Blood Testing Market Overview:

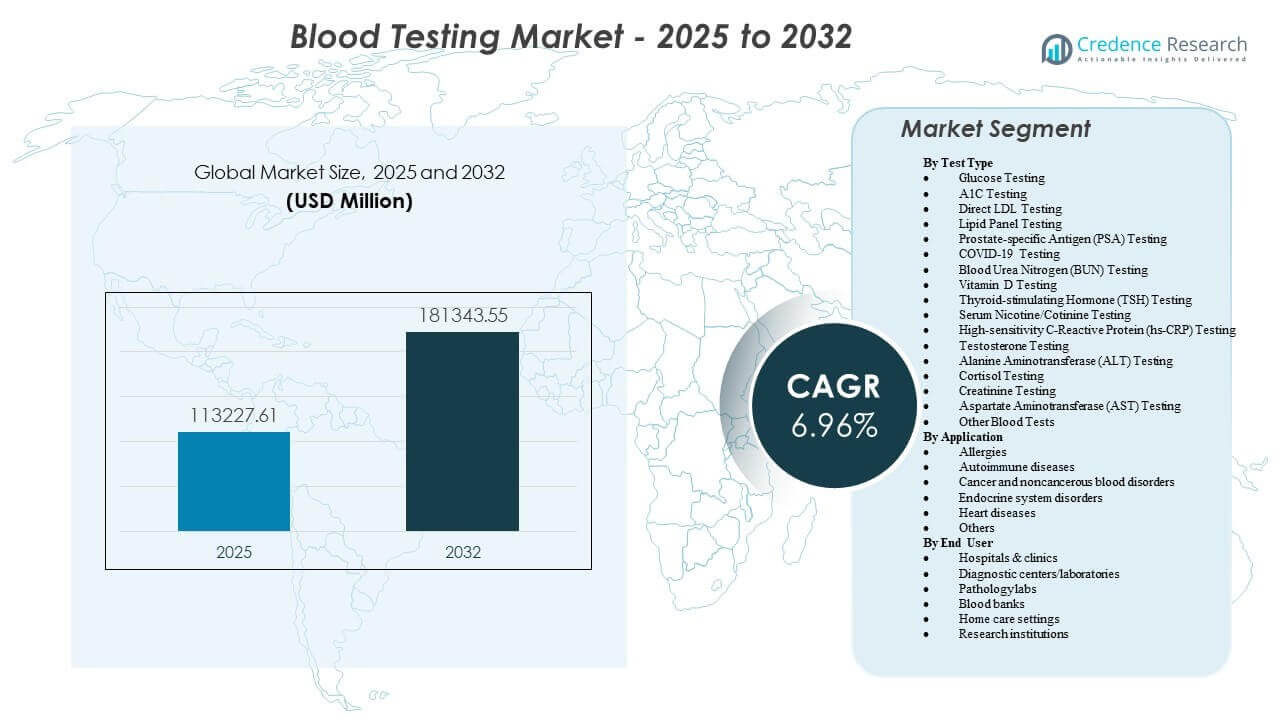

The global Blood Testing Market size was estimated at USD 113,227.61 million in 2025 and is expected to reach USD 181,343.55 million by 2032, growing at a CAGR of 6.96% from 2025 to 2032. Growth is primarily supported by rising volumes of routine screening and chronic disease monitoring, particularly for metabolic and cardiovascular risk management across primary care and outpatient settings. Expanding diagnostic infrastructure and higher test menu availability across hospital networks and independent laboratories continue to reinforce repeat testing demand.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Blood Testing Market Size 2025 |

USD 113,227.61 million |

| Blood Testing Market, CAGR |

6.96% |

| Blood Testing Market Size 2032 |

USD 181,343.55 million |

Key Market Trends & Insights

- North America accounted for 43% of Blood Testing Market revenue in 2025, supported by high routine testing penetration and broad lab network coverage.

- Glucose Testing captured 29.5% share in 2025, reflecting high-frequency monitoring needs linked to diabetes screening and management pathways.

- The Blood Testing Market is projected to expand at a 6.96% CAGR (2025–2032), driven by sustained demand for preventive and longitudinal disease monitoring.

- Blood Testing Market revenue reached USD 113,227.61 million in 2025, indicating a large installed base of testing workflows across hospitals and diagnostic labs.

- Blood Testing Market revenue is expected to reach USD 181,343.55 million by 2032, indicating continued scale-up in testing volumes and assay utilization.

Segment Analysis

Blood testing remains a foundational diagnostic tool across preventive screening, acute care triage, and long-term disease management. Increasing reliance on routine biomarkers for earlier risk identification is supporting steady growth across high-volume assays, while health systems continue to invest in workflow efficiency through automation, consolidation, and standardized testing pathways. Demand is also being reinforced by broader access to diagnostic centers and the expansion of testing menus across mid-sized laboratories.

The Blood Testing Market is also shaped by a shift toward more actionable, clinically integrated results. Providers are increasingly linking testing with treatment decisions and follow-up protocols in endocrinology, cardiology, oncology, and immune-related conditions. At the same time, home-oriented care models and decentralized sample collection are improving convenience, which can increase testing adherence for chronic monitoring use cases.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Test Type Insights

Glucose Testing accounted for the largest share of 29.5% in 2025. Glucose testing leads because diabetes screening and disease management require frequent measurement and repeat testing across primary care, hospitals, and outpatient diagnostics. Routine metabolic panels and pre-procedural testing further sustain consistent demand for glucose-related assays. Wider availability of rapid testing options and standardized clinical pathways also supports sustained utilization.

By Application Insights

Cancer and noncancerous blood disorders, endocrine system disorders, heart diseases, autoimmune diseases, and allergy-related testing collectively support broad demand across both screening and monitoring use cases. Endocrine system disorders remain a high-volume application area due to the recurring nature of monitoring and follow-up testing. Cardiometabolic risk assessment also drives repeat testing through routine panels that include lipid and related markers. Oncology and hematology segments contribute through higher-intensity diagnostic pathways and ongoing therapy monitoring requirements.

By End User Insights

Hospitals & clinics, diagnostic centers/laboratories, and pathology labs remain central demand hubs due to their ability to support broad test menus, faster turnaround requirements, and high throughput operations. Hospitals & clinics typically anchor acute and inpatient testing volumes, while independent diagnostic centers expand access for routine and preventive screening. Pathology labs support specialized workflows and confirmatory testing, particularly where integrated interpretation and standardized quality controls are required. Home care settings are increasingly relevant for patient-centric monitoring models, especially where follow-ups and adherence matter.

Test Menu and Utilization Insights

High-frequency tests continue to drive the bulk of testing volumes, particularly those linked to routine screening programs and chronic monitoring pathways. The Blood Testing Market benefits from repeat testing cycles where follow-up measurement is clinically required to guide treatment or track progression. Increasing provider preference for standardized panels also supports consistent assay utilization across diagnostic centers. Expansion of test availability in mid-tier labs strengthens volume growth beyond top-tier hospital systems.

Workflow and Automation Insights

Laboratories are increasingly prioritizing throughput, turnaround predictability, and operational efficiency, supporting adoption of integrated analyzers and automation-friendly workflows. Consolidation across lab networks can improve utilization of high-capacity systems and standardize test performance across sites. Digital reporting and tighter clinical integration also support higher test ordering consistency through aligned care pathways. These workflow improvements reinforce both testing volumes and service differentiation in the Blood Testing Market.

Blood Testing Market Drivers

Rising chronic disease burden and repeat monitoring demand

The Blood Testing Market is supported by growing testing needs for chronic diseases that require routine monitoring rather than one-time diagnosis. Diabetes, cardiovascular risk conditions, renal function monitoring, and endocrine disorders commonly require repeat testing cycles. Providers often use serial measurements to assess treatment response and guide medication decisions. As healthcare systems emphasize longitudinal management, blood tests remain central to ongoing monitoring and patient follow-up. This recurring testing cadence directly increases test volumes across hospitals, diagnostic centers, and increasingly home-linked care pathways.

- For instance, Abbott’s Afinion point-of-care HbA1c platform delivers glycated hemoglobin results from a 1.5 µL capillary blood sample in about 3 minutes, enabling physicians to perform guideline-compliant, repeat diabetes monitoring during a single visit and reducing the need for follow-up calls and revisits in outpatient settings.

Expansion of preventive screening and early risk detection

Preventive health models continue to increase the frequency of routine testing through annual checkups, risk stratification, and population-level screening. Blood-based markers are widely used to identify early-stage abnormalities before symptoms intensify. This expands demand across broad patient populations, including asymptomatic individuals undergoing routine screening. Screening-led testing also increases downstream confirmatory and follow-up testing volumes. As employer wellness programs and bundled preventive packages expand, routine panels are becoming more standardized and widely adopted.

- For instance, Quest Diagnostics’ employer population health programs conduct annual biometric health screenings for more than 3.5 million employees and support nearly 36,000 on‑site screening events each year, embedding standardized blood panels into large-scale preventive health initiatives.

Growth in diagnostic infrastructure and lab network expansion

The Blood Testing Market benefits from wider access to diagnostic centers, laboratory chains, and improved sample collection coverage. As testing becomes more accessible, utilization typically rises across routine panels and targeted assays. Hospitals and diagnostic networks are also expanding service menus to retain patient pathways and improve service differentiation. These changes strengthen demand across both urban and secondary-care settings. Network expansion also improves turnaround reliability, helping providers shift more monitoring protocols toward evidence-based, repeat testing schedules.

Technology and workflow improvements in laboratories

Laboratory investments in integrated analyzers, automation-friendly processes, and standardized workflows enable higher throughput and predictable turnaround. Improved efficiency can increase overall test capacity and support more consistent adoption of standardized panels. Integration of reporting into clinical workflows can also improve test ordering adherence and follow-up compliance. Collectively, these operational improvements support steady scaling of the Blood Testing Market. In addition, better digitization and quality control reduce re-tests and errors, improving utilization efficiency while maintaining clinical confidence.

Blood Testing Market Challenges

Blood Testing Market growth faces ongoing pressure from cost containment policies and reimbursement scrutiny in many healthcare systems. Pricing pressure can influence test mix, reduce margins for routine assays, and increase competition among diagnostic providers. Operationally, laboratories must maintain high quality standards across large volumes, which can increase compliance and staffing burdens, especially as test menus expand and performance requirements tighten. In response, providers often prioritize high-throughput automation and consolidation, but these investments can raise near-term capital and implementation costs. Frequent reimbursement updates and payer audits can also increase administrative workload and slow adoption of newer, higher-value assays in some markets.

- For instance, Roche’s cobas 6800 molecular platform can process up to 1,344 tests in 24 hours with 8 hours of walk‑away time, illustrating how high-throughput systems help absorb pricing pressure while demanding significant upfront investment in instrumentation, validation, and staff training.

The Blood Testing Market also faces challenges related to variability in access and infrastructure across regions and care settings. Uneven laboratory capacity, limited availability of advanced analyzers in smaller facilities, and differences in quality control practices can affect consistency. Supply chain disruptions for reagents and consumables can impact throughput and turnaround. Data integration and interoperability constraints can also limit seamless clinical adoption in fragmented care networks. Sample logistics and cold-chain limitations in remote areas can further delay results and reduce test reliability for time-sensitive assays. Additionally, fragmented IT systems can create reporting delays, duplicate testing, or gaps in longitudinal patient records, reducing the overall efficiency of care pathways.

Blood Testing Market Trends and Opportunities

The Blood Testing Market is seeing rising interest in blood-based biomarkers that support more actionable clinical decisions across complex diseases. This trend increases demand for high-sensitivity assays and supports broader use of blood tests in differentiated diagnostic pathways. As clinicians seek faster triage and earlier detection, demand may expand for tests that shorten time-to-decision. These dynamics can expand testing volumes in both hospitals and outpatient diagnostics. In parallel, biomarker-driven testing is encouraging labs to broaden assay menus and upgrade analyzers to meet sensitivity and specificity requirements. Over time, wider clinical acceptance and guideline inclusion can further normalize these tests, strengthening recurring utilization across care settings.

Another opportunity is the continued shift toward patient-centric testing pathways that improve convenience and adherence. Expanded decentralized collection, improved logistics, and tighter integration of test reporting into care protocols can support repeat testing compliance. Diagnostic providers that can optimize turnaround predictability and service reliability are likely to strengthen competitiveness. These opportunities support steady expansion of the Blood Testing Market across both routine and specialized testing. Home-linked monitoring and retail-adjacent diagnostics are also increasing access for follow-up testing, especially for chronic conditions that require repeat measurements. As digital reporting and care coordination improve, providers can close gaps in follow-up, increasing the frequency and consistency of recommended testing cycles.

- For instance, Roche has developed its Tina‑quant Lp(a) RxDx assay which received FDA Breakthrough Device Designation in 2024 for use on an installed base of more than 90,000 serum work area systems worldwide, while digital lab-reporting platforms such as NirogGyan report generating over 10 million AI‑enhanced lab reports that reduce diagnostic errors by up to 75%, directly supporting more reliable follow-up and chronic disease monitoring.

Regional Insights

North America

North America held the leading share of 43% in 2025, supported by high utilization of routine screening, strong reimbursement coverage, and dense laboratory networks across hospital and outpatient settings. The region benefits from broad availability of diagnostic services and high adoption of standardized panels in primary care. Integrated provider-lab workflows support steady repeat testing demand across chronic care pathways.

Europe

Europe accounted for 26% in 2025, reflecting established public healthcare infrastructure and consistent preventive screening practices. Demand is supported by standardized diagnostic protocols and wide access to laboratory services in mature healthcare systems. Laboratory modernization and consolidation trends also support stable utilization across routine and specialty testing.

Asia Pacific

Asia Pacific represented 23% in 2025, supported by expanding diagnostics access, rising chronic disease prevalence, and growing uptake of routine screening in urban health systems. Private diagnostic networks are expanding in many markets, improving availability and throughput for routine assays. Increasing healthcare spend and wider test menu penetration are expected to sustain growth momentum.

Latin America

Latin America captured 5% in 2025, supported by expanding private diagnostic chains and rising utilization of routine screening in major urban centers. Testing demand is strengthened by chronic disease management needs and broader outpatient service availability. Continued investment in lab infrastructure is expected to improve access and testing capacity.

Middle East & Africa

The Middle East & Africa held 3% in 2025, reflecting developing laboratory infrastructure and uneven access across care settings. Demand is rising with improving diagnostics coverage, expansion of private healthcare networks, and increasing focus on preventive care. Scaling of lab capacity and standardized quality processes can improve utilization over time.

Competitive Landscape

Competition in the Blood Testing Market is shaped by assay menu breadth, analyzer performance, automation readiness, and service reliability across hospital and diagnostic center customers. Established players focus on installed-base expansion, workflow integration, and portfolio depth across clinical chemistry, immunoassay, hematology, and specialized testing. Diagnostic service providers differentiate through turnaround predictability, network coverage, and the ability to support high-volume routine testing alongside specialty assays. Partnerships, regulatory clearances, and platform upgrades remain common strategies to strengthen positioning.

Hoffmann-La Roche Ltd (Roche Diagnostics) is positioned around broad diagnostic portfolios and scalable analyzer ecosystems that support both routine and advanced testing workflows. Roche Diagnostics continues to emphasize assay pipeline expansion and platform integration to improve laboratory throughput and clinical decision support. The company’s approach typically aligns with high-throughput lab environments where consistency, menu breadth, and reliability are key procurement priorities. This positioning supports competitiveness across hospital labs and large diagnostic networks.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- F. Hoffmann-La Roche Ltd (Roche Diagnostics)

- Abbott Laboratories

- Siemens Healthineers AG

- Danaher Corporation (Beckman Coulter, Radiometer)

- Thermo Fisher Scientific Inc.

- Becton, Dickinson and Company (BD)

- Sysmex Corporation

- Bio-Rad Laboratories Inc.

- bioMérieux SA

- Grifols S.A.

- Quest Diagnostics Incorporated

- Trinity Biotech Plc.

- Waters Corporation

- Shimadzu Corporation

- PerkinElmer, Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In February 2026, SGS announced a partnership with Berlin‑based start‑up theblood to support development and validation of women’s health diagnostics based on menstrual blood, creating a new non‑invasive pathway within the broader blood testing space.

- In October 2025, Sysmex Corporation entered a strategic partnership with QIAGEN N.V. in Japan for exclusive distribution of molecular diagnostic products used for blood‑based infectious disease and oncology screening, strengthening Sysmex’s advanced blood screening portfolio.

- In March 2025, Polaris DX launched the Igloo Pro device, a point‑of‑care blood testing platform that provides rapid, lab‑quality results for markers such as vitamin D, ferritin, and C‑reactive protein using single‑use capillary assays at dental and other outpatient settings.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 113,227.61 million |

| Revenue forecast in 2032 |

USD 181,343.55 million |

| Growth rate (CAGR) |

6.96% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Test Type Outlook: Glucose Testing, A1C Testing, Direct LDL Testing, Lipid Panel Testing, Prostate-specific Antigen (PSA) Testing, COVID-19 Testing, Blood Urea Nitrogen (BUN) Testing, Vitamin D Testing, Thyroid-stimulating Hormone (TSH) Testing, Serum Nicotine/Cotinine Testing, High-sensitivity C-Reactive Protein (hs-CRP) Testing, Testosterone Testing, Alanine Aminotransferase (ALT) Testing, Cortisol Testing, Creatinine Testing, Aspartate Aminotransferase (AST) Testing, Other Blood Tests; By Application Outlook: Allergies, Autoimmune diseases, Cancer and noncancerous blood disorders, Endocrine system disorders, Heart diseases, Others; By End User Outlook: Hospitals & clinics, Diagnostic centers/laboratories, Pathology labs, Blood banks, Home care settings, Research institutions |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

F. Hoffmann-La Roche Ltd (Roche Diagnostics), Abbott Laboratories, Siemens Healthineers AG, Danaher Corporation (Beckman Coulter, Radiometer), Thermo Fisher Scientific Inc., Becton, Dickinson and Company (BD), Sysmex Corporation, Bio-Rad Laboratories Inc., bioMérieux SA, Grifols S.A., Quest Diagnostics Incorporated, Trinity Biotech Plc., Waters Corporation, Shimadzu Corporation, PerkinElmer, Inc. |

| No. of Pages |

340 |

Segmentation

By Test Type

- Glucose Testing

- A1C Testing

- Direct LDL Testing

- Lipid Panel Testing

- Prostate-specific Antigen (PSA) Testing

- COVID-19 Testing

- Blood Urea Nitrogen (BUN) Testing

- Vitamin D Testing

- Thyroid-stimulating Hormone (TSH) Testing

- Serum Nicotine/Cotinine Testing

- High-sensitivity C-Reactive Protein (hs-CRP) Testing

- Testosterone Testing

- Alanine Aminotransferase (ALT) Testing

- Cortisol Testing

- Creatinine Testing

- Aspartate Aminotransferase (AST) Testing

- Other Blood Tests

By Application

- Allergies

- Autoimmune diseases

- Cancer and noncancerous blood disorders

- Endocrine system disorders

- Heart diseases

- Others

By End User

- Hospitals & clinics

- Diagnostic centers/laboratories

- Pathology labs

- Blood banks

- Home care settings

- Research institutions

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa