Antithrombin Market Overview:

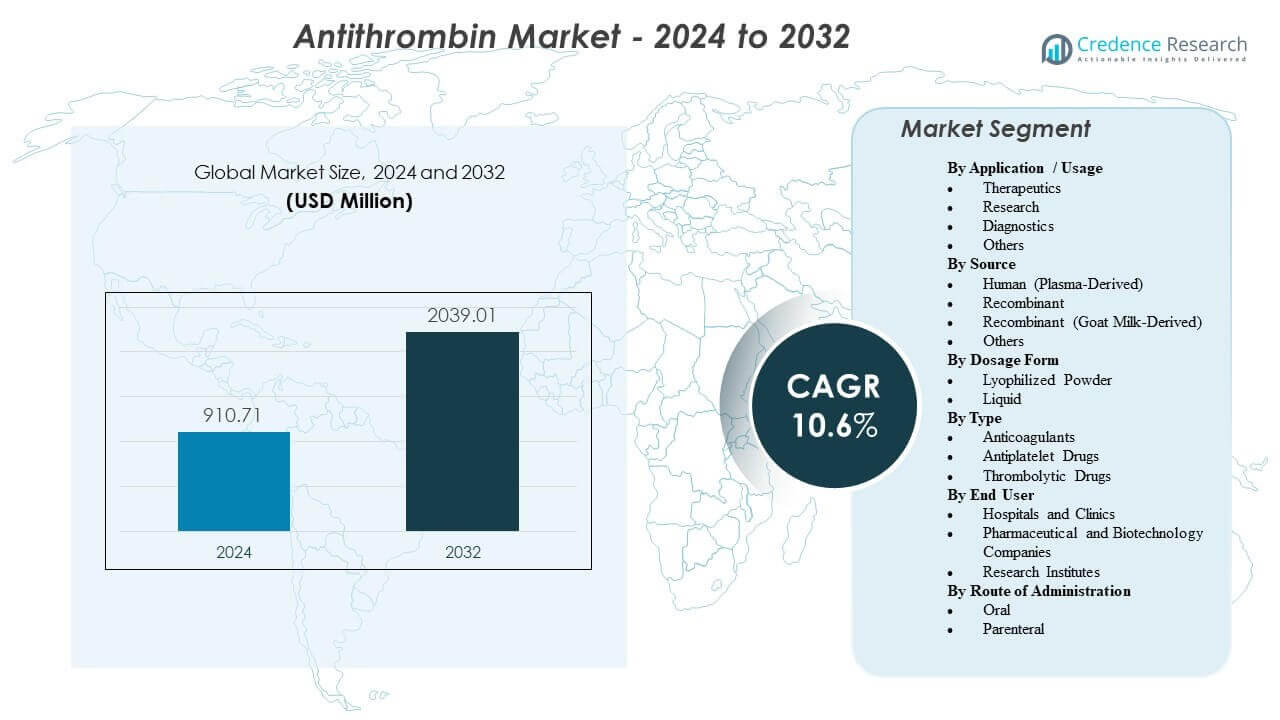

The global Antithrombin Market is projected to increase from USD 910.71 million in 2024 to USD 2,039.01 million by 2032, registering a compound annual growth rate (CAGR) of 10.6% during 2024–2032. This growth trajectory reflects expanding utilization of antithrombin in high-acuity hospital settings, particularly intensive care units (ICUs), complex surgical procedures, and advanced cardiac and respiratory support pathways.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Antithrombin Market Size 2025 |

USD 910.71 million |

| Antithrombin Market, CAGR |

10.6% |

| Antithrombin Market Size 2032 |

USD 2,039.01 million |

North America and Western Europe account for a dominant share of global revenues, supported by mature critical-care infrastructure, standardized treatment algorithms, and strong reimbursement frameworks. Asia-Pacific is emerging as a high-growth region, underpinned by the rapid expansion of tertiary hospitals, improved access to coagulation testing, and rising awareness of thrombotic risk.

Antithrombin Market Insights:

- Demand grows with higher use of ICU care, complex surgeries, and ECMO, where low antithrombin activity can affect anticoagulation control and requires fast correction in monitored settings.

- Better diagnosis of hereditary antithrombin deficiency and wider thrombosis-risk screening increase planned use during high-risk periods like surgery, pregnancy, and prolonged immobility.

- Supply dependence on plasma-derived sources, strict quality controls, and high treatment costs can limit availability and drive tight hospital stewardship on when antithrombin is used.

