Breast Cancer Screening Tests Market Overview:

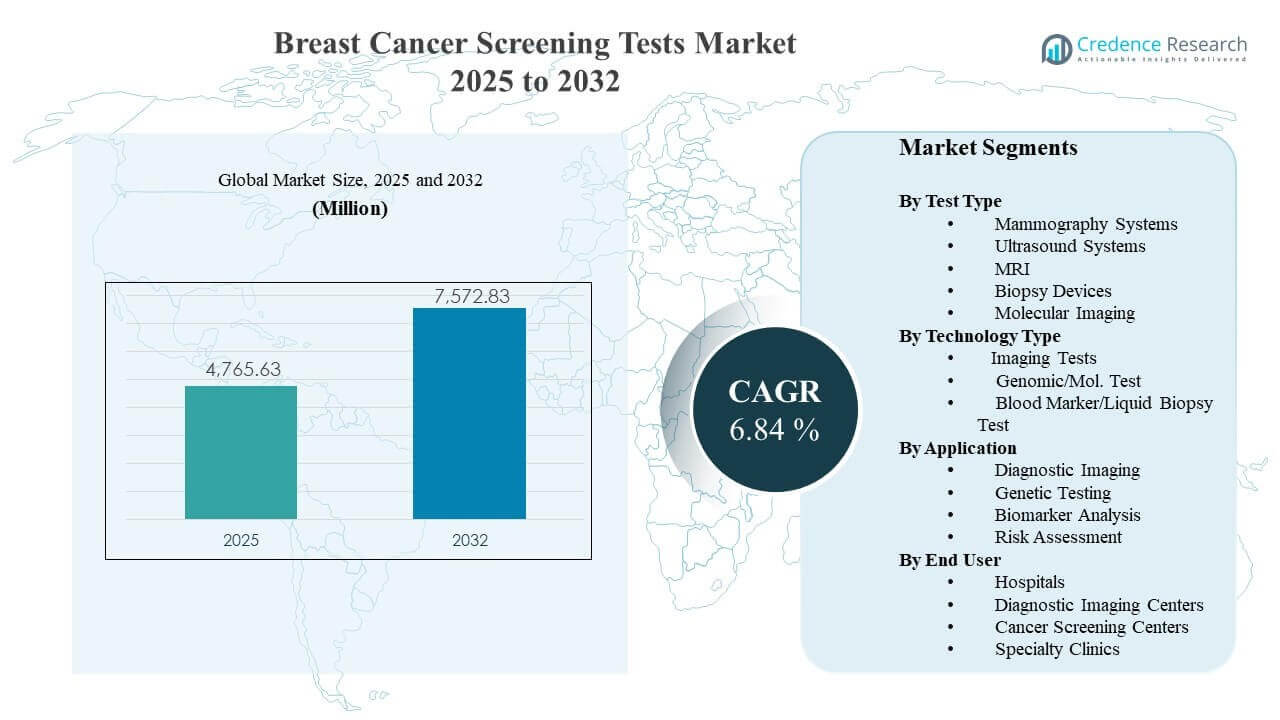

The global Breast Cancer Screening Tests Market size was estimated at USD 4765.63 million in 2025 and is expected to reach USD 7572.83 million by 2032, growing at a CAGR of 6.84% from 2025 to 2032. Growth is primarily supported by rising screening participation and protocol-driven early detection pathways that expand routine testing volumes across hospital networks and outpatient imaging settings. North America remains a major demand center due to established screening infrastructure, with steady expansion also supported by improving access and program scale-up across parts of Asia Pacific.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Breast Cancer Screening Tests Market Size 2025 |

USD 4765.63 million |

| Breast Cancer Screening Tests Market, CAGR |

6.84% |

| Breast Cancer Screening Tests Market Size 2032 |

USD 7572.83 million |

Key Market Trends & Insights

- The Breast Cancer Screening Tests Market reached USD 4765.63 million in 2025, reflecting sustained demand for population screening and diagnostic workups.

- The Breast Cancer Screening Tests Market is projected to total USD 7572.83 million by 2032, supported by expanding screening capacity and improved pathway adherence.

- The Breast Cancer Screening Tests Market is expected to grow at 6.84% CAGR during 2025–2032, indicating steady mid-single-digit expansion across modalities.

- Imaging Tests accounted for the largest share of 51.6% in 2023, supported by guideline alignment and established reimbursement pathways in screening programs.

- Hospitals accounted for the largest share of 39.2% in 2025, driven by integrated imaging-to-biopsy workflows and centralized diagnostic coordination.

Segment Analysis

Breast Cancer Screening Tests Market demand remains anchored in imaging-led pathways that connect screening participation to actionable clinical decisions such as recall imaging, biopsy referral, and follow-up monitoring. Technology upgrades in mammography and ultrasound systems, combined with workflow improvements in interpretation and scheduling, are strengthening screening throughput and consistency. Risk stratification practices are also expanding, encouraging broader use of supplemental imaging and targeted testing in high-risk populations.

Molecular and blood-based testing approaches are gaining attention as programs aim to improve early detection and refine risk assessment beyond anatomy-only evaluation. Genetic testing and biomarker workflows are increasingly integrated into specialty clinic pathways for hereditary risk and personalized monitoring strategies. These shifts support a more layered screening ecosystem where imaging remains first-line for broad populations and molecular tools expand depth for specific cohorts.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Test Type Insights

Mammography Systems continue to represent the backbone of organized breast screening pathways due to established clinical protocols and scalable throughput in routine screening settings. Ultrasound Systems and MRI support supplemental evaluation for dense breast populations and high-risk monitoring, improving sensitivity in specific cohorts. Biopsy Devices remain essential for confirmatory diagnosis following suspicious findings, sustaining procedure-linked demand. Molecular Imaging supports targeted assessment where functional or metabolic characterization is clinically required.

By Technology Type Insights

Imaging Tests accounted for the largest share of 51.6% in 2023. Imaging Tests lead because population screening programs and care pathways rely on standardized acquisition and interpretation routines supported by mature installed bases. Imaging Tests also benefit from continuous platform upgrades that improve workflow efficiency and diagnostic confidence across large screening volumes. Imaging Tests remain central because imaging outputs directly guide next-step clinical decisions such as recall, targeted imaging, and biopsy referral.

By Application Insights

Diagnostic Imaging remains the most widely utilized application because screening programs depend on imaging workflows to identify actionable findings and trigger standardized follow-up. Genetic Testing adoption is expanding in high-risk and hereditary pathways as risk identification becomes more integrated into screening decisions. Biomarker Analysis is gaining relevance for detection and monitoring use-cases, supporting additional decision support beyond anatomical assessment. Risk Assessment is rising in importance as screening becomes more stratified by age, density, family history, and clinical risk profiles.

By End User Insights

Hospitals accounted for the largest share of 39.2% in 2025. Hospitals lead because hospitals combine imaging, interventional biopsy capability, pathology coordination, and oncology referral pathways within integrated care settings. Hospitals also tend to adopt advanced screening modalities earlier, supporting higher complexity workups and faster escalation from screening to diagnosis. Hospitals benefit from centralized scheduling, multidisciplinary governance, and programmatic screening initiatives that increase testing volumes across affiliated sites.

Market Drivers

Expanding screening participation and pathway standardization

Breast Cancer Screening Tests Market growth is supported by broader screening uptake and increasing use of standardized clinical pathways that move patients from screening to diagnostic confirmation more efficiently. Protocol-driven workflows reduce delays in recall imaging and biopsy referral, improving throughput across facilities. Provider networks are also expanding structured screening programs that improve adherence and repeat screening frequency. These factors raise demand across imaging, confirmatory procedures, and complementary testing workflows.

Technology upgrades improving detection confidence and workflow efficiency

Breast Cancer Screening Tests Market demand benefits from ongoing equipment upgrades across mammography, ultrasound, and MRI platforms that improve image quality and operational performance. Workflow enhancements reduce repeat scans, improve scheduling utilization, and strengthen consistency across sites. Improved acquisition and interpretation capabilities also support broader deployment across outpatient and network settings. These improvements increase replacement demand alongside incremental procedure volume growth.

- For instance, Hologic’s Selenia Dimensions 3D mammography system has been shown to detect on average 41% more invasive breast cancers and reduce callbacks by up to 40% versus 2D mammography alone, while Siemens Healthineers’ Mammomat Revelation platform enables HD breast biopsy targeting with approximately ±1 mm accuracy and integrated specimen imaging within about 20 seconds, thereby shortening compression time and eliminating the need for a second imaging system in many workflows.

Increasing use of risk-stratified screening and supplemental testing

Breast Cancer Screening Tests Market expansion is reinforced by the shift toward risk-based screening approaches that tailor modalities and follow-up intensity to patient profiles. Dense breast protocols and high-risk surveillance encourage additional ultrasound and MRI utilization beyond baseline screening. Genetic testing supports identification of hereditary risk populations, improving targeted screening intensity. These factors expand testing breadth and encourage multi-modality pathways for prioritized cohorts.

- For instance, supplemental ultrasound in women with dense breasts detects about 4.4 additional cancers per 1,000 exams beyond mammography, and supplemental MRI detects roughly 3.5–28.6 additional cancers per 1,000 exams with recall rates of 12–24%, while a pooled analysis of over 130,000 women with dense breasts showed MRI providing an incremental cancer detection rate of approximately 1.5 additional cancers per 1,000 screenings over other supplemental modalities, supporting modality selection based on risk and density.

Growth in integrated care models and diagnostic coordination

Breast Cancer Screening Tests Market demand rises as care delivery models emphasize integrated screening-to-diagnosis coordination across hospitals, imaging centers, and specialty clinics. Integrated referral systems improve follow-up completion rates and reduce patient drop-off after abnormal screening results. Multidisciplinary coordination also supports faster confirmatory workups and improved case management. These operational shifts translate into more consistent test utilization across connected provider ecosystems.

Market Challenges

Breast Cancer Screening Tests Market expansion faces operational and access constraints linked to imaging capacity, workforce availability, and variability in screening infrastructure across regions. Equipment costs, service requirements, and facility readiness can slow adoption of advanced modalities in lower-resource settings. Interpretation workloads and staffing variability also create bottlenecks that affect appointment availability and follow-up completion. These constraints can limit screening throughput even when demand signals remain strong.

- For instance, in the U.S. there are only about four dedicated breast imaging radiologists per 100,000 women aged 40 years and older, highlighting how workforce scarcity directly constrains screening capacity and access even as demand grows. Equipment costs, service requirements, and facility readiness can slow adoption of advanced modalities in lower-resource settings.

Breast Cancer Screening Tests Market adoption is also influenced by differences in reimbursement policies, guideline variability, and patient adherence challenges across geographies. Screening participation can be uneven due to awareness gaps, fear of procedures, and logistical barriers such as travel time and appointment availability. False positives and follow-up burden can affect patient experience and program efficiency. Data integration limitations across sites can further hinder coordinated recall tracking and population screening management.

Market Trends and Opportunities

Breast Cancer Screening Tests Market trends reflect increasing focus on workflow modernization and standardized quality management across imaging and diagnostic pathways. Screening programs are investing in improved scheduling, protocol adherence tracking, and integrated reporting to reduce recall delays and incomplete follow-up. Imaging platform upgrades continue to support higher throughput and more consistent interpretation across multi-site networks. These initiatives improve utilization and support consistent screening participation outcomes.

- For instance, RadNet’s DeepHealth Breast Suite now supports AI-enabled workflows on more than 10 million mammograms annually and has demonstrated a 21.6% increase in cancer detection rate with a 15% rise in positive predictive value while keeping recall rates within American College of Radiology guidelines, highlighting how integrated AI plus workflow tools can modernize reporting, prioritization, and interpretation at scale.

Breast Cancer Screening Tests Market opportunities are emerging around multi-modality pathways that combine imaging with molecular and blood-based approaches for improved risk assessment and early detection strategies. Genetic testing integration into screening decisions is expanding in high-risk populations, supporting personalized surveillance intensity. Biomarker and blood-based testing innovation supports new pathway designs for adjunct detection and monitoring. These opportunities expand the addressable testing mix beyond imaging-only pathways while maintaining imaging as a foundational modality.

Regional Insights

North America

Breast Cancer Screening Tests Market revenue share in North America was 44.2% in 2025. North America benefits from established screening infrastructure, broad diagnostic capacity, and strong integration across hospital networks and outpatient imaging centers. Mature reimbursement environments and high clinical awareness support regular screening participation and timely follow-up. Technology upgrades and multi-site program management further strengthen sustained screening volumes.

Europe

Breast Cancer Screening Tests Market revenue share in Europe was 23.6% in 2025. Europe demand is supported by organized screening programs and strong public health emphasis on early detection across many countries. High installed imaging capacity and standardized pathways support stable utilization across screening and diagnostic workups. Continued modernization of imaging systems and expansion of risk-stratified approaches support incremental growth.

Asia Pacific

Breast Cancer Screening Tests Market revenue share in Asia Pacific was 22.4% in 2025. Asia Pacific growth is supported by improving access to diagnostic infrastructure, rising awareness, and expansion of screening programs in major urban centers. Provider networks are increasing capacity and adopting standardized screening pathways, supporting higher screening participation. Variability across countries remains, but large population bases and expanding healthcare investment support long-term demand.

Latin America

Breast Cancer Screening Tests Market revenue share in Latin America was 6.3% in 2025. Latin America demand is driven by gradual expansion of imaging access and screening initiatives concentrated in higher-resource urban areas. Private providers and hospital systems often lead adoption of advanced screening modalities. Infrastructure constraints and uneven coverage continue to shape utilization patterns across countries.

Middle East & Africa

Breast Cancer Screening Tests Market revenue share in Middle East & Africa was 3.5% in 2025. Middle East & Africa growth is supported by expanding diagnostic capacity in selected markets and increasing awareness initiatives for early detection. Demand is often concentrated in major cities and higher-resource health systems, supporting localized adoption. Infrastructure variability and access constraints remain key factors influencing overall regional share.

Competitive Landscape

Breast Cancer Screening Tests Market competition is shaped by imaging platform upgrades, workflow differentiation, and expansion of modality portfolios across screening and diagnostic settings. Market participants compete on image quality, throughput, service coverage, and integration with clinical workflows that reduce follow-up delays. Portfolio breadth across mammography, ultrasound, MRI, and biopsy support influences purchasing decisions for integrated provider networks. Partnerships and product enhancements that improve screening efficiency and pathway coordination continue to drive differentiation.

Hologic, Inc. maintains a strong position through mammography platform focus and continuous enhancement of screening room workflows and diagnostic follow-up pathways. Product strategy emphasizes imaging performance improvements, workflow integration, and broad deployment suitability across hospital and outpatient settings. Ongoing enhancements support adoption in high-throughput screening environments where operational efficiency and consistent interpretation are critical. Commercial positioning also benefits from long-standing relationships with screening programs and imaging providers.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Hologic, Inc.

- Siemens Healthineers AG

- GE HealthCare Technologies Inc.

- Koninklijke Philips N.V.

- FUJIFILM Holdings Corporation

- Canon Medical Systems Corporation

- Samsung Medison Co., Ltd.

- Mindray Medical International Limited

- Exact Sciences Corporation

- Guardant Health, Inc.

- Natera, Inc.

- Biocept, Inc.

- F. Hoffmann-La Roche Ltd

- Myriad Genetics, Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In March 2026, Guardant Health announced the launch of its Shield multi‑cancer detection (MCD) laboratory-developed blood test in multiple Asian markets, with the methylation-based assay designed to detect several cancers including breast cancer in average‑risk individuals aged 45 years and older.

- In March 2026, findings from the GEMINI study in the United Kingdom demonstrated that integrating the Mia v3 artificial intelligence system into breast cancer screening workflows increased cancer detection by 10.4% while simultaneously reducing radiology workload by up to 31% and shortening notification times for detected cancers.

- In December 2025, Astrin Biosciences introduced Certitude Breast, a first-of-its-kind, non-imaging, blood-based early breast cancer detection test, with study data showing 92% sensitivity and 93% specificity and commercial availability planned in the United States from early 2026.

- In October 2025, PrecisionRNA Biotech Pvt Ltd (Prerna), based in Hyderabad, launched CANTEL, a microRNA-based qualitative in‑vitro blood test aimed at improving early-stage breast cancer screening in India by providing a convenient and accurate alternative to traditional imaging methods.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 4765.63 million |

| Revenue forecast in 2032 |

USD 7572.83 million |

| Growth rate (CAGR) |

6.84% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Test Type; By Technology Type; By Application; By End User |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Hologic, Inc.; Siemens Healthineers AG; GE HealthCare Technologies Inc.; Koninklijke Philips N.V.; FUJIFILM Holdings Corporation; Canon Medical Systems Corporation; Samsung Medison Co., Ltd.; Mindray Medical International Limited; Exact Sciences Corporation; Guardant Health, Inc.; Natera, Inc.; Biocept, Inc.; F. Hoffmann-La Roche Ltd; Myriad Genetics, Inc. |

| No.of Pages |

332 |

Segmentation

By Test Type

- Mammography Systems

- Ultrasound Systems

- MRI

- Biopsy Devices

- Molecular Imaging

By Technology Type

- Imaging Tests

- Genomic/Mol. Test

- Blood Marker/Liquid Biopsy Test

By Application

- Diagnostic Imaging

- Genetic Testing

- Biomarker Analysis

- Risk Assessment

By End User

- Hospitals

- Diagnostic Imaging Centers

- Cancer Screening Centers

- Specialty Clinics

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa