Autotransfusion Systems Market Overview:

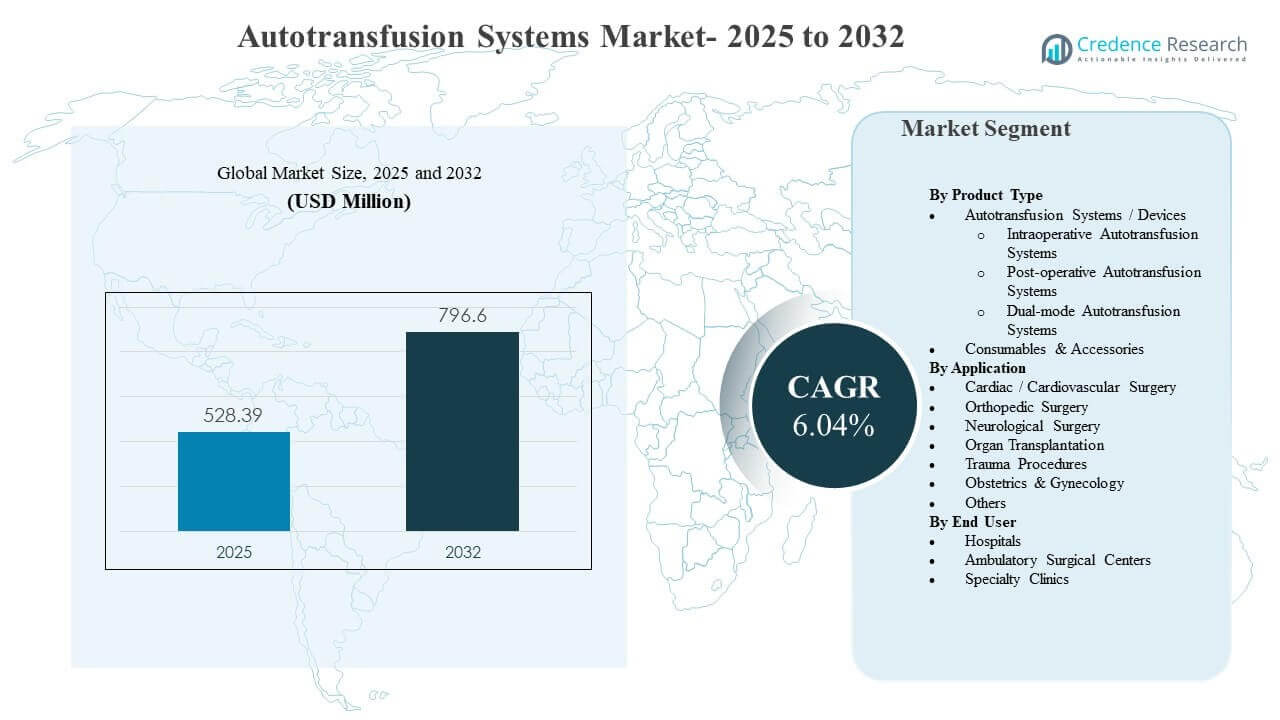

The global Autotransfusion Systems Market size was estimated at USD 528.39 million in 2025 and is expected to reach USD 796.6 million by 2032, growing at a CAGR of 6.04% from 2025 to 2032. The primary growth driver is the wider adoption of patient blood management practices in high-blood-loss surgeries, where intraoperative and post-operative blood recovery is used to reduce dependence on allogeneic transfusions and support surgical workflow predictability. North America remains the largest revenue contributor, supported by strong procedure volumes in cardiac, orthopedic, and trauma care and sustained investment in hospital-based surgical infrastructure.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Autotransfusion Systems Market Size 2025 |

USD 528.39 million |

| Autotransfusion Systems Market, CAGR |

6.04% |

| Autotransfusion Systems Market Size 2032 |

USD 796.6 million |

Key Market Trends & Insights

- Autotransfusion Systems / Devices accounted for the largest share of 9% in 2025, supported by installed base expansion in hospitals and high-acuity surgical settings.

- Cardiac / Cardiovascular Surgery represented 6% share in 2025, reflecting sustained utilization in procedures where blood loss management is clinically prioritized.

- Hospitals held 8% share in 2025, driven by concentration of complex surgeries and availability of perfusion and transfusion support teams.

- North America led the market with 9% share in 2025, reflecting mature adoption of surgical blood management technologies.

- Consumables & Accessories are positioned as a faster-growth revenue stream with a projected 03% CAGR through 2031, supported by recurring demand for single-use sets and tubing.

Segment Analysis

Autotransfusion Systems Market demand is strongly influenced by operating room workflow requirements and the clinical goal of reducing exposure to allogeneic blood in surgeries with predictable or sudden blood loss. Hospitals commonly evaluate systems on setup time, wash quality, output consistency, and ease of use across perfusion and OR staff, because these factors directly affect procedural efficiency and standardization. Procurement decisions also reflect the economics of total cost of ownership, where capital equipment placement is often paired with long-term consumable usage and service support.

The segment mix also reflects procedure-driven utilization patterns. High-volume surgical specialties such as cardiac and orthopedic care provide stable baseline demand, while trauma and emergency pathways increasingly favor solutions that can be deployed quickly and reliably under time pressure. Across end users, the shift toward efficient surgical throughput and standardized patient blood management protocols continues to shape both device upgrades and recurring consumable purchasing.

By Product Type Insights

Autotransfusion Systems / Devices accounted for the largest share of 60.9% in 2025. The segment leads due to the concentration of installed systems in hospital operating rooms where complex procedures require predictable blood recovery workflows. Device selection is strongly influenced by ease of operation, wash performance, and integration into OR protocols, which supports replacement and upgrade cycles. Consumable pull-through further reinforces device placement strategies because the installed base anchors recurring revenue streams.

By Application Insights

Cardiac / Cardiovascular Surgery accounted for the largest share of 37.6% in 2025. The segment leads because cardiac procedures frequently involve managed blood loss risk where recovered red blood cells can support transfusion minimization strategies. Clinical teams prioritize consistency and speed of red cell recovery in these procedures to maintain workflow efficiency. Cardiac centers also tend to have established perfusion support, enabling routine utilization across eligible cases.

By End User Insights

Hospitals accounted for the largest share of 66.8% in 2025. The segment leads because hospitals manage the highest volume of complex surgeries, including cardiac, orthopedic, transplant, and trauma procedures that justify device placement and trained staff. Hospitals also run structured blood-management programs and maintain transfusion services that align closely with autotransfusion workflows. Larger procurement budgets and long-term vendor contracts support system standardization and consumable continuity.

Autotransfusion Systems Market Drivers

Expansion of patient blood management in high-blood-loss surgeries

Patient blood management programs increasingly emphasize reducing exposure to allogeneic transfusions and improving perioperative efficiency in complex surgeries. Autotransfusion supports these goals by enabling recovery and reinfusion of red blood cells during and after procedures. Hospitals adopt these systems to standardize blood conservation protocols across surgical service lines. Growing institutional focus on quality metrics and transfusion stewardship reinforces investment in autotransfusion workflows.

- For instance, a general hospital using the Haemonetics Cell Saver system in 100 consecutive open‑heart cases reduced average allogeneic blood use from 1.97 to 0.75 units per patient, cutting homologous blood utilization by more than 50 percent during cardiac surgery.

Rising surgical volumes in cardiac, orthopedic, and trauma care

Higher procedure volumes in cardiovascular and orthopedic care sustain routine utilization of autotransfusion systems in facilities with established perfusion support. Trauma pathways also increase the relevance of rapid blood recovery capabilities where hemorrhage risk is acute. Demand strengthens when hospitals expand surgical capacity and standardize OR equipment across departments. As procedure complexity increases, blood-loss management becomes more central to perioperative planning.

Installed-base economics and recurring consumables demand

Autotransfusion systems often follow a placement model where capital equipment decisions are linked to long-term utilization and recurring consumable purchases. Consumables and single-use accessories create predictable, repeat revenue that supports vendor service and upgrade cycles. Hospitals prefer solutions that minimize variability and simplify inventory planning for disposable sets. This dynamic encourages vendors to compete on bundled contracts, training, and service reliability.

Technology improvements that simplify workflows and training

System designs continue to improve on usability, setup time, and process consistency, which reduces dependence on highly specialized operator skill. Improved interfaces and standardized disposables support repeatable performance and enable broader adoption across surgical teams. Facilities view workflow simplicity as a key procurement criterion because it reduces training burden and helps maintain compliance with protocols. Technology improvements also support adoption beyond flagship cardiac centers into broader surgical programs.

- For instance, an autologous transfusion pressure‑control system that allows automatic and manual adjustment of suction between 100 and 300 millimeters of mercury enabled anesthetists to control negative pressure alone while maintaining red‑cell integrity at or below 200 millimeters of mercury, simplifying operation without additional surgical staff involvement.

Autotransfusion Systems Market Challenges

Autotransfusion Systems Market adoption can be constrained by upfront capital investment and the ongoing cost of proprietary consumables, particularly in facilities with lower case volumes. Purchasing decisions may be delayed when hospitals prioritize other operating room upgrades or face budget cycles that limit new capital equipment. Inconsistent utilization across specialties can weaken the business case if protocols are not standardized or if eligible procedures are not clearly identified. These constraints are more pronounced in smaller facilities and cost-sensitive settings.

- For instance, smaller NHS hospitals in the UK have reported that demand for in-house cell salvage is so low that it is not considered cost- and resource-effective to maintain their own systems, leading them instead to use outsourced mobile cell salvage services across more than 50 hospitals to avoid underutilized capital and disposable costs.

Operational complexity remains a barrier in environments with limited perfusion support or staff availability, because utilization depends on training, workflow discipline, and equipment readiness. Clinical teams may also limit use in cases where recovered blood quality is a concern or where contamination risk is perceived to be higher. Variation in procedure mix and staffing can lead to underutilization of installed systems. This creates procurement hesitancy even when patient blood management goals are recognized.

Autotransfusion Systems Market Trends and Opportunities

Autotransfusion Systems Market vendors increasingly focus on workflow standardization and bundled offerings that combine devices, disposable sets, service support, and training. This approach supports faster adoption and strengthens long-term customer retention by reducing friction in procurement and utilization. Hospitals favor solutions that integrate into standardized operating room protocols across multiple specialties. Bundled models also support predictable budgeting and reduce operational uncertainty in supply planning.

- For instance, a large orthopedic hospital chain in Germany implemented a semi‑automated, compact autotransfusion system with bundled leukocyte‑filtering disposables across its spine surgery network and reported a 33% reduction in allogeneic transfusion rates and an almost one‑day decrease in average discharge time within nine months, illustrating how standardized, vendor-supported bundles can translate into quantifiable clinical and operational gains.

There is growing opportunity in extending autotransfusion utilization beyond traditional cardiac settings into orthopedic, transplant, and selected obstetrics and gynecology use cases where blood loss risk is material. Expansion into ambulatory surgical centers is an emerging pathway as higher-acuity procedures move into outpatient settings. Vendors that offer compact designs and simplified operation can address staffing limitations and adoption barriers. This trend aligns with broader surgical throughput and efficiency objectives.

Regional Insights

North America

North America accounted for the largest share of 41.9% in 2025 due to mature adoption of surgical blood management, high procedure volumes, and strong hospital infrastructure. The region benefits from established perfusion services and standardized operating room protocols that support routine use in eligible procedures. Procurement decisions frequently emphasize workflow reliability, vendor support, and total cost of ownership. These factors sustain demand for both systems and recurring consumables.

Europe

Europe represented 26.0% share in 2025, supported by broad access to advanced surgical care and structured approaches to transfusion stewardship across many health systems. Adoption is strengthened in higher-acuity centers where cardiac and orthopedic surgery volumes justify installed base expansion. Purchasing decisions often prioritize clinical standardization and consistent quality performance across sites. Vendor differentiation is closely tied to reliability, training, and service coverage.

Asia Pacific

Asia Pacific held 21.0% share in 2025, reflecting expanding surgical capacity and growing adoption of modern perioperative blood management practices. Demand is supported by hospital infrastructure development and increased procedure volumes in large urban centers. The region also presents strong runway for adoption as clinical pathways mature and procurement shifts toward standardized OR equipment. Growth is further supported by expanding private healthcare investment and capability upgrades in tertiary hospitals.

Latin America

Latin America accounted for 7.0% share in 2025, with adoption concentrated in leading private hospitals and higher-tier public centers. Demand is shaped by budget sensitivity, uneven access to perfusion staffing, and variability in procedure volumes across facilities. Where adoption occurs, hospitals prioritize solutions that reduce operational complexity and provide dependable supply of disposables. Market expansion is linked to infrastructure upgrades and broader uptake of patient blood management programs.

Middle East & Africa

Middle East & Africa represented 4.1% share in 2025, driven mainly by tertiary hospitals and centers of excellence in select countries. Adoption is influenced by surgical infrastructure investment, clinical workforce availability, and the ability to maintain consistent consumable supply. Large hospitals that run complex procedures are more likely to standardize autotransfusion use within transfusion stewardship programs. Growth potential improves as hospital capacity expands and perioperative protocols become more standardized.

Competitive Landscape

Autotransfusion Systems Market competition centers on device performance, workflow simplicity, service reliability, and the commercial model that links installed base growth with recurring consumables. Vendors differentiate through ease of setup, consistency of processed red blood cell output, training programs, and long-term service contracts that support high utilization. Procurement is influenced by total cost of ownership and the ability to standardize equipment across surgical suites and service lines. Competitive positioning also reflects the ability to support hospital blood management goals with integrated clinical education and dependable supply chains.

Medtronic plc typically competes through breadth of hospital relationships and a strong footprint in operating room and perioperative technology ecosystems. Medtronic plc’s approach is commonly aligned to standardization across care pathways, supporting procurement teams that prioritize vendor reliability and scalable service coverage. Medtronic plc’s positioning is strengthened when facilities seek consolidated vendor support for complex surgical environments. Medtronic plc benefits from aligning technology adoption with hospital quality and efficiency objectives.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Medtronic plc

- Becton, Dickinson and Company (BD)

- Haemonetics Corporation

- Zimmer Biomet Holdings, Inc.

- Teleflex Incorporated

- Stryker Corporation

- Terumo Corporation

- LivaNova PLC

- Fresenius SE & Co. KGaA (Fresenius Kabi)

- SARSTEDT AG & Co. KG

- B. Braun SE

- Redax S.p.A.

- Macopharma SA

- Nipro Corporation

- Beijing ZKSK Technology Co., Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In August 2024, Stago, in partnership with i-SEP, launched the SAME autotransfusion system, described as a one-of-a-kind intraoperative cell salvage device capable of washing and recovering both functional platelets and red blood cells simultaneously to support blood conservation in surgery.

- In November 2024, Fresenius Kabi (Fresenius SE & Co. KGaA) entered a strategic partnership with a major group purchasing organization (GPO) to supply its CATSmart autotransfusion systems, aiming to expand adoption in mid‑sized hospitals and ambulatory surgery centers.

- In April 2025, Medtronic plc launched its new Auto-Intel series of autotransfusion systems, integrating advanced sensor technology to deliver real-time feedback on blood processing and maximize red blood cell recovery during surgery.

- In January 2025, LivaNova PLC received CE Mark approval for its next‑generation Xtra+ Autotransfusion System, which features enhanced platelet recovery protocols and advanced data management tailored for complex cardiac surgeries.

Report Scop

| Report Attribute |

Details |

| Market size value in 2025 |

USD 528.39 million |

| Revenue forecast in 2032 |

USD 796.6 million |

| Growth rate (CAGR) |

6.04% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Product Type Outlook: Autotransfusion Systems / Devices (Intraoperative Autotransfusion Systems, Post-operative Autotransfusion Systems, Dual-mode Autotransfusion Systems), Consumables & Accessories; By Application Outlook: Cardiac / Cardiovascular Surgery, Orthopedic Surgery, Neurological Surgery, Organ Transplantation, Trauma Procedures, Obstetrics & Gynecology, Others; By End User Outlook: Hospitals, Ambulatory Surgical Centers, Specialty Clinics |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Medtronic plc; Becton, Dickinson and Company (BD); Haemonetics Corporation; Zimmer Biomet Holdings, Inc.; Teleflex Incorporated; Stryker Corporation; Terumo Corporation; LivaNova PLC; Fresenius SE & Co. KGaA (Fresenius Kabi); SARSTEDT AG & Co. KG; B. Braun SE; Redax S.p.A.; Macopharma SA; Nipro Corporation; Beijing ZKSK Technology Co., Ltd. (15 companies) |

| No. of Pages |

327 |

Segmentation

By Product Type

- Autotransfusion Systems / Devices [Intraoperative Autotransfusion Systems, Post-operative Autotransfusion Systems, Dual-mode Autotransfusion Systems]

- Consumables & Accessories

By Application

- Cardiac / Cardiovascular Surgery

- Orthopedic Surgery

- Neurological Surgery

- Organ Transplantation

- Trauma Procedures

- Obstetrics & Gynecology

- Others

By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa