Blood Glucose Test Strips Market Overview:

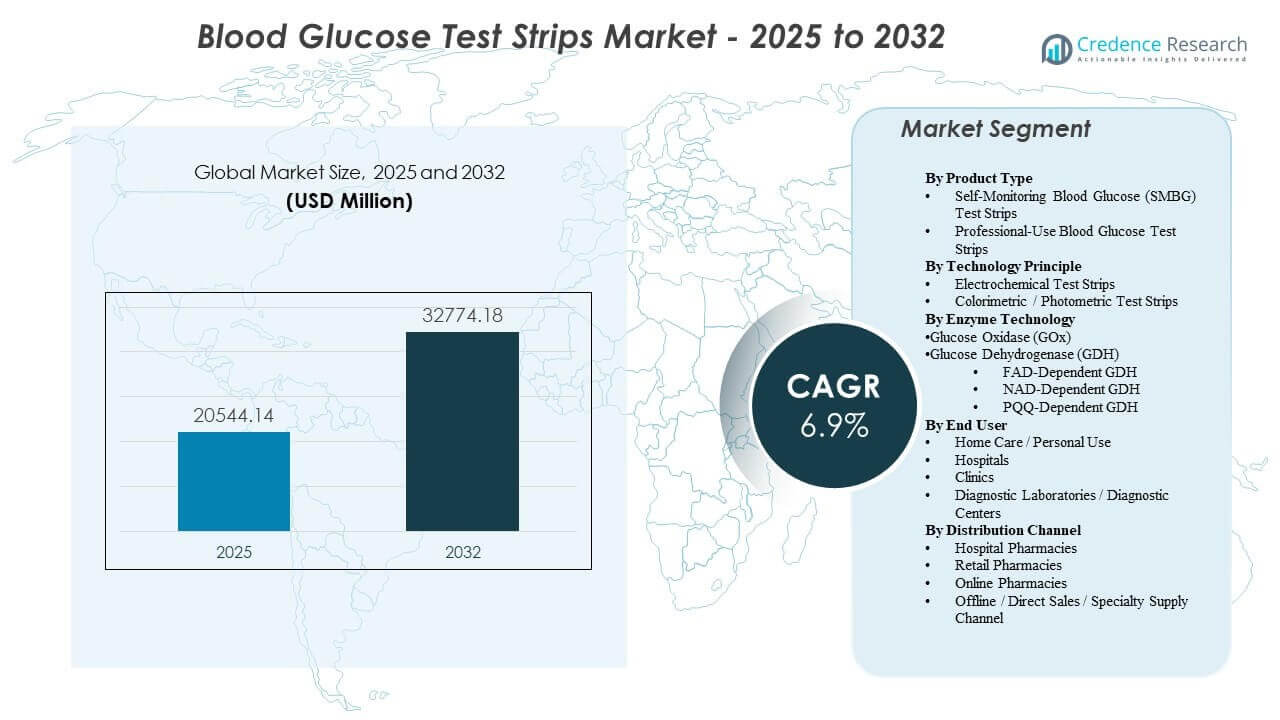

The global Blood Glucose Test Strips Market size was estimated at USD 20,544.14 million in 2025 and is expected to reach USD 32,774.18 million by 2032, growing at a CAGR of 6.9% from 2025 to 2032. Demand expansion is primarily driven by sustained growth in the diagnosed diabetes population and the continued need for frequent, low-cost fingerstick testing to support day-to-day therapy adjustments across insulin and non-insulin regimens. Market purchasing is also shaped by reimbursement rules and distribution access, which influence brand continuity and repeat consumption in chronic users. North America remains the largest revenue contributor in the base year due to higher testing intensity, structured payer coverage, and mature pharmacy fulfillment infrastructure across retail and home-delivery channels.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Blood Glucose Test Strips Market Size 2025 |

USD 20,544.14 million |

| Blood Glucose Test Strips Market, CAGR |

6.9% |

| Blood Glucose Test Strips Market Size 2032 |

USD 32,774.18 million |

Key Market Trends & Insights

- North America accounted for 44.10% of global revenue in 2025, supported by mature reimbursement and high testing adherence.

- Hospital pharmacies represented 54.90% of 2025 sales, reflecting institutional procurement and discharge-linked fulfillment pathways.

- Electrochemical test strips captured 51.40% share in 2025, supported by accuracy expectations and broad device compatibility across high-volume users.

- Hospitals and clinics held 44.50% share in 2025, driven by inpatient glucose management and point-of-care testing intensity.

- The market is projected to expand at 6.9% CAGR from 2025–2032, supported by recurring consumable demand in chronic monitoring.

Segment Analysis

Demand dynamics in the Blood Glucose Test Strips Market remain anchored in recurring use patterns, coverage-driven purchasing, and device ecosystem stickiness. Many buyers evaluate strip options through a total-cost lens that combines per-test pricing with reimbursement eligibility and channel access, which can reinforce preferred brands over time. Connectivity expectations are also rising, shifting differentiation toward reliability, data capture, and ease of reordering rather than single-point product features. These forces collectively sustain high baseline utilization in established markets, even as therapy pathways evolve.

Channel structure and care setting mix continue to shape volume distribution. Institutional demand is maintained by inpatient protocols, perioperative monitoring, and emergency care pathways, which translate into consistent high-frequency testing. At the same time, home-based management drives steady replenishment cycles and supports growth in fulfillment models such as subscription refills and home delivery. Competitive positioning therefore depends on a company’s ability to secure formulary placement, maintain meter-strip compatibility, and deliver dependable supply through high-reach pharmacy and direct channels.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Product Type Insights

Self-monitoring demand leads overall consumption because routine testing at home creates repeat purchasing cycles and higher test frequency across chronic users. Personal-use buyers often prioritize consistent availability, affordability within coverage rules, and compatibility with an existing meter ecosystem. Professional-use volumes remain important in inpatient and outpatient workflows, but utilization is more episodic and tied to clinical encounters. The resulting mix typically favors consumer replenishment patterns even when clinical settings remain influential in initiating device adoption.

By Technology Principle Insights

Electrochemical test strips accounted for the largest share of 51.40% in 2025. Electrochemical principles are widely selected because they align with accuracy expectations and robust performance across typical point-of-care and home-use conditions. Meter and strip ecosystem lock-in further supports this leadership, as switching costs can be meaningful for both institutions and individual users. Standardized workflows, familiarity among providers, and stable large-scale manufacturing also reinforce electrochemical dominance.

By Enzyme Technology Insights

Enzyme selection is driven by a balance of accuracy requirements, interference profiles, and production consistency in high-volume strip manufacturing. Many manufacturers use established enzyme systems because they support predictable performance under common usage conditions and facilitate regulatory continuity across product generations. Procurement and reimbursement considerations also favor stable product configurations that minimize user retraining and support consistent outcomes. As a result, adoption patterns often reflect installed-base compatibility and supply reliability as much as pure technical differentiation.

By End User Insights

Hospitals and clinics accounted for the largest share of 44.50% in 2025. Clinical environments sustain high strip consumption through inpatient glucose management protocols, perioperative monitoring needs, and frequent testing in acute-care pathways. Point-of-care workflows value standardized performance and dependable supply, which supports purchasing concentration through preferred contracts. Clinical usage also influences brand familiarity and continuity when patients transition to home monitoring after discharge.

By Distribution Channel Insights

Hospital pharmacies accounted for the largest share of 54.90% in 2025. Institutional purchasing and formulary decisions often centralize distribution through hospital pharmacies, particularly when strips are linked to inpatient protocols or discharge planning. These channels also benefit from contract pricing, predictable stocking, and streamlined clinical workflows. Retail and online channels continue to expand as chronic users seek convenient replenishment, but hospital pharmacy dominance persists where coverage rules and institutional procurement remain strong.

Blood Glucose Test Strips Market Drivers

Rising Diabetes Prevalence and Chronic Monitoring Requirements

The diagnosed diabetes population continues to expand, increasing the number of individuals who require routine blood glucose monitoring. Test strips remain a widely used consumable because they enable frequent, low-cost measurements that support therapy decisions. Many care plans still rely on fingerstick testing for structured monitoring routines, particularly for insulin titration and day-to-day management. This persistent need for recurring consumables sustains baseline volume growth across mature and developing markets.

- For instance, a 12‑year utilization review in Canada found that blood glucose test strip use increased by 121% as the number of insulin users rose by 115%, underscoring how expanding diagnosed populations translate directly into higher strip consumption.

Reimbursement Coverage and Procurement Pathways Supporting Volume

Payer policies, tendering, and formulary placement strongly influence brand selection and repeat purchasing behavior. When strips are covered under preferred plans, users are more likely to maintain consistent usage patterns and replenish regularly. Institutional procurement can further concentrate volume through selected suppliers, reinforcing scale advantages for companies with strong contracting capabilities. These mechanisms collectively support stable demand even when pricing pressure increases.

Care-Setting Expansion and Home-Based Disease Management

Out-of-hospital care models continue to expand, increasing the importance of home monitoring as part of ongoing diabetes management. Test strips fit well in home settings because they are familiar, portable, and supported by broad channel availability. Home-based routines also support recurring purchasing cycles through pharmacy refills and direct supply programs. This shift increases the strategic value of high-reach distribution and customer retention tools such as refill reminders and subscription programs.

- For instance, large U.S. employers such as Johnson & Johnson have implemented benefits that provide employees with free meters and 200 test strips per year when elevated fasting glucose is detected, institutionalizing home-based testing and transforming one-time screenings into repeat strip usage.

Product Ecosystem Stickiness and Compatibility Dynamics

Meter-strip compatibility creates ecosystem lock-in that reduces switching behavior once a device is adopted. Buyers often remain with a compatible strip supply due to convenience, familiarity, and coverage alignment. Institutional settings also prefer standardized devices and consumables to maintain workflow consistency and reduce training burden. These factors support ongoing demand for incumbent brands and strengthen competitive advantages for suppliers with large installed bases.

Blood Glucose Test Strips Market Challenges

Pricing pressure remains a persistent challenge, particularly where reimbursement caps, tendering, or preferred-product lists drive down per-test economics. Competitive bidding can compress margins and increase volume concentration among a smaller set of contracted suppliers, raising barriers for smaller brands. Supply continuity and inventory management are also critical, as shortages can quickly disrupt patient adherence and institutional workflows. Companies must therefore balance cost control with quality assurance and resilient production planning.

- For instance, in several low- and middle-income countries, median retail prices for blood glucose test strips from multinational brands such as Abbott and Roche range from 0.27 to 0.56 US dollars per strip, leading large public tenders to concentrate purchases with a few lowest-bid suppliers and compress margins for other manufacturers.

Substitution risk from alternative monitoring approaches can reshape demand patterns in certain patient cohorts, especially where continuous monitoring adoption accelerates. Even when substitution is partial, it can reduce testing frequency for some users and shift value emphasis toward integrated monitoring ecosystems. At the same time, variability in patient adherence and disparities in access can constrain volume growth in emerging markets. Managing these challenges requires flexible channel strategies, differentiated value propositions, and strong payer and provider engagement.

Market Trends and Opportunities

Pharmacy fulfillment is evolving toward convenience-led models that support recurring purchasing behavior, including home delivery and automated refills. This trend is particularly relevant for chronic users who value predictable supply and reduced friction in reordering. Suppliers that optimize digital ordering, customer support, and distribution reliability can strengthen retention and improve share in expanding channels. The shift also creates opportunities to bundle services, education, and monitoring support alongside consumable replenishment.

- For instance, Optum Home Delivery reports shipping 98% of prescriptions within two days while maintaining a 99.998% dispensing accuracy rate, and a Veterans Health Administration pilot of automatic mailed prescription refills for diabetes patients increased the medication possession ratio for reference medicines from 54.5% to 63.9% over six months.

Connectivity and data-driven care workflows are increasing expectations for monitoring products that integrate smoothly into digital health ecosystems. Even for strip-based testing, buyers increasingly value reliable data capture, interoperability, and ease of sharing results with providers. These preferences support innovation in user experience, companion apps, and integration with care management programs. Companies that pair consumables with stronger data workflows can defend share and improve differentiation as competition intensifies.

Regional Insights

North America

North America led the Blood Glucose Test Strips Market with a 44.10% share in 2025 due to high testing intensity and well-established reimbursement pathways. The region benefits from broad access to pharmacy channels and strong fulfillment infrastructure that supports recurring replenishment. Institutional procurement and structured disease management programs reinforce stable volume through preferred products and standardization. The United States remains the primary demand center, supported by payer coverage and high prevalence of diabetes requiring frequent monitoring.

Europe

Europe held an estimated 22.35% share in 2025, supported by structured diabetes care pathways and established reimbursement in many countries. Demand remains steady due to routine monitoring practices and strong clinical engagement in chronic care management. Pricing controls and tendering can increase competitive pressure, but overall utilization remains supported by wide access through pharmacies and clinical networks. Major markets including Germany, the United Kingdom, France, and Italy anchor regional consumption.

Asia Pacific

Asia Pacific accounted for an estimated 21.05% share in 2025, driven by large diabetes populations and expanding access to monitoring supplies. Growth is supported by increasing diagnosis rates and gradual improvements in affordability and distribution reach. However, lower per-patient strip usage in some markets and variability in reimbursement coverage can temper base-year share. China and India remain key contributors as monitoring penetration increases across urban and semi-urban settings.

Latin America

Latin America represented an estimated 7.65% share in 2025, with demand shaped by public procurement dynamics and retail pharmacy access. Utilization is meaningful in larger economies, but price sensitivity and coverage variability can limit consistent high-frequency testing. Supply-chain reliability and tender outcomes can influence brand share and channel mix year to year. Brazil and Mexico remain core markets due to scale and established distribution networks.

Middle East & Africa

The Middle East & Africa accounted for an estimated 4.85% share in 2025, reflecting uneven access across countries. GCC markets contribute a larger portion of regional demand due to stronger hospital procurement and coverage structures. Broader regional growth can be constrained by affordability, distribution gaps, and variable care access in several countries. Suppliers often compete on channel partnerships, reliability of supply, and product affordability to expand penetration.

Competitive Landscape

Competition in the Blood Glucose Test Strips Market is shaped by installed-base ecosystems, reimbursement positioning, and channel access. Suppliers compete to secure preferred status with payers and institutions, maintain meter-strip compatibility, and deliver reliable supply at scale through high-volume pharmacy networks. Differentiation increasingly includes data workflows and user experience features that support adherence and easier replenishment. Pricing pressure and procurement cycles elevate the importance of contracting capabilities, manufacturing efficiency, and distribution reach.

Abbott Laboratories operates with a broad diabetes monitoring footprint and leverages scale advantages in distribution and brand recognition across multiple care settings. The company’s approach typically emphasizes integration across monitoring workflows, channel access, and continued product enhancement aligned with patient and provider expectations. Large installed bases support recurring consumable demand, and strong commercial execution helps defend placement in key channels. Abbott Laboratories also benefits from global reach that supports portfolio positioning across both mature and emerging markets.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- F. Hoffmann-La Roche Ltd

- LifeScan IP Holdings, LLC

- ARKRAY Inc.

- Ascensia Diabetes Care Holdings AG

- AgaMatrix

- Bionime

- Sinocare

- Trividia Health

- Rossmax

- Ypsomed

- SD Biosensor Inc.

- TaiDoc Technology

- i-SENS Inc.

- Omron Healthcare Co., Ltd.

- Nova Biomedical

- 77 Elektronika Kft.

- OK Biotech Co., Ltd.

- ACON Laboratories

- Prodigy Diabetes Care, LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In February 2026, LifeScan entered a transformational partnership with i SENS Inc. to develop and launch a OneTouch branded continuous glucose monitoring system (OneTouch Vita), marking LifeScan’s strategic expansion beyond traditional blood glucose meters and test strips into the CGM segment, with initial launches planned in European markets by early 2027.

- In February 2026, i SENS Inc. was named as LifeScan’s global biosensor partner in this CGM collaboration, under which i SENS will supply sensor technology and manufacturing capabilities for the OneTouch Vita continuous glucose monitoring system, strengthening its position as a key technology provider in glucose monitoring solutions

- In October 2025, F. Hoffmann-La Roche Ltd introduced a new glucose monitoring solution in the Middle East, supporting broader adoption of advanced monitoring workflows within the region.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 20,544.14 million |

| Revenue forecast in 2032 |

USD 32,774.18 million |

| Growth rate (CAGR) |

6.9% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Product Type Outlook: Self-Monitoring Blood Glucose (SMBG) Test Strips, Professional-Use Blood Glucose Test Strips;

By Technology Principle Outlook: Electrochemical Test Strips, Colorimetric / Photometric Test Strips;

By Enzyme Technology Outlook: Glucose Oxidase (GOx), Glucose Dehydrogenase (GDH) (FAD-Dependent GDH, NAD-Dependent GDH, PQQ-Dependent GDH, PQQ-Dependent GDH);

By End User Outlook: Home Care / Personal Use, Hospitals, Clinics, Diagnostic Laboratories;

By Distribution Channel Outlook: Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Offline / Direct Sales / Specialty Supply Channel |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Abbott Laboratories; F. Hoffmann-La Roche Ltd; LifeScan IP Holdings, LLC; ARKRAY Inc.; Ascensia Diabetes Care Holdings AG; AgaMatrix; Bionime; Sinocare; Trividia Health; Rossmax; Ypsomed; SD Biosensor Inc.; TaiDoc Technology; i-SENS Inc.; Omron Healthcare Co., Ltd.; Nova Biomedical; 77 Elektronika Kft.; OK Biotech Co., Ltd.; ACON Laboratories; Prodigy Diabetes Care, LLC |

| No. of Pages |

340 |

Segmentation

By Product Type

- Self-Monitoring Blood Glucose (SMBG) Test Strips

- Professional-Use Blood Glucose Test Strips

By Technology Principle

- Electrochemical Test Strips

- Colorimetric / Photometric Test Strips

By Enzyme Technology

- Glucose Oxidase (GOx)

- Glucose Dehydrogenase (GDH)

- FAD-Dependent GDH

- NAD-Dependent GDH

- PQQ-Dependent GDH

By End User

- Home Care / Personal Use

- Hospitals

- Clinics

- Diagnostic Laboratories

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Offline / Direct Sales / Specialty Supply Channel

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa