| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| U.S. Honey Powder market Size 2024 |

USD 240.1 million |

| U.S. Honey Powder market, CAGR |

3.47% |

| U.S. Honey Powder market Size 2032 |

USD 316.0 million |

Market Overview:

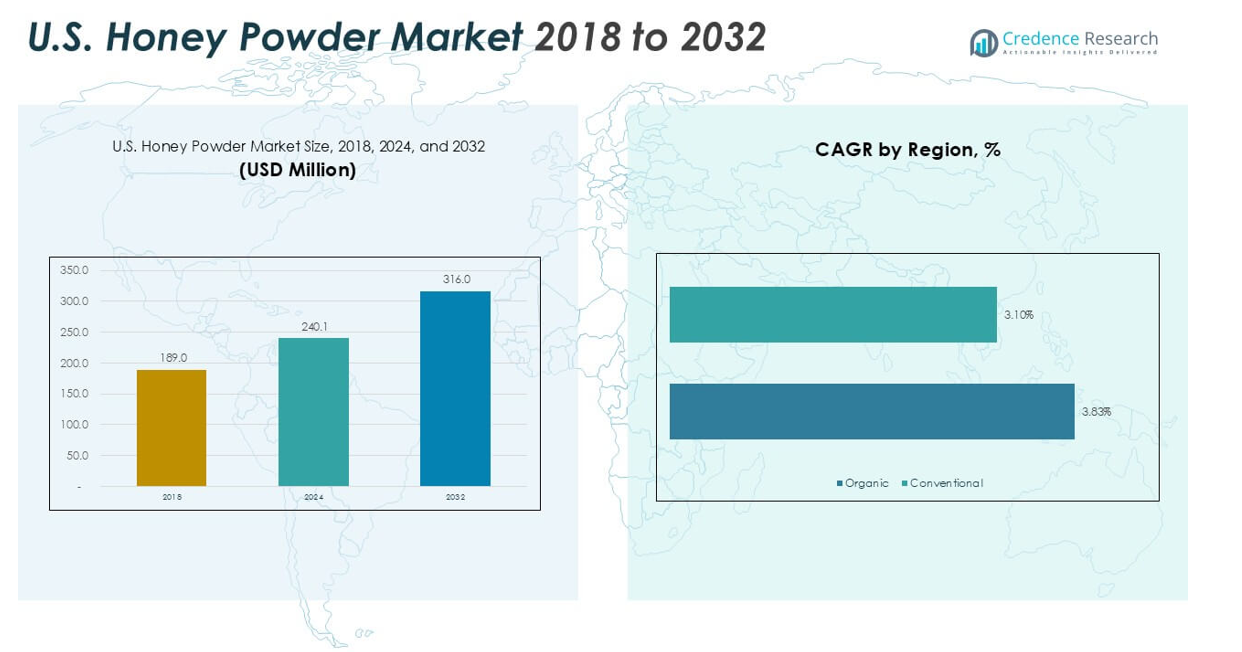

The U.S. Honey Powder market size was valued at USD 189.0 million in 2018 and reached USD 240.1 million in 2024. It is anticipated to reach USD 316.0 million by 2032, registering a compound annual growth rate (CAGR) of 3.47% during the forecast period.

The U.S. Honey Powder market features several top-tier players capturing significant share through scale, product innovation, and regional alignment. Cargill leads with approximately 15% market share, followed by ADM at 12%, reflecting their dominant position in large-scale production, R&D, and pan‑U.S. distribution. Among U.S. regions, the Western United States is the primary demand center due to its thriving food-processing infrastructure and organic market strength, closely trailed by the Midwest, South, and Northeast. These companies optimize regional capacities and logistics to capitalize on varying consumer preferences, emphasizing clean-label, organic, and traceable honey powder formats to maintain leadership across food, nutraceutical, and personal care sectors.

Market Insights

- The U.S. Honey Powder market was valued at USD 240.1 million in 2024 and is projected to reach USD 316.0 million by 2032, registering a CAGR of 3.47% during the forecast period.

- Demand is driven by increasing consumer preference for natural sweeteners, clean-label ingredients, and functional food additives in food, beverage, and nutraceutical applications.

- Trends include rising adoption of organic honey powder, a shift toward online sales channels, and product innovation targeting health-conscious and specialty markets.

- The market remains competitive with major players such as Cargill and ADM together accounting for about 27% share, while challenges include volatility in raw honey supply and competition from alternative sweeteners.

- Regionally, the Western U.S. leads with around 34% market share, followed by the Midwest at 28%, South at 23%, and Northeast at 15%; by product type, the conventional segment dominates due to its affordability and broad usage.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

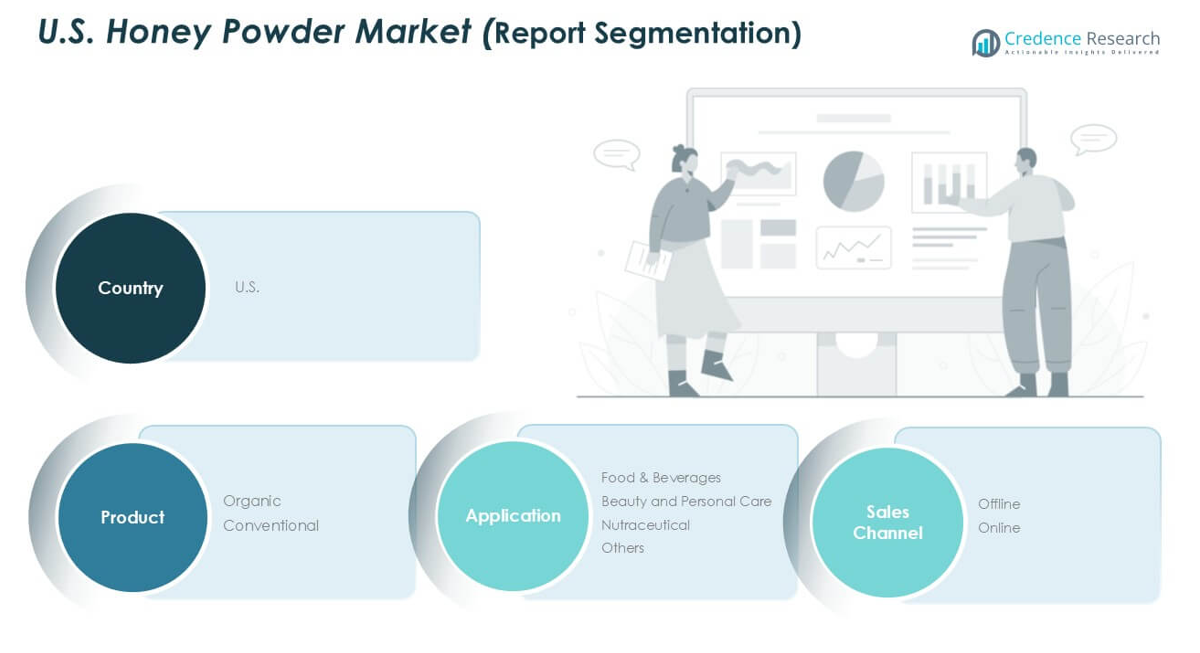

Market Segmentation Analysis:

By Product Type:

Within the U.S. Honey Powder market, the conventional segment holds the largest market share, accounting for a significant portion of total revenue. Conventional honey powder benefits from widespread availability and competitive pricing, making it the preferred choice among food manufacturers and industrial users. Although organic honey powder has gained attention due to rising consumer interest in clean-label and natural products, its adoption remains limited by higher costs and stricter certification requirements. The dominance of conventional honey powder is driven by cost-effectiveness and established distribution networks.

- For instance, ADM’s Decatur, Illinois facility has a dedicated production capacity of 1,250 metric tons of conventional honey powder annually, serving major North American food manufacturers.

By Application:

The food & beverages segment dominates the application category in the U.S. Honey Powder market, holding the largest revenue share. Food and beverage manufacturers rely heavily on honey powder as a natural sweetener and flavor enhancer, leveraging its extended shelf life and ease of incorporation into various products. The segment’s growth is supported by increasing demand for clean-label ingredients and sugar alternatives in baked goods, confectionery, and ready-to-eat products. The food & beverages application continues to outperform others due to consumer preference for healthier, naturally sourced ingredients.

- For instance, Cargill states that it supplies honey powder to over 100 food processing plants across the U.S. and includes the ingredient in at least 85 separate product formulations in the U.S. market.

By Sales Channel:

Offline sales channels represent the dominant segment in the U.S. Honey Powder market, capturing a major share of total sales. Distributors, specialty ingredient suppliers, and wholesalers ensure robust product availability to commercial buyers and large-scale users. The preference for offline channels persists due to the established business relationships and bulk purchasing options they offer. However, the online segment is experiencing steady growth, supported by the expanding reach of e-commerce and demand for direct-to-consumer purchasing. The dominance of offline channels is driven by efficient supply chains and industry trust in traditional procurement methods.

Market Overview

Expanding Demand for Natural Sweeteners

Rising consumer awareness of the health risks associated with refined sugar is driving increased adoption of honey powder as a natural sweetener. Food and beverage manufacturers leverage honey powder’s clean-label appeal, extended shelf life, and ease of formulation in various products. The trend toward reducing artificial additives and promoting healthier diets positions honey powder as a desirable alternative, fueling its demand in packaged foods, beverages, and health-conscious product lines across the U.S.

- For example, Nestlé USA revealed in a recent ingredient disclosure that honey powder is now included in 47 product SKUs ranging from granola bars to instant cereals.

Growth in Functional Food and Nutraceutical Markets

The growing interest in functional foods and nutraceuticals boosts the use of honey powder for its antioxidant and antimicrobial properties. Manufacturers incorporate honey powder into supplements, meal replacements, and health snacks to cater to consumers seeking added wellness benefits. The ingredient’s natural origin and nutritional profile support product differentiation in an increasingly competitive market, further strengthening its presence within health-focused categories and expanding its use beyond traditional food and beverage applications.

- For instance, NOW Foods has launched 14 new supplements and wellness products in 2022 and 2023 that feature honey powder as a functional ingredient.

Rising Popularity in Beauty and Personal Care Applications

Honey powder is gaining traction in the beauty and personal care sector due to its moisturizing and antibacterial properties. Formulators use it in skincare and haircare products, appealing to consumers who prioritize natural, effective ingredients. The trend toward clean beauty and organic formulations accelerates this shift, with honey powder offering both functional benefits and a compelling marketing story. This driver broadens the market’s scope and enhances its growth prospects across non-food industries.

Key Trends & Opportunities

Expansion of Clean-Label and Organic Product Lines

The U.S. Honey Powder market is witnessing a surge in clean-label and organic product offerings. Brands capitalize on consumer preferences for transparency, minimal processing, and sustainable sourcing by introducing organic honey powder lines. This trend presents opportunities for manufacturers to target premium segments and cater to health-focused buyers willing to pay higher prices for certified organic ingredients, thus enhancing margins and brand loyalty.

- For instance, Woodland Foods expanding its organic honey powder portfolio by releasing six new certified organic honey powder SKUs in the past 18

Digitalization and E-commerce Growth

The proliferation of digital platforms and e-commerce channels is transforming market access and consumer engagement. More producers and suppliers are leveraging online marketplaces to reach a wider audience, offer direct-to-consumer sales, and provide product information transparency. This trend creates new growth avenues for small and mid-sized players, reducing entry barriers and increasing the accessibility of honey powder products nationwide.

- For instance, Z Natural Foods reported that it processed over 60,000 direct online orders for honey powder products through its website and major e-commerce platforms during the 2023 calendar year

Key Challenges

Volatility in Raw Honey Supply and Pricing

Fluctuating availability and cost of raw honey pose a significant challenge for honey powder manufacturers. Adverse weather, disease, and environmental factors can disrupt honey production, causing supply shortages and price spikes. These uncertainties complicate procurement strategies and affect profitability, requiring market participants to develop more resilient supply chains and risk management practices.

Competition from Alternative Sweeteners

The U.S. Honey Powder market faces strong competition from a broad array of natural and artificial sweeteners, including stevia, agave, and monk fruit. These alternatives often offer different functional properties and price points, influencing manufacturer decisions and consumer preferences. Sustaining market share requires continuous product innovation, clear communication of honey powder’s benefits, and competitive pricing strategies.

Stringent Regulatory and Certification Requirements

Meeting stringent regulatory standards and obtaining necessary certifications, especially for organic honey powder, present hurdles for market players. Compliance with food safety, labeling, and quality assurance regulations can increase operational costs and extend time-to-market for new products. Navigating these complexities is critical for successful market participation, particularly for companies seeking to access premium and export-oriented segments.

Regional Analysis

Western United States

The Western United States holds the largest share in the U.S. Honey Powder market, contributing approximately 34% of the total market value. In 2018, the market size in this region stood at USD 64.3 million. The region benefits from a strong presence of natural and organic product manufacturers, driving higher demand for both organic and conventional honey powder. Organic honey powder in the West demonstrates a robust CAGR of 3.83%, outpacing conventional products, supported by consumers’ preference for clean-label ingredients and sustainable sourcing.

Midwestern United States

The Midwestern United States accounts for roughly 28% market share in the U.S. Honey Powder market, with a 2018 value estimated at USD 53.0 million. The region’s established food processing sector is a key driver for honey powder consumption, particularly in bakery and snack products. Conventional honey powder remains dominant, with a CAGR of 3.10%, as large-scale manufacturers prioritize cost efficiency. However, the organic segment is gaining traction, supported by rising health consciousness and demand for natural sweeteners across Midwestern states.

Southern United States

Representing about 23% of the U.S. Honey Powder market, the Southern United States registered a market size of USD 43.5 million in 2018. The region’s growth is fueled by the expanding food and beverage industry and increasing popularity of nutraceuticals. Conventional honey powder continues to lead, but organic variants are seeing accelerated adoption, supported by a CAGR of 3.83%. Southern consumers’ growing awareness of healthy living and interest in value-added products support market expansion across both product types.

Northeastern United States

The Northeastern United States captures nearly 15% of the market, with a 2018 market value of USD 28.4 million. This region is characterized by a strong inclination toward organic and premium food products, contributing to a higher CAGR of 3.83% for organic honey powder compared to conventional types. The market benefits from dense urban populations and demand from gourmet and specialty food manufacturers. While conventional honey powder maintains steady growth, organic options are rapidly gaining share in the Northeast’s dynamic and health-conscious market.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Market Segmentations:

By Product Type

By Application

- Food & Beverages

- Beauty and Personal Care

- Nutraceutical

- Others

By Sales Channel

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The U.S. Honey Powder market reflects a highly competitive landscape, shaped by multinational ingredient giants and specialized regional producers. Leading global players: Cargill (approximately 15% market share), ADM (12%), and Nestlé—collectively command around 40% of the market, leveraging extensive distribution networks, broad product portfolios, and deep R&D capabilities. These firms continuously invest in capacity expansion and value-chain integration to support rising demand. Companies compete on the basis of product purity, adherence to clean-label standards, and the ability to offer organic and functional variants. Strategic moves such as expanding production capacity, investing in research and development, and securing certifications have become common as firms seek to strengthen their presence. The market also benefits from an evolving supply chain and growing demand across food, nutraceutical, and personal care applications, encouraging continuous improvement and adaptation among market participants.

Key Player Analysis

- Imperial Sugar Company

- Lamex Food Group Limited

- Archer Daniels Midland Company

- Nestlé

- Domino Specialty Ingredients

- AmTech Ingredients

- Z Natural Foods

- Woodland Foods

- Augason Farms

- NOW Foods

Recent Developments

- In December 2024, Aldi introduced a new range of snacks featuring hot honey, a flavor trend popularized on TikTok. Priced at £1.49, the range includes items like Hot Honey Flatbreads, Greek Feta and hot honey bites, Hot Honey Pork Belly bites, and Honey, Chilli, and Camembert crisps. Additionally, Aldi collaborated with Sauce Shop to create a Spiced Cranberry Hot Honey Sauce for the festive season.

- In November 2024, Topgam introduced Hanumam, which is a line of honey-based gum doses, started locally characterized by a high dose of liquid honey in Israel. This product differs by using liquid honey instead of powder shapes and appeals to health -conscious consumers in search of natural ingredients.

- In October 2024, Nespresso launched its first ready for drink coffee, Measant Origins Columbia, Colombia with high quality coffee beans with honey from Colombia. This limited-Setsrit drink starts from October 2, 2024, the United States available in, which was in line with the commitment to the functionality and stability of Nesspresso.

- In 2023, Belize Sugar Industries (BSI) successfully attained recertification with zero non-conformities, following an external audit against the updated ProTerra Standard. Compliance with 80% of all indicators, including core ones, is essential for ProTerra certification. This achievement underscores BSI’s commitment to meeting stringent sustainability criteria and maintaining high operational standards.

- In August 2023, the New Zealand Olympic Committee revealed that Mānuka Pharm had been designated as the official honey partner of the New Zealand Team. Mānuka Pharm leveraged this partnership to promote its unique offerings.

Market Concentration & Characteristics

The U.S. HONEY POWDER Market demonstrates moderate concentration, with a handful of prominent players such as Cargill, ADM, and Nestlé holding a significant share, while numerous regional and niche firms contribute to competitive diversity. It features a dynamic environment shaped by innovation in product formulation, certification standards, and clean-label initiatives. Leading companies leverage large-scale manufacturing capabilities, integrated supply chains, and established distribution networks to secure their market positions. The market displays strong consumer orientation toward natural sweeteners, functional ingredients, and organic variants, which encourages ongoing investment in research and product development. Entry barriers remain moderate due to the need for compliance with food safety regulations, consistent quality, and certification requirements. It experiences steady demand from food, beverage, nutraceutical, and personal care sectors, with conventional honey powder leading due to its cost-effectiveness and versatility. Regional variations in demand and preferences influence supply strategies and drive targeted product offerings.

Report Coverage

The research report offers an in-depth analysis based on Product Type, Application, Sales Channel and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Producers will expand organic honey powder offerings to meet rising demand for clean-label and natural products.

- Manufacturers will invest in traceability systems to enhance product transparency and consumer trust.

- Formulators will incorporate honey powder into functional foods and nutraceuticals for added health benefits.

- The online channel will gain importance as e-commerce platforms reach wider audiences and niche markets.

- Supply chains will diversify to reduce reliance on raw honey from traditional sources and mitigate price volatility.

- Certification standards, such as non-GMO and fair trade, will become more widespread across the value chain.

- Manufacturers will pursue strategic partnerships and acquisitions to accelerate capacity expansion and market reach.

- Innovation in flavor-infused and blend products will increase to support food, beverage, and personal care applications.

- Demand will grow in personal care and cosmetics as formulators leverage honey powder’s antimicrobial and moisturizing properties.

- Regional producers will tailor their product portfolios to address local consumer preferences and regulatory requirements.