Hair and Scalp Care Market Overview:

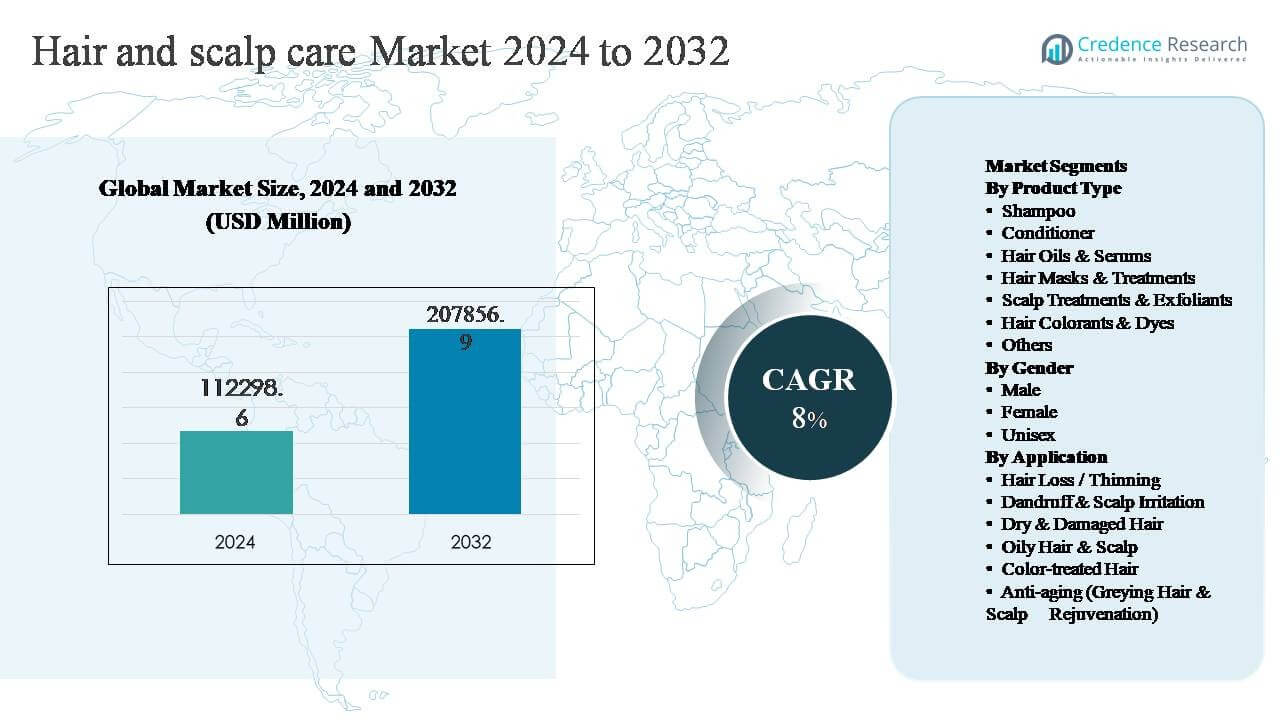

Hair and scalp care market size was valued at USD 112,298.6 million in 2024 and is anticipated to reach USD 207,856.9 million by 2032, expanding at a CAGR of approximately 8% during the forecast period (2025-2032).

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Hair and Scalp Care Market Size 2024 |

USD 112,298.6 million |

| Hair and Scalp Care Market, CAGR |

8% |

| Hair and Scalp Care Market Size 2032 |

USD 207,856.9 million |

Hair and Scalp Care Market Insights

- Market growth is primarily driven by increasing consumer focus on scalp health, hair loss prevention, and treatment-based routines, with shampoo remaining the dominant product segment, accounting for over 35% share, due to its daily usage and expanding multifunctional formulations.

- Key trends include premiumization, clean-label products, and dermatology-aligned claims, while competition remains intense among global brands leveraging innovation, digital engagement, and broad distribution to defend market positions.

- Market restraints include product commoditization in core categories, high marketing costs, and regulatory scrutiny on ingredients and efficacy claims, which increase compliance complexity and pressure margins.

- Regionally, Asia Pacific leads with ~38% share, followed by North America (~26%) and Europe (~23%), while Latin America (~7%) and Middle East & Africa (~6%) show steady growth driven by rising grooming awareness and retail expansion.

Hair and Scalp Care Market Segmentation Analysis:

By Product Type

By product type, shampoo remains the dominant sub-segment in the hair and scalp care market, accounting for the largest share due to its essential, high-frequency usage across all consumer groups. Demand is driven by product innovation focused on sulfate-free formulations, scalp-balancing actives, and multifunctional benefits such as anti-dandruff and hair-fall control. Conditioners and hair oils & serums follow as strong secondary segments, supported by rising focus on hair nourishment and damage repair. Rapid growth in scalp treatments and exfoliants reflects increasing consumer awareness of scalp health as the foundation of hair care.

- For instance, L’Oréal Paris Research & Innovation developed the sulfate-free EverPure shampoo line using amino acid–based surfactants (such as sodium cocoyl isethionate) and gentle botanicals like rosemary and lotus flower.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Gender

By gender, the female segment dominates market share, driven by higher product penetration, broader routines, and strong demand for treatment-oriented solutions addressing damage, coloring, and styling stress. Women-led demand supports premium shampoos, masks, serums, and color-protection products. The male segment is expanding steadily, supported by rising grooming awareness and targeted solutions for hair loss and dandruff. Meanwhile, the unisex category is gaining momentum as brands prioritize inclusive branding and simplified formulations, particularly in mass-market shampoos and scalp-care products designed for shared household use.

- For instance, Kao Corporation’s Goldwell Dualsenses Color Extra Rich line utilizes Luminescine technology, which transforms non-visible UV light into visible light to enhance color luminosity. The line features the microPROtec complex to distribute care ingredients quickly and evenly.

By Application

By application, hair loss and thinning represents the dominant sub-segment, driven by increasing stress levels, lifestyle changes, aging populations, and greater acceptance of preventive hair care solutions. Products addressing hair fall combine scalp stimulation, strengthening actives, and dermatologically positioned claims, supporting strong consumer uptake. Dandruff and scalp irritation remains a core application due to widespread prevalence, while dry and damaged hair benefits from rising chemical treatments and heat styling. Growing interest in anti-aging and scalp rejuvenation further supports premiumization and innovation across application-focused formulations.

Key Growth Drivers

Rising Consumer Focus on Scalp Health and Preventive Care

Growing awareness that scalp health directly influences hair quality is a major driver of the hair and scalp care market. Consumers increasingly view scalp care as preventive wellness rather than corrective grooming, accelerating demand for exfoliating shampoos, scalp serums, tonics, and anti-dandruff treatments. Education through dermatologists, trichologists, and digital platforms has strengthened understanding of issues such as follicle blockage, inflammation, and microbiome imbalance. This shift supports regular, long-term product usage rather than occasional treatments, improving category value and volume growth. The trend is further reinforced by urban lifestyles marked by pollution, stress, and hard water exposure, which exacerbate scalp-related concerns. As a result, brands are prioritizing scalp-first positioning and functional benefits, driving sustained expansion across mass, premium, and professional channels.

- For instance, Unilever’s Clear Scalpceuticals Pro platform integrates a “skinification” approach using amino acid–based surfactants (such as glycine) and skincare-inspired actives like Niacinamide. These formulations are clinically proven to improve the scalp barrier and reduce hair fall within 30 days (approximately 12–15 wash cycles in standard trials).

Premiumization Driven by Ingredient Transparency and Performance Claims

Premiumization remains a strong growth driver as consumers seek high-efficacy products with visible results. Shoppers increasingly scrutinize ingredient labels, favoring formulations that highlight clinically recognized actives such as peptides, botanical extracts, ceramides, and scalp-soothing compounds. This behavior supports higher spending on targeted solutions for hair loss, damage repair, color protection, and scalp sensitivity. Clean-label positioning, sulfate-free and silicone-free formulations, and dermatologically tested claims further enhance brand credibility and pricing power. Premium growth is also fueled by salon-grade and dermatology-inspired products migrating into retail and online channels. As consumers associate higher price points with safety, efficacy, and long-term benefits, premium and masstige segments continue to outpace overall market growth.

- For instance,The Aveda Invati Advanced and newer Invati Ultra Advanced systems highlight ginseng and certified organic turmeric as part of an Ayurvedic herb blend designed to invigorate the scalp when massaged in. Their efficacy in reducing hair loss due to breakage is substantiated through instrumental repeat grooming tests on hair tresses.

Expanding Male Grooming and Gender-Neutral Product Adoption

The increasing acceptance of male grooming and self-care significantly contributes to market growth. Men are adopting specialized products for hair thinning, dandruff control, and scalp maintenance, moving beyond basic shampoos toward treatment-oriented solutions. Simultaneously, gender-neutral and unisex products are gaining traction, particularly among younger consumers seeking simplified routines and inclusive branding. These products appeal to shared household usage and align with evolving perceptions of personal care as non-gendered. Brands are responding with versatile formulations, neutral fragrances, and minimalist packaging. This expansion beyond traditional female-dominated demand broadens the consumer base, improves penetration in emerging markets, and supports steady long-term growth across demographic segments.

Key Trends & Opportunities

Growth of Natural, Clean, and Dermatology-Aligned Formulations

A strong trend toward natural and clean beauty continues to shape the hair and scalp care market. Consumers increasingly prefer products formulated with plant-based ingredients, minimal additives, and transparent sourcing practices. This creates opportunities for brands to combine natural positioning with dermatological credibility, addressing concerns around sensitivity, long-term use, and scalp health. The convergence of clean beauty and science-backed efficacy enables differentiation, particularly in anti-dandruff, hair loss, and scalp treatment categories. Products that balance safety, performance, and sustainability are well positioned to capture both premium and mass-market demand, especially among health-conscious and younger consumers.

- For instance, Pierre Fabre’s Ducray dermatological haircare line formulates scalp-soothing products tested under dermatologist supervision on over 500 sensitive-scalp subjects, with transepidermal water loss measured using closed-chamber evaporimeters recording 120 data points per assessment.

Digital Engagement and Direct-to-Consumer Expansion

E-commerce and digital platforms present significant growth opportunities by improving product accessibility and personalization. Online channels enable brands to educate consumers on scalp diagnostics, routine building, and targeted solutions through content, quizzes, and expert consultations. Direct-to-consumer strategies allow companies to gather consumer insights, launch niche products, and respond quickly to evolving preferences. Subscription models for shampoos, serums, and treatment kits further enhance customer retention. As digital-first brands gain credibility and established players strengthen omnichannel strategies, online engagement continues to reshape purchasing behavior and accelerate category innovation.

- For instance,Henkel’s SalonLab&Me (the first hyper-personalized “B2B2C” brand from Schwarzkopf Professional) integrates in-salon hair analysis with a digital fulfillment model for individualized regimens. While Henkel operates highly automated logistics centers such as the hub in Montornès del Vallès these facilities are designed for an annual throughput of approximately 7 million product units (averaging ~19,000 units per day) to meet the growing demand for personalized solutions.

Innovation in Application-Specific and Treatment-Based Solutions

Demand is shifting toward application-specific solutions that address distinct concerns such as hair fall, greying, irritation, and color damage. This creates opportunities for innovation in treatment-based formats, including leave-in serums, ampoules, exfoliants, and overnight scalp treatments. Consumers increasingly accept multi-step routines when benefits are clearly communicated and results are tangible. Brands that invest in targeted efficacy claims and routine-based product ecosystems can strengthen brand loyalty and increase average spend per user, particularly in premium and professional segments.

Key Challenges

Intense Competition and Brand Differentiation Pressure

The hair and scalp care market faces intense competition from global brands, regional players, and emerging digital-native companies. Product saturation in core categories such as shampoos and conditioners makes differentiation increasingly difficult. Frequent product launches, overlapping claims, and aggressive pricing strategies reduce brand loyalty and margin stability. Companies must continuously invest in innovation, marketing, and consumer education to maintain relevance. Smaller brands face scalability challenges, while established players must balance innovation with cost efficiency. This competitive intensity raises barriers to sustained differentiation and long-term profitability.

Regulatory Scrutiny and Ingredient Compliance Complexity

Regulatory requirements surrounding ingredient safety, labeling, and environmental impact pose a significant challenge for market participants. Restrictions on certain preservatives, fragrances, and active compounds vary across regions, increasing formulation complexity and compliance costs. Additionally, heightened scrutiny of marketing claims related to hair loss prevention and scalp treatment efficacy increases legal and reputational risk. Brands must invest in testing, documentation, and regulatory expertise to ensure compliance while maintaining innovation speed. These factors can delay product launches, increase operational costs, and limit flexibility, particularly for companies operating across multiple international markets.

Regional Analysis

North America:

North America accounts for approximately 26% of the global hair and scalp care market, driven by high consumer awareness, premium product penetration, and strong dermatology-backed brand adoption. The region shows robust demand for scalp health solutions, anti-hair loss products, and clean-label formulations, supported by advanced retail infrastructure and e-commerce dominance. Consumers actively seek performance-driven products addressing thinning, dandruff, and aging-related concerns, encouraging premiumization. Innovation in ingredient transparency, clinical claims, and personalized care routines further supports market maturity. The presence of leading multinational brands and strong marketing influence continues to sustain steady growth across both mass and premium segments.

Europe:

Europe holds an estimated 23% market share, supported by strong demand for natural, organic, and sustainability-focused hair and scalp care products. Regulatory emphasis on ingredient safety and environmental compliance shapes product development, favoring clean and eco-certified formulations. The region demonstrates balanced demand across shampoos, conditioners, and treatment-based products, particularly for sensitive scalp, anti-dandruff, and color-protection applications. High adoption of salon-quality products in retail channels supports premium growth. Western Europe leads consumption, while Eastern Europe shows rising penetration as disposable incomes and grooming awareness improve, contributing to consistent regional expansion.

Asia Pacific:

Asia Pacific dominates the global market with approximately 38% share, driven by large population base, increasing urbanization, and rising grooming awareness. High prevalence of hair fall, dandruff, and pollution-related scalp issues fuels strong demand for functional and preventive solutions. The region benefits from frequent product usage and strong penetration of hair oils, serums, and treatment shampoos. Rapid growth in middle-income consumers supports premium and masstige segments, while digital commerce accelerates product accessibility. Countries such as China, India, Japan, and South Korea play a central role, supported by innovation, traditional ingredient integration, and localized product development.

Latin America:

Latin America represents around 7% of the global market, supported by strong cultural emphasis on hair appearance and grooming. Demand is driven by conditioners, hair masks, and treatments targeting dryness, damage, and chemically treated hair. Rising awareness of scalp health and increasing availability of specialized products through retail and online channels support market development. Brazil and Mexico lead regional consumption due to large populations and established beauty industries. Although price sensitivity remains a challenge, growing interest in premium and salon-inspired products is gradually improving value growth across the region.

Middle East & Africa:

The Middle East & Africa region accounts for approximately 6% of the global hair and scalp care market, with growth supported by increasing urban populations and rising personal care expenditure. Demand is concentrated in shampoos, hair oils, and scalp treatments addressing dryness, hair fall, and scalp irritation linked to climatic conditions. The Middle East shows higher adoption of premium and imported brands, while Africa remains driven by mass-market and traditional formulations. Expanding retail infrastructure, social media influence, and improving grooming awareness continue to enhance long-term growth potential across the region.

Hair and Scalp Care Market Segmentations:

By Product Type

- Shampoo

- Conditioner

- Hair Oils & Serums

- Hair Masks & Treatments

- Scalp Treatments & Exfoliants

- Hair Colorants & Dyes

- Others

By Gender

By Application

- Hair Loss / Thinning

- Dandruff & Scalp Irritation

- Dry & Damaged Hair

- Oily Hair & Scalp

- Color-treated Hair

- Anti-aging (Greying Hair & Scalp Rejuvenation)

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The hair and scalp care market is highly competitive, characterized by the presence of multinational consumer goods companies, regional manufacturers, and emerging digital-first brands. Leading players compete through broad product portfolios spanning shampoos, conditioners, treatments, and scalp-focused solutions, supported by strong brand equity and extensive distribution networks. Innovation remains a key differentiator, with companies investing in ingredient science, dermatology-backed claims, and application-specific formulations targeting hair loss, dandruff, and scalp sensitivity. Strategic emphasis on premiumization, clean-label positioning, and sustainability strengthens market positioning. Digital marketing, influencer engagement, and direct-to-consumer channels enhance brand visibility and consumer reach. Meanwhile, regional players leverage localized formulations and pricing strategies to compete effectively. Ongoing product launches, portfolio expansion, and geographic penetration continue to intensify competition, reinforcing the importance of differentiation, trust, and consistent product performance in maintaining market share.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- L’Oréal S.A.

- Procter & Gamble

- Unilever

- Kao Corporation

- Henkel AG & Co. KGaA

- Shiseido Company, Limited

- Marico Limited

- Johnson & Johnson Services, Inc.

- Amway Corp.

- Oriflame Cosmetics AG

Recent Developments

- In December 2025, Unilever announced expanded efforts in the “skinification of scalp care,” with Dove and Clear brands advancing targeted dandruff and scalp formulations that combine premium skincare ingredients with traditional haircare benefits to meet evolving consumer needs.

- June 2025, Kao released its Kao Integrated Report 2025, outlining strategic progress under its “Global Sharp Top” innovation framework signaling continued investment in R&D and long-term hair and scalp care science initiatives.

Report Coverage

The research report offers an in-depth analysis based on Product type, Gender, Application, and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Scalp-focused products will gain wider adoption as consumers increasingly link scalp health with long-term hair quality and growth.

- Demand for treatment-oriented solutions addressing hair loss, thinning, and scalp sensitivity will continue to expand across age groups.

- Premium and masstige segments will grow faster than mass products, supported by ingredient transparency and performance-driven claims.

- Clean, natural, and dermatology-aligned formulations will become standard expectations rather than niche offerings.

- Male grooming and unisex product lines will strengthen market penetration and broaden the consumer base.

- Digital platforms will play a larger role in education, personalization, and direct-to-consumer sales models.

- Application-specific routines will drive multi-product usage, increasing average consumer spend per household.

- Innovation in formats such as serums, exfoliants, and leave-in treatments will reshape traditional care routines.

- Emerging markets will contribute significantly to volume growth due to rising urbanization and grooming awareness.

- Sustainability in packaging and responsible sourcing will increasingly influence brand selection and loyalty.