Blood Pressure Cuffs Market Overview

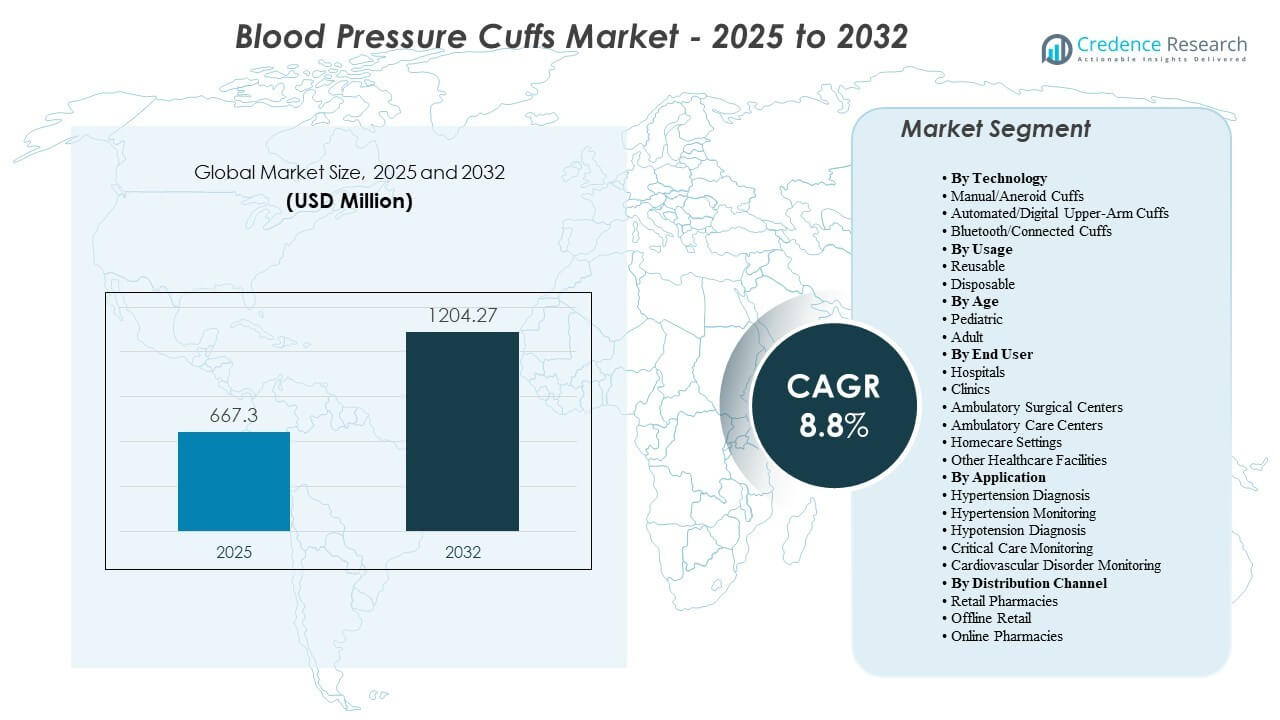

The global blood pressure cuffs market size was valued at USD 667.3 million in 2025 and is expected to reach USD 1,204.27 million by 2032, growing at a CAGR of 8.8% from 2025 to 2032. Rising hypertension screening volumes across primary care and hospitals, along with wider adoption of automated monitoring in routine workflows, is supporting demand. In addition, infection-control protocols are influencing replacement cycles and purchasing decisions, increasing use across reusable and disposable cuff formats. North America accounted for 40% of the market in 2025, while automated cuffs held the largest technology share at 50%.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Blood Pressure Cuffs Market Size 2025 |

USD 667.3 million |

| Blood Pressure Cuffs Market , CAGR |

8.8% |

| Blood Pressure Cuffs Market Size 2032 |

USD 1,204.27 million |

Key Market Trends & Insights

- The market is expected to expand from USD 667.3 million (2025) to USD 1,204.27 million (2032).

- The market is projected to grow at a CAGR of 8.8% during 2025–2032.

- North America accounted for 40% of the market in 2025, supported by high testing frequency and broad clinical adoption.

- Automated/Digital Upper arm Cuffs held 50% of the technology segment in 2025, reflecting demand for faster, operator-independent measurements.

- Reusable cuffs accounted for 65% of the usage segment in 2025, driven by cost efficiency in high-volume care settings.

Blood Pressure Cuffs Market Segment Analysis

Demand patterns reflect two parallel needs: high-throughput clinical measurement and expanding monitoring beyond traditional hospital environments. Hospitals and outpatient facilities sustain steady procurement due to continuous vital-sign workflows, while home-based monitoring ecosystems reinforce demand for standardized cuff sizing and user-friendly designs. Product performance expectations increasingly focus on measurement consistency, comfort across repeated readings, and durability under disinfection routines. Over the forecast period, vendors that offer broad size ranges, compatibility with common monitors, and clear differentiation across reusable and disposable portfolios are likely to capture institutional demand.

Purchasing decisions vary by care setting and protocol requirements. Clinical buyers typically prioritize lifecycle cost, cleaning compatibility, and supply continuity, while home-use demand favors convenience, ease of application, and integration with digital monitoring devices. These dynamics support a market structure where automated solutions and institutional replacement cycles anchor volume, and connected monitoring trends expand the addressable base for advanced configurations.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Technology Insights

Automated/Digital Upper arm Cuffs accounted for the largest share of 50% in 2025. This position is supported by routine vitals workflows that prioritize fast readings and reduced operator dependency across hospitals and clinics. Automated configurations align with standardized measurement practices, improving throughput during screening and follow-up monitoring. Demand also benefits from broad device compatibility in patient monitoring systems and routine ambulatory care use.

By Usage Insights

Reusable accounted for the largest share of 65% in 2025. Reusable cuffs remain preferred in high-volume environments where total cost of ownership and product longevity influence purchasing decisions. Cleaning and disinfection compatibility supports continued adoption under infection-control protocols without shifting entirely to single-use. Reusable portfolios also offer wider size availability, supporting consistent measurement across diverse adult and pediatric populations.

By Age Insights

Adult demand typically concentrates market volume because hypertension prevalence rises with age and monitoring frequency increases with chronic disease management and cardiovascular risk screening. Adult sizing breadth, including large adult and bariatric options, supports consistent procurement across care settings. Pediatric demand remains essential for accurate measurement in neonatal and pediatric care, where precise sizing and softer materials are operational priorities.

By End User Insights

Hospitals accounted for the largest share of 55% in 2025. Hospital demand is sustained by continuous use across emergency, inpatient wards, ICU, and perioperative settings, which increases utilization intensity and replacement frequency. Standardization initiatives and device compatibility requirements also support recurring purchases of clinically validated cuffs. Homecare settings are expanding with remote monitoring programs, but hospital workflows continue to anchor the largest share in the base year.

By Application Insights

. Hypertension diagnosis and monitoring continue to represent the core usage base because blood pressure measurement is a routine vital sign and a primary tool for cardiovascular risk management. Critical care monitoring increases cuff utilization frequency, especially in high-acuity settings where repeated readings are needed. Cardiovascular disorder monitoring supports broader adoption by integrating blood pressure measurement into multi-parameter assessment pathways.

By Distribution Channel Insights

Retail and offline channels support home-use replenishment and replacement needs, particularly for common cuff sizes associated with consumer monitoring devices. Online pharmacies and e-commerce channels continue to expand access, supporting faster replacement cycles and broader product choice. Institutional procurement remains the main pathway for clinical-grade cuffs, while consumer channels support incremental demand tied to home monitoring adoption.

Blood Pressure Cuffs Market Drivers

Expansion Of Hypertension Screening And Chronic Monitoring

Hypertension screening continues to expand as health systems emphasize early detection and ongoing risk management. Regular blood pressure measurement remains a primary clinical tool for diagnosis, therapy titration, and adherence tracking. Higher visit volumes for chronic disease follow-up increase routine cuff utilization across primary and specialty care. These patterns support recurring purchases and replacement cycles for cuffs across multiple care settings.

- For instance, the India Hypertension Control Initiative scaled protocol‑driven screening and treatment across more than 100 districts and reported control rates above 50% among registered hypertensive patients in several participating facilities after implementation, demonstrating the impact of systematic blood pressure measurement on long-term follow-up volumes and device use.

Shift Toward Automated Measurement Workflows In Clinical Settings

Clinical environments increasingly adopt automated workflows to improve throughput and reduce measurement variability. Automated cuffs align with patient monitoring systems and standardized protocols in inpatient and outpatient settings. Routine vitals collection in high-volume clinics supports steady demand for automated configurations and compatible accessories. This shift also strengthens demand for cuffs designed for durability and repeated disinfection.

- For instance, studies of the BpTRU automated office blood pressure device showed strong agreement with ambulatory blood pressure in a cohort of 309 patients referred for hypertension evaluation, supporting its use to standardize readings and reduce white‑coat effects in routine clinical practice.

Infection Control Protocols Supporting Replacement Demand

Infection-control requirements influence product selection and replacement frequency, especially in higher-acuity environments. Facilities often require cleaning compatibility, durable materials, and clear labeling for safe reuse practices. In specific units, single-patient or single-use protocols increase adoption of disposable cuffs to reduce cross-contamination risk. These protocols support ongoing demand across both reusable and disposable categories.

Growth In Home Monitoring And Remote Care Pathways

Home monitoring adoption is increasing as patients and providers track blood pressure outside traditional care settings. Remote follow-up and chronic condition management programs contribute to more frequent measurements over longer periods. This increases demand for comfortable, easy-to-apply cuffs and consistent sizing that reduces user error. Connected monitoring trends also support incremental demand for cuffs aligned with app-enabled and digitally integrated devices.

Blood Pressure Cuffs Market Challenges

Cuff sizing, fit, and user technique remain critical barriers to consistent readings across care settings. Inadequate cuff selection can affect measurement accuracy, which can undermine clinical confidence and increase the need for repeated measurements. Training gaps for home users and variation in clinical practice can also introduce inconsistency across populations. These factors raise the importance of clear sizing guidance and standardization.

- For instance, validation work on the Omron HEM‑1040 home monitor found mean device‑observer differences of −2.7 ± 5.89 mmHg systolic and −3.3 ± 4.99 mmHg diastolic, indicating that even validated devices require proper user technique to stay within international accuracy thresholds.

Supply continuity and product compatibility requirements can complicate procurement, especially where facilities use multiple monitor brands across departments. Standardizing cuff inventories while meeting department-specific needs may increase complexity for purchasing teams. Infection-control compliance also increases operational burden for reusable products, requiring consistent cleaning workflows and materials that tolerate repeated disinfection. These dynamics can influence total cost of ownership and purchasing decisions.

Blood Pressure Cuffs Market Trends and Opportunities

Connected monitoring adoption is increasing focus on integration, data continuity, and patient engagement. Cuffs that support digital ecosystems can benefit from demand tied to remote monitoring programs and home-care follow-up. Product differentiation increasingly centers on comfort, ease of placement, and repeat-measurement usability, especially for chronic monitoring. These trends create opportunities for portfolio upgrades and bundled solutions aligned with monitoring devices.

- For instance, Smart Meter’s iBloodPressure Classic is sold as a multi‑cuff RPM bundle with three cuff sizes (covering arm circumferences from 8.6 to 20.5 inches) that feed directly into its population‑level RPM analytics platform for chronic hypertension management.

Hospitals and outpatient networks continue to emphasize standardization across clinical pathways to reduce variability. This supports demand for cuffs designed around consistent performance, wide size ranges, and durable materials compatible with disinfection workflows. Growth of ambulatory care and outpatient procedural volumes also expands points of measurement beyond inpatient settings. Vendors that align offerings to these operational priorities can strengthen institutional penetration.

Regional Insights

North America

North America accounted for 40% of the market in 2025, supported by high screening frequency, broad clinical adoption, and established monitoring workflows across hospitals and clinics. Procurement often prioritizes standardization, durability, and compatibility with installed monitoring systems. Demand also benefits from expanding chronic disease management pathways and routine outpatient vital sign measurement.

Europe

Europe captured 27% share in 2025, supported by strong primary care systems and structured cardiovascular risk management practices. Hospitals and clinics sustain demand through routine vitals checks and chronic monitoring programs. Purchasing emphasis often includes compliance, product consistency, and suitability for standardized workflows across multi-site networks.

Asia Pacific

Asia-Pacific held 26% share in 2025, supported by expanding access to routine screening, growth in outpatient care volumes, and rising focus on chronic disease management. Increasing use of home monitoring in urban centers contributes to incremental demand for consumer-compatible cuffs and replacement products. Expansion of healthcare infrastructure also supports institutional procurement growth over the forecast period.

Latin America

Latin America accounted for 3% of the global Blood Pressure Cuffs Market in 2025, supported by rising hypertension screening in urban centers and steady procurement from hospitals and outpatient networks. Public health initiatives focused on cardiovascular risk management continue to increase routine blood pressure checks in primary care. Growth in private clinics and diagnostic chains also supports recurring demand for replacement cuffs and standardized accessories.

Middle East & Africa

Middle East & Africa represented 3% of the global market in 2025, driven by gradual expansion of healthcare infrastructure, increasing chronic disease burden, and higher adoption of routine monitoring in hospitals and clinics. Investments in hospital capacity and outpatient care delivery improve access to basic vital-sign monitoring. Procurement growth is also supported by infection-control protocols and periodic replacement cycles in high-acuity settings.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Competitive Landscape

Competition centers on product breadth, compatibility with common monitoring systems, and performance consistency across repeated measurements. Suppliers differentiate through broad cuff size portfolios, material durability under disinfection routines, and configurations spanning reusable, disposable, and digital-adjacent offerings. Institutional buyers typically prioritize lifecycle cost, supply continuity, and compliance with infection-control requirements, which reinforces the role of established distribution and service capabilities.

OMRON Corporation continues to emphasize innovation in home monitoring ecosystems, including expanded capabilities aligned with digital monitoring and user-friendly device experiences. This direction supports demand for automated upper-arm configurations and accessories that align with repeat-use monitoring patterns. Product development focus on clinical utility at home and improved user confidence can reinforce brand positioning in both consumer and clinical-adjacent segments. Not specified in the provided inputs.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- OMRON Corporation

- Baxter International Inc.

- Koninklijke Philips N.V.

- GE HealthCare Technologies Inc.

- McKesson Corporation

- Cardinal Health Inc.

- B. Braun Melsungen AG

- Halma plc

- Medline Industries LP

- Microlife Corporation

- Mindray

- SunTech Medical

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments

- In January 2026, Hillrom (Baxter International) announced the launch of its new Welch Allyn FlexiPort EcoCuff blood pressure cuff line, designed with PVC- and DEHP‑free materials to support hospital sustainability goals in non‑invasive blood pressure monitoring applications

- In October 2025, Omron Healthcare introduced an updated range of Bluetooth‑enabled home blood pressure monitors featuring improved, multi‑size upper‑arm cuffs and enhanced smartphone‑app connectivity as part of its strategy to expand remote hypertension management solutions.

- In September 2025, Baxter International Inc. launched the Welch Allyn Connex 360 Vital Signs Monitor, a next‑generation connected device that captures non‑invasive blood pressure alongside other vital signs in under a minute, enhancing the clinical use of compatible cuffs and advancing its connected monitoring portfolio.

- In August 2025, GE HealthCare secured a blood pressure cuffs and associated consumables supply contract with an NHS contracting authority in the United Kingdom to provide non‑invasive blood pressure cuffs integrated with its patient‑monitoring systems for the contract period through March 2026.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 667.3 million |

| Revenue forecast in 2032 |

USD 1,204.27 million |

| Growth rate (CAGR) |

8.8% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Technology, By Usage, By Age, By End User, By Application, By Distribution Channel |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

OMRON Corporation; Baxter International Inc.; Koninklijke Philips N.V.; GE HealthCare Technologies Inc.; McKesson Corporation; Cardinal Health Inc.; B. Braun Melsungen AG; Halma plc; Medline Industries LP; Microlife Corporation; Mindray; SunTech Medical. |

Segmentation

BY TECHNOLOGY

- Manual/Aneroid Cuffs

- Automated/Digital Upper arm Cuffs

- Bluetooth/Connected Cuffs

BY USAGE

BY AGE

BY END USER

- Hospitals

- Clinics

- Ambulatory Surgical Centers

- Ambulatory Care Centers

- Homecare Settings

- Other Healthcare Facilities

BY APPLICATION

- Hypertension Diagnosis

- Hypertension Monitoring

- Hypotension Diagnosis

- Critical care Monitoring

- Cardiovascular Disorder Monitoring

BY DISTRIBUTION CHANNEL

- Retail Pharmacies

- Offline Retail

- Online Pharmacies

BY REGION

- North America

- Europe

- Asia-Pacific

- South America

- Middle East and Africa