported by large dam upgrades and expanded power evacuation routes.

- Renewable energy zones will gain stronger policy backing, encouraging EPC investment in solar clusters and grid tie-ins across emerging provinces.

- Transmission modernization will strengthen system reliability and increase EPC demand for advanced substations and protection systems.

- Distribution upgrades will accelerate in rural regions to support wider electrification targets and improve service quality.

- Private sector participation will grow through joint ventures that improve technical capability and project execution efficiency.

- Advanced digital tools will guide design optimization and support predictive maintenance strategies across large assets.

- Regional power trade planning will increase demand for high-voltage corridors and cross-border integration works.

- Workforce development programs will expand local engineering capacity, reducing dependence on foreign labor for basic EPC tasks.

- Smart grid components will gain adoption as utilities seek to improve monitoring, control and energy flow management.

- Long-cycle infrastructure commitments will maintain steady EPC project pipelines and support sustained market competitiveness.