Breast Ultrasound Market Overview:

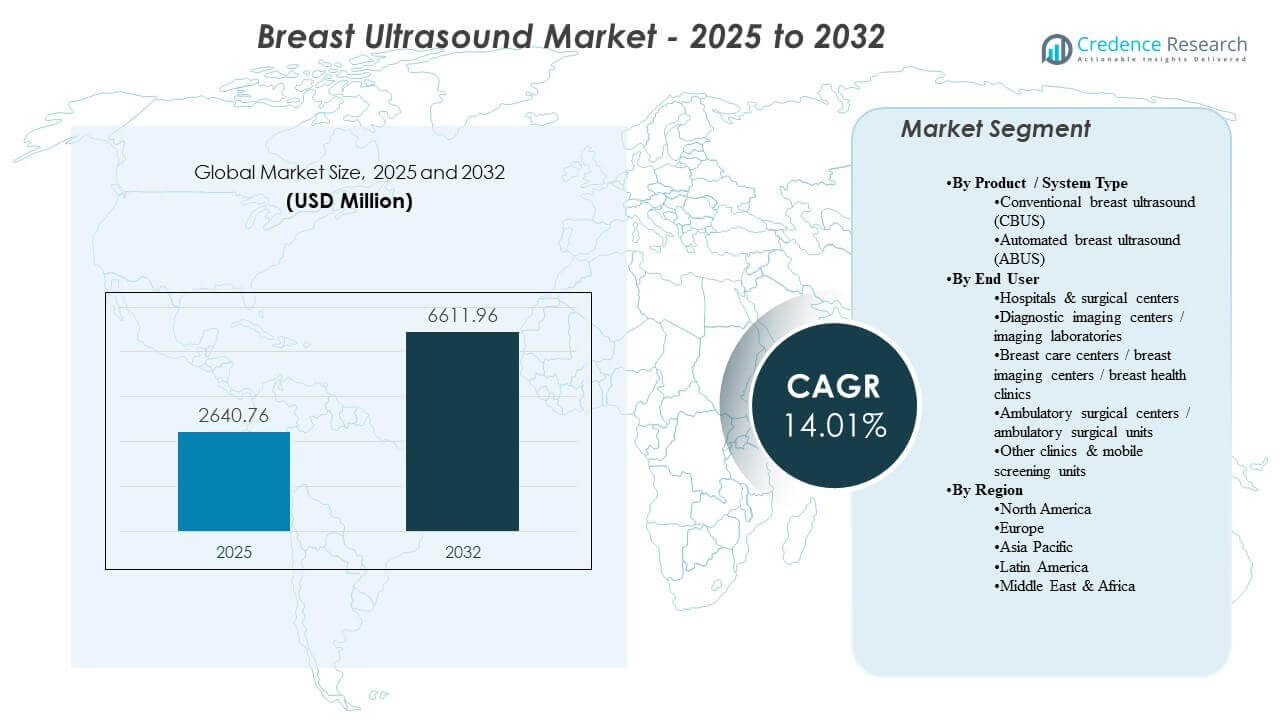

The global Breast Ultrasound Market size was estimated at USD 2640.76 million in 2025 and is expected to reach USD 6611.96 million by 2032, growing at a CAGR of 14.1% from 2025 to 2032. Demand is being propelled by rising breast cancer screening and diagnostic workups, where ultrasound is used to improve lesion characterization, guide biopsies, and support assessment in dense breast tissue. Adoption is also strengthened by technology refresh cycles that prioritize workflow automation, consistency in image acquisition, and integration into radiology operations across high-volume care settings.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Breast Ultrasound Market Size 2025 |

USD 2640.76million |

| Breast Ultrasound Market, CAGR |

14.1% |

| Breast Ultrasound Market Size 2032 |

USD 6611.96 million |

Key Market Trends & Insights

- The market expands from USD 2640.76 million in 2025 to USD 6611.96 million by 2032, reflecting a 14.1% CAGR over 2025–2032.

- North America accounts for 33.4% of revenue in 2025, supported by screening intensity and established imaging infrastructure.

- Europe represents 25.3% of revenue in 2025, sustained by organized care pathways and strong diagnostic imaging utilization.

- Asia Pacific holds 24.6% share in 2025, underpinned by capacity expansion and broader access to diagnostic imaging.

- Conventional breast ultrasound (CBUS) accounts for 61.9% share in 2025, reflecting continued preference for flexible, operator-led diagnostic assessment.

Segment Analysis

Purchasing decisions in breast ultrasound emphasize image quality, exam consistency, and throughput in screening-driven environments. Conventional systems remain widely deployed because clinical teams rely on flexible scanning for targeted diagnostic assessment, follow-up imaging, and interventional guidance. At the same time, automated systems are increasingly evaluated for their ability to standardize acquisition and reduce variability across operators, particularly in workflows that support dense-breast supplemental screening.

Adoption is also shaped by staffing and productivity constraints in imaging departments. Providers prioritize tools that shorten exam time, reduce repeat scans, and improve reporting consistency across sites. Integration with broader imaging IT, structured reporting, and embedded analytics supports faster reading workflows and operational control. These themes reinforce replacement demand and upgrades across installed bases in hospitals and outpatient imaging networks.

By Product / System Type Insights

Conventional breast ultrasound (CBUS) accounted for the largest share of 61.9% in 2025. CBUS leads because targeted diagnostic assessment and interventional guidance depend on real-time operator control, which fits day-to-day radiology and breast clinic needs. CBUS also benefits from broad availability across care settings and familiar clinical workflows, which supports high utilization and replacement demand. Automated breast ultrasound (ABUS) is adopted as a complement in standardized screening pathways, especially where acquisition consistency and throughput are priorities.

By End User Insights

Hospitals & surgical centers accounted for the largest share of 51.4% in 2025. Hospitals lead because breast imaging is embedded within multidisciplinary diagnostic and treatment pathways that require imaging availability, biopsy guidance capability, and coordinated follow-up. Capital budgets and consolidated procurement structures also favor standardized ultrasound platforms across departments. Outpatient imaging centers and specialized breast clinics strengthen demand by competing on access and throughput, creating steady upgrades and incremental placements as volumes grow.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Breast Ultrasound Market Drivers

Expanding screening and diagnostic evaluation volumes

Breast cancer awareness and screening participation continue to increase the number of diagnostic workups and follow-up assessments. Ultrasound plays an essential role in lesion characterization, supplemental imaging for dense breast tissue, and targeted evaluation after suspicious findings. This supports higher utilization rates for both general and breast-dedicated ultrasound systems. The result is steady demand for new systems, transducer upgrades, and productivity-focused software enhancements. As screening programs broaden, imaging providers also need faster scheduling capacity to manage higher callback volumes. In parallel, growth in biopsy guidance and follow-up imaging strengthens recurring utilization in routine clinical practice.

Demand for supplemental imaging in dense breast pathways

Dense breast tissue can reduce mammography sensitivity, increasing reliance on ultrasound as a complementary modality in many care pathways. Providers adopt ultrasound to improve detection confidence and to support rapid, point-of-care decision making. Automated solutions strengthen this driver by offering standardized acquisition for screening-adjacent protocols. This dynamic expands addressable demand beyond tertiary hospitals into networks of breast centers and imaging providers. More jurisdictions and clinical pathways emphasize supplemental imaging discussions for dense breasts, which adds incremental ultrasound volume. Providers also value solutions that can integrate into structured reporting and longitudinal patient tracking for repeat screening.

Workflow productivity and standardization priorities

Radiology departments face growing imaging volumes and staffing constraints, creating demand for solutions that improve throughput and reduce repeat scanning. Automation features, guided workflows, and faster acquisition improve operational consistency. Standardization also supports multi-site networks that want comparable imaging protocols and reporting quality. These priorities influence procurement decisions toward systems that combine performance with efficiency. Sites increasingly evaluate systems on total exam time, from acquisition through reporting, not just image quality. Demand also rises for tools that reduce operator variability and support training across rotating staff teams.

- For instance, AI-enabled breast ultrasound decision support has demonstrated sensitivity of 91.1% and specificity of 92.4%, while reducing radiologist reading time to less than 2 seconds for the AI component, enabling radiologists to increase daily case volume without compromising accuracy.

Technology refresh cycles and software-led differentiation

Vendors continue to compete through platform updates that enhance image processing, ergonomics, and clinical application packages. Software upgrades and AI-enabled features support higher productivity and more consistent exam quality. Health systems favor solutions that extend lifecycle value through upgrades rather than frequent hardware replacement. This accelerates adoption of premium platforms and strengthens replacement and upgrade momentum. Buyers also prioritize connectivity features that streamline PACS/RIS integration and reduce manual steps in documentation. As competition increases, vendors use software roadmaps and service contracts to protect installed bases and drive recurring revenue.

- For instance, integrated ABUS platforms that link directly with PACS and electronic records have been reported to improve data accessibility by over 40% and increase imaging center throughput by around 20%, helping providers justify refresh investments on the basis of measurable operational gains.

Breast Ultrasound Market Challenges

Cost pressure remains a constraint, especially for smaller imaging providers and systems in emerging markets. Premium platforms and automated solutions can require higher upfront investment and dedicated workflow changes, slowing adoption where budgets are limited. Facilities also weigh lifecycle service costs and probe replacement needs, which can affect total cost of ownership and procurement timing. These issues are more pronounced for sites that operate mixed fleets with varied service profiles. Reimbursement variability across geographies can further complicate purchase decisions and delay upgrades.

Operator dependence and variability remain important practical challenges for ultrasound performance in real-world environments. Training requirements, scan-to-scan consistency, and documentation quality can vary across operators and sites. Integration into clinical IT, structured reporting, and image archiving can also be uneven, particularly where legacy infrastructure persists. These factors create implementation friction and can delay standardization benefits. High staff turnover or reliance on rotating sonographers can increase variability and reduce reproducibility across visits.

- For instance, skill‑assessment studies in fetal ultrasound have shown that models trained on probe motion data can distinguish expert from newly qualified operators with about 95% classification accuracy, underscoring the measurable performance gap between user groups.

Breast Ultrasound Market Trends and Opportunities

Automation and AI-enabled workflow tools are increasingly used to address productivity constraints and improve exam consistency. Providers are prioritizing features that support guided acquisition, reproducible measurements, and faster review. This trend creates opportunities for vendors to differentiate through software roadmaps, upgradeability, and integrated analytics. It also supports expansion of automated solutions where screening-driven volumes are highest. Growing interest in decision-support and triage features also reflects the need to manage reading backlogs and prioritize suspicious findings.

- For instance, Hologic’s FDA‑cleared Genius AI Detection for 3D mammography uses deep learning to pre‑annotate suspicious regions and has been shown in clinical evaluations to reduce radiologist reading time per exam by about 30% while maintaining cancer detection sensitivity around 90% in high‑volume screening settings.

Decentralized care delivery is expanding addressable demand beyond large hospitals into specialized breast clinics, imaging centers, and outreach models. Mobile screening units and distributed service networks require systems that balance portability, reliability, and image quality. As access improves, procurement shifts toward platforms that can be deployed across multiple sites with standardized protocols. This supports multi-unit contracts and service-based partnerships across provider networks. Increasing outpatient imaging volumes also intensify competition on patient access, pushing providers to invest in faster, more standardized workflows.

Regional Insights

North America (33.4%)

North America holds a leading revenue position (33.4%) supported by established screening pathways, dense-breast supplemental imaging adoption, and mature imaging infrastructure. Health systems prioritize platforms that improve throughput and consistency across high-volume radiology operations. Purchasing behavior favors upgradeable systems with strong service coverage and workflow integration. These factors support a sizable installed base and recurring replacement demand.

Europe (25.3%)

Europe accounts for 25.3% of revenue, benefiting from organized care pathways and broad utilization of diagnostic imaging services across public and private providers. Procurement tends to emphasize standardized protocols, clinical performance, and lifecycle value. Vendor competition is shaped by the ability to support multi-site deployments and consistent imaging quality. Demand remains resilient as providers modernize fleets and expand capacity in specialized breast imaging services.

Asia Pacific (24.6%)

Asia Pacific represents 24.6% of revenue, driven by expanding diagnostic capacity, increased access to imaging services, and rising awareness that supports earlier evaluation. The region includes a mix of premium urban centers and cost-sensitive deployments, shaping a two-speed market for platforms. Buyers often prioritize reliability and throughput, with rising interest in automation where workloads are growing fastest. These dynamics sustain both new placements and upgrades as installed bases expand.

Latin America (9.1%)

Latin America holds 9.1% of revenue, influenced by gradual modernization of imaging fleets and expanding access in major urban centers. Providers balance capability needs with budget constraints, supporting a strong market for value-oriented systems alongside selective premium placements. Growth is supported by improving diagnostic capacity and rising utilization of women’s health services. Service availability and procurement financing can influence purchase timing and platform choice.

Middle East & Africa (7.6%)

Middle East & Africa accounts for 7.6% of revenue, shaped by imaging infrastructure expansion and growth of private hospital networks in select countries. Demand is supported by improving access to diagnostic services and increased attention to women’s health screening and early evaluation. Buyers often prioritize systems with durable service models and flexible configurations suitable for varied clinical settings. Market expansion remains uneven across countries, reflecting differences in healthcare investment and capacity.

Competitive Landscape

Competition in the Breast Ultrasound Market is driven by platform performance, workflow efficiency, and software-led differentiation. Vendors emphasize image quality, automation features, and integration into radiology IT to improve productivity and consistency across sites. Product strategies increasingly highlight upgradeability, clinical application breadth, and service models that support installed-base retention. Competitive intensity is highest in premium systems and automated solutions, where providers value throughput gains and standardized acquisition.

GE HealthCare focuses on strengthening breast imaging workflows through automated solutions and software enhancements that support consistency and operational efficiency. The company leverages broad ultrasound portfolios and service reach to support multi-site deployments and standardized protocols. Portfolio positioning benefits from integrating breast-focused capabilities into wider radiology ecosystems. This approach supports competitive presence across both large hospitals and networks that manage screening-driven volumes.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- GE HealthCare (General Electric Company)

- Siemens Healthineers AG

- Koninklijke Philips N.V. (Philips)

- Canon Medical Systems Corporation (Canon Inc.)

- Hologic, Inc. (incl. Supersonic Imagine technology)

- FUJIFILM Holdings Corporation

- Samsung Electronics (Samsung Healthcare)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (Mindray)

- Hitachi (Hitachi Healthcare / Fujifilm-Hitachi in some markets)

- Esaote S.p.A.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In March 2025, GE HealthCare launched the Invenia Automated Breast Ultrasound (ABUS) Premium, an AI enabled 3D automated breast ultrasound system designed for supplemental screening in dense breasts, with the launch announced on March 20, 2025 and initial roll out planned in key global markets throughout 2025.

- In December 2025, DeepHealth (a subsidiary of RadNet, Inc.) announced the launch of its DeepHealth Breast Suite, a modular AI powered platform integrating breast cancer detection, breast density assessment, risk stratification, and reporting tools, with the product officially unveiled on December 1, 2025.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 2,640.76 million |

| Revenue forecast in 2032 |

USD 6,611.96 million |

| Growth rate (CAGR) |

14.1% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Product / System Type Outlook: Conventional breast ultrasound (CBUS), Automated breast ultrasound (ABUS);

By End User Outlook: Hospitals & surgical centers, Diagnostic imaging centers / imaging laboratories, Breast care centers / breast imaging centers / breast health clinics, Ambulatory surgical centers / ambulatory surgical units, Other clinics & mobile screening units |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

GE HealthCare (General Electric Company); Siemens Healthineers AG; Koninklijke Philips N.V. (Philips); Canon Medical Systems Corporation (Canon Inc.); Hologic, Inc. (incl. Supersonic Imagine technology); FUJIFILM Holdings Corporation; Samsung Electronics (Samsung Healthcare); Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (Mindray); Hitachi; Esaote S.p.A. |

| No. of Pages |

325 |

Segmentation

By Product / System Type

- Conventional breast ultrasound (CBUS)

- Automated breast ultrasound (ABUS)

By End User

- Hospitals & surgical centers

- Diagnostic imaging centers / imaging laboratories

- Breast care centers / breast imaging centers / breast health clinics

- Ambulatory surgical centers / ambulatory surgical units

- Other clinics & mobile screening units

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa