Atrial Fibrillation Surgery Market Overview:

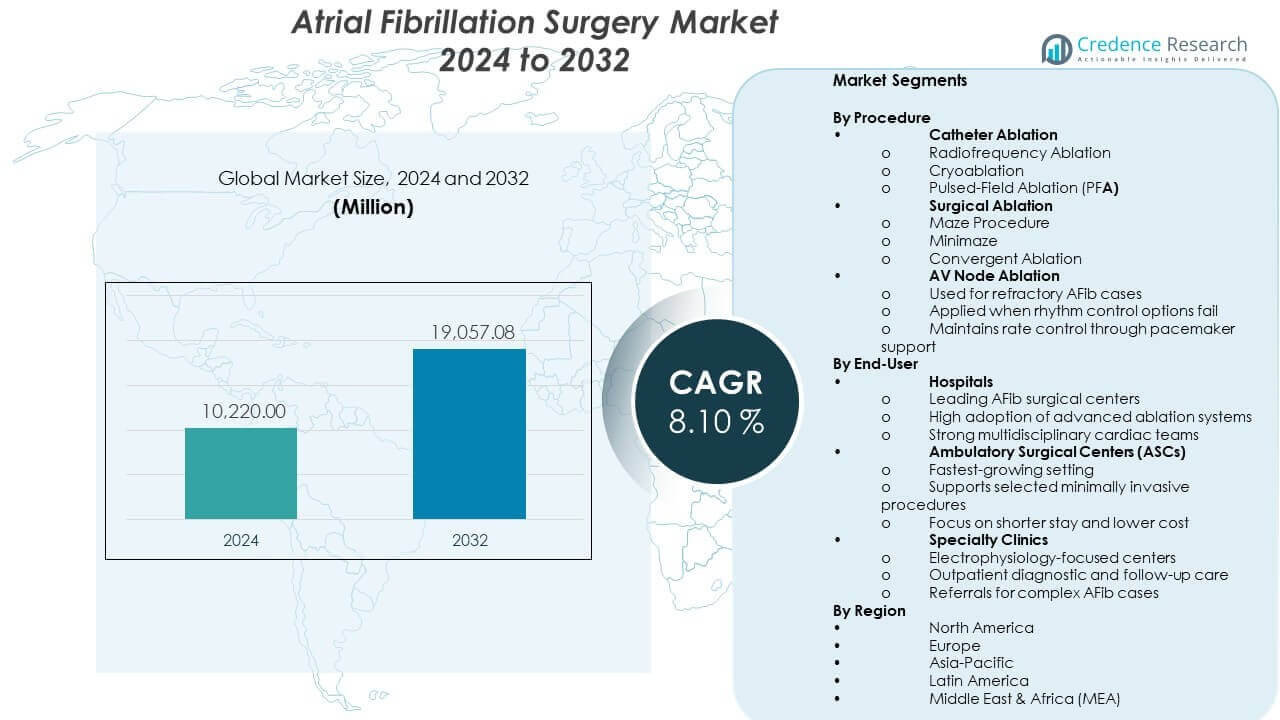

The Atrial Fibrillation Surgery Market is projected to grow from USD 10,220 million in 2024 to an estimated USD 19,057.08 million by 2032, with a CAGR of 8.10% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Automotive Automatic Tire Inflation System Market Size 2024 |

USD 794.01 Million |

| Automotive Automatic Tire Inflation System Market, CAGR |

9.7% |

| Automotive Automatic Tire Inflation System Market Size 2032 |

USD 1665.25 Million |

Atrial Fibrillation Surgery Market Insights:

- North America (>30%), Europe (28%), and Asia-Pacific (22%) dominate due to advanced cardiac infrastructure, strong clinical adoption, and expanding guideline-driven treatment programs supporting AFib surgery.

- Asia-Pacific (22%) stands as the fastest-growing region, supported by large patient pools, rising investment in cardiac surgery capabilities, and increased availability of modern ablation platforms.

- Catheter ablation holds 60–70% share, driven by broad clinical acceptance of radiofrequency, cryoablation, and pulsed-field systems that deliver predictable rhythm correction outcomes.

- Hospitals command the leading end-user share, supported by advanced electrophysiology units, multidisciplinary teams, and strong capacity to adopt high-end ablation technologies.

Market Drivers:

Growing Burden of Atrial Fibrillation Fueling Demand for Advanced Surgical Interventions

The rising global incidence of AFib strengthens demand for reliable treatment paths that support timely symptom control and long-term rhythm stability. Many patients present earlier in the disease cycle due to expanded screening programs in primary care networks. It increases referrals for interventional guidance and surgical planning. Hospitals strengthen clinical pathways that promote faster diagnosis and structured case management. The Atrial Fibrillation Surgery Market benefits from expanding awareness among patients seeking effective correction for persistent arrhythmias. Cardiologists rely on advanced devices that reduce risk during complex workflows. Health systems adopt standardized treatment protocols that reduce variability across centers. Surgeons prefer approaches that create durable results and lower readmission rates.

- For instance, AtriCure’s EPi-Sense Guided Coagulation System has demonstrated clinical efficacy in the CONVERGE trial, achieving freedom from AFib in 67.7% of patients with persistent or long-standing persistent AFib at the 12-month follow-up.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Rising Adoption of Minimally Invasive and Hybrid Ablation Procedures Across Cardiac Centers

Hybrid ablation methods gain traction due to improved safety profiles supported by real-time imaging tools. Many providers shift from open procedures to minimally invasive options to reduce complications and accelerate recovery. It helps hospitals shorten inpatient stay and improve procedure turnover. Strong interest in epicardial and endocardial combined techniques expands training programs for specialists. Manufacturers introduce platforms that enhance lesion quality and procedural precision. Demand grows for tools that support consistent energy delivery across diverse anatomical structures. Teams rely on integrated workflows that improve coordination between surgical and electrophysiology units. This shift strengthens technology investment cycles across multiple regions.

- For instance, Boston Scientific’s FARAPULSE Pulsed Field Ablation (PFA) System demonstrated a primary safety rate of 99.1% and a primary effectiveness rate of 73.3% in the ADVENT pivotal trial, facilitating high procedural efficiency with a mean skin-to-skin time of 29.2 minutes.

Improved Technology Capabilities Enhancing Surgical Outcomes and Treatment Confidence

Technology upgrades support higher adoption of ablation systems designed to improve long-term rhythm control. Robotics and mapping innovations guide surgeons toward more accurate ablation points with lower risk. It supports predictable results and increases confidence in minimally invasive methods. Improved energy sources help generate consistent lesion sets required for durable success. Manufacturers launch systems that streamline device handling and reduce operational burdens for clinical teams. Hospitals invest in platforms that integrate with imaging software to enhance visibility. Electrophysiologists collaborate with surgeons to refine procedural strategies. These advances lift surgical volume and strengthen acceptance across healthcare networks.

Shift Toward Early Intervention Strategies in High-Risk and Persistent AFib Patients

Growing emphasis on early intervention motivates providers to treat rhythm disorders before structural changes worsen. Many patients enter surgical pipelines sooner due to strong evidence supporting earlier correction of AFib. It reshapes decision-making patterns in cardiology clinics. Providers use diagnostic scoring tools to identify ideal candidates for procedural treatment. Health systems promote integrated care pathways that speed patient progression toward definitive therapy. Demand rises for procedures that reduce lifetime treatment burden. Evidence from clinical trials supports wider adoption across high-risk groups. The trend enhances long-term care outcomes and stimulates technology advancement.

Atrial Fibrillation Surgery Market Trends:

Expansion of Integrated Surgical-Electrophysiology Care Models Enhancing Procedural Efficiency

More hospitals adopt unified care frameworks that blend surgical expertise with electrophysiology guidance. The Atrial Fibrillation Surgery Market benefits from structured coordination that reduces workflow gaps. It helps teams operate with higher precision and shared clinical insight. Facilities redesign their procedural suites to support seamless integration of imaging, mapping, and ablation systems. Providers build multidisciplinary programs to standardize quality. Demand grows for flexible platforms that fit these coordinated environments. Hospitals document improved outcomes tied to integrated care delivery. This trend shapes future facility planning across growing cardiac centers.

Growing Use of AI-Driven Mapping Tools and Predictive Analytics in Surgical Decision Pathways

AI-assisted mapping expands due to its ability to detect rhythm patterns with strong accuracy. Many surgeons use predictive analytics to refine lesion strategies based on patient-specific patterns. It guides planning that reduces guesswork during complex cases. Hospitals invest in platforms that combine imaging, mapping, and computational modeling. Innovation accelerates around tools that support better navigation through atrial structures. Providers adopt digital guidance systems that reduce procedure time. Manufacturers explore algorithms that forecast treatment response. This shift enhances personalization in AFib management.

Increasing Preference for Energy-Efficient Ablation Platforms Across Cardiac Surgery Segments

Energy-efficient devices attract significant attention due to their controlled lesion delivery. The Atrial Fibrillation Surgery Market sees rapid adoption of systems that reduce thermal risk during procedures. It supports safer outcomes and builds confidence among surgical teams. Hospitals evaluate platforms that combine precision with reduced collateral damage. Demand rises for cryothermal and focused RF solutions designed for predictable performance. Manufacturers refine catheter designs to improve maneuverability in tight anatomical spaces. Teams track improved workflow consistency during repetitive tasks. The trend strengthens procurement activity in high-volume institutions.

- For instance, Medtronic’s Arctic Front Advance Cryoballoon has been shown in the FIRE AND ICE trial to reduce repeat ablation procedures by 33% and all-cause hospitalizations by 21% compared to radiofrequency ablation due to its consistent, circumferential cooling technology.

Rapid Expansion of Training Programs Advancing Surgical Skill Development Worldwide

Training programs expand due to the need for greater procedural proficiency in AFib correction. Global cardiac societies host structured skill courses for surgeons and electrophysiologists. It improves knowledge transfer and accelerates device adoption. Hospitals develop simulation centers to support safe learning environments. Demand rises for mentorship-based programs that build confidence in complex ablation tasks. Manufacturers collaborate with leading institutes to strengthen hands-on workshops. These efforts improve uniformity in procedural outcomes. The trend aligns with growing patient expectations for experienced surgical teams.

- For instance, Abbott’s EP Academy provides global electrophysiology training through hands-on simulation and advanced mapping workshops that support widespread adoption of the EnSite X EP System. The program helps clinicians strengthen procedural skills and improve workflow confidence across diverse cardiac centers.

Atrial Fibrillation Surgery Market Challenges Analysis:

High Procedure Cost, Technology Complexity, and Uneven Global Adoption Creating Structural Barriers

Cost remains a major limitation due to advanced device requirements and long procedural durations. Many hospitals in developing regions lack infrastructure needed for sophisticated ablation tools. It restricts equal access to surgical solutions despite strong clinical need. Technology complexity demands extensive training that not all centers can support. Reimbursement variations reduce financial predictability for providers. Procurement cycles slowdown in regions facing budget constraints. The Atrial Fibrillation Surgery Market experiences delayed adoption in areas with inconsistent funding. These barriers create uneven treatment access worldwide.

Limited Skilled Workforce and Variability in Procedural Outcomes Reducing Market Acceleration

Shortage of trained surgeons and electrophysiologists limits procedural expansion across many regions. Many centers struggle to maintain consistent outcomes without specialized training pathways. It challenges hospitals that aim to scale their cardiac surgery programs. Variability in lesion quality impacts long-term success rates. Providers face increased pressure to adopt technologies without adequate preparation. Training investments take time to deliver workforce improvements. Hospitals evaluate new delivery models to address experience gaps. These constraints slow rapid growth expected in high-demand regions.

Atrial Fibrillation Surgery Market Opportunities:

Growth Potential from Expanding Access to Minimally Invasive Surgical Solutions in Emerging Regions

Emerging markets show rising acceptance of ablation procedures supported by improving healthcare funding. Hospitals upgrade cardiac units to handle higher surgical demand linked to untreated AFib. It creates strong opportunity for device manufacturers entering new territories. Governments prioritize cardiac care programs that encourage early treatment pathways. Providers introduce screening efforts that increase eligible patient pools. Manufacturers leverage partnerships to expand local presence. The Atrial Fibrillation Surgery Market gains momentum where infrastructure improves steadily. This creates favorable ground for long-term expansion.

Advancement of Smart Technologies Encouraging Innovation in Hybrid Therapy Approaches

Smart platforms combining mapping, imaging, and real-time analytics create new growth paths. Hospitals prefer integrated solutions that improve rhythm correction accuracy. It supports wider adoption of hybrid approaches used in complex AFib cases. Manufacturers design systems that guide safer and faster procedures. Providers incorporate digital decision tools to optimize lesion planning. Interest grows in robotics that enhance precision in constrained surgical fields. These innovations offer strong opportunity for technology differentiation. The trend attracts investment across global cardiac care networks.

Atrial Fibrillation Surgery Market Segmentation Analysis:

By Procedure

The Atrial Fibrillation Surgery Market shows strong dominance of catheter ablation, holding 60–70% share due to its precision and broad clinical acceptance. Radiofrequency ablation leads usage, while cryoablation gains traction for predictable lesion control. Pulsed-field ablation expands quickly due to its safety profile and selective tissue effect. Surgical ablation supports patients who require more extensive intervention through Maze, Minimaze, and convergent techniques. It provides durable rhythm outcomes in complex cases. AV node ablation serves refractory patients when rhythm control strategies fail. This method maintains stable rate control supported by pacemaker implantation. Together, these segments shape procedural decisions across diverse patient groups.

- For instance, the Cox-Maze IV procedure using bipolar radiofrequency clamps from AtriCure has demonstrated strong long-term durability, with a multicenter study reporting approximately 80% freedom from atrial fibrillation at one year and about 76% at three years. These results reinforce its role as a benchmark surgical approach for persistent and long-standing AFib.

By End-User

Hospitals lead end-user adoption due to advanced cardiac units, experienced surgical teams, and strong integration of electrophysiology services. These centers adopt high-end mapping and ablation technologies that support complex AFib corrections. It strengthens procedure volume and enhances treatment capability. Ambulatory Surgical Centers show rapid growth supported by demand for minimally invasive care and shorter recovery needs. These centers manage selected ablation procedures that fit outpatient pathways. Specialty clinics contribute through diagnostic evaluation, rhythm monitoring, and referral of advanced cases to surgical units. Their role supports steady patient flow into interventional programs and promotes structured long-term management.

- For instance, the CARTO 3 System from Johnson & Johnson supports reduced fluoroscopy exposure by enabling real-time 3D electroanatomical mapping, a benefit consistently reported across clinical workflows using advanced mapping systems. Its adoption helps hospitals improve procedural efficiency and enhance safety in high-volume electrophysiology labs.

Segmentation:

By Procedure

- Catheter Ablation

- Radiofrequency Ablation

- Cryoablation

- Pulsed-Field Ablation (PFA)

- Surgical Ablation

- Maze Procedure

- Minimaze

- Convergent Ablation

- AV Node Ablation

- Used for refractory AFib cases

- Applied when rhythm control options fail

- Maintains rate control through pacemaker support

By End-User

- Hospitals

- Leading AFib surgical centers

- High adoption of advanced ablation systems

- Strong multidisciplinary cardiac teams

- Ambulatory Surgical Centers (ASCs)

- Fastest-growing setting

- Supports selected minimally invasive procedures

- Focus on shorter stay and lower cost

- Specialty Clinics

- Electrophysiology-focused centers

- Outpatient diagnostic and follow-up care

- Referrals for complex AFib cases

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America

North America holds the leading position in the Atrial Fibrillation Surgery Market with a share exceeding 30%, supported by high AFib prevalence and strong adoption of advanced ablation systems. The region benefits from well-established cardiac centers that integrate surgical and electrophysiology capabilities. It gains momentum from early technology availability and strong reimbursement structures. Hospitals across the U.S. lead demand for catheter ablation and hybrid procedures due to large treatment volumes. Canada strengthens adoption through expanding specialty programs and investments in minimally invasive cardiac surgery. Training networks in the region improve procedural proficiency and support stable growth. Continuous upgrades in mapping platforms enhance overall treatment effectiveness.

Europe

Europe maintains a significant share of the market, contributing roughly 28% supported by structured healthcare frameworks and high awareness of rhythm management. Germany, the U.K., and France act as major hubs for surgical ablation and advanced catheter technologies. The Atrial Fibrillation Surgery Market benefits from strong clinical guidelines that encourage rhythm control pathways for eligible patients. Hospitals adopt technologies that support improved lesion durability and safer procedural workflows. It reflects broad integration of cryoablation and growing interest in pulsed-field ablation. Training collaborations across European cardiac societies strengthen workforce readiness. Regional investments in digital mapping and imaging upgrades sustain steady demand.

Asia-Pacific, Latin America, and MEA

Asia-Pacific holds the fastest growth trajectory, contributing around 22% driven by rising AFib incidence and rapid expansion of cardiac surgery infrastructure. China, India, and Japan strengthen demand through large patient pools and growing technology adoption. It benefits from government-backed programs that improve access to electrophysiology care. Latin America accounts for an estimated 10% share, led by Brazil and Mexico, where hospitals expand capacity for ablation procedures. MEA contributes roughly 5% supported by emerging infrastructure and rising investment in cardiac care modernization. Regional centers improve capability through partnerships with global device manufacturers. The combined expansion across these regions broadens treatment availability and supports overall market growth.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Medtronic plc

- Abbott Laboratories (St. Jude Medical)

- Boston Scientific Corporation

- Johnson & Johnson (Biosense Webster, Inc.)

- AtriCure, Inc.

- Biotronik SE & Co. KG

- Koninklijke Philips N.V.

- Siemens Healthineers AG

- CardioFocus, Inc.

- MicroPort Scientific Corporation

Competitive Analysis:

Competition in the Atrial Fibrillation Surgery Market centers on device innovation, procedural efficiency, and precision improvement across ablation technologies. Leading companies invest in pulsed-field systems, mapping upgrades, and minimally invasive platforms that support safer rhythm correction. It drives strong differentiation in product depth and clinical performance. Firms strengthen portfolios through strategic alliances with hospitals and research groups. Global players expand training programs to build surgeon capability and enhance device familiarity. Companies pursue regulatory approvals to accelerate commercial reach. Competitors focus on hybrid therapy systems that integrate electrophysiology and surgical workflows, shaping long-term leadership.

Recent Developments:

- In February 2026, Johnson & Johnson introduced the VARIPULSE Plus Platform at the AF Symposium, featuring automated irrigation to enhance procedural safety and confidence in PFA treatments.

- In January 2026, Medtronic announced the CE Mark in Europe and the first U.S. clinical trial cases for its Sphere-360™ PFA catheter, a rotation-free, single-shot device designed to treat paroxysmal atrial fibrillation.

- In January 2026, Abbott obtained the CE Mark for its TactiFlex™ Duo Ablation Catheter, which is uniquely designed to deliver both radiofrequency and PFA energy in a single platform.

Report Coverage:

The research report offers an in-depth analysis based on By Procedure and By End-User. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Demand for pulsed-field ablation is expected to rise as clinicians pursue safer and faster energy-delivery systems that improve precision and reduce unwanted tissue impact, strengthening broader clinical adoption in advanced cardiac centers.

- Hybrid ablation programs will expand as hospitals integrate surgical and electrophysiology teams, creating unified treatment pathways that improve rhythm control outcomes and support stronger procedural consistency across diverse patient groups.

- Robotics will gain traction in complex AFib procedures, offering improved catheter stability, enhanced maneuverability, and reduced operator fatigue, which helps support long-term standardization of high-precision workflows.

- AI-powered mapping and predictive tools will shape treatment planning by identifying optimal lesion sets tailored to patient-specific patterns, helping physicians achieve stronger rhythm correction with fewer repeat procedures.

- Hospitals will invest in digital surgery ecosystems that combine imaging, navigation, and ablation systems into streamlined platforms designed to shorten procedure time and support higher throughput capability.

- Growth in outpatient pathways will accelerate due to minimally invasive approaches that reduce post-procedure recovery needs, allowing selected AFib cases to shift toward same-day care models in suitable centers.

- Workforce development programs will expand globally, focusing on hands-on procedural training, technology familiarization, and competency-building to support growing demand for skilled AFib specialists.

- Regulatory approvals for new ablation platforms will widen technology access, enabling faster introduction of next-generation systems into clinical practice across multiple regions.

- Emerging countries will experience stronger adoption due to rising awareness, expanding cardiac infrastructure, and government-supported programs that improve access to electrophysiology services.

- Strategic partnerships between device manufacturers, research institutes, and healthcare networks will accelerate innovation, enhance clinical evidence, and broaden the global footprint of new ablation technologies.