Artemisinin Combination Therapy Market Overview:

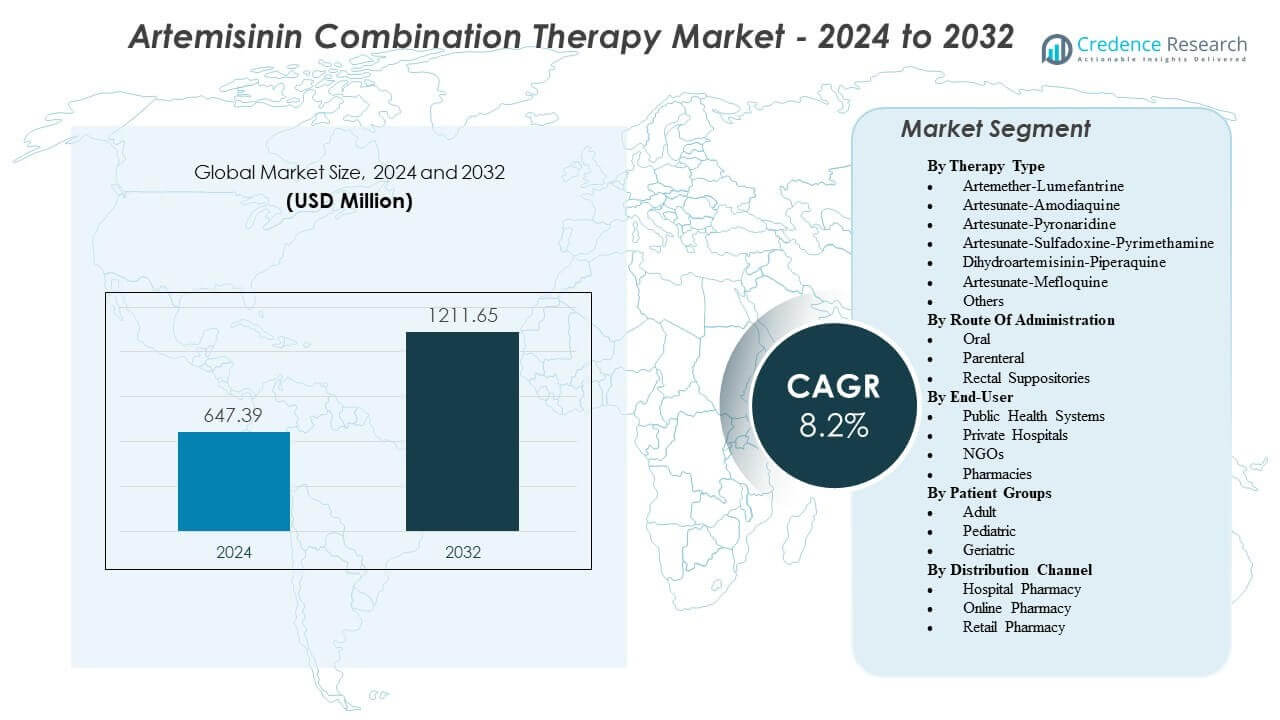

The Artemisinin Combination Therapy Market is projected to grow from USD 647.39 million in 2024 to an estimated USD 1211.65 million by 2032, with a compound annual growth rate (CAGR) of 8.2% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Artemisinin Combination Therapy Market Size 2024 |

USD 647.39 million |

| Artemisinin Combination Therapy Market, CAGR |

8.2% |

| Artemisinin Combination Therapy Market Size 2032 |

USD 1211.65 million |

Rising malaria incidence in endemic settings continues to drive ACT utilization through primary care and community channels. National programs expand test-and-treat coverage, which increases confirmed-case treatment volumes and supports routine replenishment. Health systems also strengthen stewardship to reduce monotherapy use and improve adherence to full treatment courses. Wider access to rapid diagnostic tests supports appropriate dispensing and reduces unnecessary use. Pediatric care needs raise demand for dispersible tablets and weight-band packs that simplify dosing. Supply reliability and quality documentation remain key purchase criteria in tender-driven procurement.

Artemisinin Combination Therapy Market Insights:

- Public tenders and donor-funded procurement expand test-and-treat coverage, which increases confirmed-case treatment volumes and supports steady replenishment.

- Pediatric-friendly formats, weight-band packs, and wider rapid diagnostic test use improve correct dosing and strengthen adherence in community care.

- Resistance pressure, weak adherence in some settings, and counterfeit risk in fragmented private channels can reduce regimen confidence and complicate supply planning.

- Sub-Saharan Africa leads demand due to high malaria burden and large public-sector distribution, while India and parts of Southeast Asia show growth as surveillance and access programs expand.

Artemisinin Combination Therapy Market Drivers

Expanding Public Procurement And Donor-Funded Treatment Coverage Programs

National malaria programs purchase large ACT volumes through tenders and multi-year supply contracts, which supports predictable demand. Donor funding sustains these purchases and strengthens annual order planning across endemic countries. Health ministries expand test-and-treat pathways, which increases the number of confirmed cases that receive therapy. Public clinics rely on standard first-line regimens for fast fever case management and consistent prescribing. The Artemisinin Combination Therapy Market benefits when procurement teams widen facility coverage and maintain stronger buffer stocks. Better distribution planning reduces stockouts and protects treatment continuity in remote districts. Quality assurance requirements also push buyers toward compliant manufacturers with reliable batch documentation. These combined factors keep baseline demand steady even when transmission patterns vary by season.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Rising Burden In High-Transmission Settings And Persistent Vulnerable Populations

High transmission zones continue to report repeated malaria episodes, which sustains routine ACT use in frontline care. Children under five and pregnant women account for a large share of treated cases in many endemic settings. Clinicians prefer fixed-dose combinations that simplify dosing and reduce misuse at household level. It supports adherence when caregivers manage therapy after a clinic visit and follow pack instructions. Community health worker networks extend access and raise treated case counts in rural communities. Wider use of rapid diagnostic tests increases confirmed detection and supports appropriate dispensing. Health campaigns also promote early care-seeking, which reduces delays and improves clinical confidence. These drivers keep consumption volumes strong in high-burden districts and peri-urban areas.

- For instance, a Reuters report said Codix Bio and SD Biosensor planned local output with initial capacity of 147 million malaria and HIV test kits per year, which can lift confirmed diagnosis volume in high-burden settings

Guideline Alignment And Stewardship Efforts That Protect Clinical Confidence

Many countries align national malaria protocols with global treatment guidance, which supports consistent prescribing across care levels. This alignment improves clinician confidence and reduces variation between facilities and regions. Stewardship actions limit monotherapy use and promote correct dosing, which helps protect treatment performance. It reduces failure risk linked to partial courses, wrong regimens, or poor adherence. Training programs reinforce weight-based dosing and strengthen counseling for caregivers of pediatric patients. Supportive supervision improves compliance in peripheral facilities and outreach clinics. Standardized patient records help track outcomes and guide regimen use over time. These systems maintain trust in ACTs and support stable procurement and replenishment cycles.

Formulation Improvements That Support Pediatric Use And Wider Access Points

Pediatric-friendly formulations improve acceptance and make dosing easier for caregivers in low-resource settings. Dispersible tablets support accurate dosing and help children take therapy when swallowing tablets proves difficult. Unit-dose packs reduce confusion and improve the likelihood of course completion at home. It lowers missed doses and supports better perceived outcomes in routine practice. Manufacturers pursue registrations for multiple strengths to match national weight-band protocols. Programs prefer clear labeling and local language instructions to improve safe use. Heat-stable packs also support field storage where temperature control remains limited. These product features strengthen uptake across public clinics, outreach programs, and private pharmacies.

- For instance, Novartis received approval for Coartem Baby for infants weighing 2–5 kg and reported more than 1.1 billion antimalarial treatment courses delivered since 1999, which shows both dosing precision and long-run supply execution.

Artemisinin Combination Therapy Market Trends

Shift Toward More Granular Resistance Surveillance And Data-Driven Treatment Choices

Endemic countries expand therapeutic efficacy studies and molecular marker surveillance to track performance across regions. Data from sentinel sites guides policy teams on where current regimens remain effective and where risk rises. The Artemisinin Combination Therapy Market sees demand mix shift when national programs adjust first-line choices by geography. It supports more frequent guideline reviews and faster updates when new evidence appears. Laboratories adopt standardized methods to improve comparability across sites and time periods. Donors also request stronger post-market reporting to link procurement with field outcomes. Manufacturers respond by strengthening evidence packages and maintaining clearer batch and quality documentation. This trend changes product mix shares even when total treatment volumes remain stable.

- For instance, Novartis and MMV reported the Phase III KALUMA study enrolled 1,688 patients across 34 sites in 12 African countries, which shows how large trials now support evidence-led policy.

Growing Preference For Child-Centered Packaging And Simplified Dosing Experiences

Public buyers increase focus on child-appropriate dosage forms and pack formats that match weight-band dosing. Caregivers prefer packs with simple instructions and clear visuals, which improves correct use at home. It lowers confusion during multi-day dosing and supports higher completion rates. Pharmacovigilance teams also value packs that reduce accidental underdosing and repeat visits. Suppliers redesign leaflets and pictograms to work in low-literacy settings and rural communities. Programs request smaller pack sizes to support community-level dispensing and outreach care. Private pharmacies stock user-friendly formats to meet retail demand from travelers and urban buyers. This packaging trend supports brand preference beyond price competition.

Higher Focus On Supply Security Through Regional Manufacturing And Dual-Sourcing

Procurement agencies place higher weight on supply resilience due to past shocks in logistics and raw material availability. Tender documents increasingly favor dual-sourcing plans and backup production capacity for critical SKUs. It encourages regional finishing, secondary packaging, and local manufacturing partnerships in selected markets. Quality audits expand beyond finished goods to cover upstream suppliers and subcontractors. Manufacturers build redundancy for key inputs and packaging materials to protect delivery schedules. Some buyers offer longer contract terms to secure stable capacity and reduce emergency orders. Warehousing partners improve inventory visibility and batch traceability to support program reporting. This trend raises emphasis on reliability and compliance over short-term price alone.

Stronger Integration Of Pharmacovigilance And Digital Track-And-Trace Tools

National programs adopt digital tools to record dispensing, batch numbers, and patient outcomes in near real time. It supports faster quality investigations and improves recall readiness when issues arise. Track-and-trace pilots also help detect diversion and reduce counterfeit exposure in fragmented private channels. Donors encourage digital reporting to strengthen accountability and program performance monitoring. Manufacturers align labeling, serialization, and data formats to meet tender and regulator requirements. Health workers use mobile tools to capture adverse event reports and improve follow-up. Data systems also help measure adherence patterns and guide patient counseling improvements. This trend improves transparency across procurement, distribution, and clinical use.

- For instance, a Ghana pilot with mPedigree labeled 3,500 boxes of an anti-malarial medicine for SMS-based authentication, which shows how verification systems can support quality control.

Artemisinin Combination Therapy Market Challenges Analysis

Rising Threat Of Drug Resistance And The Need For Timely Policy Shifts

Drug resistance risk creates uncertainty for long-term regimen planning in parts of Asia and selected African settings. Health authorities must revise protocols when efficacy studies show declining cure rates for a given combination. The Artemisinin Combination Therapy Market faces mix volatility when countries shift first-line regimens and update procurement lists. It increases pressure on suppliers to scale alternative combinations quickly while maintaining quality and continuity. Delays in policy updates can increase failure risk and weaken confidence at facility level. Resistance hotspots also require stronger stewardship to prevent misuse, partial dosing, and informal monotherapy access. Cross-border movement complicates control and makes surveillance coverage harder to maintain. These factors raise operational complexity for programs, suppliers, and regulators.

Quality Risks, Counterfeits, And Procurement Pressures Across Fragmented Channels

Counterfeit or substandard antimalarials remain a concern in markets with weaker oversight and complex distribution routes. It can reduce trust in therapy performance and complicate clinical decisions for fever management. Intense tender price pressure may limit supplier margins and reduce incentives to hold capacity buffers. Lengthy registrations and slow dossier reviews can delay access to new strengths and updated pack formats. Import processes, customs delays, and last-mile constraints can disrupt deliveries to remote districts. Harsh storage conditions can also harm product quality when handling lacks adequate controls. Fragmented private channels can bypass supervision and reduce pharmacovigilance reporting. These challenges require strict quality systems, stronger enforcement, and better supply governance.

Market Opportunities

Next-Generation Regimens And Combination Innovation To Protect Long-Term Efficacy

Endemic countries seek therapy options that retain high cure rates in areas with resistance pressure and changing parasite profiles. The Artemisinin Combination Therapy Market can expand through new combinations that meet evolving national guidance and program needs. It creates space for suppliers that build strong clinical evidence and maintain rapid scale-up plans. Fixed-dose innovations can simplify dosing and reduce misuse in community settings with limited supervision. Products that improve tolerability can support better adherence and fewer repeat visits. Developers can partner with global health groups to speed adoption and strengthen access pathways. Local studies can help align products with regional transmission patterns and patient needs. These pathways open value beyond volume growth and support long-term market stability.

Digital Health Linkages That Improve Forecasting, Adherence, And Patient Follow-Up

Digital case records can strengthen demand forecasting, reduce emergency procurement, and improve facility-level stock planning. It supports better replenishment decisions at district and clinic level with fewer stockouts and expiries. SMS reminders and caregiver education tools can improve course completion and correct dosing at home. Pharmacy systems can flag repeat visits and support referral when symptoms persist after treatment. Supply chain analytics can reduce wastage and improve allocation across high-burden districts. Verification tools can lower counterfeit exposure in retail channels with fragmented distribution. Public-private data sharing can improve visibility across mixed supply systems and support faster response. These tools create new service layers that complement core drug sales and procurement demand.

Artemisinin Combination Therapy Market Segmentation Analysis:

By Therapy Type

Artemether-Lumefantrine leads first-line use in many national protocols due to broad adoption and strong supply. Artesunate-Amodiaquine remains important where cost control and public tenders drive selection. Dihydroartemisinin-Piperaquine gains preference in some settings due to convenient dosing and post-treatment protection. Artesunate-Pyronaridine supports use cases where programs seek alternatives under efficacy pressure. Artesunate-Sulfadoxine-Pyrimethamine serves select policy pathways and specific local practices. Artesunate-Mefloquine holds value in limited geographies that maintain this regimen. Others cover niche combinations and country-specific selections.

- For instance, DNDi noted ASAQ fixed-dose presentations that enable 1 tablet once daily for 3 days for infants and children, which reduces dosing complexity in the field.

By Route Of Administration

Oral therapy dominates routine outpatient care and supports rapid scale through primary facilities. Parenteral use serves severe cases and hospital protocols that require fast therapeutic action. Rectal suppositories address pre-referral care where injections are not feasible and access remains limited.

- For instance, WHO prequalified Guilin Pharmaceutical’s artesunate 60 mg powder for injection, which supports quality-assured hospital supply for severe cases

By End-User

Public health systems drive the largest volumes through tenders, free care, and national malaria programs. Private hospitals treat urban and insured patients and prefer assured availability and clinical support. NGOs strengthen last-mile reach through campaigns and community programs. Pharmacies serve self-pay demand and refill needs where regulations allow.

By Patient Groups

Adult patients form a major share in routine case management and workplace exposure settings. Pediatric demand remains critical due to high incidence and the need for child-friendly dosing. Geriatric use is smaller but requires careful dosing oversight due to comorbidities.

By Distribution Channel

Hospital pharmacy channels support inpatient protocols and severe case care. Retail pharmacy channels serve walk-in treatment access in mixed public-private systems. Online pharmacy channels remain limited in many endemic markets but expand where regulation and e-prescription systems mature.

Segmentation:

By Therapy Type

- Artemether-Lumefantrine

- Artesunate-Amodiaquine

- Artesunate-Pyronaridine

- Artesunate-Sulfadoxine-Pyrimethamine

- Dihydroartemisinin-Piperaquine

- Artesunate-Mefloquine

- Others

By Route Of Administration

- Oral

- Parenteral

- Rectal Suppositories

By End-User

- Public Health Systems

- Private Hospitals

- NGOs

- Pharmacies

By Patient Groups

- Adult

- Pediatric

- Geriatric

By Distribution Channel

- Hospital Pharmacy

- Online Pharmacy

- Retail Pharmacy

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America holds 40.17% share, supported by malaria R&D capacity, strong quality standards, and steady demand for travel-related treatment. Major buyers also support global health partnerships that fund procurement and product development for endemic regions.

Europe accounts for 28.71% share, driven by strict regulatory oversight and consistent institutional purchasing. European demand also reflects humanitarian supply roles and financing support for large malaria programs abroad.

Asia Pacific represents 25.08% share, backed by artemisinin supply chains and large-scale pharmaceutical production in countries like China and India. Latin America contributes 3.80% share, with demand tied to elimination efforts in Brazil, Peru, and Colombia. Middle East and Africa holds 2.24% share in this dataset, supported by donor-funded access programs and community distribution in select countries.

In high-burden African settings, procurement often runs through centralized tenders and partner-funded supply mechanisms. Program scale and last-mile delivery capacity influence how quickly facilities convert budgets into treatment coverage. Asia Pacific growth links to Artemisia annua cultivation, extraction capacity, and strong export networks for artemisinin derivatives.

Price cycles for vegetal artemisinin can affect margins and supply confidence across manufacturers and buyers. Europe and North America also shape demand through research pipelines, regulatory pathways, and funding for quality-assured products. Latin America demand remains smaller but benefits from surveillance, targeted treatment campaigns, and cross-border control programs. Overall regional performance depends on malaria incidence, procurement speed, and reliable product availability across public channels.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Novartis AG

- Cipla Ltd.

- Ipca Laboratories Ltd.

- Ajanta Pharma Ltd.

- Sanofi S.A.

- KPC Pharmaceuticals, Inc.

- Guilin Pharmaceutical Co., Ltd.

- Bliss GVS

- Shanghai Fosun Pharmaceutical Group Co., Ltd.

- Shin Poong Pharmaceutical Co., Ltd.

- Kunming Pharmaceutical Corp.

- Mylan N.V. / Viatris, Inc.

- Reddy’s Laboratories Ltd.

Competitive Analysis:

The Artemisinin Combination Therapy Market remains moderately fragmented, with global brands and high-volume generics competing across public tenders and institutional channels.

Large suppliers prioritize quality credentials because donor-funded buyers often require strict quality assurance alignment. Novartis strengthens differentiation through WHO-prequalified Coartem dosage options that support public-sector procurement needs. Indian manufacturers such as Cipla, Ipca, Ajanta, and Dr. Reddy’s focus on scale, cost control, and broad registrations to win tenders. Chinese producers and groups such as Guilin and Fosun support supply through API access and large manufacturing capacity.

Recent Developments:

- In November 2025, Novartis, in partnership with Medicines for Malaria Venture (MMV), announced positive Phase III results from the KALUMA trial for KLU156 (ganaplacide-lumefantrine), the first novel non-artemisinin combination treatment (NACT) in decades, achieving high efficacy against resistant malaria parasites.

- In July 2025, Novartis received approval for Coartem Baby (AL dispersible), the first artemisinin-based combination therapy specifically formulated for infants weighing 2 to 5 kg, addressing a critical treatment gap for young children in malaria-endemic regions.

- In May 2025, Bliss GVS Pharma donated over GH₡ 250,000 worth of ACT medicines, including brands like Lonart and P-Alaxin, to health facilities in Ghana under its “Act for Africa: Malaria-Free Continent Campaign.

Report Coverage:

The research report offers an in-depth analysis based on Therapy Type, Route Of Administration, End-User, Patient Groups, and Distribution Channel. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Public tenders, pooled purchasing, and donor procurement will keep baseline demand stable across high-burden malaria countries.

- Resistance surveillance will reshape regimen choices by geography and reward suppliers that can support faster policy switches.

- Pediatric dispersible formats and clearer dosing packs will gain share as programs push adherence and caregiver confidence.

- Supply security efforts will favor dual-sourcing, regional packaging, and stronger buffer stocks to protect seasonal peaks.

- Digital dispensing records will improve forecasting, reduce expiries, and support more accurate facility replenishment cycles.

- Track-and-trace rollouts will tighten quality control, deter diversion, and reduce counterfeit exposure in fragmented channels.

- New combination options and optimized dosing schedules will expand choice where ministries seek alternatives under efficacy pressure.

- Partnerships with NGOs and community health workers will broaden last-mile reach through outreach care and pre-referral support.

- Private pharmacies will grow in influence in mixed systems where self-pay access complements public distribution networks.

- Manufacturers will compete on on-time delivery, audit readiness, pharmacovigilance support, and consistent documentation for tenders.