Body Temperature Monitoring Market Overview:

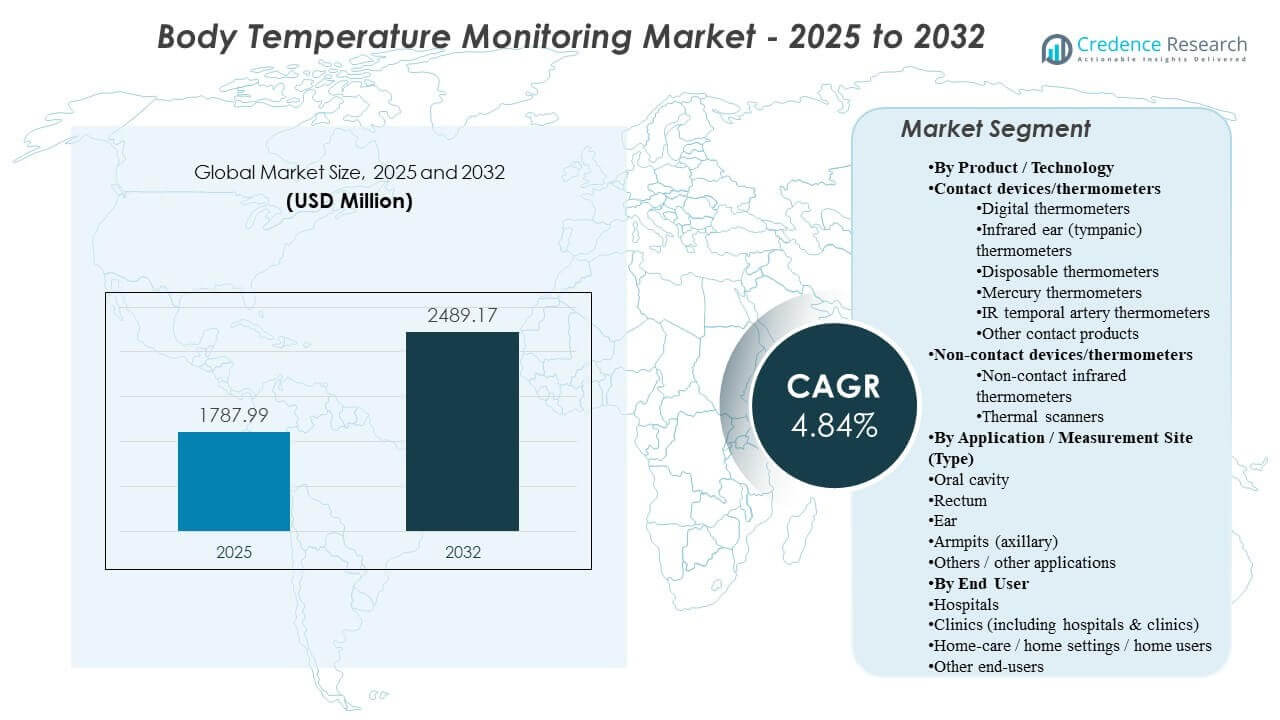

The global Body Temperature Monitoring Market size was estimated at USD 1787.99 million in 2025 and is expected to reach USD 2489.17 million by 2032, growing at a CAGR of 4.84% from 2025 to 2032. Rising reliance on rapid vital-sign checks across hospitals, outpatient settings, and home-care environments is strengthening demand for accurate, easy-to-use temperature monitoring devices. Growing adoption of connected monitoring workflows and routine fever screening across broader care pathways continues to support sustained market expansion.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Body Temperature Monitoring Market Size 2025 |

USD 1787.99 million |

| Body Temperature Monitoring Market, CAGR |

4.84% |

| Body Temperature Monitoring Market Size 2032 |

USD 2489.17 million |

Key Market Trends & Insights

- The market is projected to expand from USD 1787.99million (2025) to USD 2489.17 million (2032) at a 4.84% CAGR (2025–2032).

- Contact devices/thermometers accounted for the largest share of 60.9% in 2025, supported by established clinical workflows and repeatable measurement practices.

- Hospitals represented 55.6% in 2025, reflecting high utilization rates in inpatient monitoring, emergency care, and routine clinical assessments.

- North America held 31.8% in 2025, driven by high device penetration in hospitals and strong replacement demand for digital and IR-based devices.

- Asia Pacific captured 29.1% in 2025, supported by expanding access to primary care, higher patient throughput, and growing home-monitoring adoption.

Segment Analysis

Product and technology choices in body temperature monitoring are shaped by the trade-off between clinical accuracy, measurement speed, and workflow convenience. Contact thermometers remain widely used in hospitals and clinics due to familiar protocols, repeatable readings, and suitability for ongoing monitoring, particularly in inpatient and emergency contexts. Non-contact thermometers and thermal scanners are increasingly used where fast throughput and hygiene considerations matter, such as screening scenarios and high-traffic care environments, although measurement confidence and user technique can influence adoption.

Measurement-site preferences vary by patient age, setting, and required speed of assessment. Oral temperature measurement remains common for routine checks, especially in general care and household use, due to ease of use and familiarity. Ear and temporal approaches support quicker checks with minimal disturbance, helping adoption in pediatric, outpatient, and repeated screening contexts. End-user demand is anchored by hospital volume, but home-care growth is reinforced by self-monitoring behavior and broader care delivery outside traditional facilities.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Product / Technology Insights

Contact devices/thermometers accounted for the largest share of 60.9% in 2025. Clinical users rely on contact-based methods for consistent readings and compatibility with standard vital-sign protocols, particularly in inpatient monitoring and acute care. Product replacement cycles also support steady upgrades from legacy formats toward digital and mercury-free designs. Non-contact devices continue expanding in settings prioritizing faster checks and infection control, supported by convenience and workflow speed.

By Application / Measurement Site (Type) Insights

Oral cavity accounted for the largest share of 26.9% in 2025. Oral measurement remains a common choice for routine checks because the method is familiar, accessible, and easy to perform across clinical and home settings. Measurement-site selection is also influenced by patient age and comfort, making axillary measurements relevant in home and pediatric contexts. Ear and temporal checks are increasingly used when rapid assessment and minimal patient disturbance are priorities.

By End User Insights

Hospitals accounted for the largest share of 55.6% in 2025. High patient throughput and frequent vital-sign monitoring requirements sustain strong hospital demand across wards, emergency departments, and perioperative settings. Hospitals also adopt multiple device types to match varied workflows, from bedside monitoring to rapid screening. Home-care demand continues to grow as self-monitoring becomes routine for fever tracking, post-acute recovery, and caregiver-led monitoring at home.

Body Temperature Monitoring Market Drivers

Expanding routine vital-sign monitoring across care settings

Routine temperature checks remain a baseline clinical requirement across inpatient, outpatient, and emergency care. Increasing patient volumes and faster clinical throughput raise the frequency of measurement events per day. Standardized triage processes strengthen the need for reliable, repeatable device performance. This dynamic supports sustained replacement demand as healthcare providers refresh device fleets and standardize workflows.

- For instance, Welch Allyn’s SureTemp Plus 690 specifies ~4-second oral readings and ~10–15-second axillary/rectal readings (depending on patient/site), with calibration accuracy listed as ±0.2°F (±0.1°C) in monitor mode and battery life of ~6,000 temperature measurements, which aligns to high-utilization, repeatable workflows in busy care settings.

Growth in home monitoring and self-care behavior

Home-care temperature monitoring is expanding as consumers increasingly track symptoms and manage minor illness episodes outside hospitals. Caregiver-led monitoring for children and older adults adds to household device penetration. Telehealth and remote guidance models reinforce at-home measurements as part of symptom assessment and care escalation decisions. This broadens the addressable market beyond facility-based procurement.

- For instance, iHealth’s PT3 no-touch infrared thermometer is specified to deliver a reading in ~1 second and uses an IR sensor that collects 100+ data points per second, while its companion app supports tracking up to 99 readings and up to 5 users, which is designed for repeated, multi-user household monitoring.

Preference shift toward faster, low-contact measurement workflows

Demand is rising for faster measurement methods that reduce disruption during repeated checks, especially in pediatric and high-throughput environments. Non-contact infrared solutions and temporal approaches support quick assessments and perceived hygiene advantages. Screening needs in crowded settings also encourage rapid-check devices where throughput matters. This increases the mix of technologies adopted across different clinical and non-clinical environments.

Ongoing product upgrades, digitalization, and device standardization

Digital thermometers and infrared-based devices continue replacing older formats as organizations pursue standardization and usability improvements. Device makers improve ergonomics, readability, and measurement speed, helping reduce user error and improve compliance. Connected features and app-based support are increasingly used in consumer-facing products, reinforcing engagement and repeat usage. These enhancements collectively contribute to higher unit value and broader adoption.

Body Temperature Monitoring Market Challenges

Accuracy perception and measurement variability remain key adoption barriers, particularly for non-contact approaches that are sensitive to user technique and environmental conditions. Differences across measurement sites can also create confusion in home settings when users switch between oral, ear, and axillary methods. Procurement decisions in hospitals may prioritize proven reliability, limiting rapid conversion to newer formats unless strong performance evidence exists. Regulatory expectations and institutional protocols further influence purchasing cycles and slow technology transitions.

- For instance, Hillrom/Welch Allyn’s Braun ThermoScan PRO 6000 ear thermometer is specified at ±0.2 °C accuracy over 35.0–42.0 °C and a 2–3 second measurement time, giving clinical buyers concrete performance specs to standardize against during evaluation and training.

Pricing pressure and competition across commoditized digital thermometers can compress margins, particularly in high-volume retail and public procurement channels. Hospitals and clinics often standardize on a limited set of devices to simplify training and reduce variability, which can limit entry opportunities for newer products. Supply chain consistency and component availability can affect lead times, especially during demand spikes. In some markets, market fragmentation and distribution complexity also make it harder to scale consistently.

Body Temperature Monitoring Market Trends and Opportunities

Connected and app-enabled thermometry is expanding in consumer segments, supporting guided symptom tracking and longitudinal monitoring. This trend creates opportunities for differentiated value beyond a single reading, especially where users want trend visibility and household-level tracking. Integration with broader remote monitoring ecosystems can strengthen repeat usage and increase device stickiness. These capabilities can also support data-driven population health insights where applicable.

Opportunities are growing in healthcare standardization programs that seek consistent device performance across multiple sites of care. Multi-site provider networks may prefer standardized device families to streamline training and reduce workflow variability. In parallel, growth in outpatient care and ambulatory settings supports demand for portable, easy-to-sanitize devices. Emerging market expansion, rising healthcare access, and broader retail distribution can further lift unit volumes across both clinical and consumer channels.

- For instance, Withings’ FDA 510(k) summary for BeamO reports a thermometer clinical accuracy study with 106 subjects and quantified metrics including clinical bias of −0.074°F, limits of agreement of ±1.023°F, and repeatability of 0.29°F—data that multi-site programs can use when assessing consistency.

Regional Insights

North America

North America accounted for 31.8% in 2025, supported by strong device penetration across hospitals and outpatient facilities. Replacement demand remains consistent as providers refresh fleets and standardize measurement protocols. Home-use adoption also supports volume through retail and online channels. Preference for digital and infrared formats continues to shape product mix across clinical and household settings.

Europe

Europe held 22.6% in 2025, driven by established healthcare infrastructure and routine monitoring protocols across hospitals and primary care. Procurement policies often favor standardized products with consistent performance and ease of training. Demand is supported by ongoing replacement cycles and adoption of mercury-free solutions. Home-care growth adds incremental demand as self-monitoring becomes more common.

Asia Pacific

Asia Pacific represented 29.1% in 2025, supported by expanding healthcare access and higher patient throughput in urban centers. Increased uptake of home monitoring and broader availability through retail and e-commerce channels contribute to growth. Public health preparedness and higher screening activity in crowded environments support non-contact adoption in specific use cases. Product mix remains diverse, spanning cost-effective digital devices to higher-end infrared formats.

Latin America

Latin America accounted for 10.4% in 2025, with demand driven by hospital procurement, private clinic growth, and rising household device ownership. Budget constraints can influence purchasing decisions, supporting a strong market for value-oriented digital thermometers. Expansion of outpatient services and improving access to basic diagnostics also contributes. Distribution breadth and local availability remain important factors shaping adoption.

Middle East & Africa

Middle East & Africa held 6.1% in 2025, supported by investments in healthcare infrastructure in select countries and steady demand from hospitals and clinics. Screening needs in high-traffic public settings can support uptake of infrared and non-contact formats in targeted applications. Market growth is also supported by increasing awareness of home monitoring in urban areas. Procurement cycles and distribution reach can influence adoption speed across subregions.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Competitive Landscape

The Body Temperature Monitoring Market is moderately fragmented, combining diversified healthcare companies with focused device manufacturers. Competitive differentiation is shaped by measurement accuracy, device speed, usability, and product reliability across varied settings. Companies compete through product refresh cycles, clinical channel partnerships, retail distribution, and brand trust in both professional and consumer segments. Portfolio breadth across vital-sign monitoring and adjacent care categories supports bundling and institutional procurement strategies.

Koninklijke Philips N.V. benefits from a broad healthcare technology footprint that supports adoption across clinical workflows and adjacent monitoring ecosystems. Product positioning often emphasizes clinical reliability, workflow compatibility, and ease of use in professional settings. The company’s scale and distribution reach support multi-country commercialization and institutional procurement. Continued focus on integrated care pathways can support cross-selling opportunities where temperature monitoring is part of broader vital-sign measurement.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Koninklijke Philips N.V.

- Omron Corporation

- Becton, Dickinson and Company

- Baxter International

- Cardinal Health

- Terumo Corporation

- Microlife Corporation

- Exergen Corporation

- A&D Medical

- Kinsa Health, LLC

- iHealth Labs Inc.

- American Diagnostic Corp.

- Hartmann Group

- Helen of Troy Limited

- Citizen Systems Japan Co., Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments

- In Feb 2026, Tevogen Bio Holdings Inc. announced that it entered into a signed, non-exclusive, non-binding letter of intent to evaluate a potential transaction with Sciometrix Inc., a healthcare technology and value-based care solutions provider that develops the Clinicus digital care management platform.

- In March 2024, Kinsa Health, LLC was acquired as part of an expansion in AI-driven illness forecasting and smart-thermometer ecosystem capabilities. The development reflects continued interest in pairing connected thermometry with analytics-led differentiation.

- In July 2024, Exergen Corporation expanded availability for temporal artery thermometer offerings through a regulatory clearance to launch product lines in a Latin American market. The move supports geographic expansion and strengthens regional distribution reach for infrared temporal devices.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 1,787.99 million |

| Revenue forecast in 2032 |

USD 2,489.17 million |

| Growth rate (CAGR) |

4.84% |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Product / Technology Outlook: Contact devices/thermometers (Digital thermometers, Infrared ear (tympanic) thermometers, Disposable thermometers, Mercury thermometers, IR temporal artery thermometers, Other contact products); Non-contact devices/thermometers (Non-contact infrared thermometers, Thermal scanners); By Application / Measurement Site (Type) Outlook: Oral cavity, Rectum, Ear, Armpits (axillary), Others / other applications; By End User Outlook: Hospitals, Clinics (including hospitals & clinics), Home-care / home settings / home users, Other end-users |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Koninklijke Philips N.V.; Omron Corporation; Becton, Dickinson and Company; Baxter International; Cardinal Health; Terumo Corporation; Microlife Corporation; Exergen Corporation; A&D Medical; Kinsa Health, LLC; iHealth Labs Inc.; American Diagnostic Corp.; Hartmann Group; Helen of Troy Limited; Citizen Systems Japan Co., Ltd. |

| No. of Pages |

330 |

Segmentation

BY PRODUCT / TECHNOLOGY

- Contact devices/thermometers

- Digital thermometers

- Infrared ear (tympanic) thermometers

- Disposable thermometers

- Mercury thermometers

- IR temporal artery thermometers

- Other contact products

- Non-contact devices/thermometers

- Non-contact infrared thermometers

- Thermal scanners

BY APPLICATION / MEASUREMENT SITE (TYPE)

- Oral cavity

- Rectum

- Ear

- Armpits (axillary)

- Others / other applications

BY END USER

- Hospitals

- Clinics (including hospitals & clinics)

- Home-care / home settings / home users

- Other end-users

BY REGION

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa