Market Overview

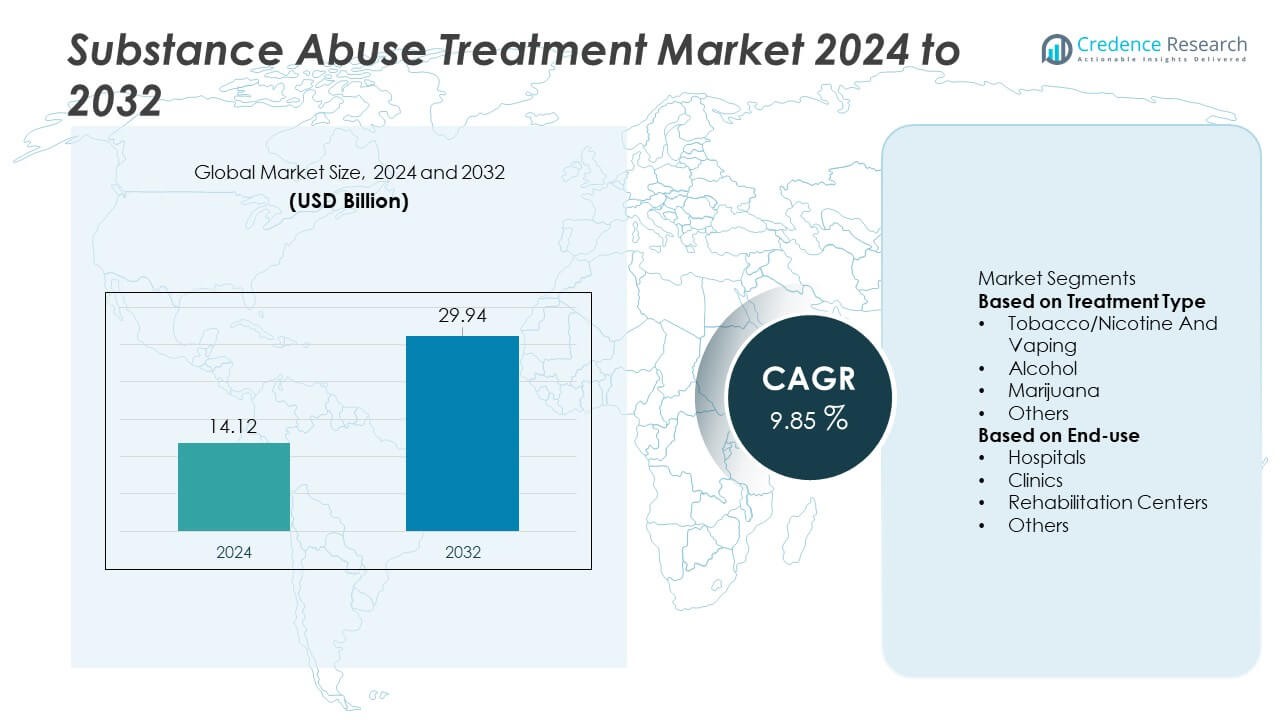

The Substance Abuse Treatment Market reached USD 14.12 billion in 2024. The market is projected to increase to USD 29.94 billion by 2032, supported by a CAGR of 9.85% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Substance Abuse Treatment Market Size 2024 |

USD 14.12 Billion |

| Substance Abuse Treatment Market, CAGR |

9.85% |

| Substance Abuse Treatment Market Size 2032 |

USD 29.94 Billion |

The top players in the Substance Abuse Treatment market include Teva Pharmaceutical Industries Ltd., Abbott, GSK plc, Cipla Inc., Lilly, Novartis AG, Sun Pharmaceutical Industries Ltd., Dr. Reddy’s Laboratories Ltd., Viatris Inc., and AstraZeneca. These companies strengthen their presence through expanded medication-assisted treatment portfolios, wider global distribution, and continued investment in safer, clinically proven therapies. North America leads the market with a 41% share, driven by strong healthcare infrastructure, advanced treatment adoption, and supportive insurance coverage. Europe and Asia Pacific follow, supported by expanding rehabilitation networks and rising awareness programs that increase treatment demand across diverse patient groups.

Market Insights

- The Substance Abuse Treatment market reached USD 14.12 billion in 2024 and will grow at a CAGR of 9.85 percent through 2032, driven by rising treatment demand across major regions.

- Growing awareness, expanding rehabilitation programs, and broader insurance coverage strengthen market drivers, with tobacco and nicotine treatment leading the segment with a 38 percent share.

- Digital therapy platforms, remote counseling services, and increasing adoption of medication-assisted treatment shape key market trends, improving patient engagement and long-term recovery outcomes.

- Strong competition among Teva, Abbott, GSK, Cipla, Lilly, Novartis, Sun Pharma, Dr. Reddy’s, Viatris, and AstraZeneca influences innovation, while persistent relapse rates and limited access in rural regions remain major restraints.

- North America leads regional growth with a 41 percent share, followed by Europe at 29 percent and Asia Pacific at 21 percent, while rehabilitation centers dominate end-use demand with a 42 percent market share.

Market Segmentation Analysis:

By Treatment Type

Tobacco/Nicotine and Vaping treatment holds the lead with a 38% market share, driven by rising dependence on e-cigarettes and stricter anti-smoking policies. Demand for counseling programs, nicotine replacement therapies, and digital cessation platforms continues to rise. Alcohol treatment follows due to higher relapse rates and increased screening in primary healthcare. Marijuana dependence programs expand as usage climbs among young adults. Other treatment types address opioids and prescription drug misuse, supported by wider adoption of medication-assisted therapy. Growth in all categories connects to better awareness and improved access to structured intervention services.

- For instance, Pfizer reported that its smoking cessation drug Chantix was prescribed to more than 24 million patients worldwide before discontinuation, showing historic clinical-scale adoption.

By End-use

Rehabilitation centers dominate the market with a 42% share, supported by higher patient intake, long-term care programs, and broader insurance coverage for addiction treatment. These centers offer structured detox, therapy, and aftercare services that drive strong adoption. Hospitals follow due to their role in emergency care and detox stabilization, while clinics gain traction with outpatient counseling and early-stage interventions. Other end-use settings include community programs and telehealth platforms that expand access in remote areas. Rising substance misuse rates and policy support sustain the segment growth across all end-use categories.

- For instance, Acadia Healthcare operates more than 250 treatment facilities and serves over 75,000 patients each year, showing high inpatient demand.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Key Growth Drivers

Rising Prevalence of Substance Dependence

Substance dependence continues to rise across tobacco, alcohol, opioids, and emerging recreational drugs, pushing demand for structured treatment programs. Higher addiction rates among young adults, growing vaping-associated disorders, and increased relapse cases drive wider adoption of intervention and rehabilitation services. Governments invest in awareness campaigns and early-stage screening programs to reduce untreated cases. Healthcare systems also expand behavioral therapy access and medication-assisted treatments. These developments strengthen the market outlook and position treatment providers to support a growing patient base with more personalized care pathways.

- For instance, Indivior documented more than 190,000 patients receiving its buprenorphine-based therapies through certified treatment centers in a single year.

Broader Insurance Coverage and Government Support

Insurance expansion for addiction care and rising public funding boost treatment accessibility. Many regions now mandate coverage for detoxification, counseling, and long-term rehabilitation under national health schemes. Grants and public subsidies support new rehabilitation centers and digital therapy platforms. Policymakers also promote early detection programs within schools and community setups. As financial barriers reduce, more individuals seek timely intervention, leading to higher treatment enrollments. This shift improves continuity of care and encourages healthcare providers to enhance service capacity and treatment quality.

- For instance, UnitedHealth Group, through its Optum division, operates a 24-hour Substance Use Helpline (1-855-780-5955) to provide confidential support, guidance on treatment options, and help in finding network providers to individuals and their families.

Growing Adoption of Medication-Assisted Treatment (MAT)

Medication-assisted treatment gains strong traction due to its proven effectiveness in reducing withdrawal symptoms and relapse rates. Demand increases for therapies involving buprenorphine, methadone, and naltrexone as regulatory bodies approve wider clinical use. Clinics and rehabilitation centers integrate MAT into combined care models that include behavioral therapy and long-term monitoring. Expanding manufacturer investments in safer, formulation-controlled drugs boost supply reliability. The rising shift toward evidence-based treatment enhances patient outcomes and supports market expansion for structured and medically supervised programs.

Key Trends & Opportunities

Expansion of Digital and Remote Addiction Treatment Platforms

Telehealth-based counseling, remote monitoring, and app-based recovery tools gain momentum as patients seek flexible and private treatment pathways. Virtual therapy sessions reduce travel barriers and provide real-time support, especially in rural areas. Digital tools also include relapse-prevention alerts, habit-tracking dashboards, and AI-enabled behavioral assessments. Providers partner with technology firms to expand hybrid care models that blend physical visits with online follow-ups. Strong adoption of remote systems opens new opportunities for scalable treatment delivery and broader patient engagement.

- For instance, in the third quarter of 2025, Talkspace recorded approximately 120,600 unique active payor members using its remote therapy platform. The company has also reported having worked with over a million clients total over its lifetime.

Growing Focus on Youth Prevention and Early Intervention Programs

Early intervention programs targeting adolescents and young adults expand as substance misuse increases in educational and social settings. Schools adopt structured awareness modules and mental-health support systems to reduce high-risk behaviors. Healthcare providers offer early screening kits, digital behavior assessments, and youth-focused rehabilitation tracks. Parents and communities show higher participation in prevention campaigns, strengthening demand for supportive services. This trend creates significant opportunities for specialized treatment programs tailored to younger demographics, promoting long-term recovery and reducing relapse rates.

- For instance, CADCA trains over 1,000 youth a year through its National Youth Leadership Initiative (NYLI) programs, which focus on fostering leadership in the design, implementation, and evaluation of strategies addressing community substance use problems.

Key Challenges

Persistent Treatment Gaps and Low Diagnosis Rates

Despite rising addiction cases, many individuals remain untreated due to stigma, lack of awareness, and limited screening. Delayed diagnosis reduces treatment effectiveness and increases relapse risk. Rural and underserved regions face shortages of specialized providers and rehabilitation centers, widening the care gap. Cultural barriers and misconceptions about therapy also discourage timely intervention. These factors limit market penetration and require stronger public education, community support systems, and early detection programs to bridge the treatment divide.

High Relapse Rates and Limited Long-Term Support Systems

Relapse remains a major challenge across alcohol, tobacco, and opioid dependence due to psychological triggers, stress, and inconsistent follow-up care. Many treatment programs struggle to maintain long-term patient engagement, especially after discharge from rehabilitation. Limited access to ongoing counseling, community support networks, and digital monitoring tools increases the risk of recurrence. This challenge highlights the need for integrated care models combining behavioral therapy, medication-assisted treatment, and continued aftercare. Strengthening long-term recovery frameworks remains essential for improving patient outcomes and market stability.

Regional Analysis

North America

North America leads the Substance Abuse Treatment market with a 41% share, driven by high addiction rates involving opioids, alcohol, and vaping products. Strong healthcare infrastructure, supportive insurance policies, and early adoption of medication-assisted treatment strengthen regional growth. Government initiatives target opioid misuse through stricter prescription controls and expanded rehabilitation coverage. Digital therapy platforms also gain traction among younger patients. Rising public awareness, wider screening programs, and active participation from community health centers reinforce the dominance of the region across all treatment categories.

Europe

Europe holds a 29% market share, supported by structured national addiction programs and strong regulatory frameworks targeting alcohol, tobacco, and drug dependence. Countries enhance treatment access through publicly funded rehabilitation centers and integrated mental-health services. The region experiences rising demand for behavioral therapies, outpatient clinics, and MAT solutions. Technological adoption increases, with digital–health platforms improving patient engagement and remote monitoring. Growing awareness campaigns and cross-border health policies further support sustained demand for evidence-based addiction treatment across key European markets.

Asia Pacific

Asia Pacific accounts for a 21% share, driven by rising alcohol consumption, tobacco dependence, and increasing misuse of prescription drugs in emerging economies. Expanding healthcare investment, urbanization, and rising mental-health awareness enhance treatment adoption. Governments integrate addiction services into primary healthcare and expand community-level rehabilitation programs. Private clinics and digital therapy platforms also gain traction as younger populations seek accessible treatment options. Growing public health initiatives and improved regulatory oversight strengthen long-term demand for structured addiction management across the region.

Latin America

Latin America holds a 6% market share, supported by gradual expansion of rehabilitation services and increasing efforts to control alcohol and drug misuse. Public health systems promote early detection and counseling programs, while NGOs support community-based recovery initiatives. Urban centers show rising adoption of MAT and outpatient therapy for alcohol and cocaine dependence. Limited healthcare resources in rural areas remain a challenge, but regional investment in mental-health infrastructure improves access. Strengthening government policies and awareness campaigns support steady market growth.

Middle East & Africa

The Middle East & Africa region represents a 3% market share, with growth driven by rising awareness of substance-related disorders and improving healthcare access. Governments expand rehabilitation centers and enforce stricter regulations on illicit drug use. Urban regions show increasing adoption of behavioral therapy and structured detox programs, while community clinics support early-stage interventions. International collaborations enhance training and treatment standards. Despite limited resources in several countries, expanding public health investment and social-awareness initiatives contribute to growing acceptance of addiction treatment services.

Market Segmentations:

By Treatment Type

- Tobacco/Nicotine And Vaping

- Alcohol

- Marijuana

- Others

By End-use

- Hospitals

- Clinics

- Rehabilitation Centers

- Others

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape features major players such as Teva Pharmaceutical Industries Ltd., Abbott, GSK plc, Cipla Inc., Lilly, Novartis AG, Sun Pharmaceutical Industries Ltd., Dr. Reddy’s Laboratories Ltd., Viatris Inc., and AstraZeneca. These companies expand their presence through advanced medication-assisted treatment portfolios, wider distribution networks, and strategic partnerships with healthcare providers. Manufacturers focus on developing safer formulations for nicotine, opioid, and alcohol dependence while strengthening regulatory approvals across key regions. Many players invest in digital adherence tools and patient-support programs to enhance treatment continuity. Rising demand for evidence-based therapies encourages firms to scale production capacity and diversify treatment options. Collaboration with rehabilitation centers and telehealth platforms also increases patient reach. Overall, continuous innovation and improved treatment accessibility drive stronger competition across the global market.

Key Player Analysis

- Sun Pharmaceutical Industries Ltd.

- AstraZeneca

- Cipla Inc.

- Novartis AG

- Viatris Inc.

- Abbott

- Reddy’s Laboratories Ltd.

- GSK plc.

- Teva Pharmaceutical Industries Ltd.

- Lilly (Eli Lilly and Company)

Recent Developments

- In November 2025, Sun Pharmaceutical Industries Ltd. did recall its ADHD drug Lisdexamfetamine in the U.S.

- In November 2024, AstraZeneca terminated the Phase II trial of its anti-addiction candidate AZD4041, aimed at treating opioid use disorder.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage

The research report offers an in-depth analysis based on Treatment Type, End-use and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Treatment adoption will rise as awareness programs and early screening efforts expand.

- Digital therapy platforms will grow as patients prefer flexible and remote support options.

- Medication-assisted treatment use will increase due to stronger clinical outcomes.

- Rehabilitation centers will enhance long-term care programs to reduce relapse rates.

- Governments will strengthen regulations to curb substance misuse across major regions.

- Youth-focused prevention programs will expand as dependence among young adults increases.

- AI-enabled monitoring tools will support personalized therapy and continuous recovery tracking.

- Collaboration between pharma companies and treatment providers will accelerate therapy innovation.

- Insurance coverage for addiction treatment will widen across public and private systems.

- Emerging markets will invest more in rehabilitation infrastructure to improve treatment access.