Bladder Scanners Market Overview:

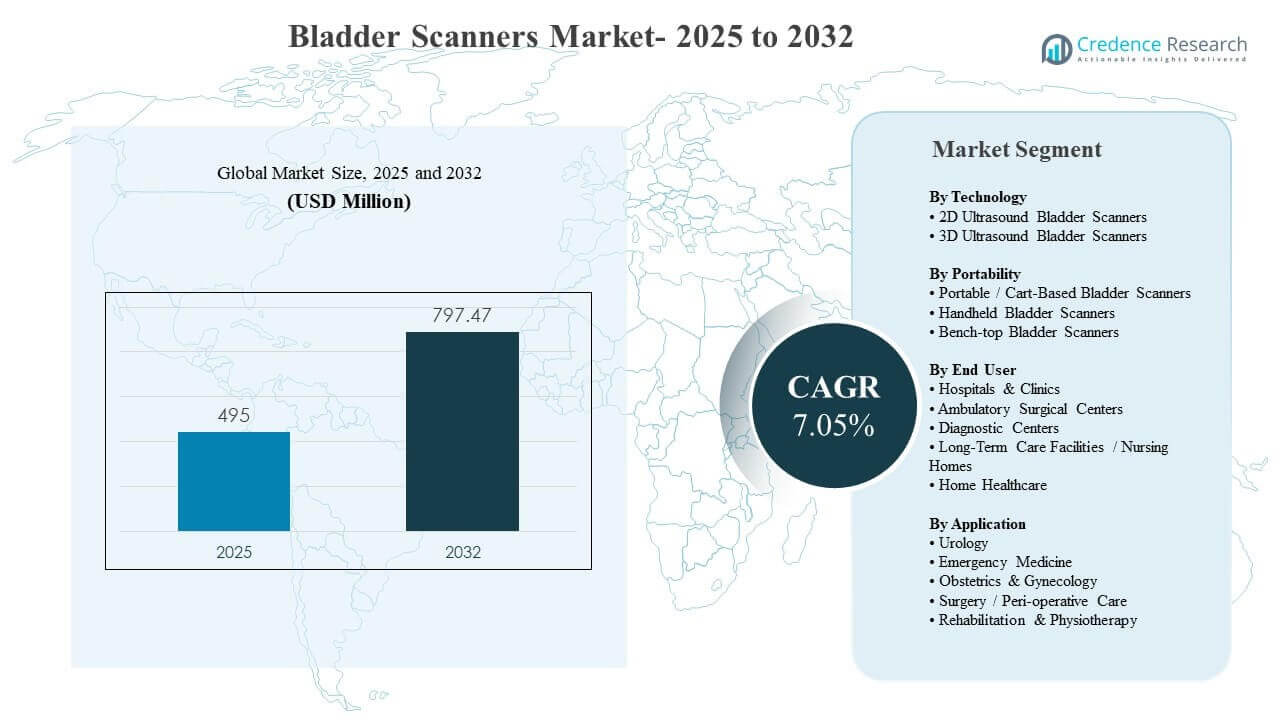

The global Bladder Scanners Market size was estimated at USD 495 million in 2025 and is expected to reach USD 797.47 million by 2032, growing at a CAGR of 7.05% from 2025 to 2032. Demand is being reinforced by stronger clinical focus on reducing unnecessary catheterization and improving urinary retention assessment, particularly in high-throughput acute and peri-operative settings where non-invasive bladder volume measurement supports faster decisions and safer care pathways. Adoption is also expanding beyond tertiary hospitals as portable and handheld systems improve usability, enabling broader deployment across outpatient sites, long-term care facilities, and home healthcare programs where workflow simplicity and infection-control practices are critical.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Bladder Scanners Market Size 2025 |

USD 495 million |

| Bladder Scanners Market, CAGR |

7.05% |

| Bladder Scanners Market Size 2032 |

USD 797.47 million |

Key Market Trends & Insights

- 2D ultrasound bladder scanners accounted for 51.4% share in 2025, supported by established workflows and lower acquisition barriers versus higher-end configurations.

- Portable / cart-based bladder scanners held 63.8% share in 2025, reflecting preference for durable, high-throughput devices across ED and peri-operative units.

- Hospitals & clinics contributed 71.0% share in 2025, driven by higher scan volumes and protocolized bladder management practices.

- Urology represented 43.6% share in 2025, supported by frequent post-void residual measurement and urinary retention evaluation routines.

- 3D ultrasound bladder scanners are projected to grow at 7.50% CAGR during 2026–2031, as volumetric precision and automation become stronger procurement criteria.

Segment Analysis

Bladder scanners are increasingly purchased as workflow tools rather than standalone imaging devices, with buyers prioritizing ease of use, repeatability, and faster bedside decision-making. In acute care and peri-operative units, high daily scan volumes make throughput, cleaning protocols, and reliability major selection criteria. Pricing accessibility is also widening adoption, with portable and handheld formats expanding into smaller clinics and home healthcare programs where budget and training time are constrained. The value proposition is further strengthened by clinical initiatives aimed at minimizing unnecessary catheterization and improving patient comfort, which supports routine scanning prior to catheter placement or discharge.

Technology differentiation is shifting toward automation, measurement consistency, and reporting readiness. As facilities demand more standardized outcomes, vendors are integrating AI-assisted volume measurement and guided workflows to reduce operator variability across nursing and allied health users. This supports wider utilization across departments beyond urology, including emergency medicine, rehabilitation, and selected OB/GYN pathways where rapid assessment supports quicker triage and care planning. As a result, procurement is increasingly influenced by total workflow fit, device uptime, and integration with documentation practices rather than image features alone.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Technology Insights

2D Ultrasound Bladder Scanners accounted for the largest share of 51.4% in 2025. This leadership is supported by broad clinical familiarity and established nursing protocols that enable consistent use with minimal incremental training. Lower purchase costs and wider availability also make 2D systems the default choice for multi-department deployment, particularly in hospitals and long-term care settings. In addition, stable performance for routine post-void residual and urinary retention checks sustains a large installed base that continues to drive replacement demand.

By Portability Insights

Portable / Cart-Based Bladder Scanners accounted for the largest share of 63.8% in 2025. Cart-based platforms remain preferred in high-volume environments because they support faster throughput, dependable uptime, and easier movement between wards without compromising cleaning routines. These systems also align well with hospital documentation practices, where consistent scanning workflows are needed across ED, peri-operative, and inpatient floors. Their durability and battery-backed mobility further reinforce procurement decisions in facilities that standardize equipment across departments.

By End User Insights

Hospitals & Clinics accounted for the largest share of 71.0% in 2025. Hospitals lead due to the concentration of urology, emergency, and peri-operative care pathways where bladder volume measurement is frequently required. Standardized protocols and higher scan volumes support stronger utilization intensity and justify investment in multiple devices across units. Hospitals also prioritize catheter avoidance initiatives and audit-ready documentation, which increases reliance on non-invasive scanning before or after procedures.

By Application Insights

Urology accounted for the largest share of 43.6% in 2025. Urology use remains dominant because post-void residual assessment and urinary retention screening are routine across a wide range of patient types. The specialty also benefits from established clinical guidance that supports bladder scanning as a first-line, non-invasive assessment tool. As urology clinics and hospital departments seek to reduce catheter use and improve patient comfort, scanning becomes a standard step in evaluation and follow-up workflows.

Bladder Scanners Market Drivers

Protocol-driven catheter avoidance and urinary retention management

Healthcare providers are increasingly standardizing bladder assessment workflows to reduce unnecessary catheterization and improve patient comfort. Bladder scanners enable quick, non-invasive decisions aligned with infection-prevention targets and quality metrics. In peri-operative units and emergency departments, rapid volume measurement reduces delays, supports earlier intervention, and improves discharge readiness. These operational benefits increase scan frequency per encounter and justify placing scanners in multiple wards, strengthening demand for installations and replacements overall globally.

- For instance, in an acute care medical–surgical unit, introducing a bladder‑scanner policy cut catheterizations among “unable to void” patients by about 80%, with only 4% needing straight catheters and 10% requiring indwelling catheters. In a post‑anesthesia care unit, an ultrasound‑guided protocol using an 800 mL volume threshold reduced sterile intermittent catheterizations by more than 65% without increasing catheter use later on the ward.

Expansion of point-of-care ultrasound workflows in acute and outpatient care

Point-of-care ultrasound adoption is rising, and bladder scanning fits naturally into bedside assessment routines. Portable and handheld systems allow scanning in ED bays, PACU, inpatient wards, clinics, and outpatient surgery centers without transporting patients. This convenience supports protocol use where time-to-decision is critical and staffing is tight. As POCUS skills expand among nurses, anesthetists, and clinicians, the trained user base grows, accelerating utilization, procurement, and service demand steadily year-on-year significantly.

Growth in aging population and chronic urology care needs

Population aging increases urinary retention incidence, BPH-related symptoms, and neurologic conditions that impair bladder function. These patients often need repeated monitoring during admissions, rehabilitation, and long-term management, raising demand for reliable, fast, non-invasive assessment. Long-term care facilities and home healthcare programs are also expanding capacity to manage chronic urology needs outside hospitals. This broadens the care footprint and shifts incremental demand toward portable devices suited to distributed settings worldwide today.

Technology upgrades improving measurement consistency and workflow efficiency Buyers increasingly prioritize measurement repeatability,

automation, and guided workflows to reduce operator dependence. Newer systems shorten scan time, improve probe positioning feedback, and deliver documentation-ready outputs that integrate with clinical charting. Facilities also prefer designs that support infection-control routines, fast cleaning, and consistent performance across shifts. These upgrades strengthen the ROI case for replacements while encouraging additional purchases to expand coverage across departments, sites, and mobile care teams today consistently.

- For instance, Verathon’s BladderScan i10, built on its ImageSense AI and BladderTraq guidance, reports volume‑measurement accuracy within ±7.5% for volumes above 100 mL (or within ±7.5 mL below 100 mL), standardizing workflows across adult and pediatric anatomies and supporting consistent performance across shifts.

Bladder Scanners Market Challenges

Bladder scanner adoption can be constrained by training variability and inconsistent measurement quality when workflows are not standardized. Operator dependence may reduce clinician confidence, especially where staff turnover is high or ultrasound exposure is limited. Budget constraints also affect procurement in smaller clinics, long-term care facilities, and home care agencies competing for capital. As a result, some providers delay upgrades, share devices across units, and underutilize scanners despite clinical need.

Economic justification can be complicated by reimbursement differences and documentation requirements across care settings. When billing pathways are unclear, some buyers prioritize multifunction ultrasound platforms over dedicated bladder scanners to maximize asset utilization. Procurement cycles in public systems and large hospitals can be lengthy, requiring approvals from infection control, nursing leadership, clinical champions, and biomedical engineering. These multi-stakeholder reviews add friction, extend sales cycles, and slow expansion into new departments.

- For instance, in the United States a dedicated CPT code for post-void residual assessment by pelvic ultrasound (code 76857) carries a national Medicare global payment under 100 dollars per study, while the non-imaging bladder capacity code 51798 reimburses at a significantly lower combined professional and technical rate, which can weaken the business case for stand-alone scanners in low-volume sites.

Bladder Scanners Market Trends and Opportunities

Handheld and smartphone-connected workflows are expanding the reachable customer base by reducing device footprint, simplifying setup, and lowering training time. As care shifts toward outpatient, post-acute, and home-based pathways, compact scanners support assessment outside tertiary hospitals and reduce unnecessary transfers. This creates opportunity for vendors offering intuitive interfaces, guided scanning, and strong after-sales support for distributed sites. Providers also value rapid deployment across multiple points of care to reduce bottlenecks.

- For instance, VSONO‑BL2’s wireless bladder ultrasound scanner connects directly to iOS devices via built‑in Wi‑Fi, enabling clinicians to perform bladder‑volume assessments in under 30 seconds at bedside or in community clinics without external consoles or carts, thereby shortening setup time by more than 50% compared with traditional cart‑based systems.

AI-enabled measurement and workflow automation are emerging differentiators for facilities seeking consistent outcomes across mixed-skill users. Automated bladder detection, instant volume calculation, and decision support reduce operator variability and improve documentation readiness. Faster onboarding supports nursing-led environments and high-throughput settings where repeatability matters. As software upgrades become more frequent, vendors can expand recurring revenue through subscriptions, cloud analytics, service contracts, and feature releases that extend device life and drive upgrades.

Regional Insights

North America

North America accounted for 37.90% of revenue in 2025, supported by high adoption of point-of-care workflows and strong emphasis on catheter avoidance practices. Hospitals and outpatient facilities in the region typically prioritize standardized protocols, which increases routine bladder scanning in emergency and peri-operative pathways. Purchasing decisions often emphasize uptime, infection-control design, and workflow integration. The region also benefits from high device replacement rates and broader availability of trained clinical users.

Europe

Europe represented 27.10% share in 2025, supported by mature hospital infrastructure and broad urology service coverage across public and private systems. Demand is reinforced by quality and safety focus, including reduction of avoidable catheterization and efficient post-operative monitoring. Procurement tends to favor proven performance, durability, and compliance readiness. Adoption is also expanding as outpatient pathways grow and hospitals seek to improve throughput and reduce unnecessary interventions.

Asia Pacific

Asia Pacific captured 22.80% share in 2025 and is positioned for faster growth as hospital capacity expands and diagnostic infrastructure modernizes across key countries. Rising urology caseloads and increasing awareness of non-invasive assessment benefits support broader adoption beyond tertiary centers. Buyers often prioritize cost-effective portability and simplified training to scale usage across multiple sites. The region’s growth is also supported by increasing investment in point-of-care diagnostics and distributed healthcare delivery.

Latin America

Latin America held 7.40% share in 2025, with adoption driven by modernization of hospital equipment fleets and expanding outpatient care networks. Procurement remains price-sensitive, so demand often concentrates on devices with strong durability and clear clinical utility. Growing private hospital networks and improved access to urology services support incremental installations. Service availability and training support can be decisive in vendor selection due to distributed care footprints.

Middle East & Africa

Middle East & Africa accounted for 4.80% share in 2025, reflecting uneven access to advanced point-of-care tools across countries and care settings. Demand is strongest in well-funded hospital clusters and expanding private networks that seek workflow efficiencies and improved patient safety. Vendors that provide robust training, after-sales support, and durable designs can gain share in this region. Over time, expanding healthcare capacity and increasing focus on infection prevention are expected to support steady adoption.

Competitive Landscape

Competition centers on workflow usability, measurement consistency, device durability, and clinical value tied to catheter avoidance and operational efficiency. Vendors differentiate through ergonomics, guided scanning interfaces, portable form factors, and software features that support faster training and consistent outcomes across users. Product positioning increasingly targets broad departmental deployment rather than specialist-only use, expanding the addressable market beyond urology. Service support and uptime assurance also influence purchasing decisions, especially in high-throughput hospitals and multi-site care networks.

Verathon, Inc. is positioned strongly in dedicated bladder scanning by emphasizing clinical workflow integration, ease of use for nursing-led environments, and reliability in high-volume settings. Its approach typically aligns with hospital procurement priorities around standardization, infection-control compatibility, and consistent measurement performance. Continuous product refinement and training enablement support adoption across ED, peri-operative, and inpatient units. This specialization helps sustain replacement demand and supports deeper penetration across hospital departments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Verathon, Inc.

- LABORIE

- dBMEDx

- Vitacon

- Mcube Technology

- Caresono Technology Co., Ltd.

- Suzhou PeakSonic Medical Technology Co., Ltd.

- Clarius Mobile Health

- GE HealthCare

- FUJIFILM Holdings Corporation

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In January 2025, dBMEDx gained renewed attention in the bladder scanner space with coverage of its BBS Revolution automatic wireless bladder scanner, which leverages eight-transducer technology to automatically locate the bladder, transmit volume results wirelessly over more than 30 feet, and eliminate the need for annual calibration to support infection control and workflow efficiency.

- In January 2024, Clarius Mobile Health received U.S. FDA 510(k) clearance for its Clarius Bladder AI solution, a non‑invasive AI tool that automatically measures bladder volume in seconds and is offered alongside the company’s wireless handheld ultrasound scanners such as Clarius PAL HD3, PA HD3, and C3 HD3.

- In January 2024, Verathon, Inc. expanded its bladder scanner portfolio by highlighting the BladderScan i10 system, powered by ImageSense technology, as its next-generation non-invasive ultrasound device designed to automatically measure bladder volume within seconds and streamline electronic health record charting workflows.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 495 million |

| Revenue forecast in 2032 |

USD 797.47 million |

| Growth rate (CAGR) |

7.05% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Technology; By Portability; By End User; By Application |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Verathon, Inc.; LABORIE; dBMEDx; Vitacon; Mcube Technology; Caresono Technology Co., Ltd.; Suzhou PeakSonic Medical Technology Co., Ltd.; Clarius Mobile Health; GE HealthCare; FUJIFILM Holdings Corporation. |

| No. of Pages |

328 |

Segmentation

By Technology

- 2D Ultrasound Bladder Scanners

- 3D Ultrasound Bladder Scanners

By Portability

- Portable / Cart-Based Bladder Scanners

- Handheld Bladder Scanners

- Bench-top Bladder Scanners

By End User

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Diagnostic Centers

- Long-Term Care Facilities / Nursing Homes

- Home Healthcare

By Application

- Urology

- Emergency Medicine

- Obstetrics & Gynecology

- Surgery / Peri-operative Care

- Rehabilitation & Physiotherapy

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa