Biomedical Refrigerator & Freezer Market Overview:

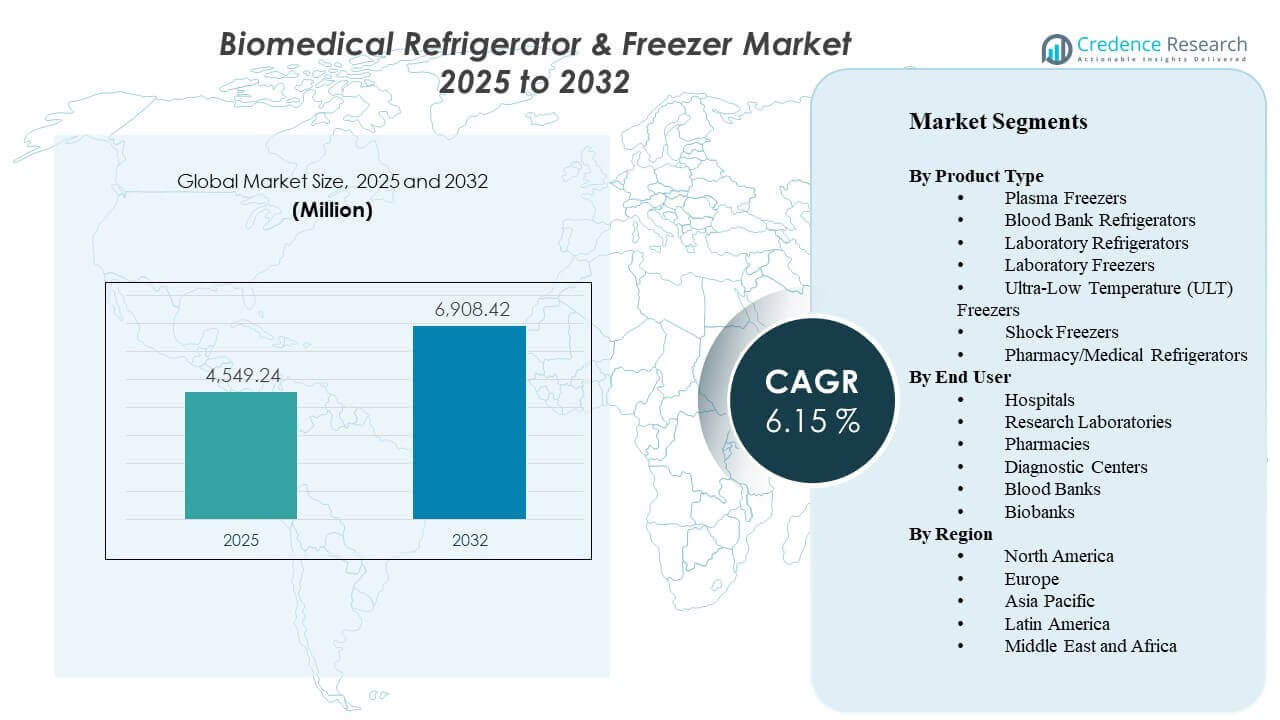

The global Biomedical Refrigerator & Freezer Market size was estimated at USD 4549.24 million in 2025 and is expected to reach USD 6908.42 million by 2032, growing at a CAGR of 6.15% from 2025 to 2032. Growth is primarily driven by stricter temperature-compliance requirements across hospitals, blood banks, and research laboratories, which are pushing upgrades toward continuous monitoring, alarms, and higher temperature-uniformity performance. Expansion in biobanking and biologics-related sample preservation is also increasing demand for higher-capacity and ultra-low temperature storage systems across both mature and emerging healthcare systems.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Biomedical Refrigerators and Freezer Market Size 2025 |

USD 4549.24 million |

| Biomedical Refrigerators and Freezer Market, CAGR |

6.15% |

| Biomedical Refrigerators and Freezer Market Size 2032 |

USD 6908.42 million |

Key Market Trends & Insights

- The market is projected to expand from USD 4549.24 million (2025) to USD 6908.42 million (2032), reflecting a 6.15% CAGR (2025–2032).

- Laboratory Refrigerators accounted for the largest share of 22.6% in 2025, supported by broad use across diagnostics, routine lab workflows, and research environments.

- Hospitals represented the leading end-user segment with 33.4% share in 2025, reflecting high installed-base needs for vaccines, reagents, and patient samples.

- North America led regional demand with a 34.70% share in 2025, driven by strong regulatory adherence and concentration of advanced laboratory infrastructure.

- Ultra-Low Temperature (ULT) Freezers show a high-growth pocket at 10.25% CAGR through 2031, reflecting demand for long-term biologics and genomic sample preservation.

Segment Analysis

Demand patterns in Biomedical Refrigerator & Freezer Market are shaped by two core purchasing realities: compliance assurance and uptime risk management. Healthcare providers and laboratory operators increasingly prioritize systems with robust temperature stability, door-open recovery performance, alarms, and data-logging capabilities to reduce excursion frequency and simplify audits. These requirements support steady replacement cycles for standard 2°C–8°C and -20°C/-40°C applications, while reinforcing value for service coverage and preventative maintenance.

Growth intensity is higher in segments tied to long-duration storage and high-value sample integrity. Capacity additions in biobanks and research programs, along with growth in biologics workflows, are raising adoption of ULT platforms and related monitoring ecosystems. Product selection is also influenced by total cost of ownership, including energy consumption, refrigeration technology choices, and facility constraints such as footprint, noise, and heat load management.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Product Type Insights

Laboratory Refrigerators accounted for the largest share of 22.6% in 2025. Laboratory Refrigerators lead due to broad deployment across hospital labs, diagnostic laboratories, and research sites where routine storage of reagents and specimens is continuous. Standardized temperature bands, frequent access cycles, and audit requirements favor reliable, high-uniformity cabinets with alarms and logging. Replacement demand also remains steady as facilities modernize fleets to improve stability and reduce excursion-related risk.

By End User Insights

Hospitals accounted for the largest share of 33.4% in 2025. Hospitals lead because cold storage is embedded across pharmacy, pathology, transfusion services, and clinical laboratory workflows that operate daily at high utilization. Procurement often emphasizes compliance features, traceability, and downtime resilience due to direct patient-care implications. Hospitals also tend to standardize platforms across departments, supporting larger volume purchasing and recurring service contracts.

Biomedical Refrigerators and Freezers Market Drivers

Compliance-driven cold storage upgrades across healthcare and laboratories

Biomedical Refrigerator & Freezer Market growth is supported by tighter requirements for temperature traceability, alarm performance, and audit readiness across hospitals, blood banks, and laboratories. Facilities increasingly upgrade to systems with integrated logging, remote monitoring, and reliable temperature uniformity to reduce excursion risk. Procurement teams also prioritize validated performance and consistent door-open recovery characteristics in high-access settings. These factors sustain recurring replacement demand in addition to incremental capacity additions. As compliance expectations rise, buyers also favor platforms that simplify documentation and reduce manual checks through automated reporting.

Expansion in biobanking and long-term sample preservation needs

Biomedical Refrigerator & Freezer Market demand is reinforced by growth in biobanks, genomics programs, and long-duration sample archiving. Long-term storage requires stable performance and risk controls because the economic and scientific value of samples is high. Expansion in sample volumes pushes investment into ULT and specialty freezers, along with monitoring ecosystems that support preventive maintenance. This driver is particularly important in research networks and precision medicine initiatives. Institutions also increasingly plan capacity in modular ways, adding units as sample collections scale and funding cycles progress.

Growth in diagnostic testing volumes and distributed laboratory networks

Biomedical Refrigerator & Freezer Market volumes benefit from rising diagnostic testing intensity and the expansion of laboratory footprints beyond major hospitals. Distributed sample collection and referral networks require reliable cold storage across multiple nodes, increasing cabinet counts and service needs. Consistent storage conditions also support standard operating procedures across labs, improving procurement standardization. Increased testing frequency elevates utilization and accelerates replacement cycles for heavily used units. This trend supports demand for compact, easy-to-service systems that can be deployed quickly across satellite labs and collection centers.

- For instance, Haier Biomedical’s HYC-68A compact refrigerator provides 68 L (2.4 cu. ft.) of 2°C to 8°C storage, includes remote alarm capability, and supports an alarm-system battery duration of at least 8 hours during power failure conditions, which is useful for decentralized collection points.

Total cost of ownership focus: energy efficiency, serviceability, and uptime

Biomedical Refrigerator & Freezer Market purchasing decisions increasingly reflect lifecycle cost evaluation rather than only upfront price. Energy consumption, heat load, maintenance intervals, and service response times influence brand selection and fleet standardization. Facilities also seek equipment that minimizes downtime risk through robust design, parts availability, and preventative maintenance support. This driver benefits suppliers that combine compliant performance with measurable operating-cost advantages. Over time, large health systems also use fleet-wide analytics to identify underperforming units and prioritize replacements that deliver the fastest payback.

- For instance, Eppendorf reports that its CryoCube F570h reaches -80°C from ambient in 3 h 30 min, uses 7.4 kWh/day at -80°C, and emits 308 W of heat at that setpoint, giving procurement teams concrete metrics for energy, HVAC load, and uptime planning.

Biomedical Refrigerators and Freezers Market Challenges

Biomedical Refrigerator & Freezer Market expansion faces cost and procurement barriers, especially for ULT and specialty freezer categories where capital expense is high and lifecycle maintenance expectations are demanding. Budget constraints can delay replacement of older assets even when performance improvements would reduce excursion risk. Facility-level constraints such as limited space, electrical capacity, and ventilation can also slow deployments or require additional infrastructure investments. These challenges are more pronounced in smaller hospitals and mid-sized laboratories.

- For instance, PHCbi’s VIP ECO SMART MDF-DU703VHA-PA is designed to run on either 115V or 220V power, delivers daily energy usage of 5.40 kWh, and uses 30% less energy than other leading ENERGY STAR-certified freezers in its class, while also generating less heat output, which can help facilities manage electrical and HVAC constraints during installation planning.

Biomedical Refrigerator & Freezer Market suppliers also operate under tightening expectations around reliability, documentation, and post-installation support. Service coverage gaps and lead-time variability can disrupt fleet planning for multi-site laboratory networks. Compliance requirements can increase documentation and validation work for buyers, extending procurement timelines. Competitive pressure can further compress margins, limiting flexibility for vendors to absorb cost increases without impacting pricing.

Biomedical Refrigerators and Freezers Market Trends and Opportunities

Biomedical Refrigerator & Freezer Market is seeing growing adoption of connected monitoring and digital compliance workflows. Facilities increasingly value remote alarms, centralized dashboards, and automated reporting that reduces manual recordkeeping burden. Integration with broader laboratory information workflows and preventive maintenance scheduling strengthens the case for connected platforms. This trend creates opportunities for suppliers to differentiate through software ecosystems and service-led recurring revenue models.

- For instance, Thermo Fisher Scientific states that its TSX Series is compatible with DeviceLink Hub for connected monitoring, while its Smart-Vue platform provides 24/7 real-time wireless monitoring and remote data logging; the same TSX platform also offers alarm-delay modules adjustable from 0.5 to 32 minutes to reduce nuisance alarms while maintaining escalation to central monitoring systems.

Biomedical Refrigerator & Freezer Market opportunities are expanding around sustainability-oriented procurement and refrigeration technology improvements. Buyers increasingly screen for energy efficiency and reduced environmental impact alongside performance requirements. Portfolio refresh cycles that target lower operating costs can accelerate replacements in large installed bases. Suppliers that combine efficient refrigeration, high uniformity, and strong service networks are positioned to benefit from fleet modernization initiatives.

Regional Insights

North America

North America held 34.70% of Biomedical Refrigerator & Freezer Market revenue in 2025, reflecting strong compliance-driven purchasing and high penetration of monitoring-enabled systems. Hospitals, reference laboratories, and research institutions contribute to stable baseline demand, while biobanking and biologics workflows support higher-growth freezer categories. Replacement cycles remain active due to fleet modernization and uptime risk management priorities.

Europe

Europe accounted for an estimated 25.30% share in 2025, supported by established hospital laboratory networks, regulated cold-chain procedures, and strong research infrastructure. Demand is shaped by compliance readiness, energy efficiency preferences, and standardization across multi-site health systems. Growth is also supported by ongoing lab modernization and capacity additions in research-oriented storage environments.

Asia Pacific

Asia Pacific represented an estimated 24.10% share in 2025, underpinned by expanding diagnostics capacity, rising research activity, and increasing adoption of advanced cold storage across major healthcare hubs. Procurement increasingly emphasizes reliable performance and monitoring features as lab networks scale and standard operating procedures mature. Growth momentum is also supported by broader infrastructure expansion that increases the installed base of compliant storage units.

Latin America

Latin America held an estimated 8.70% share in 2025, supported by healthcare infrastructure upgrades and modernization of laboratory and blood bank facilities in key markets. Budget constraints can extend replacement cycles, but demand remains resilient where compliance and quality-control expectations are rising. Service coverage, parts availability, and total cost of ownership are important purchasing factors for multi-site laboratory operators.

Middle East & Africa

Middle East & Africa accounted for an estimated 7.20% share in 2025, supported by hospital expansion programs and modernization of cold-chain capabilities. Demand is often concentrated in larger urban healthcare centers and research facilities, with adoption accelerating where compliance frameworks and centralized procurement mature. Vendor differentiation through service support and reliability remains critical in installations where uptime risk is costly.

Competitive Landscape

Biomedical Refrigerator & Freezer Market competition is characterized by a mix of diversified life science suppliers and specialized cold-storage manufacturers competing on compliance performance, temperature uniformity, energy efficiency, and service responsiveness. Product portfolios increasingly emphasize monitoring, alarms, and data-logging capabilities that support audit readiness and reduce excursion risk. Differentiation is also driven by ULT performance, cabinet capacity configurations, footprint efficiency, and lifecycle cost positioning across hospital and laboratory fleets.

Thermo Fisher Scientific Inc. is positioned as a broad life science supplier that can bundle cold storage equipment with laboratory consumables, workflow tools, and service coverage for multi-site customers. Portfolio breadth supports standardization strategies for health systems and research networks seeking fewer vendors and consistent compliance documentation. Thermo Fisher Scientific Inc. can also leverage field service capabilities and customer relationships across laboratory and bioproduction environments to support fleet expansion and replacement cycles.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Thermo Fisher Scientific Inc.

- PHC Holdings Corporation (Panasonic Healthcare)

- Haier Biomedical

- Eppendorf AG

- Helmer Scientific Inc.

- Arctiko A/S

- Liebherr-International AG

- Follett Products LLC

- Azbil Corporation

- Terumo Corporation

- Philipp Kirsch GmbH

- Binder GmbH

- Stirling Ultracold

- So-Low Environmental Equipment

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In January 2026, PHC Corporation of North America launched the PHCbi TwinGuard ECO 703VXH ultra-low temperature freezer for biorepositories, biopharmaceutical companies, and academic institutions. The company said the new model was designed to improve energy efficiency and expand operational monitoring for critical sample storage applications.

- In March 2025, Haier Biomedical highlighted several cold-chain products at Global Health Exhibition 2025, including the DW-86L728BPST ultra-low temperature freezer, the HYC-509T pharmacy refrigerator, and the HXC-158 blood bank refrigerator. The company positioned these products around sample integrity, smart storage, and energy-efficient performance for healthcare and laboratory use.

- In April 2024, Thermo Fisher Scientific launched its Thermo Scientific TSX Universal Series ultra-low temperature freezers. The new freezer line was introduced with a focus on tighter temperature control and faster recovery times, which are important for preserving sensitive biomedical and laboratory samples.

- In March, 2024, ARCTIKO announced the launch of 22 new products, including 15 pharmaceutical refrigerators and seven biomedical freezers. This update reflected a major portfolio expansion by a company focused directly on biomedical cold storage equipment.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 4549.24 million |

| Revenue forecast in 2032 |

USD 6908.42 million |

| Growth rate (CAGR) |

6.15% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Product Type Outlook: Plasma Freezers, Blood Bank Refrigerators, Laboratory Refrigerators, Laboratory Freezers, Ultra-Low Temperature (ULT) Freezers, Shock Freezers, Pharmacy/Medical Refrigerators; By End User Outlook: Hospitals, Research Laboratories, Pharmacies, Diagnostic Centers, Blood Banks, Biobanks |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Thermo Fisher Scientific Inc., PHC Holdings Corporation (Panasonic Healthcare), Haier Biomedical, Eppendorf AG, Helmer Scientific Inc., Arctiko A/S, Liebherr-International AG, Follett Products LLC, Azbil Corporation, Terumo Corporation, Philipp Kirsch GmbH, Binder GmbH, Stirling Ultracold, So-Low Environmental Equipment companies |

| No.of Pages |

330 |

By Segmentation

By Product Type

- Plasma Freezers

- Blood Bank Refrigerators

- Laboratory Refrigerators

- Laboratory Freezers

- Ultra-Low Temperature (ULT) Freezers

- Shock Freezers

- Pharmacy/Medical Refrigerators

By End User

- Hospitals

- Research Laboratories

- Pharmacies

- Diagnostic Centers

- Blood Banks

- Biobanks

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa