| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Ophthalmology Devices Market Size 2024 |

USD 19,158.43 million |

| Ophthalmology Devices Market, CAGR |

7.23% |

| Ophthalmology Devices Market Size 2032 |

USD 33,484.05 million |

Market Overview

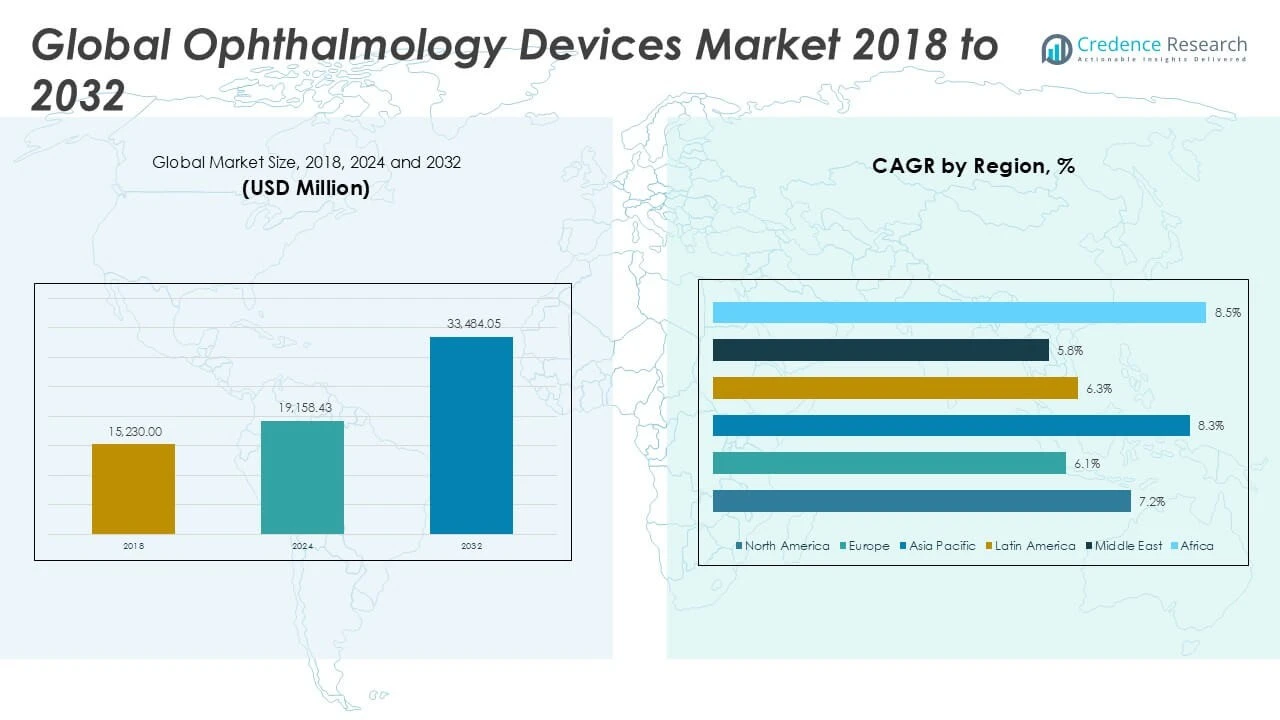

The Global Ophthalmology Devices Market is projected to grow from USD 19,158.43 million in 2024 to an estimated USD 33,484.05 million by 2032, with a compound annual growth rate (CAGR) of 7.23% from 2025 to 2032.

Key drivers propelling the ophthalmology devices market include technological advancements such as the development of minimally invasive surgical instruments, laser-based therapies, and enhanced imaging systems. The increasing incidence of cataracts, glaucoma, diabetic retinopathy, and age-related macular degeneration fuels demand for innovative treatment solutions. Furthermore, the trend toward outpatient eye care centers and growing investments by healthcare providers in ophthalmic infrastructure support market growth. Rising healthcare expenditure and improving reimbursement policies in developed and emerging economies also enhance accessibility to ophthalmology devices.

Regionally, North America holds a significant share of the ophthalmology devices market, driven by high healthcare spending and early adoption of advanced technologies. Europe follows closely, supported by well-established healthcare infrastructure and government initiatives promoting eye care awareness. The Asia-Pacific region is expected to register the fastest growth, fueled by increasing prevalence of eye diseases, growing geriatric population, and expanding healthcare access in countries such as China, India, and Japan. Leading players in this market include Alcon, Bausch + Lomb, Johnson & Johnson Vision, Carl Zeiss Meditec, and Nidek, who continue to innovate and expand their product portfolios to maintain competitive advantage.

Market Insights

- The global ophthalmology devices market is set to grow from USD 19,158.43 million in 2024 to USD 33,484.05 million by 2032, with a CAGR of 7.23% from 2025 to 2032.

- Rising incidences of cataracts, glaucoma, diabetic retinopathy, and age-related macular degeneration are driving demand for ophthalmology devices.

- Continuous innovation in minimally invasive surgical instruments, laser therapies, and advanced imaging systems is boosting market growth.

- The shift towards outpatient and ambulatory surgical centers enhances the adoption of advanced ophthalmic devices, improving patient access to care.

- Complex regulatory requirements and varying reimbursement policies across regions can slow market penetration and adoption of new technologies.

- North America holds the largest market share, followed by Europe, with Asia-Pacific expected to experience the fastest growth during the forecast period.

- Growing healthcare investments, especially in emerging markets, provide opportunities for expanding ophthalmology devices adoption in regions like Asia-Pacific and Latin America.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Prevalence of Eye Disorders and Aging Population Fuel Market Demand

The growing incidence of eye diseases such as cataracts, glaucoma, diabetic retinopathy, and age-related macular degeneration drives the demand for ophthalmology devices globally. The Global Ophthalmology Devices Market benefits from increasing vision impairment cases caused by lifestyle changes, environmental factors, and chronic conditions like diabetes. The aging population further intensifies this demand, given the higher susceptibility to eye disorders among elderly individuals. Healthcare providers focus on early diagnosis and treatment, increasing the adoption of advanced ophthalmic diagnostic and surgical equipment. Rising patient awareness about eye health promotes routine eye check-ups, which supports device utilization. Governments and organizations are promoting preventive eye care, expanding market potential in both developed and emerging regions.

- For instance, in 2024, over 661 million ophthalmic diagnostic and surgical devices were utilized in India, with government initiatives such as the National Programme for Control of Blindness (NPCB) supporting preventive eye care efforts

Technological Advancements Enhance Diagnostic Accuracy and Treatment Efficiency

Continuous innovation in ophthalmic technologies improves clinical outcomes and patient experience. The market incorporates laser-based surgical devices, optical coherence tomography, and advanced imaging systems that enable precise diagnosis and minimally invasive treatments. Manufacturers invest heavily in research and development to introduce smart and portable ophthalmology devices that facilitate outpatient procedures and teleophthalmology services. It helps healthcare providers deliver faster, safer, and more effective eye care solutions. Integration with AI and machine learning allows better disease prediction and customized treatment plans. These technological breakthroughs drive market growth by expanding the application scope and improving accessibility.

- For instance, in 2025, AI-assisted ophthalmic diagnostic tools were integrated into over 86% of teleophthalmology services in the U.S., improving early detection rates for diabetic retinopathy and glaucoma

Increasing Healthcare Expenditure and Favorable Reimbursement Policies Stimulate Adoption

Higher healthcare spending in developed countries supports infrastructure upgrades and procurement of state-of-the-art ophthalmology devices. It encourages hospitals, clinics, and specialty centers to equip themselves with the latest diagnostic and therapeutic tools. Reimbursement policies and insurance coverage improve affordability and accessibility for patients seeking eye care services. Emerging markets witness rising government investments in healthcare infrastructure and public awareness campaigns, boosting demand for ophthalmic equipment. Collaborations between device manufacturers and healthcare providers facilitate product availability and training, accelerating adoption rates. This financial and institutional support sustains consistent growth in the ophthalmology devices sector.

Shift Towards Outpatient Care Centers and Growing Patient Preference for Minimally Invasive Procedures

Healthcare systems are transitioning towards outpatient and ambulatory surgical centers to reduce costs and improve patient convenience. It propels demand for compact, portable, and easy-to-use ophthalmology devices suitable for outpatient settings. Patients increasingly prefer minimally invasive procedures that offer faster recovery, reduced risks, and less discomfort. This trend encourages providers to adopt advanced surgical instruments and laser technologies. The Global Ophthalmology Devices Market capitalizes on this shift by offering solutions that align with evolving clinical practices and patient expectations. Expansion of ambulatory centers in urban and rural areas supports market penetration and revenue growth.

Market Trends

Rapid Adoption of Minimally Invasive and Laser-Based Technologies Drives Market Transformation

The Global Ophthalmology Devices Market experiences a significant shift towards minimally invasive procedures supported by advanced laser technologies. Surgeons prefer devices that reduce operation time, enhance precision, and minimize patient discomfort. Laser-based systems, including femtosecond and excimer lasers, gain widespread use in cataract and refractive surgeries. These technologies improve clinical outcomes and allow quicker patient recovery. Manufacturers continue to innovate to provide compact, user-friendly devices suited for outpatient and ambulatory care settings. The trend favors integration of diagnostics with treatment capabilities, improving workflow efficiency in ophthalmic practices. This transformation reshapes traditional surgical approaches and fuels market expansion.

- For instance, in 2024, 126 industry reports analyzed trends in laser-assisted procedures, covering 80+ leading technology providers specializing in minimally invasive surgical solutions.

Integration of Artificial Intelligence and Digital Imaging Enhances Diagnostic and Predictive Capabilities

AI-powered diagnostic tools and advanced digital imaging technologies increasingly influence the ophthalmology devices market. It enables early detection of retinal diseases and glaucoma through automated image analysis and pattern recognition. The Global Ophthalmology Devices Market benefits from AI algorithms that improve accuracy, reduce human error, and support personalized treatment plans. Teleophthalmology platforms leverage these technologies to extend care to remote and underserved populations. Continuous data collection and machine learning improve disease management and patient monitoring. The rising application of AI enhances clinical decision-making and accelerates technology adoption across healthcare systems.

- For instance, in 2024, 61 AI-driven imaging applications, incorporating findings from 27 major studies on predictive analytics and automated disease detection.

Expansion of Teleophthalmology and Remote Patient Monitoring Accelerates Market Growth

Telemedicine in ophthalmology gains momentum due to growing demand for accessible eye care and limited specialist availability in rural regions. It supports remote screening, diagnosis, and follow-up, reducing the need for physical visits. The market integrates portable ophthalmic devices with cloud-based platforms to facilitate seamless data sharing and consultation. The Global Ophthalmology Devices Market capitalizes on this shift by offering innovative solutions compatible with telehealth infrastructure. Remote patient monitoring devices improve chronic disease management and patient compliance. Increasing digital connectivity and smartphone penetration further boost teleophthalmology adoption worldwide.

Focus on Customized and Patient-Centric Solutions Enhances Market Competitiveness

Manufacturers prioritize developing personalized ophthalmic devices that address diverse patient needs and preferences. It involves tailoring surgical instruments, intraocular lenses, and diagnostic tools to individual anatomical and pathological variations. The Global Ophthalmology Devices Market witnesses growing demand for user-friendly interfaces and ergonomic designs that improve clinician efficiency and patient comfort. Customized solutions support better surgical outcomes and reduce complication rates. Partnerships with healthcare providers enable product co-creation and iterative improvements. This patient-centric approach strengthens brand loyalty and differentiates companies in a competitive landscape.

Market Challenges

High Costs of Advanced Ophthalmic Devices and Limited Accessibility in Emerging Markets Impede Growth

The Global Ophthalmology Devices Market faces challenges due to the high costs associated with cutting-edge technologies and equipment. These expenses limit adoption, particularly in developing regions with constrained healthcare budgets. It restricts access to advanced diagnostic and surgical solutions for a significant patient population. Procurement and maintenance costs further burden smaller clinics and outpatient centers. Variability in reimbursement policies across countries adds complexity to market penetration efforts. Manufacturers must balance innovation with affordability to expand their customer base. This financial barrier slows market growth and creates disparities in eye care quality worldwide.

- For instance, over 54 million ophthalmic procedures were performed globally in 2024, highlighting the growing demand for advanced eye care solutions

Regulatory Compliance Complexities and Skilled Workforce Shortages Hinder Market Expansion

Strict regulatory requirements and lengthy approval processes delay the launch of new ophthalmology devices and increase development costs. The Global Ophthalmology Devices Market must navigate diverse regulations across different regions, complicating global commercialization. Compliance demands rigorous testing and documentation, posing challenges for smaller players. Meanwhile, shortages of trained ophthalmologists and technicians limit effective device utilization and patient outreach. It restricts the full potential of innovative technologies in clinical practice. Investment in workforce training and streamlined regulatory pathways remain critical to overcoming these obstacles. These factors collectively slow the pace of market adoption and technological advancement.

Market Opportunities

Expanding Geriatric Population and Rising Prevalence of Chronic Eye Diseases Create Significant Growth Potential

The Global Ophthalmology Devices Market can capitalize on the increasing number of elderly individuals who face a higher risk of vision-related disorders. It presents opportunities for developing specialized diagnostic and therapeutic devices tailored to age-related conditions like cataracts, glaucoma, and macular degeneration. Growing awareness about eye health and early intervention further supports demand for innovative solutions. Healthcare providers seek efficient and accurate tools to manage chronic diseases, driving market expansion. Investments in preventive care and screening programs offer additional avenues for device adoption. Emerging economies with improving healthcare infrastructure provide untapped markets for growth. This demographic trend sustains long-term demand and encourages continuous innovation.

Advancements in Digital Health Technologies and Teleophthalmology Enable Market Penetration in Underserved Areas

Integration of digital health solutions, artificial intelligence, and telemedicine in ophthalmology creates new opportunities for remote diagnosis and treatment. The Global Ophthalmology Devices Market benefits from rising adoption of portable and connected devices that facilitate access to quality eye care in rural and underserved regions. It supports efficient patient monitoring and management, reducing the burden on specialized centers. Partnerships with telehealth providers and healthcare systems enable broader deployment of these technologies. Increasing smartphone penetration and internet connectivity expand teleophthalmology’s reach globally. This trend drives product innovation and market diversification, offering significant growth prospects for device manufacturers.

Market Segmentation Analysis

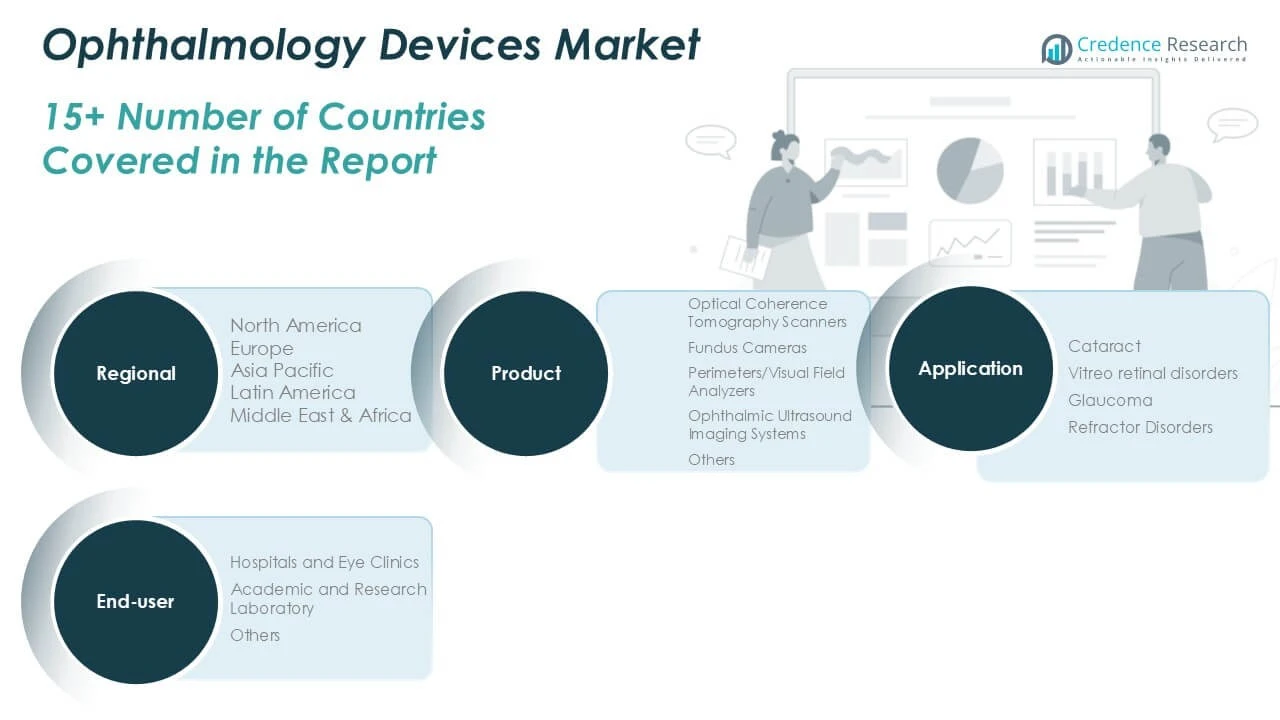

By Product

The Global Ophthalmology Devices Market is divided into several key product segments, each contributing significantly to the overall market growth. Optical coherence tomography (OCT) scanners dominate this segment due to their advanced imaging capabilities, allowing detailed cross-sectional imaging of the retina and optic nerve, essential for diagnosing and monitoring retinal diseases. Fundus cameras follow closely, aiding in the diagnosis of eye conditions like diabetic retinopathy and macular degeneration. Perimeters/visual field analyzers are crucial for glaucoma diagnosis and management, as they assess the patient’s visual field. Ophthalmic ultrasound imaging systems also hold a substantial share due to their non-invasive nature and ability to detect various eye conditions. Other products, including diagnostic and surgical instruments, contribute to the market as well.

By Application

The ophthalmology devices market is primarily driven by applications such as cataract treatment, vitreo-retinal disorders, glaucoma, and refractive disorders. Cataract treatments hold the largest market share due to the high incidence of cataracts globally, particularly in the aging population. Vitreo-retinal disorders also represent a significant market due to the rise in conditions like diabetic retinopathy and age-related macular degeneration. Glaucoma remains a key focus area, with increasing adoption of devices for its early detection and management. Refractive disorders, including myopia and hyperopia, also drive demand for diagnostic devices and treatment technologies.

By End-User

Hospitals and eye clinics hold the largest share in the end-user segment, as they are the primary healthcare settings for ophthalmic treatments and surgeries. Academic and research laboratories also play a crucial role in advancing ophthalmic technology and supporting clinical trials. Other end-users include outpatient clinics, diagnostic centers, and private practices, all contributing to the adoption of ophthalmology devices through diagnostic, therapeutic, and surgical procedures.

Segments

Based on Product

- Optical Coherence Tomography Scanners

- Fundus Cameras

- Perimeters/Visual Field Analysers

- Ophthalmic Ultrasound Imaging Systems

- Others

Based on Application

- Cataract

- Vitreo retinal disorders

- Glaucoma

- Refractor Disorders

Based on End-user

- Hospitals and Eye Clinics

- Academic and Research Laboratory

- Others

Based on Region

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America Ophthalmology Devices Market

The North American ophthalmology devices market is poised to grow from USD 6,777.66 million in 2024 to USD 11,813.98 million by 2032, with a compound annual growth rate (CAGR) of 7.2%. It holds the largest regional market share, accounting for approximately 35% of the global market. This dominance is driven by advanced healthcare infrastructure, high adoption of innovative technologies, and significant healthcare spending. The U.S. leads the market in this region, supported by a well-established ophthalmology care system and increasing demand for advanced diagnostic and surgical devices. Rising awareness of eye health, coupled with an aging population, further accelerates market growth. The presence of key market players, including Alcon and Johnson & Johnson Vision, strengthens the competitive landscape in North America. Regulatory support and favorable reimbursement policies further boost the adoption of ophthalmology devices.

Europe Ophthalmology Devices Market

Europe’s ophthalmology devices market is expected to grow from USD 3,721.96 million in 2024 to USD 5,969.29 million by 2032, registering a CAGR of 6.1%. It commands a substantial regional market share of around 20%. The region’s strong healthcare systems, widespread access to eye care technologies, and rising incidence of eye disorders contribute significantly to its market share. Countries like Germany, France, and the U.K. lead the European market. The aging population in these regions, particularly the growing number of people affected by age-related macular degeneration and cataracts, further supports market growth. European regulations for ophthalmology devices are favorable, ensuring the safety and efficacy of new technologies. The strong focus on research and development enables the region to remain competitive.

Asia Pacific Ophthalmology Devices Market

The Asia Pacific ophthalmology devices market is projected to grow from USD 5,897.84 million in 2024 to USD 11,118.37 million by 2032, with a CAGR of 8.3%. It is the fastest-growing regional market, contributing approximately 30% to the global market share. The region’s market share is expanding rapidly, fueled by the increasing prevalence of eye diseases and improving healthcare infrastructure in countries like China, India, and Japan. The growing aging population, rising disposable incomes, and government initiatives to enhance healthcare access further boost market demand. Technological advancements and the adoption of minimally invasive ophthalmic procedures are transforming the treatment landscape. The Asia Pacific region’s market share continues to rise, playing a pivotal role in the global ophthalmology devices market.

Latin America Ophthalmology Devices Market

The Latin American ophthalmology devices market is expected to grow from USD 1,499.91 million in 2024 to USD 2,441.99 million by 2032, at a CAGR of 6.3%. It holds a regional market share of approximately 8%. Brazil, Mexico, and Argentina are the primary contributors to market growth. Rising healthcare investments, expanding healthcare access, and the increasing incidence of age-related eye disorders drive demand for ophthalmic devices. As the region’s population ages, the demand for advanced ophthalmology devices rises, particularly for cataract treatments and retinal disease management. The Latin American market share continues to increase, supported by favorable economic conditions and healthcare reforms. Government initiatives to improve healthcare infrastructure enhance access to modern ophthalmic technologies.

Middle East Ophthalmology Devices Market

The Middle East ophthalmology devices market is expected to grow from USD 743.22 million in 2024 to USD 1,165.03 million by 2032, with a CAGR of 5.8%. It holds a smaller regional market share of around 4%. However, the region is showing steady growth driven by improving healthcare facilities in countries like Saudi Arabia, the UAE, and Qatar. Rising awareness of eye health, coupled with a growing aging population, drives the demand for ophthalmic devices. Expanding private healthcare infrastructure and increasing disposable incomes support market growth in the region. The Middle East’s market share remains moderate, but its growth prospects are strong due to ongoing healthcare reforms and investments in modern medical technologies.

Africa Ophthalmology Devices Market

The Africa ophthalmology devices market is projected to grow from USD 517.83 million in 2024 to USD 975.40 million by 2032, with a CAGR of 8.5%. It holds a smaller regional market share of about 3%. However, it is experiencing significant growth due to the increasing prevalence of eye diseases and growing awareness of eye health. Countries such as South Africa, Nigeria, and Egypt contribute to market growth, driven by improving healthcare infrastructure and rising demand for ophthalmic treatments. Efforts to combat avoidable blindness, particularly in rural areas, are further stimulating the market. The Africa market share is increasing steadily as the region invests in healthcare access and eye care technologies.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key players

- Johnson & Johnson Vision Care

- Alcon Vision LLC

- Carl Zeiss Meditec AG

- Bausch & Lomb Incorporated

- Essilor International S.A

- Ziemer Ophthalmic Systems Ltd

- Nidek Co. Ltd

- TOPCON Corporation

- Haag-Streit Group

- Glaukos Corporation

Competitive Analysis

The Ophthalmology Devices Market is highly competitive, with leading players striving to innovate and expand their product offerings. Johnson & Johnson Vision Care and Alcon Vision LLC lead in market share, with a broad range of advanced diagnostic and surgical devices. Companies like Carl Zeiss Meditec AG and Bausch & Lomb Incorporated strengthen their presence by introducing cutting-edge technologies in optical coherence tomography and cataract surgery. Essilor International and Nidek Co. Ltd. focus on optical lenses and laser technologies, catering to growing refractive disorder treatments. Ziemer Ophthalmic Systems Ltd and Haag-Streit Group are known for their specialized ultrasound and diagnostic systems. Glaukos Corporation leads in the glaucoma segment, providing advanced surgical options. The market is increasingly driven by technological advancements, partnerships, and strategic acquisitions as companies focus on expanding their global footprint and product offerings.

Recent Developments

- In April 2025, Carl Zeiss Meditec AG announced that over 2 million cataract surgeries had been digitally planned using the ZEISS VERACITY Surgery Planner, highlighting the growing adoption of digital workflows in ophthalmology.

- In May 2025, Bausch & Lomb Incorporated received European CE Mark approval for its preloaded LuxLife® Full Range of Vision Intraocular Lens, enhancing its portfolio of surgical eye care solutions.

- In January 2025, Nidek Co. Ltd launched the AutoTint automated dry laser tinting system, expanding its range of ophthalmic device offerings.

Market Concentration and Characteristics

The Ophthalmology Devices Market is moderately concentrated, with a few key players holding substantial market share. Leading companies like Johnson & Johnson Vision Care, Alcon Vision LLC, and Carl Zeiss Meditec AG dominate the market due to their extensive product portfolios, advanced technologies, and strong global presence. The market is characterized by continuous innovation, especially in diagnostic imaging, cataract treatment, and refractive disorder solutions. Players focus on strategic collaborations, acquisitions, and product advancements to maintain a competitive edge. Despite the dominance of a few large players, smaller companies specializing in niche technologies and customized solutions contribute to market diversity. The increasing demand for minimally invasive procedures and teleophthalmology solutions further drives market evolution. This competitive landscape fosters a dynamic environment where both established and emerging companies work to address the growing global need for advanced ophthalmic care.

Report Coverage

The research report offers an in-depth analysis based on Product, Application, End-user and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The growing prevalence of eye diseases, especially age-related macular degeneration and diabetic retinopathy, will drive demand for advanced diagnostic devices like optical coherence tomography (OCT) and fundus cameras.

- Innovations in laser-based surgical devices and minimally invasive techniques will continue to shape the future of ophthalmology, making procedures quicker and safer for patients.

- The rise of telemedicine and teleophthalmology will provide more remote access to eye care, particularly in underserved regions, improving healthcare accessibility and patient outcomes.

- With an aging global population, the demand for ophthalmology devices will increase, particularly for treatments related to cataracts, glaucoma, and other age-related vision disorders.

- The expansion of healthcare infrastructure and rising disposable incomes in emerging markets, such as India and China, will contribute to significant growth in the ophthalmology devices market.

- There will be a growing focus on customized ophthalmology devices, catering to individual patient needs, offering more personalized treatment options for various eye disorders.

- Governments and healthcare organizations will increasingly promote preventive eye care and regular screenings, leading to higher demand for diagnostic equipment and early-stage treatments.

- AI and machine learning will enhance the diagnostic capabilities of ophthalmology devices, enabling faster, more accurate identification of conditions such as glaucoma and retinal diseases.

- Minimally invasive procedures will continue to gain popularity due to shorter recovery times and reduced risks, driving demand for specialized devices such as laser systems and surgical tools.

- To maintain a competitive edge, leading players in the ophthalmology devices market will pursue strategic partnerships, collaborations, and acquisitions to expand their product portfolios and reach new markets.