Mining Waste Management Market Overview:

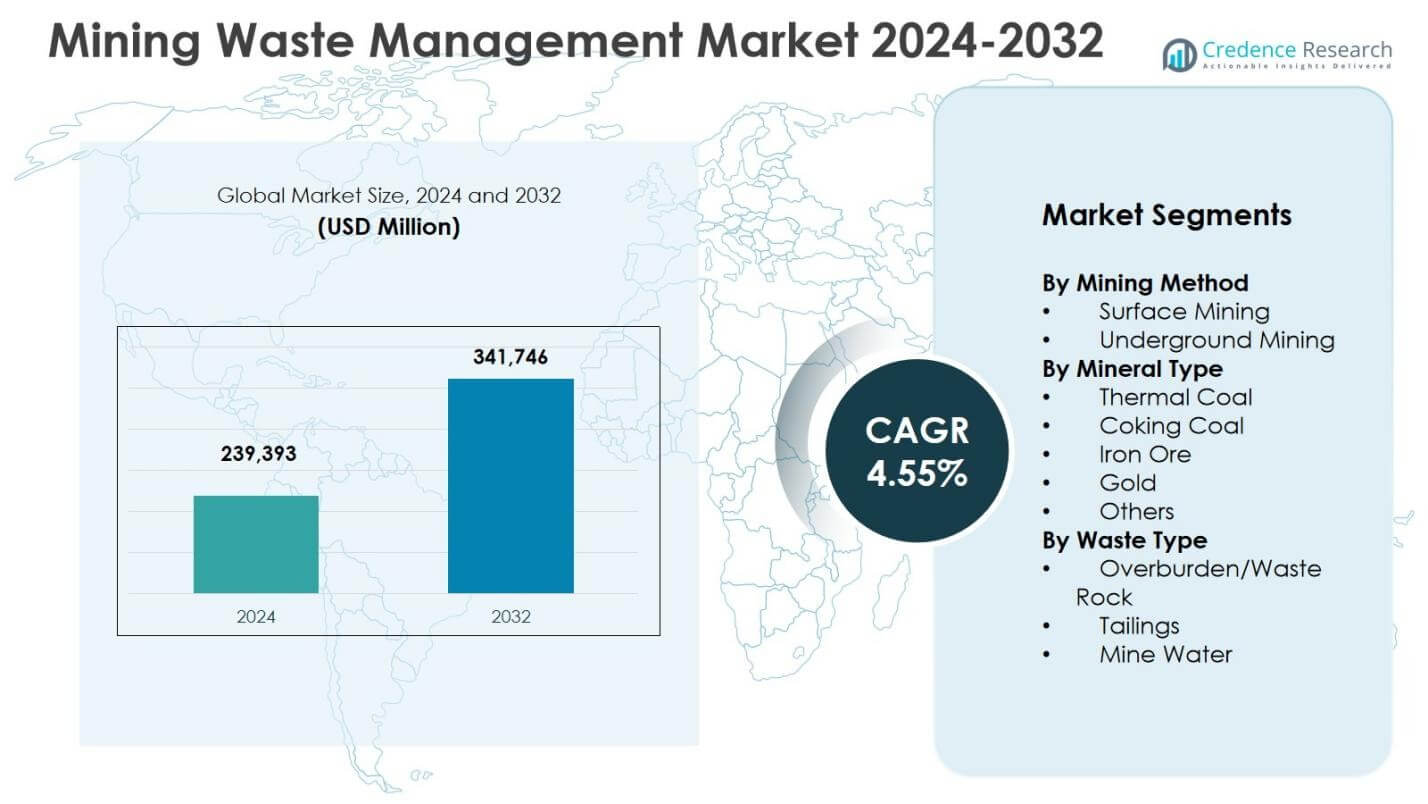

Mining Waste Management Market size was valued at USD 239,393 million in 2024 and is anticipated to reach USD 341,746 million by 2032, registering a CAGR of 4.55% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Mining Waste Management Market Size 2024 |

USD 239,393 million |

| Mining Waste Management Market, CAGR |

4.55% |

| Mining Waste Management Market Size 2032 |

USD 341,746 million |

Mining Waste Management Market Insights

- Market growth is driven by stringent environmental regulations, large-scale surface mining activities, and increasing focus on structured mine closure and rehabilitation, with surface mining holding 64.8% share in 2024 due to high overburden and waste rock generation.

- Key market trends include adoption of advanced tailings management technologies, dry stacking systems, and digital monitoring, while major players focus on integrated service models, long-term contracts, and regulatory compliance across mining lifecycles.

- Market restraints include high capital and operational costs associated with engineered tailings facilities, water treatment plants, and long-term monitoring, along with extended environmental liability risks post mine closure.

- Regionally, Asia Pacific dominated with 34.6% share in 2024, driven by China, Australia, and India, followed by North America with 28.4% and Europe with 22.1%, while overburden and waste rock accounted for 52.3% share among waste types.

Mining Waste Management Market Segmentation Analysis:

By Mining Method:

The mining waste management market by mining method is led by surface mining, which accounted for 64.8% market share in 2024, driven by its extensive adoption in coal, iron ore, and bauxite extraction. Surface mining generates significantly higher volumes of overburden and waste rock, necessitating structured waste handling, storage, and rehabilitation solutions. Regulatory scrutiny on land restoration and slope stability further supports demand for advanced waste management practices in surface operations. Underground mining held 35.2% share, supported by rising deep-ore extraction and increasing focus on mine water treatment and tailings management.

- For instance, AngloGold Ashanti modernized its gold mine’s wastewater treatment plant with Veolia support to handle tailings overflow amid heavy rainfall, improving extraction, tailings ponds, and discharge compliance through revised operations and local team training.

By Mineral Type:

By mineral type, iron ore dominated the mining waste management market with a 38.6% share in 2024, owing to large-scale extraction activities and substantial waste generation during beneficiation processes. High production volumes in Australia, Brazil, and India drive continuous investment in tailings dams, waste rock handling, and environmental compliance systems. Thermal coal followed with 27.4% share, supported by power sector demand and legacy mine operations. Gold accounted for 18.1% share, driven by complex tailings treatment requirements, while coking coal and others jointly represented 15.9% share.

- For instance, Rio Tinto and BHP collaborate on tailings technologies like dewatering to boost water recovery, reducing TSF risks and environmental impact across their Australian iron ore sites.

By Waste Type:

Based on waste type, overburden and waste rock held the dominant 52.3% market share in 2024, primarily due to extensive stripping activities in surface mining operations. The segment’s growth is driven by stringent regulations on waste rock dumping, slope management, and land reclamation. Tailings accounted for 34.7% share, supported by rising investments in tailings dam safety, dry stacking technologies, and recovery of residual minerals. Mine water represented 13.0% share, driven by increasing requirements for water treatment, recycling, and compliance with discharge standards.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Key Growth Drivers

Stringent Environmental Regulations and Compliance Requirements

Stringent environmental regulations governing mine waste disposal, tailings storage, and land rehabilitation strongly drive the mining waste management market. Governments increasingly enforce strict standards related to waste containment, groundwater protection, and post-closure site restoration. Mining operators are required to implement engineered waste storage facilities, continuous environmental monitoring systems, and structured rehabilitation plans. Non-compliance penalties and reputational risks further encourage proactive investment in waste management solutions. As regulatory frameworks continue to tighten across both developed and emerging mining regions, demand for professional waste handling, treatment, and long-term environmental management services remains consistently high.

- For instance, Teck Resources manages 55 tailings facilities across its operating and legacy sites, all meeting or exceeding regulatory requirements through regular audits, independent reviews, and governance processes aligned with Mining Association of Canada standards.

Expansion of Surface Mining and Mineral Production

The continued expansion of surface mining activities significantly accelerates demand for mining waste management solutions. Surface mining operations generate substantial volumes of overburden and waste rock, requiring efficient handling, transportation, and disposal systems. Rising global demand for iron ore, coal, and construction minerals supports sustained production levels, directly increasing waste generation. Mining companies increasingly integrate waste management strategies into mine planning to enhance operational efficiency and environmental performance. This expansion of large-scale extraction projects ensures steady demand for scalable, compliant, and long-duration waste management services.

- For instance, Tata Steel at its Joda East Iron Mine implemented Paste Thickening technology for tailings management, achieving a pulp ratio of 30:70 compared to 70:30 in conventional thickeners.

Increasing Focus on Mine Closure and Rehabilitation

Growing emphasis on responsible mine closure and land rehabilitation is a key driver for the mining waste management market. Regulatory authorities mandate comprehensive closure plans addressing tailings stabilization, waste rock recontouring, and ecosystem restoration. Mining companies are adopting progressive rehabilitation practices during active operations to reduce long-term liabilities and closure costs. Community engagement and sustainability commitments further reinforce this trend. The need for structured post-closure monitoring and maintenance sustains demand for waste management services beyond the operational life of mines.

Key Trends & Opportunities

Adoption of Advanced Tailings Management Technologies

The adoption of advanced tailings management technologies is a major trend shaping the mining waste management market. Mining operators increasingly implement dry stacking, thickened tailings, and real-time monitoring systems to enhance safety and reduce environmental risks. These technologies lower water consumption, improve tailings stability, and minimize the risk of catastrophic failures. Heightened awareness following major tailings incidents has accelerated global adoption. Service providers offering engineered solutions, digital monitoring, and lifecycle management capabilities are well positioned to benefit from increasing investments in safer and more sustainable tailings management practices.

- For instance, Hindustan Zinc Limited partnered with FLSmidth for an integrated dry stack tailings solution at its Rajpura Dariba lead-zinc mine, incorporating two Automatic Filter Presses and a 26m-diameter High-Density Thickener.

Resource Recovery from Mining Waste

Resource recovery from mining waste is emerging as a significant opportunity in the market. Advances in processing and separation technologies enable recovery of residual metals and minerals from tailings and waste rock. Mining companies increasingly treat waste streams as secondary resource reservoirs, supporting circular economy objectives. Investments in reprocessing facilities and waste valorization projects reduce environmental footprints while creating additional revenue streams. Regulatory incentives and sustainability goals further encourage this shift, positioning waste recovery as a long-term growth opportunity within mining waste management.

- For instance, Barrick explores critical metals recovery at Nevada Gold Mines using an ion-exchange system on heap leach copper solutions. This targets nickel, cobalt, scandium, and zinc from waste streams.

Key Challenges

High Capital and Operational Costs

High capital and operational costs remain a critical challenge for the mining waste management market. Engineered tailings storage facilities, water treatment plants, and long-term monitoring systems require substantial upfront investment. Ongoing costs related to maintenance, compliance reporting, and rehabilitation further impact operational budgets. Smaller mining operators often face financial limitations in adopting advanced waste management technologies. Rising compliance requirements increase cost pressure, potentially delaying implementation of best-practice solutions, particularly in cost-sensitive or developing mining regions.

Long-Term Environmental and Liability Risks

Managing long-term environmental and liability risks presents a persistent challenge for mining waste management. Tailings facilities and waste rock dumps require continuous monitoring and maintenance long after mine closure. Structural failures, groundwater contamination, or unforeseen environmental impacts can result in severe legal and financial consequences. Climate variability further heightens risk by affecting hydrology and slope stability. Mining companies must maintain financial assurance mechanisms and long-term stewardship plans, requiring sustained investment and technical expertise over extended time horizons.

Regional Analysis

North America

North America accounted for 28.4% of the mining waste management market in 2024, driven by strict environmental regulations and extensive legacy mining operations. The United States dominates regional demand due to large-scale coal, gold, and metal mining activities that generate significant volumes of tailings and waste rock. Regulatory frameworks enforced by federal and state authorities require advanced waste containment, mine water treatment, and long-term site rehabilitation. Canada also contributes strongly, supported by active metal mining and mandatory closure planning. Continuous investment in tailings dam safety, digital monitoring, and post-closure management sustains market growth across the region.

Europe

Europe held 22.1% market share in 2024, supported by stringent environmental compliance standards and strong emphasis on mine rehabilitation. Countries such as Germany, Sweden, and Poland focus heavily on responsible waste handling in metal and coal mining operations. The region places high priority on groundwater protection, land restoration, and long-term environmental monitoring, driving demand for advanced waste management services. Limited new mining projects are offset by extensive management requirements for legacy and closed mines. Increasing adoption of sustainable mining practices and waste reprocessing initiatives further strengthens Europe’s position in the mining waste management market.

Asia Pacific

Asia Pacific dominated the mining waste management market with a 34.6% share in 2024, driven by high mining activity across China, Australia, and India. Large-scale extraction of coal, iron ore, and industrial minerals generates substantial volumes of overburden, tailings, and mine water. Rapid industrialization and infrastructure development continue to support mineral demand, increasing waste management requirements. Governments are strengthening environmental regulations, particularly around tailings safety and water treatment. Australia’s focus on tailings dam integrity and China’s tightening environmental oversight significantly contribute to sustained growth in waste management services across the region.

Latin America

Latin America accounted for 9.3% of the global market in 2024, supported by extensive copper, gold, and silver mining activities. Countries such as Chile, Peru, and Brazil generate high volumes of tailings due to mineral-rich ore bodies and intensive beneficiation processes. Increasing regulatory scrutiny on tailings storage facilities and water usage drives demand for engineered waste management solutions. Mining companies are investing in dry stacking, water recycling, and rehabilitation programs to comply with evolving standards. Expansion of large-scale mining projects and modernization of waste infrastructure continue to support regional market growth.

Middle East & Africa

The Middle East & Africa region captured 5.6% market share in 2024, driven by expanding mining activities in South Africa, Saudi Arabia, and selected African economies. Gold, phosphate, and industrial mineral mining contribute significantly to waste generation. Governments are increasingly implementing environmental regulations to manage mine tailings, waste rock disposal, and water contamination risks. South Africa remains a key contributor due to its mature mining sector and focus on rehabilitation of legacy sites. Growing foreign investment in mineral extraction and gradual regulatory strengthening support steady demand for mining waste management solutions across the region.

Mining Waste Management Market Segmentations:

By Mining Method

- Surface Mining

- Underground Mining

By Mineral Type

- Thermal Coal

- Coking Coal

- Iron Ore

- Gold

- Others

By Waste Type

- Overburden/Waste Rock

- Tailings

- Mine Water

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

Competitive landscape analysis of the Mining Waste Management Market features key players including Veolia Environment S.A., Cleanaway Environmental Services, John Wood Group plc, Ramboll Group, Tetra Tech Inc., Interwaste Holding Ltd., EnviroServ, Seche Environnement, Tetronics International, and Golder Associates Inc.. The market is moderately consolidated, with global environmental service providers competing alongside specialized engineering and consulting firms. Leading companies focus on integrated service offerings covering tailings management, mine water treatment, waste rock handling, and site rehabilitation. Strategic priorities include expanding long-term service contracts, strengthening regulatory compliance capabilities, and deploying advanced tailings monitoring technologies. Partnerships with mining operators and government bodies support stable revenue streams. Regional players maintain strong positions through localized expertise and regulatory familiarity, while multinational firms leverage scale, technical innovation, and global project experience to secure large mining contracts across developed and emerging regions.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Ramboll Group

- Cleanaway Environmental Services

- Tetronics International

- Veolia Environment S.A.

- Seche Environment Company

- Interwaste Holding Ltd.

- John Wood Group plc

- EnviroServ

- Tetra Tech Inc.

- Golder Associates Inc.

Recent Developments

- In December 2025, IAMGOLD Corporation completed the acquisition of Mines D’Or Orbec Inc., finalizing the previously announced transaction to expand its gold mining footprint.

- In December 2025, Champion Iron Ltd entered into an agreement to acquire Norwegian iron ore company Rana Gruber, expanding its iron ore asset base in Europe.

- In December 2025, Latin Metals and Daura Gold activated a strategic alliance and exploration initiative at a gold-silver project in Argentina to advance geophysical exploration activities.

Report Coverage

The research report offers an in-depth analysis based on Mining Method, Mineral Type, Waste Type and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will continue to grow steadily, supported by increasing mineral production and stricter environmental regulations.

- Mining companies will integrate waste management planning more deeply into early mine design and feasibility stages.

- Adoption of advanced tailings management technologies will accelerate to improve safety and reduce environmental risks.

- Demand for mine water treatment and recycling solutions will rise due to water scarcity and regulatory pressure.

- Progressive mine rehabilitation during active operations will become a standard industry practice.

- Resource recovery and reprocessing of legacy tailings will gain importance as sustainability goals strengthen.

- Digital monitoring and automation will play a larger role in waste facility management and compliance reporting.

- Long-term post-closure management services will generate sustained demand beyond mine operational life.

- Emerging mining regions will invest more in compliant waste infrastructure as regulations mature.

- Collaboration between mining operators, service providers, and regulators will increase to ensure safer waste management practices.