Blood Bank Market Overview:

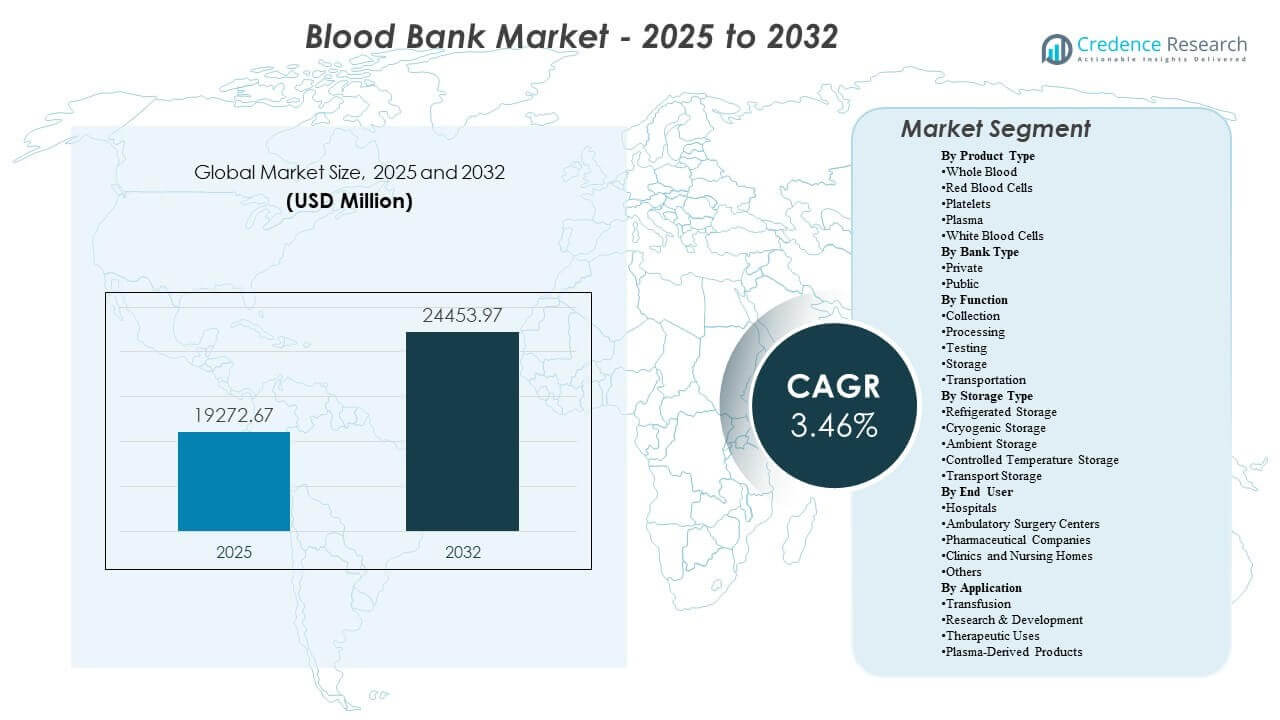

The global Blood Bank Market size was estimated at USD 19,272.67 million in 2025 and is expected to reach USD 24,453.97 million by 2032, growing at a CAGR of 3.46% from 2025 to 2032. Blood Bank Market growth is primarily driven by sustained transfusion demand across surgeries, trauma care, oncology, and chronic anemia management, which keeps collection, testing, and distribution volumes structurally consistent across healthcare systems. Blood Bank Market expansion is also supported by continued modernization of screening workflows and cold-chain infrastructure that improves safety, traceability, and availability across hospital networks.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Blood Bank Market Size 2025 |

USD 19,272.67 million |

| Blood Bank Market, CAGR |

3.46% |

| Blood Bank Market Size 2032 |

USD 24,453.97 million |

Key Market Trends & Insights

- Blood Bank Market is projected to expand at a 3.46% CAGR during 2025–2032, reflecting steady demand supported by essential-care utilization patterns.

- North America accounted for 44% share in 2025, supported by mature donation networks, high testing intensity, and dense hospital coverage.

- Red Blood Cells accounted for the largest share of 41% in 2025, reflecting routine clinical reliance on RBC components for acute and chronic transfusion needs.

- Testing represented 38% share in 2025 within Blood Bank Market functions, reflecting mandatory screening, compliance requirements, and quality systems per unit handled.

- Public blood banks held 56% share in 2025, indicating continued dominance of public donation and distribution infrastructure across many healthcare systems.

Segment Analysis

Blood Bank Market segment performance is shaped by component therapy preferences, compliance-led testing intensity, and the operational reality that reliable donor inflow is the binding constraint in many systems. Blood Bank Market operators increasingly prioritize donor acquisition and retention programs because predictable collection volumes stabilize downstream processing and inventory planning. Blood Bank Market demand also reflects procedure mix changes, with higher surgical throughput and chronic disease management sustaining RBC and platelet utilization while plasma remains important for both transfusion support and plasma-derived value chains.

Blood Bank Market buyer behavior places high weight on safety, traceability, and turnaround time, which increases adoption of standardized workflows and validated storage practices across networked facilities. Blood Bank Market donor participation can be materially influenced by convenience factors, with survey evidence indicating that time-off support can increase donation intent among working-age cohorts. Blood Bank Market institutional partners also continue to expand distribution footprints and service agreements, improving availability across large hospital networks and enabling better inventory balancing during demand spikes.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Product Type Insights

Red Blood Cells accounted for the largest share of 41% in 2025. Blood Bank Market demand concentrates around RBC components because RBC transfusion remains central to surgery support, trauma stabilization, oncology care pathways, and chronic anemia management. Blood Bank Market workflows also favor component therapy, enabling separation, standardized labeling, and predictable storage for RBC inventory. Blood Bank Market distribution systems frequently prioritize RBC availability because RBC shortfalls have immediate clinical impact on high-acuity services.

By Bank Type Insights

Public accounted for the largest share of 56% in 2025. Blood Bank Market structure remains anchored by public donation and distribution networks that operate at scale and support national or regional supply balancing. Blood Bank Market public systems often maintain broad donor access points and centralized processing capabilities that improve standardization. Blood Bank Market public dominance is reinforced where regulation, safety oversight, and public funding frameworks prioritize universal access and continuity of supply across hospitals.

By Function Insights

Testing accounted for the largest share of 38% in 2025. Blood Bank Market cost and value concentration in testing reflects mandatory infectious disease screening, compatibility checks, and quality assurance requirements that apply across most collected units. Blood Bank Market operators invest in validated testing workflows because screening reliability directly impacts safety outcomes and regulatory compliance. Blood Bank Market service differentiation increasingly depends on traceability and audit-ready systems, which further elevates the importance of testing and documentation.

By Storage Type Insights

Blood Bank Market storage activity remains a critical operational layer because blood components require specific temperature and handling conditions to preserve viability and reduce wastage. Blood Bank Market systems typically rely on refrigerated storage for routine component inventory, with frozen or cryogenic capability expanding where plasma programs, fractionation feedstock, or specialty needs are prioritized. Blood Bank Market growth in network distribution increases reliance on controlled temperature monitoring, alarm systems, and validated transport storage. Blood Bank Market providers also emphasize inventory rotation and cold-chain integrity to reduce expiries and improve availability across hub-and-spoke hospital supply models.

By End User Insights

Hospitals accounted for the largest share of 63% in 2025. Blood Bank Market demand is concentrated in hospitals because hospitals manage transfusion-heavy use cases including surgery, trauma, intensive care, oncology, and high-risk obstetrics. Blood Bank Market hospital requirements also elevate demand for rapid cross-matching, reliable component availability, and consistent cold-chain performance to prevent procedure delays. Blood Bank Market hospital networks often shape procurement standards and supplier qualification criteria, influencing broader adoption of standardized testing and distribution workflows.

By Application Insights

Blood Bank Market application mix is led by transfusion needs that are structurally tied to acute care and chronic disease management across healthcare systems. Blood Bank Market activity also includes therapeutic uses supported by apheresis-enabled protocols and specialized clinical pathways that require tighter process control. Blood Bank Market relevance to plasma-derived products increases where collection programs support downstream fractionation and biologics supply security. Blood Bank Market research and development use remains smaller but supports innovation in screening, traceability, and process optimization across collection and laboratory operations.

Blood Bank Market Drivers

Expanding clinical demand for transfusion-supported care pathways

Blood Bank Market demand is sustained by the continuing need for transfusion support across surgeries, trauma incidents, oncology care, and chronic anemia management. Blood Bank Market utilization remains structurally resilient because transfusion is a clinical necessity rather than discretionary consumption. Blood Bank Market volumes also track procedural throughput and hospital occupancy, supporting steady component demand even during moderate economic cycles. Blood Bank Market growth benefits from expansion of specialized care centers that require reliable and rapid access to RBCs, platelets, and plasma.

- For instance, the Aragón ecosystem’s software‑based decision support and data connectivity optimized blood processing across fluctuating activity levels, improving productivity and reducing waste while ensuring timely supply for hospital procedures.

Tightening safety expectations and compliance-driven workflow intensity

Blood Bank Market operations are heavily shaped by safety requirements, increasing the importance of validated testing, documentation, and traceability systems. Blood Bank Market stakeholders prioritize screening rigor to minimize transfusion-transmitted risks and ensure compatibility accuracy. Blood Bank Market compliance practices increase recurring operational demand because each unit must pass standardized testing and quality checks. Blood Bank Market providers that invest in automation and interoperability can reduce errors and improve turnaround time for hospital partners.

- For instance, implementation of a cloud‑based digital sample tracking system at CBT Bonn in Germany reduced missing test tubes from 13.72% to 2.31% across more than 50,000 processed samples, while errors related to inappropriate containers dropped from 0.34% to zero, showing how digital traceability directly strengthens safety.

Modernization of cold-chain infrastructure and inventory management

Blood Bank Market performance depends on maintaining temperature integrity across storage and transportation to preserve component quality and reduce wastage. Blood Bank Market operators continue to upgrade refrigerated, controlled temperature, and transport storage capabilities to support wider distribution networks. Blood Bank Market inventory management improvements help address component shelf-life constraints by enabling better stock rotation and demand forecasting. Blood Bank Market expansion across hospital networks increases the need for consistent cold-chain monitoring and validated logistics practices.

Strengthening donor engagement, convenience, and collection access points

Blood Bank Market supply stability depends on donor participation, making donor recruitment and retention programs central to collection capacity. Blood Bank Market collection performance improves when donation is convenient and aligned with work-life constraints, which increases repeat donor rates and reduces shortage risk. Blood Bank Market organizations also expand fixed-site centers and mobile drives to improve geographic coverage and reduce access barriers. Blood Bank Market systems that coordinate donor scheduling, eligibility screening, and outreach can stabilize inflows and reduce downstream volatility in processing and distribution.

Blood Bank Market Challenges

Blood Bank Market faces persistent supply volatility driven by donor availability, seasonal patterns, and localized demand surges that challenge inventory balancing. Blood Bank Market operators must manage short shelf-life constraints for certain components, which increases wastage risk and operational pressure to align collection and distribution. Blood Bank Market complexity rises when hospital networks expand across multiple sites, requiring consistent testing standards and integrated logistics visibility. Blood Bank Market capacity constraints can become acute during outbreaks, emergencies, or staffing shortages that reduce collection throughput.

- For instance, Carter BloodCare’s transition to Terumo BCT’s Reveos automated whole blood processing platform reduced more than 20 manual steps in component preparation and enabled processing of up to four whole blood units per run, helping centers do more with the same donor base and stabilize supply during peak demand windows.

Blood Bank Market operations also carry high cost sensitivity because safety and compliance requirements are non-negotiable, yet funding models vary widely across health systems. Blood Bank Market organizations must absorb costs for testing, quality systems, cold-chain infrastructure, and specialized workforce capabilities to maintain reliability. Blood Bank Market interoperability challenges can limit data sharing across collection, laboratory, and hospital systems, complicating traceability and performance benchmarking. Blood Bank Market fragmentation in certain geographies can reduce standardization and create uneven access to high-quality transfusion services.

Blood Bank Market Trends and Opportunities

Blood Bank Market is increasingly shaped by automation and digitization across testing, labeling, and inventory control, improving throughput and reducing manual error exposure. Blood Bank Market opportunities also expand in integrated cold-chain monitoring and audit-ready data systems that support compliance and improve hospital confidence. Blood Bank Market providers that standardize workflows across multi-site networks can improve consistency and reduce turnaround time for urgent component requests. Blood Bank Market also benefits from stronger coordination between collection scheduling and hospital demand signals, enabling more efficient stock allocation.

Blood Bank Market opportunity growth is also linked to specialized services associated with therapeutic applications, including apheresis-based procedures and advanced component management. Blood Bank Market stakeholders increasingly emphasize donor experience and retention, creating opportunities in scheduling tools, targeted outreach, and employer-supported donation programs. Blood Bank Market expansion in plasma collection capacity supports broader value chains linked to plasma-derived products and supply security objectives. Blood Bank Market differentiation is likely to increase through network partnerships that improve coverage, responsiveness, and service reliability for large hospital systems.

- For instance, an IoT‑enabled, RFID‑tagged temperature‑monitored blood supply chain deployed between a mother blood bank and a storage center in India recorded continuous bag‑level temperature data and reduced blood wastage at the storage center by 68% over a six‑month implementation period.

Regional Insights

North America

Blood Bank Market in North America held 44% share in 2025, supported by mature donation infrastructure, extensive hospital networks, and standardized screening workflows. Blood Bank Market organizations in the region emphasize reliability, turnaround time, and traceability to support high-volume transfusion demand across acute and specialty care settings. Blood Bank Market operational scale encourages investment in automation and distribution optimization to balance inventory across large catchment areas. Blood Bank Market growth remains linked to sustained clinical utilization patterns and continuous upgrades in testing and cold-chain systems.

Europe

Blood Bank Market in Europe accounted for 23% share in 2025, supported by structured public health systems and established transfusion services across most countries. Blood Bank Market demand is reinforced by compliance-led screening practices and standardized quality requirements across hospital networks. Blood Bank Market procurement decisions in Europe often prioritize safety, consistency, and continuity of supply, supporting investment in validated processes. Blood Bank Market performance depends on reliable donor inflow and efficient inventory rotation across regional distribution hubs.

Asia Pacific

Blood Bank Market in Asia Pacific represented 21% share in 2025, supported by expanding hospital capacity and increasing emphasis on strengthening transfusion infrastructure. Blood Bank Market growth is reinforced by scaling of tertiary care services and rising procedural volumes in major population centers. Blood Bank Market supply dynamics remain mixed across the region due to differences in donation systems, access coverage, and logistics maturity. Blood Bank Market modernization in testing and cold-chain systems creates long-run opportunity as healthcare delivery expands.

Latin America

Blood Bank Market in Latin America held 7% share in 2025, reflecting developing donation networks and uneven infrastructure across countries. Blood Bank Market demand is sustained by expanding hospital services, but operational performance can be constrained by collection capacity and distribution coverage. Blood Bank Market stakeholders increasingly prioritize standardization and safety practices to reduce wastage and improve availability. Blood Bank Market opportunity remains strongest where hospital systems invest in process modernization and cold-chain reliability.

Middle East & Africa

Blood Bank Market in Middle East & Africa accounted for 5% share in 2025, supported by capacity build-out in select countries and gradual expansion of organized transfusion services. Blood Bank Market adoption of modern testing and cold-chain practices is uneven, with advanced systems concentrated in higher-income markets. Blood Bank Market performance is influenced by donor participation rates, infrastructure availability, and logistics reach across large geographies. Blood Bank Market investments in centralized processing and validated transport storage can improve supply reliability and reduce component losses.

Competitive Landscape

Blood Bank Market competition is shaped by the ability to secure consistent donor inflow, operate reliable testing and processing systems, and maintain audit-ready cold-chain distribution. Blood Bank Market participants differentiate through network scale, hospital relationships, turnaround performance, and the breadth of services offered across collection, testing, storage, and transportation. Blood Bank Market positioning also depends on quality system maturity and interoperability across laboratory and hospital workflows. Blood Bank Market leaders tend to invest in automation, standardized protocols, and logistics optimization to improve efficiency and reduce wastage.

The American Red Cross remains central to Blood Bank Market operations through large-scale donor programs, broad distribution reach, and deep alignment with hospital supply needs. The American Red Cross strengthens Blood Bank Market presence by maintaining standardized quality systems and coordinated inventory management to support continuity of supply during demand variability. The American Red Cross also supports Blood Bank Market reliability through partnerships and operational practices that prioritize safety, traceability, and responsiveness. The American Red Cross benefits from institutional trust and infrastructure depth that supports stable collection and distribution at scale.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- The American Red Cross

- Vitalant

- New York Blood Center / New York Blood Centre

- Australian Red Cross Society

- Japanese Red Cross Society

- America’s Blood Centers

- Canadian Blood Services

- American Association of Blood Banks (AABB)

- Sanquin Blood Supply Foundation / Sanquin Bloedvoorziening

- Blood Bank of Alaska

- NHS Blood and Transplant

- Haemonetics Corporation

- Terumo Corporation / Terumo Blood and Cell Technologies

- Grifols S.A.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In February 2026, Haemonetics Corporation announced U.S. FDA 510(k) clearance for its NexSys PCS Plasma Collection System with Persona PLUS technology, representing a next generation, donor tailored plasma collection platform designed to increase average plasma volume per donation and help plasma collectors scale operations more efficiently.

- In September 2025, Blood Bank Computer Systems, Inc. (BBCS) announced a new partnership with Blood Assurance, a nonprofit regional blood center in the U.S., under which BBCS will implement its ForLife Biologics Platform to modernize Blood Assurance’s blood bank management and donor operations.

- In June 2025, the American Red Cross and the U.S. Defense Health Agency’s Armed Services Blood Program entered into a formal partnership to strengthen the national blood supply for military personnel and bolster support for America’s service members through coordinated blood collection, processing and distribution efforts.

- In December 2024, GVS S.p.A. signed a binding agreement to acquire Haemonetics Corporation’s Transfusion Medicine (whole blood) business, adding Haemonetics’ proprietary blood collection, processing, filtration, and transfusion solutions to GVS’s portfolio and strengthening its vertically integrated position in transfusion medicine.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 19,272.67 million |

| Revenue forecast in 2032 |

USD 24,453.97 million |

| Growth rate (CAGR) |

3.46% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Product Type Outlook: Whole Blood, Red Blood Cells, Platelets, Plasma, White Blood Cells;

By Bank Type Outlook: Private, Public;

By Function Outlook: Collection, Processing, Testing, Storage, Transportation;

By Storage Type Outlook: Refrigerated Storage, Cryogenic Storage, Ambient Storage, Controlled Temperature Storage, Transport Storage;

By End User Outlook: Hospitals, Ambulatory Surgery Centers, Pharmaceutical Companies, Clinics and Nursing Homes, Others;

By Application Outlook: Transfusion, Research & Development, Therapeutic Uses, Plasma-Derived Products |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

The American Red Cross, Vitalant, New York Blood Center / New York Blood Centre, Australian Red Cross Society, Japanese Red Cross Society, America’s Blood Centers, Canadian Blood Services, American Association of Blood Banks (AABB), Sanquin Blood Supply Foundation / Sanquin Bloedvoorziening, Blood Bank of Alaska, NHS Blood and Transplant, Haemonetics Corporation, Terumo Corporation / Terumo Blood and Cell Technologies, Grifols S.A. |

| No. of Pages |

340 |

Segmentation

By Product Type

- Whole Blood

- Red Blood Cells

- Platelets

- Plasma

- White Blood Cells

By Bank Type

By Function

- Collection

- Processing

- Testing

- Storage

- Transportation

By Storage Type

- Refrigerated Storage

- Cryogenic Storage

- Ambient Storage

- Controlled Temperature Storage

- Transport Storage

By End User

- Hospitals

- Ambulatory Surgery Centers

- Pharmaceutical Companies

- Clinics and Nursing Homes

- Others

By Application

- Transfusion

- Research & Development

- Therapeutic Uses

- Plasma-Derived Products

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa