Brugada Syndrome Market Overview:

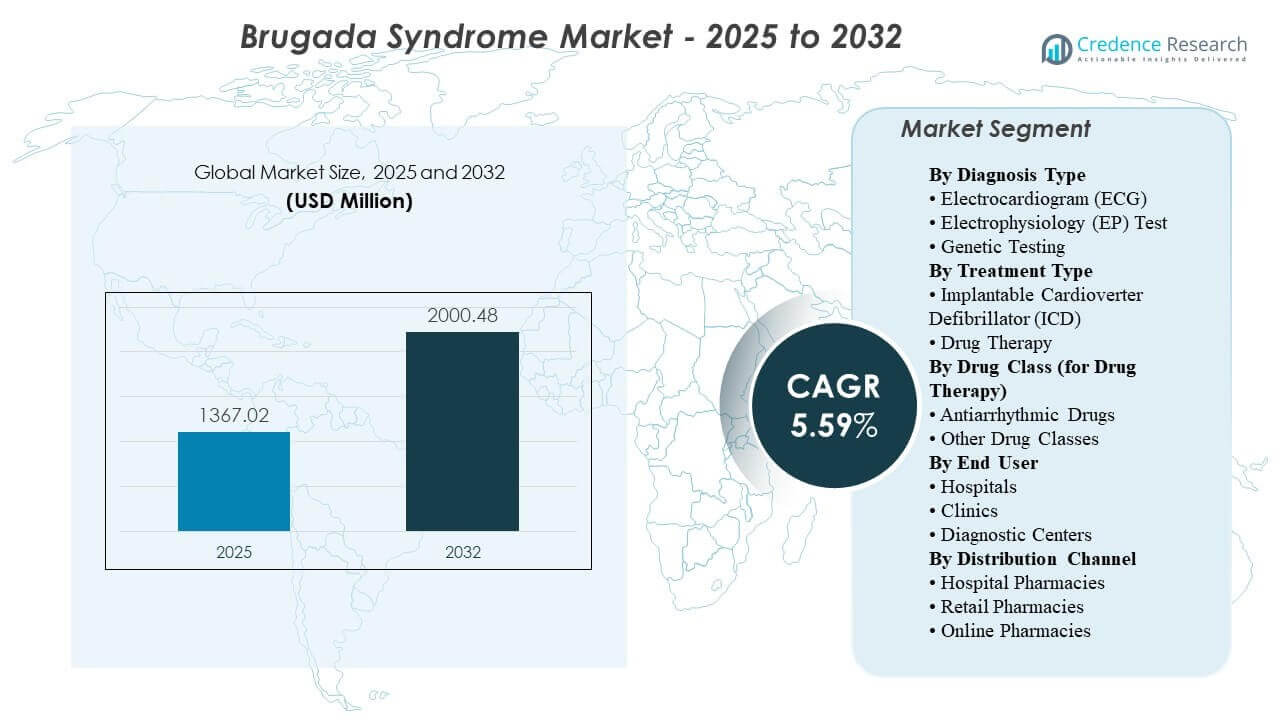

The global Brugada Syndrome market size was estimated at USD 1367.02 million in 2025 and is expected to reach USD 2000.48 million by 2032, growing at a CAGR of 5.59% from 2025 to 2032. Primarily driven by greater clinical focus on preventing sudden cardiac death in higher-risk patients, which sustains demand for definitive rhythm-management pathways supported by specialist evaluation and device therapy. Ongoing expansion of ECG access across emergency and outpatient settings, along with gradual adoption of inherited-risk assessment for family screening, supports earlier identification and referral into electrophysiology-led care pathways across major healthcare systems.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Brugada Syndrome Market Size 2025 |

USD 1367.02 million |

| Brugada Syndrome Market, CAGR |

5.59% |

| Brugada Syndrome Market Size 2032 |

USD 2000.48 million |

Key Market Trends & Insights

- The global Brugada Syndrome market is projected to increase from USD 1,367.02 million in 2025 to USD 2,000.48 million by 2032, at a 5.59% CAGR (2025–2032).

- Implantable Cardioverter Defibrillator (ICD) accounted for the largest share of 65% in 2025, supported by high-risk prevention protocols in specialist cardiac care.

- Electrocardiogram (ECG) accounted for the largest share of 49% in 2025, reflecting broad first-line usage across screening and triage settings.

- Hospital Pharmacies led distribution with 56% in 2025, and Hospitals led end-user adoption with 51% in 2025, reflecting hospital-centered diagnosis-to-treatment pathways.

- Regional demand remained concentrated in North America (38% in 2025), followed by Europe (30% in 2025) and Asia Pacific (22% in 2025), reflecting specialist capacity and diagnostic access across developed and scaling healthcare systems.

Segment Analysis

The Brugada Syndrome market is defined by a care pathway that begins with ECG-based identification and progresses toward risk stratification, specialist electrophysiology evaluation, and definitive prevention for higher-risk populations. Diagnosis demand is sustained by broader availability of ECG testing in emergency departments and outpatient cardiology settings, where suspicious patterns can trigger downstream referrals. Genetic testing adoption continues to expand for family screening and inherited-risk workups, although utilization remains selective and protocol-driven in many health systems.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Treatment revenue remains concentrated in device-led prevention for patients with elevated arrhythmic risk, supported by hospital-based electrophysiology teams and procedure capacity. Drug therapy plays a narrower role, most commonly as targeted management for selected patients under specialist oversight or as supportive therapy within broader arrhythmia management. End-user and channel concentration aligns with hospital-led diagnosis, procedural management, and pharmacy dispensing patterns linked to inpatient and specialist outpatient workflows.

Diagnosis Type Insights

Electrocardiogram (ECG) accounted for the largest share of 49% in 2025. ECG leads because ECG testing represents the first-line, widely available diagnostic tool used across both acute and outpatient settings. Broad access enables higher screening and triage volumes, which increases referral flow into specialist electrophysiology services. Standardized ECG interpretation pathways and increased clinician awareness support earlier recognition of suspicious patterns and follow-on evaluation.

Treatment Type Insights

Implantable Cardioverter Defibrillator (ICD) accounted for the largest share of 65% in 2025. ICD therapy leads because ICD implantation provides direct protection against life-threatening ventricular arrhythmias in higher-risk patients. Clinical decision-making is concentrated in tertiary centers with electrophysiology capability, supporting consistent utilization in eligible populations. Device-led management also aligns with long-term monitoring and follow-up pathways that remain anchored in hospital and specialty cardiology networks.

Drug Class Insights

Antiarrhythmic Drugs and other drug classes remain important within drug therapy, with utilization shaped by specialist protocols and patient-specific risk profiles. Antiarrhythmic use is typically concentrated in selected clinical scenarios where pharmacologic rhythm control is appropriate under close supervision. Treatment selection is influenced by clinician preference, local guideline interpretation, and patient tolerance to therapy. Drug therapy demand also links to ongoing outpatient follow-up and continuity of care managed through cardiology-led pathways.

End User Insights

Hospitals accounted for the largest share of 51% in 2025. Hospitals lead because hospitals consolidate electrophysiology labs, acute arrhythmia care capacity, and procedural infrastructure for device-based treatment. Referral patterns also concentrate complex rhythm evaluation and follow-up within tertiary hospital networks. Hospitals additionally provide multidisciplinary care coordination, which supports higher diagnostic throughput and treatment conversion within a single system.

Distribution Channel Insights

Hospital Pharmacies accounted for the largest share of 56% in 2025. Hospital pharmacy leadership reflects the hospital-centered flow of diagnosis, electrophysiology evaluation, procedural management, and structured follow-up. Medication dispensing linked to peri-procedural care and specialist outpatient services remains concentrated within hospital networks in many countries. Continuity of therapy for selected patients also supports repeat dispensing through hospital-affiliated channels that coordinate with specialist care teams.

Brugada Syndrome Market Drivers

Expansion of first-line ECG screening and triage

Broader ECG availability across emergency departments, outpatient cardiology clinics, and diagnostic networks increases detection of suspicious rhythm patterns. Earlier recognition strengthens referral flows into specialist electrophysiology evaluation. Improved clinical awareness and structured triage pathways support more consistent evaluation after abnormal findings. Expanded testing access also improves identification in populations with intermittent presentation and non-specific symptom profiles.

- For instance, GE HealthCare’s MAC 5 Resting ECG Analysis System (FDA 510(k) K221321) can acquire 3-, 6-, or 12‑lead ECGs and connect over wired LAN or Wi‑Fi to cardiology information systems (e.g., MUSE) to support a more consistent triage workflow from acquisition through interpretation review by clinicians.

Greater emphasis on sudden cardiac death prevention in high-risk patients

Specialist care pathways prioritize prevention strategies for patients with elevated arrhythmic risk. Device-based therapy remains a central clinical option for high-risk cohorts, sustaining procedure volumes in tertiary centers. Risk stratification practices supported by specialist evaluation reinforce treatment conversion for eligible populations. Long-term follow-up needs also support continuity of care and associated service utilization.

Growth in electrophysiology capacity and specialized arrhythmia care

Investment in electrophysiology labs, specialized staffing, and workflow optimization supports higher patient throughput. Expanded procedural capacity improves access for complex evaluation and management. Consolidation of arrhythmia services within tertiary hospitals strengthens standardization of protocols and care coordination. The concentration of expertise supports adoption of advanced diagnostic and intervention pathways.

- For instance, in the GUARD‑AF randomized trial (11,905 enrolled patients across 149 U.S. primary care sites; median follow‑up 15 months), screening with iRhythm’s on‑label Zio XT 14‑day long‑term continuous monitoring increased new AF diagnoses versus usual care (5.0% vs 3.3%), which can translate into higher downstream referral and specialist workload in systems that expand EP capacity.

Gradual expansion of inherited-risk assessment and family screening

Genetic testing adoption increases for family screening and inherited-risk workups in selected protocols. Identification of at-risk relatives can expand diagnostic volume and specialist follow-up over time. Integration with counseling and cardiology-led surveillance supports continuity of care and repeat clinical touchpoints. Adoption rates vary by health system, but expansion supports incremental market growth.

Brugada Syndrome Market Challenges

Care pathways face diagnostic complexity because Brugada patterns can be dynamic and may not be consistently visible across routine assessments. Variation in interpretation and referral timing can delay definitive evaluation and reduce treatment conversion in some settings. Specialist capacity remains uneven, with electrophysiology services concentrated in urban tertiary centers and limited availability in smaller cities. Access gaps can reduce diagnostic follow-through after initial ECG findings.

- For instance, Philips’ DXL 12/16‑lead ECG Algorithm (FDA 510(k) K132068) is explicitly positioned to provide automated ECG measurements and interpretive statements “on an advisory basis” with physician over‑read required, illustrating how interpretation workflows depend on clinician validation rather than automation alone.

Genetic testing utilization remains constrained by variability in clinical protocols, differing reimbursement environments, and uneven availability of integrated counseling services. Clinical decision-making around risk stratification and downstream management can differ across countries and institutions, which creates heterogeneity in care pathways. Device affordability and procedure access can limit penetration in cost-sensitive systems. Follow-up burden and long-term monitoring needs can also reduce continuity of care in resource-constrained settings.

Market Trends and Opportunities

Adoption of advanced ECG workflows, including improved interpretation pathways and integration into broader cardiac diagnostic programs, supports earlier identification and standardized referral. Expansion of portable and point-of-care ECG capabilities broadens access beyond tertiary hospitals and improves triage in community settings. Increasing integration of diagnostic data into clinical workflows supports more consistent clinical decision-making. These factors collectively improve downstream evaluation volumes for specialist services.

- For instance, AliveCor reported FDA clearance updates that brought the total to 39 cardiac determinations for its Kardia 12L AI (KAI 12L), and also stated the platform has recorded over 350 million ECGs and can remotely detect six common arrhythmias in 30 seconds, which are concrete examples of workflow-standardizing capabilities at scale.

Opportunities remain strong for scaling inherited-risk testing services through integrated programs that combine testing, counseling, and structured cascade screening. Expansion of specialist networks and shared-care pathways can improve access in emerging markets and secondary cities. Partnerships between device providers, hospitals, and health systems can strengthen training, service support, and procedural standardization. Growth potential remains particularly relevant in regions where access to electrophysiology services and structured pathways continues to expand.

Regional Insights

North America

North America held 38% share in 2025, supported by strong electrophysiology capacity and established device-based prevention pathways for higher-risk populations. Hospital networks often provide integrated diagnosis-to-treatment workflows, which supports higher conversion from initial ECG findings to specialist evaluation. Access to advanced diagnostics and specialist follow-up strengthens continuity of care. Market demand also benefits from mature referral systems linking emergency settings and outpatient cardiology to tertiary electrophysiology centers.

Europe

Europe held 30% share in 2025, reflecting established cardiology networks and structured pathways for specialized arrhythmia care. Tertiary centers provide electrophysiology evaluation capacity and procedural infrastructure for device therapy, which supports consistent utilization in eligible patients. Adoption is influenced by country-level reimbursement and care delivery models, but specialist concentration remains a key demand factor. Ongoing modernization of electrophysiology services supports gradual expansion across major healthcare systems.

Asia Pacific

Asia Pacific held 22% share in 2025, supported by expanding diagnostic access, growing specialist capacity, and increasing clinical awareness in large healthcare markets. Growth is reinforced by improving hospital infrastructure and gradual expansion of electrophysiology services across urban centers. Screening and triage improvements support earlier identification and referrals in systems with increasing outpatient cardiology access. Regional growth is also supported by increasing investment in advanced cardiac care services and diagnostic workflows.

Latin America

Latin America held 4% share in 2025, with demand influenced by access to tertiary cardiology centers and variability in electrophysiology capacity across countries. Market expansion is supported by gradual growth in specialist services within large urban hospitals and private healthcare systems. Improvements in diagnostic access and referral networks can increase follow-through from initial ECG detection to specialist evaluation. Affordability and access constraints continue to shape penetration, but steady infrastructure expansion supports incremental growth.

Middle East & Africa

Middle East & Africa held 6% share in 2025, with market performance shaped by uneven distribution of specialist capacity and variable access to advanced diagnostics. Demand concentrates in tertiary hospitals and private systems where electrophysiology services are available. Expansion of cardiac centers and specialist staffing supports gradual improvement in access. Development of structured referral pathways and broader diagnostic availability can improve downstream evaluation and treatment volumes.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Competitive Landscape

Competition is driven by differentiation across cardiac rhythm management devices, electrophysiology ecosystems, and diagnostic platforms that support screening, triage, and specialist workflows. Companies compete through product performance, clinical integration, service coverage, training support, and the ability to align offerings with hospital-led protocols. Strategic focus often includes deepening relationships with tertiary centers that set clinical pathways and purchasing decisions. Portfolio breadth across diagnostics and intervention support remains an important positioning lever.

Medtronic plc maintains a strong footprint through cardiac rhythm management and device-led arrhythmia prevention capabilities aligned with tertiary electrophysiology pathways. The company emphasis typically includes integration with hospital workflows, service support, and product innovation that targets procedural efficiency and long-term patient management. A broad presence across cardiac device categories supports cross-selling within hospital networks and specialist centers. Continued engagement with electrophysiology stakeholders supports protocol alignment and adoption in high-volume centers.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Medtronic plc

- Abbott Laboratories

- Boston Scientific Corporation

- BIOTRONIK SE & Co. KG

- Koninklijke Philips N.V.

- GE HealthCare

- Nihon Kohden Corporation

- Johnson & Johnson (Biosense Webster)

- LivaNova PLC

- Stereotaxis, Inc.

- AliveCor, Inc.

- GeneDx

- Mayo Clinic Laboratories

- Invitae Corporation

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments

- In December 2025, Victor Chang Cardiac Research Institute partnered with Vanderbilt University Medical Center to advance Brugada Syndrome diagnosis by developing a high-throughput SCN5A genetic function test aimed at improving risk assessment and variant interpretation.

- In July 2025, Omron Healthcare expanded its collaboration with Tricog Health to launch “KeeboHealth,” a connected remote cardiac care platform that integrates home monitoring devices with Tricog’s AI engine for continuous cardiac monitoring and alerts (relevant to arrhythmia-focused care pathways that overlap with Brugada Syndrome screening and management workflows).

- In March 2025, Abbott received CE Mark approval for its Volt Pulsed Field Ablation System and began commercial procedures across European markets, reflecting continued product expansion in electrophysiology tools used in arrhythmia care settings that also manage high-risk Brugada Syndrome patients.

- In January 2025, AliveCor validated its Kardia 12L ECG System, reporting equivalence to conventional 12‑lead ECGs across multiple determinations and strengthening the case for point-of-care ECG screening approaches used in inherited arrhythmia pathways such as Brugada Syndrome workups.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 1,367.02 million |

| Revenue forecast in 2032 |

USD 2,000.48 million |

| Growth rate (CAGR) |

5.59% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Diagnosis Type Outlook: Electrocardiogram (ECG), Electrophysiology (EP) Test, Genetic Testing; By Treatment Type Outlook: Implantable Cardioverter Defibrillator (ICD), Drug Therapy; By Drug Class (for Drug Therapy) Outlook: Antiarrhythmic Drugs, Other Drug Classes; By End User Outlook: Hospitals, Clinics, Diagnostic Centers; By Distribution Channel Outlook: Hospital Pharmacies, Retail Pharmacies, Online Pharmacies |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Medtronic plc, Abbott Laboratories, Boston Scientific Corporation, BIOTRONIK SE & Co. KG, Koninklijke Philips N.V., GE HealthCare, Nihon Kohden Corporation, Johnson & Johnson (Biosense Webster), LivaNova PLC, Stereotaxis, Inc., AliveCor, Inc., GeneDx, Mayo Clinic Laboratories, Invitae Corporation |

| No. of Pages |

335 |

By Segmentation

BY DIAGNOSIS TYPE

- Electrocardiogram (ECG)

- Electrophysiology (EP) Test

- Genetic Testing

BY TREATMENT TYPE

- Implantable Cardioverter Defibrillator (ICD)

- Drug Therapy [Antiarrhythmic Drugs; Other Drug Classes]

BY END USER

- Hospitals

- Clinics

- Diagnostic Centers

BY DISTRIBUTION CHANNEL

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

BY REGION

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa