Bioactive Wound Dressing Market Overview:

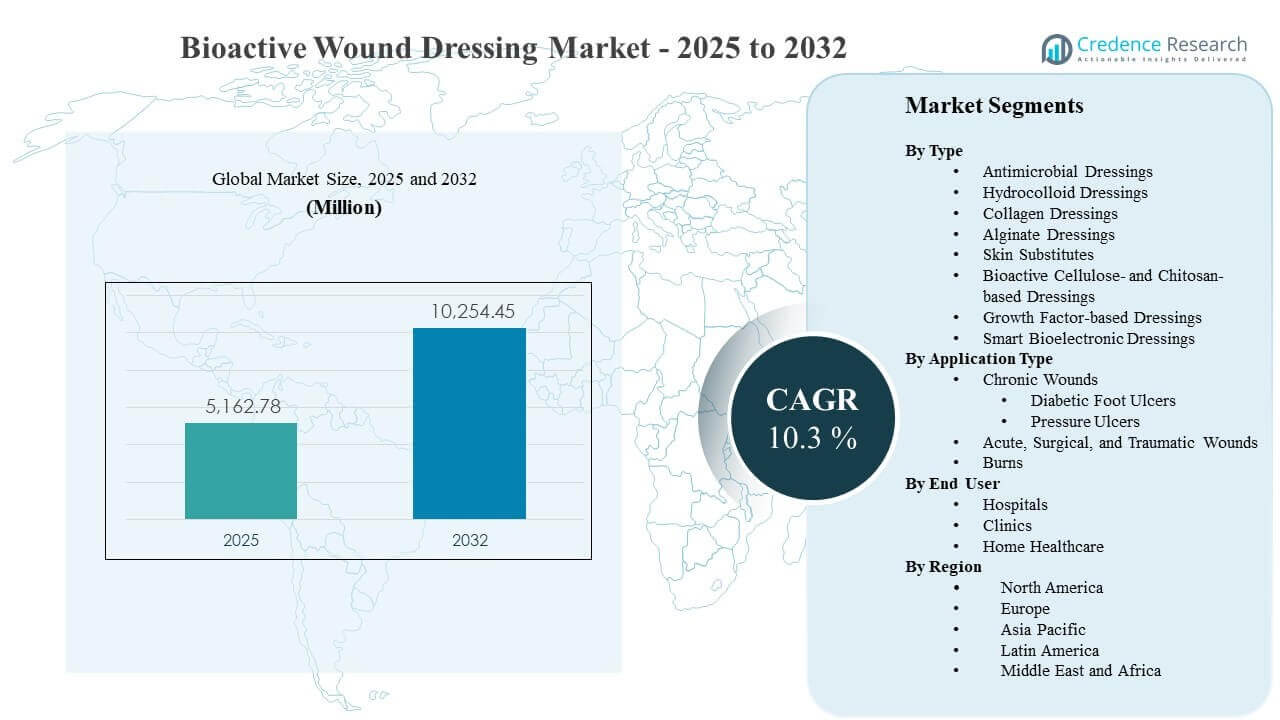

The global Bioactive Wound Dressing Market size was estimated at USD 5162.78 million in 2025 and is expected to reach USD 10254.45 million by 2032, growing at a CAGR of 10.3% from 2025 to 2032. Rising clinical and economic pressure to accelerate closure of hard-to-heal wounds is strengthening adoption of bioactive solutions that can address infection risk, moisture balance, and tissue regeneration within a single care pathway. Bioactive wound dressing demand is also supported by the growing chronic disease burden and higher procedural volumes that expand the treated wound pool across hospital and outpatient settings, with North America remaining a major revenue anchor due to established advanced wound care utilization.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Bioactive Wound Dressing Market Size 2025 |

USD 5162.78 million |

| Bioactive Wound Dressing Market, CAGR |

10.3% |

| Bioactive Wound Dressing Market Size 2032 |

USD 10254.45 million |

Key Market Trends & Insights

- The global Bioactive Wound Dressing Market increased from USD 5162.78 million (2025) to an expected USD 10254.45 million (2032) at a CAGR of 10.3% during 2025–2032.

- Skin Substitutes accounted for the largest share of 41.6% in 2025, supported by their role in complex chronic wounds and high-acuity care pathways.

- Acute, Surgical, and Traumatic Wounds held 45.2% share in 2025, reflecting high treatment volumes and standardized post-procedure wound management protocols.

- Inpatient settings represented 77.4% share in 2025, driven by higher case complexity, clinician oversight, and formulary-led purchasing.

- Regional revenue in 2025 was led by North America (41.7%), followed by Europe (25.4%), Asia Pacific (23.6%), Latin America (5.9%), and Middle East & Africa (3.4%).

Segment Analysis

Bioactive wound dressings are increasingly selected when conventional dressings do not deliver predictable outcomes in chronic and high-risk wounds. The clinical value proposition is anchored in faster closure, reduced infection complications, and fewer dressing changes, which can improve patient comfort and lower total care intensity. Rising diabetes prevalence and the associated diabetic foot ulcer burden continue to expand the addressable pool for advanced therapies, while aging populations increase pressure ulcer incidence and recurrence risk. Providers are also standardizing wound pathways, which increases repeatable use of advanced products once protocolized.

Purchasing decisions are strongly influenced by evidence, ease of use, and site-of-care suitability. Hospital adoption remains high due to multidisciplinary care teams, availability of debridement and adjunct therapies, and stronger reimbursement pathways for advanced products. At the same time, outpatient clinics and home healthcare programs are expanding advanced wound care delivery as products become simpler to apply and are designed for longer wear time. This creates a pathway for higher volume usage beyond inpatient care, particularly for stable chronic wounds under longitudinal monitoring.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Type Insights

Skin Substitutes accounted for the largest share of 41.6% in 2025. These products benefit from strong clinician familiarity in complex wounds where tissue regeneration support and structural coverage are prioritized. Hospital formularies and advanced wound clinics often prefer biologic matrices for difficult-to-heal wounds because they align with protocol-based escalation after standard care fails. Ongoing product improvements and broader clinical evidence reinforce premium positioning and repeat ordering within chronic wound pathways.

By Application Type Insights

Acute, Surgical, and Traumatic Wounds accounted for the largest share of 45.2% in 2025. High procedural volumes create steady throughput for post-operative wound management, where consistency and ease of use matter at scale. Standardized discharge pathways and infection-prevention priorities encourage selection of advanced materials that can stabilize the wound environment and reduce complications. Trauma care also supports advanced use when wound complexity increases, accelerating demand for higher-performance dressings.

By End User Insights

Inpatient settings accounted for the largest share of 77.4% in 2025. Hospitals treat higher-acuity wounds with greater comorbidity burden, requiring clinician oversight and access to adjunct therapies that make advanced products more deployable. Centralized procurement and formulary frameworks also favor vendors with broad portfolios and evidence packages, supporting stable utilization across departments. Inpatient dominance is further reinforced by reimbursement structures and quality metrics tied to infection prevention and wound outcomes.

Bioactive Wound Dressing Market Drivers

Rising chronic wound burden linked to diabetes and aging

Higher prevalence of diabetes and vascular disease is expanding the treated population for diabetic foot ulcers and other chronic wounds that require advanced therapies. Aging demographics increase pressure ulcer risk and wound recurrence, raising longitudinal demand for products that support reliable closure. Providers face pressure to reduce infection complications and re-admissions, which increases willingness to adopt dressings with antimicrobial and regenerative performance. As wound care pathways become protocolized, advanced products see higher repeat utilization across standardized clinical steps.

- For instance, Organogenesis’ Apligraf showed complete healing in 56% of diabetic foot ulcer patients at 12 weeks versus 38% with standard therapy, while median time to closure improved to 65 days from 90 days in its multicenter pivotal trial. As wound care pathways become protocolized, advanced products see higher repeat utilization across standardized clinical steps.

Hospital protocol standardization and quality-driven care pathways

Hospitals are increasingly applying protocol-led wound assessment and escalation pathways to reduce variation in outcomes. Bioactive dressings fit these pathways by offering more predictable healing support in complex cases and improving workflow efficiency through longer wear times. Infection prevention and complication reduction targets reinforce adoption of dressings that manage bioburden and exudate more effectively than basic alternatives. As multidisciplinary wound teams expand, ordering becomes more consistent and vendor relationships become stickier through formulary positioning.

- For instance, Mölnlycke states that Mepilex Border Flex can stay in place for up to 7 days, and its clinical evidence summary reports an 88% reduced risk of pressure-ulcer development when five-layer soft silicone foam dressings were added to ICU prevention protocols.

Technology innovation in materials and multimodal functionality

Innovation in biomaterials, antimicrobial technologies, and regenerative cues is strengthening clinical differentiation and expanding use cases. Collagen matrices, bioactive cellulose/chitosan materials, and growth-factor-linked concepts improve performance in hard-to-heal wounds where conventional moisture balance alone is insufficient. Smart and bioelectronic concepts support future integration of monitoring and response, improving adherence to care plans and enabling earlier intervention when wounds deteriorate. These improvements support premium pricing and reduce switching back to commodity dressings once performance is demonstrated.

Shift toward total cost of care and resource efficiency

Providers and payers are increasingly focused on total cost of care rather than unit product cost, especially for chronic wounds that drive repeated visits. Bioactive products can reduce dressing change frequency, lower infection-related complications, and shorten care timelines, improving staffing efficiency. This economic logic is particularly relevant in inpatient settings where nursing time and length of stay are major cost drivers. As value-based care expands, demand strengthens for solutions that can demonstrate outcome improvement and operational savings.

Bioactive Wound Dressing Market Challenges

Bioactive wound dressings face adoption barriers related to reimbursement variability, evidence thresholds, and budget constraints across sites of care. Hospitals may require strong clinical documentation, local pathway alignment, and formulary approvals before scaling use, which slows uptake for newer technologies. Pricing premiums can limit penetration in cost-sensitive settings where basic dressings remain the default option. Procurement teams also evaluate vendor reliability and supply continuity, making consistent availability a critical requirement for standardization.

- For instance, Organogenesis states that Apligraf is backed by randomized controlled trials that supported FDA approval, with 57% of venous leg ulcers closed by week 24 versus 40% for control, a median time to closure of 99 days versus 184 days, and 56% of diabetic foot ulcers closed by week 12 versus 38% for control.

Market complexity is increased by heterogeneous wound types, patient comorbidities, and differences in clinician practice patterns. Outcomes can vary by debridement quality, offloading adherence, infection control, and patient compliance, which can complicate product-level attribution. Product selection is also influenced by training needs and ease-of-application, particularly when expanding use into outpatient and home settings. Regulatory requirements and claims limitations can further constrain how value is communicated, reducing speed of switching from incumbent solutions.

Bioactive Wound Dressing Market Trends and Opportunities

Advanced wound care is expanding beyond inpatient settings as outpatient clinics scale specialized wound programs and seek tools that support repeatable outcomes. Longer wear designs, simplified application, and bundled care kits enable broader use in clinics and supervised home healthcare pathways. This trend supports higher treatment volumes for stable chronic wounds and post-discharge management, increasing addressable demand for products that balance performance with usability. Companies that align training, service, and evidence with these settings can gain share through pathway adoption.

- For instance, Smith+Nephew reported in a randomized 50-patient trial that its PICO Single Use NPWT system reduced surgical site infections by 74% versus standard care, with infection rates of 8.3% compared with 32.0%, and shortened average length of stay to 6.1 days from 14.7 days; the company also states that PICO is suitable for both hospital and community settings.

Technology convergence is creating opportunities for next-generation bioactive platforms that combine antimicrobial control, moisture management, and regenerative support within integrated systems. Smart bioelectronic concepts can enable monitoring, early-warning indicators, and more personalized care decisions, supporting earlier intervention and improved adherence. As wound documentation becomes more digital, data-enabled solutions may gain preference in organized care networks seeking measurable outcomes. This creates whitespace for differentiated products that can demonstrate both clinical value and workflow efficiency.

Regional Insights

North America

North America held the leading revenue share of 41.7% in 2025. The region benefits from established advanced wound care utilization, high treatment intensity for chronic wounds, and mature hospital procurement pathways that support portfolio-based contracting. Specialized wound clinics and integrated care networks also strengthen repeat usage once products are embedded into standardized protocols. Higher diabetes prevalence and strong emphasis on infection prevention continue to sustain demand for advanced solutions.

Europe

Europe accounted for 25.4% share in 2025. Demand is supported by structured healthcare systems and increasing emphasis on evidence-led product selection in hospital and community care pathways. Advanced wound care adoption is strengthened by specialist services in major markets and ongoing modernization of clinical protocols. Sustainability and material innovation also influence procurement priorities, particularly where procurement frameworks encourage standardized product rationalization.

Asia Pacific

Asia Pacific represented 23.6% share in 2025. Growth is driven by expanding access to advanced care in urban hospitals, rising diabetes prevalence, and increasing investments in healthcare infrastructure. Adoption remains uneven across countries due to reimbursement variability and affordability constraints, but modernization of clinical pathways is improving uptake in higher-acuity settings. As outpatient wound programs expand, demand is expected to broaden beyond tertiary hospitals into clinics and supervised home care.

Latin America

Latin America held 5.9% share in 2025. Adoption is supported by private healthcare expansion and improving availability of advanced wound care products in major urban centers. However, budget sensitivity and variability in access to specialist wound clinics constrain penetration in broader public systems. Vendors that offer clear training pathways and cost-effective protocols can accelerate adoption in high-burden chronic wound segments.

Middle East & Africa

Middle East & Africa accounted for 3.4% share in 2025. Demand is concentrated in countries with higher healthcare spending and better access to advanced wound care services, while broader penetration is constrained by affordability and uneven specialist availability. Hospital infrastructure investments and expansion of private care networks are improving access to advanced products in select markets. Continued focus on diabetes management and infection prevention supports gradual expansion of advanced dressing utilization.

Competitive Landscape

Competition in the bioactive wound dressing market is shaped by portfolio breadth, clinical evidence, and the ability to win hospital formulary access through differentiated performance claims and service support. Leading suppliers compete on infection control, regenerative performance, wear time, and ease of application, while also emphasizing clinician education and pathway integration. Contracting strength and distribution reach influence purchasing decisions, particularly in large hospital networks. Innovation cycles remain active as companies refresh legacy products and introduce advanced materials to defend share.

3M competes by leveraging broad wound care capabilities and strong relationships across hospital procurement channels, supporting adoption through standardized workflows and clinician familiarity. The company’s positioning typically emphasizes usability, performance consistency, and pathway fit across acute and chronic settings. Portfolio breadth can support cross-selling across departments, strengthening contract resilience. Product refresh cycles also help maintain relevance in high-volume indications where hospitals prefer proven brands.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In April 2025, Convatec announced regulatory approval for ConvaNiox, which it described as the first nitric oxide-generating multimodal dressing for the wound care market, with an initial rollout planned later in 2025 across France, Germany, Italy, Poland, Spain, and the UK.

- In July 2025, Convatec said it had secured regulatory clearance in the UK, EU, Australia, and the US for Aquacel ConvaFiber, a next-generation dressing built on its Hydrofiber technology, and added that the product is scheduled for launch in 2026.

- In July 2025, MiMedx Group and Vaporox announced a strategic collaboration to co-promote and co-market their wound care offerings, while MiMedx also made an investment in Vaporox and received certain exclusivity rights related to possible acquisition discussions.

- In November 2025, Solventum announced a definitive agreement to acquire Acera Surgical for $725 million in cash plus up to $125 million in contingent payments, saying the deal is intended to accelerate adoption of Acera’s Restrata products in the acute care market.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 5162.78 million |

| Revenue forecast in 2032 |

USD 10254.45 million |

| Growth rate (CAGR) |

10.3% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Type; By Application Type; By End User |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

3M; Smith & Nephew plc; Mölnlycke Health Care AB; ConvaTec Group plc; B. Braun SE; Coloplast A/S; Organogenesis Holdings Inc.; Integra LifeSciences Holdings Corporation |

| No. of Pages |

328 |

Segmentation

By Type

- Antimicrobial Dressings

- Hydrocolloid Dressings

- Collagen Dressings

- Alginate Dressings

- Skin Substitutes

- Bioactive Cellulose- and Chitosan-based Dressings

- Growth Factor-based Dressings

- Smart Bioelectronic Dressings

By Application Type

- Chronic Wounds [Diabetic Foot Ulcers, Pressure Ulcers]

- Acute, Surgical, and Traumatic Wounds

- Burns

By End User

- Hospitals

- Clinics

- Home Healthcare

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa