Blood Purification Equipment Market Overview:

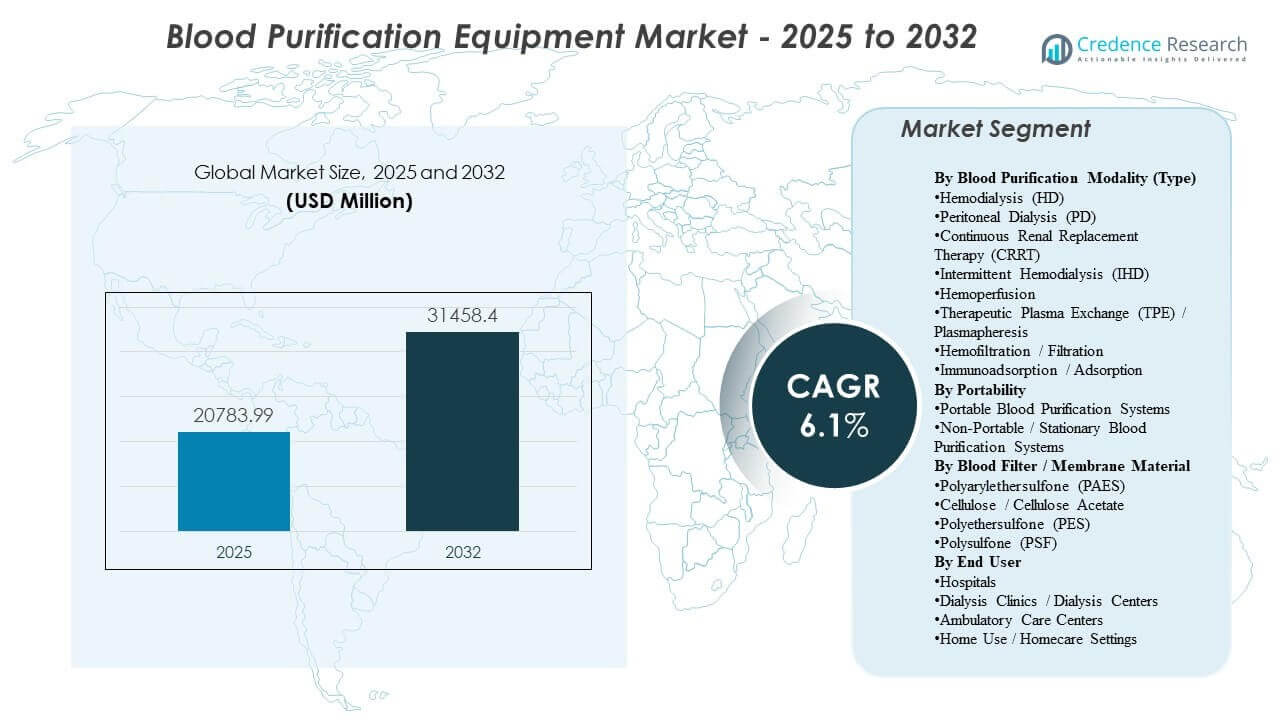

The global Blood Purification Equipment Market size was estimated at USD 20,783.99 million in 2025 and is expected to reach USD 31,458.4 million by 2032, growing at a CAGR of 6.1% from 2025 to 2032. Demand expansion is primarily supported by the rising chronic kidney disease and end-stage renal disease treatment burden, which sustains recurring utilization of dialysis equipment and consumables across organized care settings. Blood Purification Equipment Market growth is further reinforced by care delivery modernization, including equipment upgrades, expanding treatment capacity, and gradual migration of select therapies toward lower-acuity and home-based environments.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Blood Purification Equipment Market Size 2025 |

USD 20,783.99 million |

| Blood Purification Equipment Market, CAGR |

6.1% |

| Blood Purification Equipment Market Size 2032 |

USD 31,458.4 million |

Key Market Trends & Insights

- Intermittent Hemodialysis (IHD) accounted for the largest modality share of ~51.4% (2025), reflecting the dominant installed base and routine ESRD treatment volumes.

- Hemodialysis systems represented ~58.9% share (2025) of equipment demand, indicating hemodialysis remains the core modality versus alternative purification approaches.

- Hospitals and dialysis centers contributed ~72.6% share (2025) of end-user demand, underscoring the concentration of therapy delivery in organized treatment networks.

- North America represented 39.3% share (2025), maintaining the largest regional contribution supported by mature reimbursement, high treatment penetration, and established provider networks.

- Portable blood purification equipment is projected to expand supported by care-shift momentum and technology enabling lower-footprint deployment.

Segment Analysis

Blood Purification Equipment Market demand is anchored in high-frequency renal replacement therapy delivery, where installed-base economics support stable capital replacement cycles and consistent consumables pull-through. Provider procurement decisions are typically influenced by therapy throughput, system reliability, and the ability to standardize workflows across multi-site networks. Blood Purification Equipment Market adoption dynamics are also shaped by the growing need to manage complex patients, which increases interest in broader therapy capabilities across acute and chronic care pathways.

Blood Purification Equipment Market buying behavior increasingly prioritizes operational efficiency, service coverage, and supply continuity for membranes, cartridges, tubing sets, and other high-volume consumables. The market also shows gradual expansion beyond routine dialysis into specialized purification approaches used in critical care and toxin removal settings, which supports differentiated positioning for adsorption and hemoperfusion technologies. These dynamics collectively reinforce a mixed growth profile in which mature modalities sustain volume, while advanced therapies improve the overall value mix.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Blood Purification Modality (Type) Insights

Intermittent Hemodialysis (IHD) accounted for the largest share of 51.4% in 2025. Blood Purification Equipment Market leadership for IHD is supported by standardized clinical protocols, a large installed base across dialysis networks, and predictable scheduling that enables high patient throughput. Reimbursement structures and procurement preferences also favor modalities with stable consumables utilization and well-established service pathways. Continuous and specialty purification modalities expand the overall therapy mix, but routine ESRD care volumes keep IHD central to modality demand.

By Portability Insights

Portable systems lead Blood Purification Equipment Market demand in settings that prioritize flexibility of deployment, compact footprints, and workflow simplification. Portable adoption is supported by the gradual shift of select therapies toward home and lower-acuity environments, where space constraints and ease of setup are critical. Providers also emphasize usability features that reduce staffing intensity and training complexity across distributed sites. Connectivity and remote monitoring capabilities further strengthen the value proposition of portable configurations for longitudinal care management.

By Blood Filter / Membrane Material Insights

Membrane material selection in the Blood Purification Equipment Market is primarily influenced by biocompatibility, clearance performance, sterilization compatibility, and cost-to-performance trade-offs. Synthetic membrane families are widely preferred for consistent filtration characteristics and scalable manufacturing, which supports procurement standardization in high-volume dialysis networks. Clinical preferences for higher-flux performance and improved hemocompatibility drive ongoing innovation in polymer blends and surface modifications. Supply assurance and quality consistency remain central evaluation criteria because membrane availability directly impacts therapy continuity.

By End User Insights

Hospitals and dialysis centers accounted for the largest share of 72.6% in 2025. Blood Purification Equipment Market concentration in organized care sites is driven by infrastructure requirements such as water treatment, infection control protocols, and specialized staffing, which remain essential for high-throughput dialysis delivery. Dialysis networks also benefit from economies of scale in procurement, maintenance, and training, reinforcing centralized purchasing behavior. Home use and ambulatory care settings are expanding, but organized treatment sites continue to dominate overall utilization and equipment deployment.

Blood Purification Equipment Market Drivers

Rising chronic kidney disease and ESRD treatment burden

Blood Purification Equipment Market growth is strongly supported by the increasing prevalence of chronic kidney disease and progression to end-stage renal disease across aging populations and high-risk groups. Higher treatment volumes raise recurring utilization of dialysis equipment, membranes, and related consumables. Provider networks expand capacity through new centers, incremental chair additions, and equipment upgrades that improve throughput and reliability. These factors collectively sustain long-cycle demand for both capital equipment and high-frequency disposables.

- For instance, Fresenius Medical Care reported delivering more than 44 million dialysis treatments globally in 2023 through a network of over 3,600 dialysis centers, underscoring the scale of recurring demand for dialysis systems and consumables.

Expansion of organized dialysis networks and capacity build-out

Blood Purification Equipment Market demand benefits from continued expansion and consolidation of dialysis delivery networks, which increases standardization across equipment fleets and consumables sourcing. Multi-site operators typically pursue harmonized protocols to improve clinical consistency, procurement efficiency, and maintenance planning. Equipment replacement cycles are also accelerated by efforts to reduce downtime and improve operational utilization. This driver reinforces demand stability even in mature geographies.

Technology upgrades and workflow standardization

Blood Purification Equipment Market adoption is reinforced by product improvements that enhance clearance efficiency, safety monitoring, usability, and integration with clinical workflows. Facilities invest in upgraded systems to reduce treatment variability, support staff productivity, and improve patient management. Digital connectivity and remote monitoring capabilities increasingly support longitudinal oversight across distributed sites. These upgrades strengthen replacement demand in mature modalities and support gradual penetration of advanced therapy features.

- For instance, Baxter’s Prismaflex and PrisMax systems for continuous renal replacement therapy are designed to support multiple extracorporeal therapies on a single platform and can be integrated with digital data management tools to streamline bedside workflows in intensive care settings.

Increasing use of extracorporeal purification in acute and complex care

Blood Purification Equipment Market growth is additionally supported by broader clinical interest in extracorporeal purification approaches beyond routine ESRD therapy, including acute care applications and toxin or inflammatory mediator removal. Intensive care utilization increases demand for therapies that can be delivered continuously or targeted to specific clinical needs. Hospitals evaluate systems and consumables based on rapid deployment, compatibility with critical care workflows, and therapy flexibility. This driver expands the addressable market value mix by increasing adoption of specialized solutions.

Blood Purification Equipment Market Challenges

Blood Purification Equipment Market expansion faces challenges related to procurement complexity and cost pressures, particularly for systems with high consumables dependency and strict quality requirements. Large providers often negotiate aggressively on recurring supplies, compressing margins and increasing the importance of scale, service coverage, and supply chain resilience. In addition, clinical training and protocol alignment remain significant barriers when facilities introduce new modalities or specialized cartridges, which can slow adoption and lengthen sales cycles.

- For instance, the U.S. FDA placed haemodialysis bloodlines on its medical device shortage list in 2025 after manufacturer B. Braun warned customers it expected to run out of a key bloodline (SL‑2000M2095) by January 20, forcing providers to adjust usage patterns and renegotiate sourcing strategies under tight supply conditions.

Blood Purification Equipment Market participants also face operational risks from supply disruptions in key components and consumables, which can impact therapy continuity and procurement decisions. Facilities increasingly demand redundancy in sourcing, robust inventory planning, and proven manufacturing reliability from vendors. Regulatory and reimbursement variability across regions adds further complexity, creating uneven market access and differences in modality adoption. These factors can limit rapid penetration of newer technologies in cost-sensitive settings.

Blood Purification Equipment Market Trends and Opportunities

Blood Purification Equipment Market trends increasingly reflect a shift toward care models that emphasize flexibility, including greater interest in portable configurations and support infrastructure for distributed delivery. Digital enablement and connected workflows strengthen monitoring and standardization across multi-site networks, improving operational efficiency. These trends create opportunities for vendors that can integrate service support, software capabilities, and workflow design with core equipment offerings. Product strategies that reduce setup complexity and improve ease of use are particularly aligned with provider staffing constraints.

Blood Purification Equipment Market opportunities also expand through therapy diversification, including adsorption, hemoperfusion, and advanced extracorporeal approaches evaluated in critical care settings. Hospitals seek solutions that can be integrated into existing apheresis or renal replacement infrastructure without major workflow disruption. Vendors that can demonstrate clinical utility, operational benefits, and reliable supply for specialized consumables may capture incremental value beyond conventional dialysis. This trend supports a gradual shift toward higher-value therapy portfolios over the forecast period.

- For instance, the HA380 hemoperfusion cartridge from Jafron has been used in combination with continuous veno‑venous hemodiafiltration, where a clinical study reported significant decreases in procalcitonin and interleukin‑6 within 24 hours while using standard CRRT circuits and protocols.

Regional Insights

North America

Blood Purification Equipment Market performance in North America is supported by a large treated patient base, established reimbursement pathways, and dense dialysis provider networks that standardize equipment fleets. North America accounted for 39.3% share in 2025, reflecting high per-patient spend and strong service infrastructure. Procurement in North America emphasizes uptime, service coverage, and predictable consumables supply to support high-throughput delivery models. Technology refresh cycles also remain an important contributor to replacement demand across organized networks.

Europe

Blood Purification Equipment Market demand in Europe is sustained by mature renal care infrastructure, broad treatment access, and strong clinical standardization across public and private delivery channels. Europe represented 26.9% share in 2025, supported by a sizable installed base and steady utilization. Purchasing behavior in Europe frequently prioritizes cost-effectiveness and long-term supply continuity, particularly for membranes and disposables. Adoption of therapy upgrades remains steady, with emphasis on protocol consistency and operational efficiency.

Asia Pacific

Blood Purification Equipment Market growth momentum in Asia Pacific is reinforced by expanding dialysis capacity, growing chronic disease burden, and increasing access to renal replacement therapy in large-population countries. Asia Pacific held 25.1% share in 2025, reflecting large volume potential alongside varied per-patient spending levels. Providers in Asia Pacific increasingly invest in modern equipment fleets and consumables standardization as care delivery scales. The region also shows expanding interest in solutions that can support distributed delivery models and reduce resource intensity.

Latin America

Blood Purification Equipment Market demand in Latin America continues to develop through gradual expansion of treatment capacity and improving access to renal replacement therapy. Latin America represented 5.8% share in 2025, reflecting lower per-patient spending and uneven infrastructure across countries. Procurement often focuses on affordability, dependable consumables supply, and vendor service capabilities in metropolitan treatment hubs. Capacity additions and network development remain central growth levers over the forecast period.

Middle East & Africa

Blood Purification Equipment Market demand in the Middle East & Africa is shaped by access variability, infrastructure constraints, and differing reimbursement environments across countries. Middle East & Africa accounted for 2.9% share in 2025, reflecting a smaller installed base and uneven treatment penetration. Growth is supported by expansion of organized healthcare capacity and increasing chronic disease awareness in select markets. Vendors that can provide reliable service support and stable consumables availability are positioned to strengthen adoption in priority countries.

Competitive Landscape

Blood Purification Equipment Market competition is characterized by installed-base economics, where capital equipment placements drive recurring consumables demand and long-term service relationships. Vendors compete on therapy breadth across chronic and acute settings, clinical performance, operational reliability, and the ability to support multi-site standardization. Differentiation also depends on service footprint, training capabilities, and supply chain resilience for membranes and high-frequency disposables. Competitive intensity is highest in mature dialysis categories, while specialized purification technologies create additional positioning opportunities.

Fresenius Medical Care (Fresenius SE & Co. KGaA) remains a leading participant in the Blood Purification Equipment Market through deep dialysis network alignment, broad equipment portfolios, and scale-driven service capabilities. Fresenius Medical Care strategy typically emphasizes fleet standardization, consumables integration, and operational support to reduce downtime across high-throughput environments. Ongoing product refresh activity supports replacement demand and reinforces long-cycle customer relationships. The approach also strengthens continuity in consumables supply and service coverage, which are key procurement priorities for large providers.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Fresenius Medical Care (Fresenius SE & Co. KGaA)

- Baxter International Inc.

- B. Braun Melsungen AG (B. Braun Avitum)

- Nikkiso Co., Ltd.

- Asahi Kasei Corporation (Asahi Kasei Medical)

- Nipro Corporation (Nipro Pharma)

- Terumo Corporation

- Medtronic (including Bellco)

- Toray Medical Co., Ltd.

- CytoSorbents Corporation (CytoSorbents Europe GmbH)

- ExThera Medical Corporation

- Aethlon Medical, Inc.

- Spectral Medical Inc.

- Cerus Corporation

- Spectra Medical

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In November 2025, Terumo Blood and Cell Technologies and Santersus AG entered into an exclusive partnership to advance NucleoCapture, a novel blood purification technology for critically ill sepsis patients, by combining it with Terumo’s Spectra Optia Apheresis System (announced November 12, 2025).

- In November 2025, Santersus AG also reported that this collaboration is coupled with a Series A financing round led in part by Terumo Ventures, intended to fund pivotal NUC-CAP clinical trials of the NucleoCapture blood purification device across the U.S., UK, and EU.

- In June 2025, Fresenius Medical Care (Fresenius SE & Co. KGaA) reported U.S. FDA 510(k) clearance for an updated 5008X CAREsystem, supporting broader U.S. commercialization and strengthening the product refresh cycle for high-throughput dialysis settings.

- In December 2025, Nikkiso Co., Ltd. announced the launch of the DBB-06 PRO hemodialysis system with full-assist functionality, supporting usability-led differentiation and enabling faster deployment across U.S. dialysis facilities.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 20783.99 million |

| Revenue forecast in 2032 |

USD 31458.4 million |

| Growth rate (CAGR) |

6.1% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Blood Purification Modality (Type) Outlook: Hemodialysis (HD), Peritoneal Dialysis (PD), Continuous Renal Replacement Therapy (CRRT), Intermittent Hemodialysis (IHD), Hemoperfusion, Therapeutic Plasma Exchange (TPE) / Plasmapheresis, Hemofiltration / Filtration, Immunoadsorption / Adsorption; By Portability Outlook: Portable, Non-Portable (Stationary); By Blood Filter / Membrane Material Outlook: Polyarylethersulfone (PAES), Cellulose / Cellulose Acetate, Polyethersulfone (PES), Polysulfone (PSF); By End User Outlook: Hospitals, Dialysis Clinics / Dialysis Centers, Ambulatory Care Centers, Home Use |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Fresenius Medical Care (Fresenius SE & Co. KGaA), Baxter International Inc., B. Braun Melsungen AG (B. Braun Avitum), Nikkiso Co., Ltd., Asahi Kasei Corporation (Asahi Kasei Medical), Nipro Corporation (Nipro Pharma), Terumo Corporation, Medtronic (including Bellco), Toray Medical Co., Ltd., CytoSorbents Corporation (CytoSorbents Europe GmbH), ExThera Medical Corporation, Aethlon Medical, Inc., Spectral Medical Inc., Cerus Corporation, Spectra Medical companies |

| No.of Pages |

332 |

Segmentation

By Blood Purification Modality (Type)

- Hemodialysis (HD)

- Peritoneal Dialysis (PD)

- Continuous Renal Replacement Therapy (CRRT)

- Intermittent Hemodialysis (IHD)

- Hemoperfusion

- Therapeutic Plasma Exchange (TPE) / Plasmapheresis

- Hemofiltration / Filtration

- Immunoadsorption / Adsorption

By Portability

- Portable

- Non-Portable (Stationary)

By Blood Filter / Membrane Material

- Polyarylethersulfone (PAES)

- Cellulose / Cellulose Acetate

- Polyethersulfone (PES)

- Polysulfone (PSF)

By End User

- Hospitals

- Dialysis Clinics / Dialysis Centers

- Ambulatory Care Centers

- Home Use

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa