Neuroendocrine Carcinoma Market Overview:

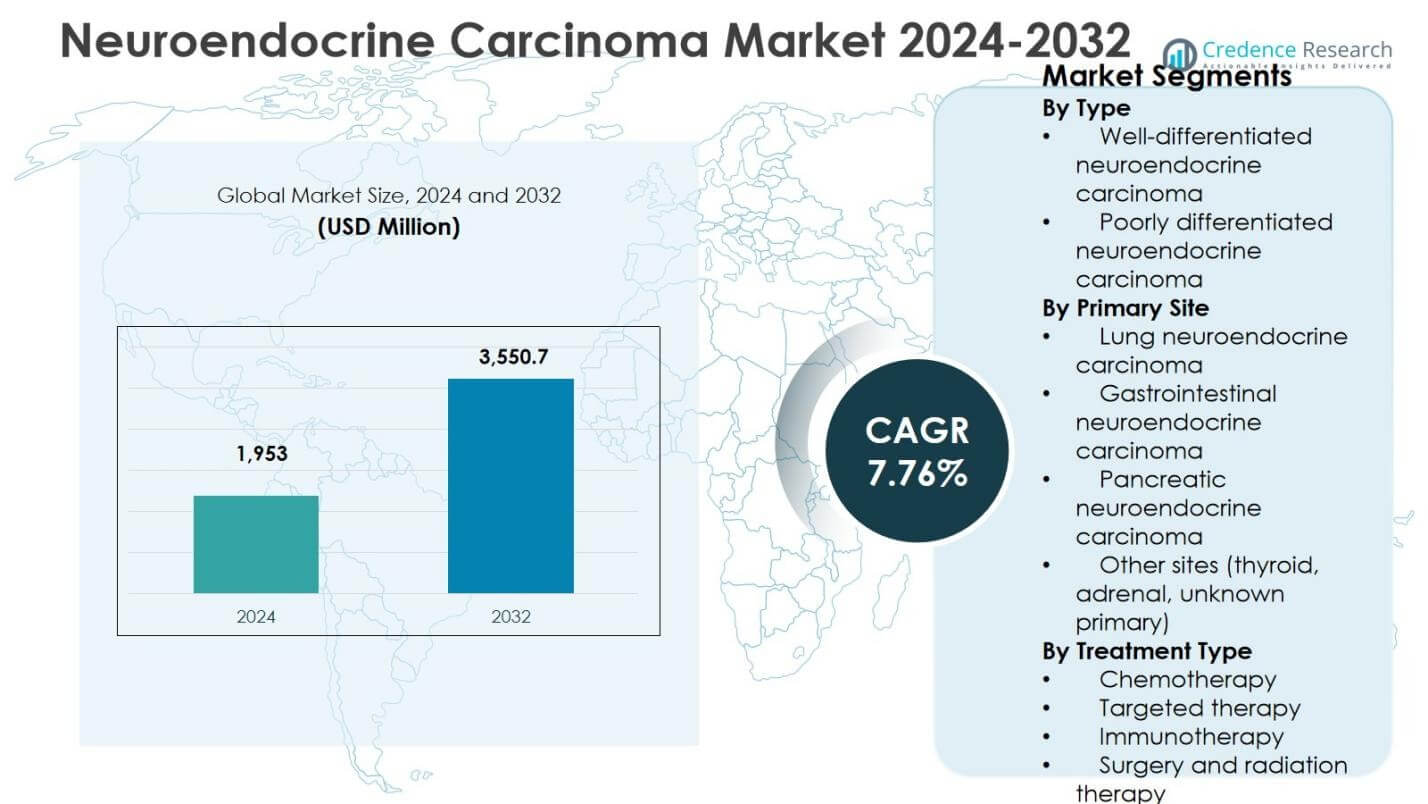

Neuroendocrine Carcinoma Market size was valued at USD 1,953 million in 2024 and is anticipated to reach USD 3,550.7 million by 2032, growing at a CAGR of 7.76% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Neuroendocrine Carcinoma Market Size 2024 |

USD 1,953 million |

| Neuroendocrine Carcinoma Market, CAGR |

7.76% |

| Neuroendocrine Carcinoma Market Size 2032 |

USD 3,550.7 million |

Neuroendocrine Carcinoma Market Insights

- Market growth is driven by increasing incidence of high-grade neuroendocrine carcinoma, improved imaging and biomarker diagnostics, and rising demand for systemic therapies, with poorly differentiated neuroendocrine carcinoma holding a 58.6% segment share in 2024 due to aggressive disease progression.

- Ongoing market trends include growing adoption of targeted therapy and immunotherapy, expansion of combination treatment regimens, and continuous clinical trial activity, while chemotherapy remains dominant with a 8% treatment share in 2024 driven by first-line usage.

- Market restraints include high treatment costs, limited reimbursement in developing economies, and disease heterogeneity, which complicates standardized treatment protocols and slows therapy optimization across patient populations.

- Regionally, North America led with 38.4% share in 2024, followed by Europe at 27.6%, Asia-Pacific at 22.1%, Latin America at 7.1%, and Middle East & Africa at 4.8%, reflecting disparities in healthcare infrastructure and access.

Market Segmentation Analysis:

By Type:

The Neuroendocrine Carcinoma Market, segmented by type, is led by poorly differentiated neuroendocrine carcinoma, which accounted for 58.6% market share in 2024, driven by its higher incidence, aggressive disease progression, and greater demand for systemic therapies. These tumors often present at advanced stages, necessitating intensive treatment regimens and prolonged clinical management. In contrast, well-differentiated neuroendocrine carcinoma holds a smaller share due to slower progression and limited therapeutic intervention intensity. Rising awareness, improved diagnostic accuracy, and increased hospitalization rates for high-grade tumors continue to support the dominance of poorly differentiated variants.

- For instance, Exelixis’ Cabometyx (cabozantinib) received FDA approval in March 2025 for previously treated, advanced, well-differentiated pancreatic and extra-pancreatic neuroendocrine tumors based on phase 3 CABINET trial data demonstrating progression-free survival improvement.

By Primary Site:

By primary site, lung neuroendocrine carcinoma dominated the market with a 41.3% share in 2024, supported by high prevalence, strong association with smoking, and frequent late-stage diagnosis. Gastrointestinal neuroendocrine carcinoma followed due to expanding screening programs and rising incidence across aging populations. Pancreatic neuroendocrine carcinoma captured a notable share owing to advancements in imaging and biomarker-based detection. Other sites, including thyroid, adrenal, and unknown primary tumors, represented a smaller portion of demand. The dominance of lung-origin tumors is reinforced by higher treatment intensity and sustained oncology drug utilization.

- For instance, Novartis offers Afinitor (everolimus), approved for progressive nonfunctional lung neuroendocrine tumors, supporting sustained drug utilization in late-stage cases.

By Treatment Type:

Based on treatment type, chemotherapy held the largest share at 46.8% in 2024, driven by its widespread use as first-line therapy for high-grade and metastatic neuroendocrine carcinoma. The segment benefits from established clinical protocols, broad availability, and reimbursement coverage across major markets. Targeted therapy followed, supported by growing adoption in well-characterized tumors with specific molecular markers. Immunotherapy showed rising uptake due to durable response rates in select patients, while surgery and radiation therapy remained adjunct options. The dominance of chemotherapy reflects its central role in managing aggressive disease forms.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Key Growth Drivers

Rising Incidence and Improved Diagnosis of Neuroendocrine Carcinoma

The Neuroendocrine Carcinoma Market benefits significantly from the rising global incidence of neuroendocrine malignancies, supported by improved diagnostic capabilities. Advances in imaging technologies, biomarker-based testing, and pathology classification systems enable earlier and more accurate detection of both well-differentiated and poorly differentiated tumors. Increased physician awareness and expanded screening for high-risk populations, particularly for lung and gastrointestinal neuroendocrine carcinoma, further strengthen diagnosis rates. Earlier detection directly increases treatment volumes and long-term disease management needs, driving sustained demand for systemic therapies and specialized oncology care.

- For instance, the NETest liquid biopsy test achieves over 90% sensitivity and up to 98% specificity in detecting neuroendocrine tumors, outperforming traditional markers like chromogranin A by enabling earlier identification through multigene expression analysis.

Expansion of Targeted and Precision Oncology Therapies

The growing adoption of targeted therapy and precision oncology approaches acts as a strong growth driver for the Neuroendocrine Carcinoma Market. Improved understanding of tumor biology, receptor expression, and molecular pathways enables personalized treatment selection, particularly for pancreatic and gastrointestinal neuroendocrine carcinoma. Pharmaceutical investments in targeted agents and combination regimens improve progression-free survival and treatment outcomes, encouraging broader clinical adoption. As treatment protocols shift toward personalized approaches, demand for advanced therapeutics continues to rise, strengthening market growth across both developed and emerging healthcare systems.

- For instance, Novartis’s Afinitor (everolimus), an mTOR inhibitor, extended median progression-free survival to 11.0 months versus 4.6 months with placebo in patients with advanced pancreatic neuroendocrine tumors in the phase III RADIANT-3 trial.

Increasing Healthcare Spending and Oncology Infrastructure

Rising healthcare expenditure and strengthening oncology infrastructure significantly support market expansion. Governments and private healthcare providers are investing in cancer treatment facilities, advanced radiotherapy systems, and specialized oncology centers. Improved reimbursement coverage for chemotherapy, targeted therapy, and immunotherapy enhances patient access to treatment. In addition, expanding insurance penetration in emerging economies increases diagnosis and treatment rates for neuroendocrine carcinoma, supporting long-term market growth through improved affordability and access to advanced cancer therapies.

Key Trends & Opportunities

Growing Adoption of Immunotherapy and Combination Regimens

The Neuroendocrine Carcinoma Market is witnessing a strong trend toward immunotherapy adoption, particularly in advanced and metastatic cases. Immune checkpoint inhibitors and combination regimens with chemotherapy or targeted therapy are gaining clinical acceptance due to improved response durability in select patient populations. Ongoing clinical trials and real-world evidence continue to validate these approaches, creating opportunities for treatment innovation. Combination therapies offer enhanced efficacy compared to monotherapy, positioning immunotherapy as a high-growth opportunity segment within the evolving neuroendocrine carcinoma treatment landscape.

- For instance, Dual immune checkpoint inhibition with ipilimumab plus nivolumab in the DART SWOG 1609 trial (NCT02834013) yielded a 44% objective response rate in high-grade neuroendocrine carcinoma patients, outperforming results in lower-grade cases.

Expansion in Emerging Markets and Unmet Clinical Needs

Emerging markets present significant growth opportunities due to improving cancer awareness, expanding diagnostic capabilities, and increasing access to oncology care. Large patient populations, rising urbanization, and government-led cancer control programs support market penetration in Asia-Pacific, Latin America, and the Middle East. Additionally, unmet clinical needs in high-grade and refractory neuroendocrine carcinoma create opportunities for novel drug development. Companies focusing on cost-effective therapies and region-specific clinical strategies are well positioned to capture long-term growth in these markets.

- For instance, Merck’s Keytruda (pembrolizumab) has gained traction in India via expedited regulatory approvals and customs duty exemptions, enabling faster patient access to immunotherapy for various cancers.

Key Challenges

Disease Heterogeneity and Complex Clinical Management

A major challenge in the Neuroendocrine Carcinoma Market is the high heterogeneity of the disease, which complicates diagnosis, treatment selection, and outcome prediction. Variability in tumor grade, differentiation, and primary site limits the effectiveness of standardized treatment protocols. Clinicians often rely on individualized treatment decisions, increasing complexity and treatment costs. This heterogeneity also slows drug development and regulatory approval processes, as clinical trials must account for diverse patient populations and disease presentations.

High Treatment Costs and Limited Access in Developing Regions

High costs associated with advanced therapies, including targeted therapy and immunotherapy, pose a significant barrier to market expansion. Limited reimbursement coverage and uneven healthcare infrastructure restrict patient access, particularly in low- and middle-income regions. The financial burden of long-term treatment and follow-up further challenges affordability. Addressing cost constraints and expanding reimbursement frameworks remain critical for improving treatment accessibility and sustaining equitable growth across the global neuroendocrine carcinoma market.

Regional Analysis

North America

The Neuroendocrine Carcinoma Market in North America accounted for 38.4% market share in 2024, supported by high disease awareness, advanced diagnostic infrastructure, and strong adoption of systemic therapies. The region benefits from early diagnosis, broad access to chemotherapy, targeted therapy, and immunotherapy, and the presence of specialized oncology centers. Favorable reimbursement policies and sustained investment in cancer research further strengthen treatment uptake. The United States drives the majority of regional demand due to high healthcare spending, robust clinical trial activity, and continuous introduction of innovative oncology therapies.

Europe

Europe represented 27.6% market share in 2024, driven by strong public healthcare systems, increasing cancer screening initiatives, and standardized treatment guidelines for neuroendocrine carcinoma. Countries such as Germany, France, and the United Kingdom contribute significantly due to advanced hospital infrastructure and access to multidisciplinary oncology care. Growing use of targeted therapies and expanding immunotherapy adoption support market growth. Government-funded cancer programs and rising investment in rare cancer research enhance early diagnosis and treatment continuity, reinforcing Europe’s position as a key contributor to global market revenues.

Asia-Pacific

Asia-Pacific captured 22.1% market share in 2024, reflecting rapid improvements in healthcare infrastructure and rising awareness of neuroendocrine carcinoma. Increasing cancer incidence, expanding diagnostic capabilities, and growing access to oncology services drive demand across China, Japan, and India. Government-led healthcare reforms and higher healthcare spending support broader adoption of chemotherapy and targeted therapies. The region also benefits from a large patient pool and improving reimbursement coverage. Expanding pharmaceutical manufacturing and clinical research activities further strengthen Asia-Pacific’s growth trajectory during the forecast period.

Latin America

Latin America accounted for 7.1% market share in 2024, supported by improving cancer care infrastructure and increasing access to oncology treatments. Brazil and Mexico lead regional demand due to rising cancer diagnosis rates and expanding hospital networks. Adoption of chemotherapy remains dominant, while targeted therapies show gradual uptake in urban healthcare centers. Public health initiatives focused on cancer awareness and early detection contribute to market development. However, uneven access to advanced therapies continues to influence treatment patterns across the region.

Middle East & Africa

The Middle East & Africa region held 4.8% market share in 2024, driven by gradual improvements in oncology infrastructure and rising healthcare investment. Gulf countries contribute a significant portion of regional demand due to modern healthcare facilities and increasing adoption of advanced cancer therapies. In Africa, limited access to diagnostic tools and treatment options restrict market penetration. Ongoing government initiatives, international collaborations, and expansion of private healthcare facilities are improving diagnosis rates and treatment availability, supporting steady market growth across the region.

Neuroendocrine Carcinoma Market Segmentations

By Type

- Well-differentiated neuroendocrine carcinoma

- Poorly differentiated neuroendocrine carcinoma

By Primary Site

- Lung neuroendocrine carcinoma

- Gastrointestinal neuroendocrine carcinoma

- Pancreatic neuroendocrine carcinoma

- Other sites (thyroid, adrenal, unknown primary)

By Treatment Type

- Chemotherapy

- Targeted therapy

- Immunotherapy

- Surgery and radiation therapy

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

Competitive landscape of the Neuroendocrine Carcinoma Market is shaped by the strong presence of Novartis AG, Pfizer Inc., Ipsen Pharma, Bristol-Myers Squibb, and F. Hoffmann-La Roche Ltd.. The market remains moderately consolidated, with leading players focusing on expanding oncology portfolios through targeted therapies, immunotherapy, and radiopharmaceutical innovations. Strategic priorities include clinical trial expansion, regulatory approvals for new indications, and combination therapy development to improve outcomes in high-grade and metastatic disease. Companies invest heavily in research collaborations and biomarker-driven treatment strategies to address disease heterogeneity. Geographic expansion into emerging markets, coupled with improved reimbursement access, further strengthens competitive positioning. Continuous pipeline development and lifecycle management of existing therapies remain critical for sustaining long-term market presence and differentiation.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Novartis AG

- Pfizer Inc.

- Ipsen Pharma

- Boehringer Ingelheim

- Eli Lilly and Company

- Bristol-Myers Squibb

- F. Hoffmann-La Roche Ltd.

- Lantheus Holdings

- AVEO Pharmaceuticals

- Hutchison MediPharma

Recent Developments

- In January 2025, Lantheus announced its planned acquisition of Life Molecular Imaging for an upfront payment of $350 million, enhancing its radiopharmaceutical capabilities including assets relevant to neuroendocrine tumor diagnostics and treatments like Octevy for PET imaging.

- In June 2025, Chimeric Therapeutics received FDA Fast Track Designation for CHM CDH17, a CAR T-cell therapy targeting CDH17 in gastroenteropancreatic neuroendocrine tumors (GEP-NETs), advancing its clinical trial for this unmet need.

- In October 2024, Boehringer Ingelheim partnered with Circle Pharma in a collaboration and license agreement worth up to $607 million to develop a first-in-class cyclin inhibitor targeting hard-to-treat cancers, potentially including neuroendocrine carcinomas.

Report Coverage

The research report offers an in-depth analysis based on Type, Primary Site, Treatment Type and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The Neuroendocrine Carcinoma Market is expected to witness sustained growth driven by increasing disease incidence and improved diagnostic accuracy.

- Advancements in molecular profiling will support wider adoption of precision and targeted treatment approaches.

- Immunotherapy is likely to gain stronger clinical acceptance, particularly in advanced and refractory neuroendocrine carcinoma cases.

- Combination treatment regimens will increasingly replace monotherapy to enhance therapeutic efficacy and survival outcomes.

- Ongoing clinical trials will expand approved indications and strengthen evidence-based treatment protocols.

- Expanding access to oncology care in emerging markets will contribute to higher diagnosis and treatment rates.

- Improved reimbursement frameworks will support broader patient access to advanced therapies.

- Technological progress in imaging and biomarker testing will enable earlier disease detection and monitoring.

- Strategic partnerships and research collaborations will accelerate innovation and pipeline development.

- Focus on personalized medicine will shape long-term treatment strategies and market evolution.