- North America and Western Europe lead due to advanced critical-care pathways and strong hospital procurement, while Asia-Pacific is emerging as tertiary hospitals expand and access to coagulation testing improves.

Antithrombin Market Drivers:

Robust Clinical Demand in High-Risk Hospital Settings

Antithrombin usage is expanding in high-acuity hospital environments where thrombosis risk is elevated and rapid correction of coagulation imbalances is essential. ICUs, operating rooms, trauma centers, and sepsis management pathways increasingly rely on antithrombin replacement when reduced antithrombin levels heighten clot risk or impair response to heparin and other anticoagulants.

The ongoing expansion of intensive care capacity supports consistent demand for specialty plasma proteins, including antithrombin. Treatment protocols in critical care and perioperative management are designed to achieve rapid stabilization, reinforcing the integration of antithrombin into acute care workflows when clinically indicated.

- For example, Werfen’s ROTEM® sigma point-of-care viscoelastic system is reported to deliver a comprehensive coagulation status overview from whole blood samples in approximately 10 minutes, facilitating protocol-driven decision-making in operating rooms, ICUs, and emergency departments, where antithrombin may be incorporated into broader coagulation-correction strategies.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Rising Incidence and Improved Recognition of Hereditary Antithrombin Deficiency and VTE Risk

Advances in genetic and thrombophilia screening are enhancing detection of hereditary antithrombin deficiency, particularly among patients presenting with early-onset or recurrent venous thromboembolism (VTE). Increased awareness among hematologists and thrombosis specialists supports earlier diagnosis, risk stratification, and structured follow-up.

Antithrombin supplementation is increasingly used in high-risk phases such as surgery, pregnancy, and extended immobilization in patients with established deficiency. Family-based screening and long-term preventive planning in affected lineages expand the underlying base of medically justified demand.

- For instance, Illumina’s NovaSeq X Plus platform is specified with an approximate 25B flow cell capacity, enabling sequencing of ~64 human genomes or ~750 exomes per flow cell (with output around ~8–10.5 Tb for 2 × 150 bp). Such high-throughput genetic workflows can support systematic thrombophilia evaluation and confirmatory testing in appropriately selected patients.

Expansion of ECMO, Cardiopulmonary Bypass, and Advanced Procedures Impacting Coagulation Control

The growing use of ECMO, cardiopulmonary bypass, and other advanced organ-support and interventional platforms is placing additional emphasis on precise anticoagulation management. These procedures can consume antithrombin and destabilize anticoagulation control, particularly in patients requiring high-intensity heparin therapy.

In tertiary and quaternary care centers, antithrombin replacement is increasingly used to restore heparin responsiveness and maintain safe anticoagulation thresholds under tightly monitored conditions. As more cardiac, respiratory, and transplant programs are established, routine stocking and protocolized use of antithrombin are expected to expand, lifting baseline demand.

Ongoing Need for Targeted, Rapid-Acting Biologics in Bleeding and Thrombosis Pathways

Antithrombin occupies a targeted and well-defined role within coagulation management, fitting clinical strategies that aim to avoid broad or prolonged systemic anticoagulant exposure. Rapid onset of action and the ability to titrate treatment against measurable laboratory targets support its adoption in hospital environments.

Providers prioritize biologic therapies that align with coagulation monitoring systems, electronic pathways, and specialist oversight. While oral anticoagulants address many chronic thrombotic conditions, they do not substitute for antithrombin’s function in acute, high-risk scenarios where targeted replacement is required. This clinical differentiation supports recurring procurement by large hospitals and specialized centers.

Antithrombin Market Trends and Opportunities:

Strengthening of Supply Chains and Expansion of Fractionation and Biologics Capacity

Manufacturers are investing in expanded plasma collection networks, improved fractionation efficiency, and reinforced quality systems to mitigate the risk of supply disruptions. Health systems increasingly favor suppliers that demonstrate robust capacity, diversified sourcing strategies, and reliable lead times for critical-care biologics.

Regional production capabilities and long-term plasma procurement agreements are emerging as key competitive differentiators. Strategic partnerships and contracts that secure access to plasma inputs and biologics manufacturing capacity create opportunities to strengthen market position, especially in regions prioritizing uninterrupted access to antithrombin.

Growing Preference for Standardized Dosing Protocols and Stewardship-Supported Use

Hospitals are expanding the use of standardized anticoagulation and coagulation management pathways to minimize variability and adverse events. Antithrombin is well suited to such frameworks when dosing is linked to measurable activity levels, patient-specific targets, and diagnostic algorithms.

Vendors that offer protocol-development support, clinician education, and integrated data tools can drive higher adoption and more consistent use. Enhanced integration with laboratory workflows and point-of-care diagnostics further accelerates decision-making. This environment creates opportunities for manufacturers to differentiate through value-added clinical and stewardship support programs.

Broader Use in Complex Care Episodes with Heparin Resistance or Consumptive Coagulopathy

Inflammation-driven coagulopathy and heparin resistance are increasingly observed in high-acuity ICU settings, including cases involving severe infection, trauma, ECMO, and advanced surgical interventions. When antithrombin levels are low, heparin resistance may necessitate targeted replacement therapy to restore effective anticoagulation.

Centers with high case volumes in ECMO, transplant, major trauma, and complex cardiovascular surgery are key demand hubs. Antithrombin products that provide rapid and predictable correction of antithrombin activity can gain preference in these settings, particularly when supported by robust clinical data and clear dosing guidance.

Innovation in Product Formats, Presentation, and Support Services

Product innovation is focusing on formats that reduce preparation time, simplify administration, and minimize dosing errors. Ready-to-use presentations, optimized packaging, and flexible storage conditions are increasingly valued by hospital pharmacies and nursing teams.

Enhanced pharmacovigilance, product traceability, and training services help providers meet regulatory and compliance requirements. Manufacturers are also exploring new indications, expanded label claims, or supportive evidence in specialized patient populations to reinforce clinical value. Such initiatives strengthen differentiation beyond price and improve competitiveness in tender-based purchasing environments.

Antithrombin Market Challenges Analysis:

Dependence on Plasma-Derived Inputs and Stringent Quality Requirements

A significant proportion of antithrombin products remain plasma-derived, exposing supply to fluctuations in donor availability, collection volume, and processing constraints. Plasma fractionation is technically complex and subject to rigorous regulatory and quality requirements, limiting the speed at which capacity can be scaled.

Any disruption in plasma collection, testing, or manufacturing can result in localized or regional shortages, quickly felt in hospital settings. Compliance with evolving quality and safety standards adds cost and can extend timelines for product scale-up or facility expansion. These structural constraints may sustain pressure on both pricing and availability.

- For example, Grifols reports operating approximately 400 plasma donation centers supported by six plasma testing laboratories and processing over 14 million plasma donations annually. This scale underscores the dependence on continuous donor throughput and extensive quality-testing infrastructure prior to fractionation.

High Treatment Costs, Utilization Controls, and Competition from Alternative Pathways

Antithrombin therapy is associated with high acquisition costs, prompting payers and hospital pharmacy committees to implement strict utilization criteria and stewardship protocols. Use is often restricted to clearly defined, protocol-backed indications, with scrutiny on dosing, wastage, and adherence to guidelines.

In certain clinical scenarios, teams may favor alternative anticoagulation or antithrombotic strategies, particularly when budgetary constraints are significant or when evidence for antithrombin’s incremental benefit is perceived as limited. Variability in guideline adoption across smaller or resource-limited hospitals can further temper uptake.

- For instance, Pfizer’s ELIQUIS (apixaban) ARISTOTLE trial, involving 18,201 patients, reported relative reductions versus warfarin of 21% in stroke/systemic embolism, 31% in major bleeding, and 11% in mortality. Such outcomes support strong positioning of non-antithrombin anticoagulants in formulary decisions, indirectly influencing resource allocation and prescribing patterns.

Antithrombin Market Segmentation Analysis:

By Application / Usage

The antithrombin market demonstrates clear demand concentration in the Therapeutics segment, which represents the dominant share of global revenue. Therapeutic use is primarily driven by antithrombin replacement in high-risk clinical settings, including intensive care units, perioperative management, ECMO support, and complex cardiovascular procedures. In these environments, maintaining adequate antithrombin activity is critical to ensuring effective anticoagulation and mitigating thrombotic complications. The growing adoption of protocol-based coagulation management further reinforces therapeutic demand.

The Research segment contributes a smaller but strategically important share, supported by ongoing studies in coagulation biology, thrombophilia, assay development, and bioprocess optimization. Academic institutions, biotechnology companies, and contract research organizations utilize antithrombin in experimental and translational research applications.

The Diagnostics segment supports laboratory workflows focused on measuring antithrombin activity, evaluating clotting function, and monitoring treatment response. Increased thrombophilia screening and companion diagnostic development are strengthening the relevance of this segment. The Others category encompasses educational use, quality control materials, and specialized validation applications.

By Source

Human (Plasma-Derived) antithrombin products account for the majority of market revenue, reflecting longstanding clinical use, physician familiarity, and well-established safety and efficacy data. These products are deeply integrated into hospital formularies and critical-care pathways, particularly in North America and Europe.

Recombinant antithrombin represents a strategically important growth segment, offering advantages in supply stability, scalability, and reduced dependency on plasma collection. As healthcare systems prioritize supply-chain resilience, recombinant technologies are expected to gain incremental share over the forecast period.

Recombinant (Goat Milk-Derived) antithrombin remains a niche but differentiated segment, attracting attention in markets seeking diversified biologics production platforms. The Others category includes emerging expression systems and limited-use or region-specific variants that may gain relevance as manufacturing technologies evolve.

By Dosage Form

Lyophilized powder formulations currently dominate the market due to extended shelf life, storage flexibility, and controlled reconstitution in hospital pharmacies. These characteristics align with institutional inventory management practices and bulk procurement strategies.

Liquid formulations are gaining traction in acute-care environments where speed of preparation and administration is critical. Ready-to-use presentations reduce preparation time and may minimize dosing variability, making them particularly attractive in emergency and ICU settings. Over the forecast period, incremental growth in liquid formats is anticipated as hospitals prioritize workflow efficiency.

By Type

Within the broader classification, anticoagulants represent the leading segment, as antithrombin directly supports anticoagulation pathways and enhances heparin responsiveness in high-risk patients. Its role is particularly significant in conditions characterized by heparin resistance or consumptive coagulopathy.

Antiplatelet drugs and thrombolytic drugs occupy adjacent positions in overall thrombosis management; however, they serve different mechanistic purposes and do not substitute for antithrombin replacement in deficiency states. As such, anticoagulant-related applications maintain clear dominance within the antithrombin-specific market context.

By End User

Hospitals and clinics constitute the largest end-user segment, accounting for the majority of global consumption. Demand is concentrated in tertiary and quaternary care centers with established ICU capacity, advanced surgical programs, and cardiac or transplant services. Structured procurement systems and adherence to standardized treatment protocols further consolidate hospital dominance in this segment.

Pharmaceutical and biotechnology companies represent an additional end-user category, utilizing antithrombin in drug development, biologics manufacturing processes, and assay validation. Research institutes also contribute to demand through academic and translational studies in hemostasis and thrombosis.

By Route of Administration

Parenteral administration overwhelmingly dominates the market, reflecting the need for rapid, controlled, and predictable delivery in acute and high-risk clinical settings. Intravenous infusion allows precise titration of antithrombin activity and aligns with existing hospital anticoagulation protocols.

Oral administration remains negligible within the antithrombin market, given the molecular characteristics of the protein and the absence of established oral formulations. Consequently, growth across the forecast period will remain closely aligned with parenteral delivery in institutional healthcare settings.

Regional Analysis:

North America is expected to lead the global Antithrombin Market in 2024, accounting for approximately 42.7% of revenue. The region benefits from advanced hospital infrastructure, high diagnosis rates for coagulation disorders, and consistent demand generated by complex surgical procedures and critical-care pathways. The United States is the primary contributor, supported by strong access to specialized care and well-established plasma-product supply chains.

Europe represents around 29.3% of the market in 2024, underpinned by structured healthcare systems, high penetration of plasma-derived therapies, and comprehensive coverage of hematology and perioperative care. Germany, France, and the United Kingdom anchor regional demand due to robust critical-care capacity and established reimbursement frameworks.

Asia-Pacific accounts for approximately 20.0% of the market and is anticipated to exhibit the fastest growth. Key drivers include expanding tertiary-care infrastructure, increasing availability of coagulation diagnostics, and rising awareness of thrombosis and hereditary disorders. Major markets such as China, Japan, India, and South Korea are expected to play significant roles in regional expansion.

Latin America holds an estimated 6.2% share in 2024, led by Brazil and Mexico, where adoption is increasing in larger hospitals and specialty centers. In the Middle East & Africa, which account for about 1.8% of global revenue, demand is concentrated in Gulf Cooperation Council (GCC) countries and South Africa, often linked to tertiary hospitals and private-sector facilities.

Key Player Analysis:

- CSL Limited

- Grifols, S.A.

- Takeda Pharmaceutical Company Limited

- Octapharma AG

- LFB USA

- Kedrion S.p.A.

- Lee Biosolutions

- Scripps Laboratories

- rEVO Biologics, Inc.

- Thermo Fisher Scientific

- Siemens Healthcare GmbH

- Diapharma Group, Inc.

Competitive Analysis:

The Antithrombin Market is moderately concentrated, with leading positions held by plasma-derived specialists that maintain strong hospital and tender-based channels. CSL, Grifols, Takeda, Octapharma, and LFB are among the key players frequently referenced in hospital formularies and procurement frameworks.

Competitive differentiation is largely driven by access to plasma, fractionation and biologics capacity, quality and regulatory compliance, and the strength of institutional relationships. Product portfolio breadth, including multiple presentations and complementary coagulation products, further influences buyer preference, particularly in large hospital systems.

Manufacturers protect and grow market share through robust distribution networks, extensive regional registrations, and investments in recombinant antithrombin to enhance supply resilience. In Latin America and the Middle East & Africa, partnerships with local distributors and hospital groups are critical to overcoming access barriers and logistics constraints.

Companies that combine reliable supply, comprehensive protocol support, strong pharmacovigilance, and value-added education typically secure longer-term contracts with acute-care providers and integrated health systems.

Recent Developments:

- In November 2025, Grifolsreported that the U.S. FDA approved an expanded indication for Thrombate III (antithrombin III [human]) to include pediatric patients with hereditary antithrombin deficiency (hATd), describing it as the first and only antithrombin concentrate approved for both adult and pediatric patients with hATd

- In April 2025, Siemens Healthineersannounced FDA clearance of its Innovance Antithrombin assay for a new claim enabling its use as a companion diagnostic test for people receiving Qfitlia (fitusiran), and noted the test supports monitoring AT activity to support Qfitlia dosing in eligible adult and pediatric patients.

- In March 2025, Sanofiannounced that the U.S. FDA approved Qfitlia (fitusiran) for routine prophylaxis to prevent or reduce bleeding episodes in adults and pediatric patients (12+) with hemophilia A or B (with or without inhibitors), positioning it as the first antithrombin-lowering therapy in hemophilia.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage:

The research report offers an in-depth analysis based on Application / Usage, Source, Dosage Form, Type, End User, and Route of Administration. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years.

The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Report Scope

| Report Attribute |

Details |

| Market size value in 2024 |

USD 910.71 million |

| Revenue forecast in 2032 |

USD 2,039.01 million |

| Growth rate (Revenue) |

CAGR of 10.6% from 2024 to 2032 |

| Base year for estimation |

2024 |

| Historical data |

2022 – 2023 |

| Forecast period |

2024 – 2032 |

| Quantitative units |

Revenue in USD million, CAGR from 2024 to 2032 |

| Report coverage |

Revenue forecast, market segmentation, company profiling, competitive landscape, growth drivers, challenges, trends, regional analysis, and strategic recommendations |

| Segments covered |

Application / Usage, Source, Dosage Form, Type, End User, Route of Administration, Region |

| Regional scope |

North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Country scope |

U.S.; Canada; Germany; France; UK; Italy; Spain; China; Japan; India; South Korea; Brazil; Mexico; GCC Countries; South Africa |

| Key companies profiled |

CSL Limited; Grifols, S.A.; Takeda Pharmaceutical Company Limited; Octapharma AG; LFB USA; Kedrion S.p.A.; Lee Biosolutions; Scripps Laboratories; rEVO Biologics, Inc.; Thermo Fisher Scientific; Siemens Healthcare GmbH; Diapharma Group, Inc. |

| Customization scope |

Customization available based on specific country, regional, and segment requirements, including additional company profiling and deeper regional analysis |

| Pricing and purchase options |

Customized purchase options available based on research scope and licensing requirements |

Segmentation:

By Application / Usage

- Therapeutics

- Research

- Diagnostics

- Others

By Source

- Human (Plasma-Derived)

- Recombinant

- Recombinant (Goat Milk-Derived)

- Others

By Dosage Form

- Lyophilized Powder

- Liquid

By Type

- Anticoagulants

- Antiplatelet Drugs

- Thrombolytic Drugs

By End User

- Hospitals and Clinics

- Pharmaceutical and Biotechnology Companies

- Research Institutes

By Route of Administration

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa